Venture Studio vs Venture Capital: Models, Careers, and How to Choose

Venture studios build companies; VC firms select and fund them. Compare the models, daily work, incentives, career paths, and diligence questions that matter before you join one.

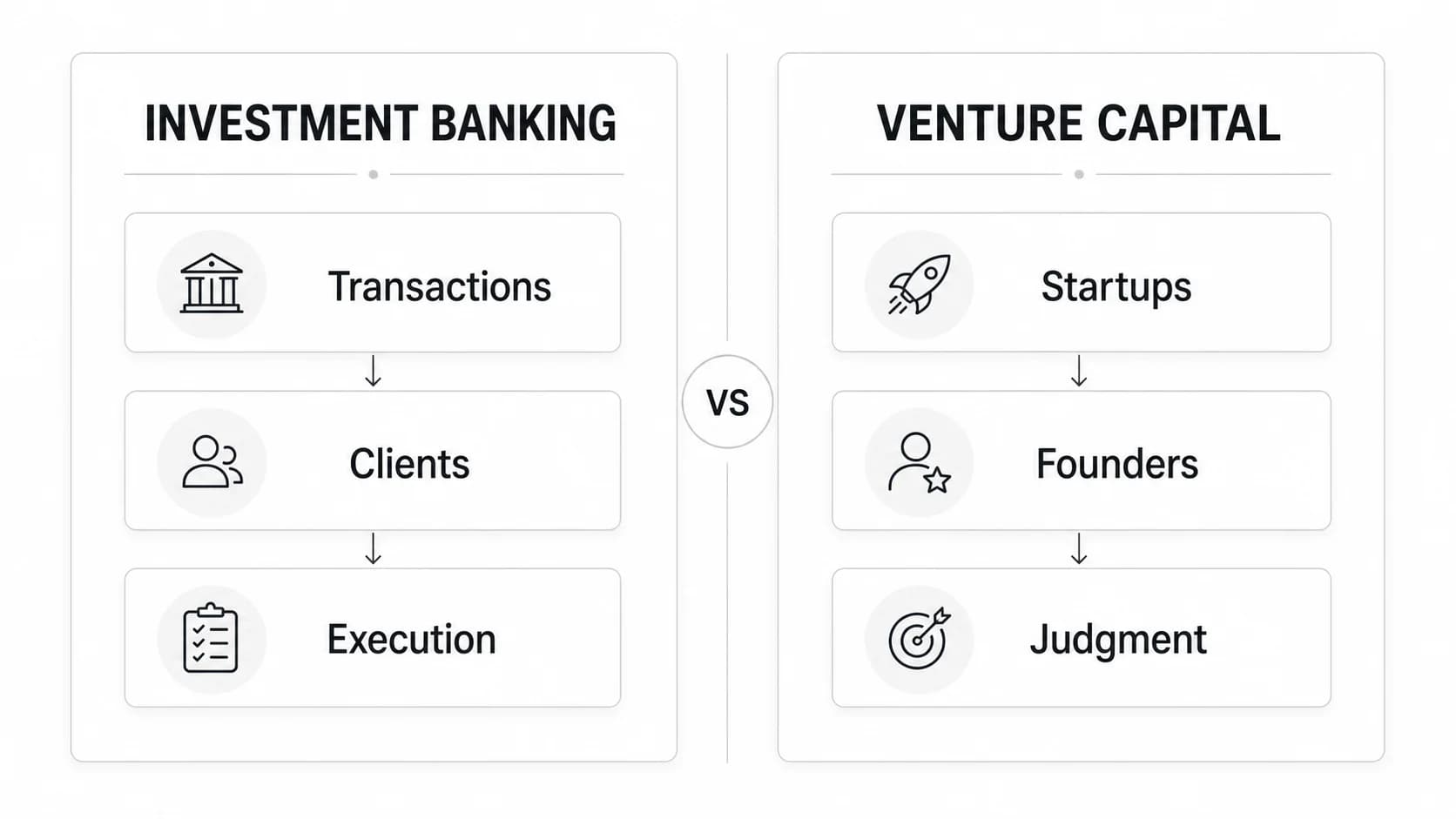

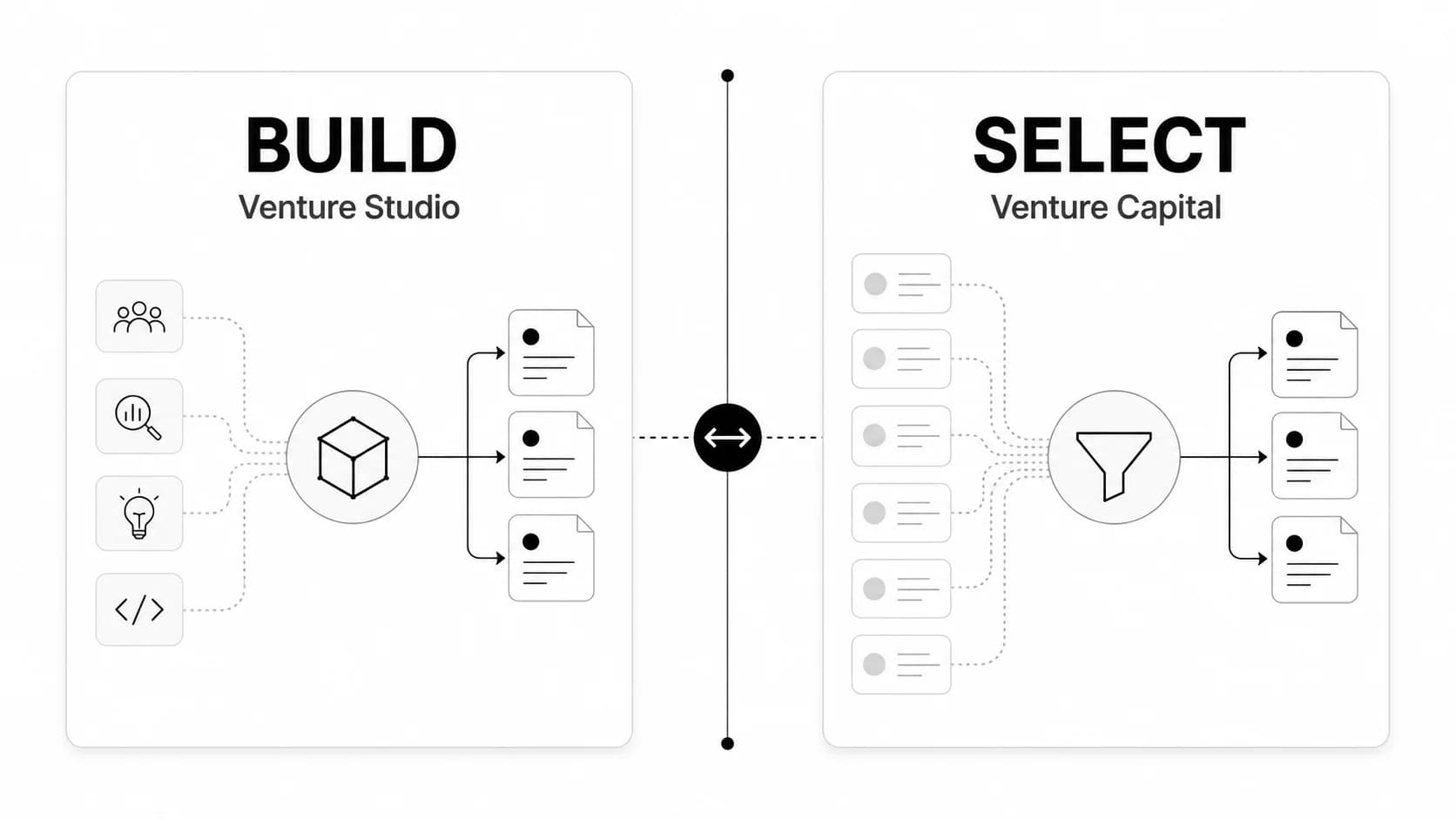

A venture studio builds companies; a venture capital firm selects and funds companies that already exist. That difference changes almost everything about the work. Studio teams spend more time on ideation, customer discovery, product formation, and recruiting founders. VC teams spend more time sourcing, diligence, investment decisions, portfolio construction, and board-level support.

The labels are not reliable on their own. Some studios run dedicated funds. Some VC firms incubate companies. Corporate venture builders may combine a parent company's assets with external capital. Before you compare two employers or financing offers, ask four questions: Where do ideas originate? Who supplies the build team? Where does the capital come from? Who has decision authority?

Venture studio vs venture capital at a glance

| Dimension | Venture studio | Venture capital firm |

|---|---|---|

| Core job | Create and launch companies | Select and finance companies |

| Starting point | A problem, thesis, technology, or internally generated idea | An existing founder, team, product, or company |

| Primary work | Validation, product, founding-team recruitment, company formation, early go-to-market | Sourcing, screening, diligence, investment committee, portfolio support |

| Capital | Studio balance sheet, dedicated studio fund, corporate sponsor, or outside investors | Pooled fund capital from limited partners |

| Decision cadence | Frequent build, pivot, and kill decisions | Fewer investment decisions followed by long holding periods |

| Ownership logic | Reflects capital plus contributed idea, team, services, and operating risk | Reflects capital invested at an agreed valuation and round terms |

| Portfolio model | Fewer companies with deeper operating involvement | More companies with selective board, network, and platform support |

| Feedback loop | Customer behavior, product progress, team formation, and launch milestones | Deal access, investment judgment, portfolio progress, and eventual returns |

| Common roles | EIR, venture architect, venture builder, product, growth, talent, finance | Analyst, associate, principal, partner, platform, operating partner |

| Best fit | Zero-to-one operators who want to build repeatedly | Investors who want to choose, underwrite, and support a portfolio |

The simple shorthand is build versus select. It is useful, but incomplete. A studio still makes investment decisions, and a modern VC firm may provide substantial recruiting, go-to-market, and operational help. The important distinction is whether company creation is the firm's repeatable product or whether investment selection is.

The models are built around different questions

A venture studio asks: what should we build?

A studio begins upstream of a conventional fund. Its team may develop a sector thesis, interview customers, test a workflow, recruit an entrepreneur in residence, and fund the first product experiments. The studio is not merely advising a founder. It is helping assemble the company.

That model demands a repeatable formation system: opportunity selection, validation standards, access to design and engineering, founder recruitment, legal formation, capital allocation, and rules for stopping weak concepts. Alloy Partners' comparison describes this as acting more like a co-founder than a financial backer. Treat that as an operator's framing, then verify how a specific studio actually behaves.

A VC firm asks: which existing company should we back?

A traditional VC firm starts with an external market of founders and companies. The team builds a network, sources opportunities, tests an investment thesis, conducts diligence, negotiates terms, and decides which businesses deserve a place in the portfolio. After investing, the firm may help with hiring, customers, later fundraising, strategy, and governance.

The fund's repeatable system is selection and portfolio management. Its core artifacts include sourcing notes, market maps, diligence work, investment memos, ownership analysis, reserve plans, board materials, and LP reporting. If you need a broader primer, how venture capital works explains the fund cycle.

Hybrids make the label unreliable

There are at least four common hybrids:

- A studio that forms companies and invests through a dedicated fund.

- A VC fund that incubates one or two companies alongside its main portfolio.

- A corporate venture builder that uses distribution, data, IP, or domain experts from a parent company.

- An accelerator or incubator that adds follow-on capital but does not originate companies.

VC Lab's research on competing fund types shows why the hybrid can be operationally demanding: a team may be running a company-creation engine while also raising and managing a fund. The VC Lab analysis is fund-formation evidence, not proof that one model produces better companies.

Use the four-question test instead of trusting the brand name:

- Idea source: Does the firm originate concepts or accept founder pitches?

- Build resources: Does it supply dedicated product, growth, recruiting, finance, or engineering capacity?

- Capital source: Is money coming from a fund, corporate sponsor, studio balance sheet, or a mix?

- Decision authority: Who can approve a build, stop it, appoint leadership, or authorize the next financing?

Those answers tell you more about the job and incentives than “studio,” “builder,” or “ventures” in the company name.

How the daily work differs

The cleanest career comparison is not “operator versus investor.” It is the type of uncertainty you are paid to reduce.

A studio team reduces company-formation uncertainty. Does the problem matter? Can the team build a credible product? Who should lead the company? Which channel can produce the first evidence of demand? A VC team reduces investment-selection uncertainty. Is this company unusually strong? Can it become large enough for the fund? What must be true for the deal to work? Is the price and ownership attractive?

Imagine one week in each role.

| Day | Studio team | VC team |

|---|---|---|

| Monday | Review customer interviews and decide which assumption to test next | Review pipeline and prioritize founder meetings |

| Tuesday | Write a validation brief and scope a prototype | Build a market map and prepare diligence questions |

| Wednesday | Interview an EIR or potential founding executive | Meet a founder and reference customers or experts |

| Thursday | Review product evidence, channel tests, and formation budget | Draft an investment memo and model ownership scenarios |

| Friday | Make a build, pivot, pause, or kill recommendation | Debate the opportunity in investment committee and plan follow-up |

The studio's output is closer to an operating decision: a tested insight, a product requirement, a founder match, a launch plan, or a reason to stop. The VC output is closer to an allocation decision: a sourced opportunity, a diligence conclusion, a term-sheet view, an investment recommendation, or a portfolio action.

The feedback loops also feel different. Studio work can produce evidence within days, but that evidence is noisy and the team may kill months of work. VC work has a faster yes/no decision on a deal, but the quality of the investment may remain uncertain for years. Choose the model whose uncertainty you can tolerate, not the one with the more fashionable title.

Role titles do not translate one-for-one

| Role | Typical mandate | Closest role in the other model | Important difference |

|---|---|---|---|

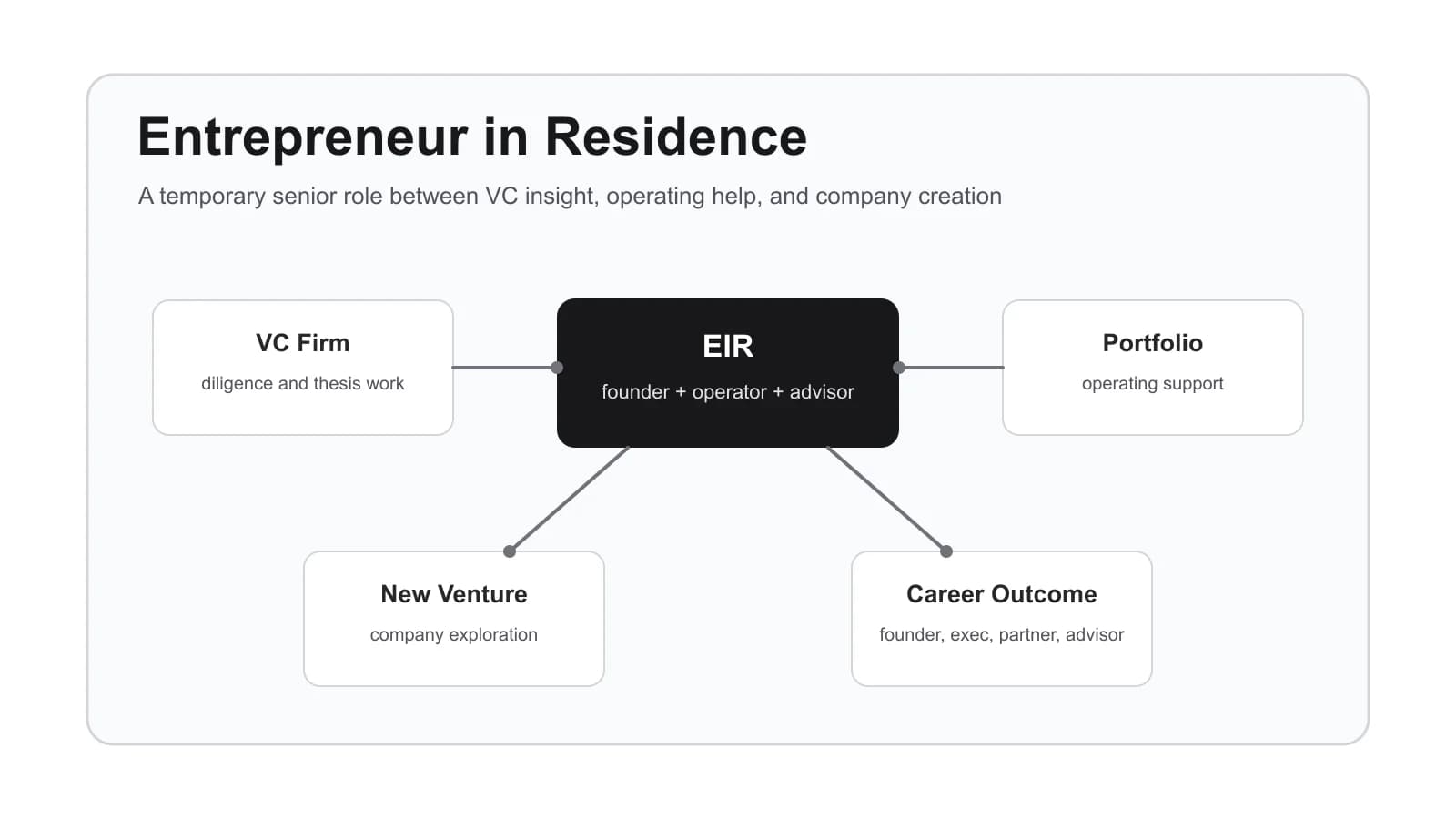

| Entrepreneur in residence | Explore a thesis and potentially lead a new company | Founder-in-residence or sector expert at a fund | The studio may expect company formation; a fund may use the role for sourcing or thesis work. |

| Venture architect / venture builder | Turn an opportunity into a validated company plan | No exact equivalent; parts resemble associate, product, and platform work | Owns experiments and formation work rather than only evaluating external companies. |

| Studio operator | Manage several builds, resources, and stage gates | Principal or portfolio/operating leader | Allocates operating resources across builds, not only investment capital. |

| Shared product, talent, growth, or finance specialist | Support multiple studio companies during formation | VC platform professional | Often executes inside a company rather than advising an independent portfolio team. |

| VC analyst or associate | Source, research, diligence, model, and write recommendations | Junior venture builder | Evaluates founders and markets but usually does not own product formation. |

| VC principal or partner | Lead deals, make or influence investment decisions, support portfolio, raise funds | Studio managing director or venture partner | Owns portfolio and LP outcomes; studio leaders also own the build system. |

| VC platform professional | Help portfolio companies with talent, go-to-market, community, or operations | Shared studio specialist | Platform support begins after investment; studio support may start before the company exists. |

An entrepreneur in residence can sit in either environment, and a VC platform role can look operational. Do not infer scope from the title. Ask:

- What must I deliver in the first 90 days?

- How many companies or concepts will I cover at once?

- Can I make build, investment, hiring, or budget decisions?

- Am I executing work, advising teams, or preparing recommendations?

- How is success measured before a company has raised or exited?

- Is compensation tied to salary, fund carry, studio equity, company equity, or a mix?

If the interviewer cannot answer those questions clearly, the role may be undefined rather than merely broad.

Skills and career paths

Both models reward market judgment, clear writing, founder assessment, and relationship building. They build those skills through different repetitions.

What a studio teaches

- Zero-to-one product judgment: turning an uncertain problem into a testable proposition.

- Customer discovery: separating polite interest from evidence that someone will change behavior or pay.

- Cross-functional execution: moving between product, recruiting, finance, legal formation, and go-to-market.

- Founder matching: judging whether a potential leader fits the opportunity and the studio relationship.

- Kill discipline: stopping a concept when the evidence no longer supports additional time or capital.

Strong studio experience can lead to founding a company, joining a startup, leading innovation, operating another studio, moving into corporate development, or taking an operating/platform role at a fund. The strongest proof is not the number of ideas touched. It is evidence that you improved decisions: experiments designed, assumptions retired, founders recruited, products launched, or weak concepts stopped early.

What a VC firm teaches

- Sourcing judgment: developing a credible network and recognizing unusual companies before a process becomes competitive.

- Investment analysis: testing team, market, product, traction, defensibility, price, and fund fit.

- Memo and decision writing: compressing uncertainty into a recommendation others can challenge.

- Portfolio thinking: understanding ownership, reserves, concentration, follow-ons, and opportunity cost.

- Long-duration relationship work: supporting founders through financing, hiring, governance, and difficult moments.

Traditional paths often progress from analyst or associate to principal and partner, although titles and promotion models vary. The Venture Capital Careers career-path guide explains the investment-team ladder in more detail.

Switching between the models

A studio-to-VC move is plausible when you can show that operating work improved investment judgment. Translate experiments into thesis evidence, explain why a market became investable, and demonstrate that you can compare an opportunity with alternatives rather than advocate only for the company you built.

A VC-to-studio move is plausible when you can show execution, not only analysis. A polished memo does not prove that you can recruit a founding team, run customer discovery, ship a prototype, or manage a kill decision. Build evidence through a portfolio project, founder support, an EIR sprint, or direct operating work.

Candidates coming from startups face the same choice. Moving from a startup operator to venture capital trades depth inside one company for breadth across many. A studio can be a middle path: repeated company formation with more operating ownership than a conventional investment role.

A two-week work-sample test

Do both assignments before you commit to a path.

Studio track

Pick a narrow customer problem. Conduct five structured conversations, write the strongest evidence for and against the problem, define one cheap validation experiment, and finish with a one-page build/pivot/stop recommendation.

VC track

Map a narrow market, identify ten relevant companies, choose one, write five decisive diligence questions, and finish with a one-page invest/pass/watch recommendation that explains fund fit and the key disconfirming evidence.

Then compare your energy and judgment:

| Signal | Studio fit | VC fit |

|---|---|---|

| You wanted to keep changing the proposition and test | strong | neutral |

| You wanted to compare more companies before choosing | neutral | strong |

| Recruiting a founder or operator felt central | strong | moderate |

| Portfolio and opportunity-cost questions felt central | moderate | strong |

| A fast kill decision felt satisfying | strong | moderate |

| A defensible investment recommendation felt satisfying | moderate | strong |

The test is not a hiring credential by itself. It reveals which work loop you are more likely to sustain: building evidence inside a company or selecting among companies.

The economics change the incentives

A VC firm usually buys preferred shares in an existing company at a negotiated valuation. A venture studio may contribute cash and the initial thesis, research, product work, recruiting, shared services, and team time. It may receive common equity for company creation, preferred equity for invested cash, service fees, or some combination.

That is why “How much equity does a studio take?” has no useful universal answer. The percentage matters, but so do the contributions, security types, governance rights, option pool, vesting, and future financing plan. Two studios with the same headline ownership can create very different incentives.

Separate the pieces:

| Component | What to understand | Why it matters |

|---|---|---|

| Common equity | Who receives founder-like ownership, on what vesting schedule, and for which contribution | Determines long-term upside and whether ownership follows continued work |

| Preferred capital | How much cash is invested and with what liquidation, conversion, and protective terms | Affects proceeds and control in future financings or exits |

| Founder/EIR allocation | What the operating leader owns at formation and after expected dilution | Tests whether the person carrying execution risk has durable motivation |

| Option pool | How much capacity exists to hire the early team and who bears the dilution | Reveals whether the company can recruit without immediately reopening the cap table |

| Governance | Board seats, reserved matters, budgets, hiring authority, and kill rights | Determines whether the company can act independently after launch |

| Follow-on rights | Pro-rata rights, internal funding rules, and external-investor access | Shows how the company can finance the next stage |

Studio operators often argue that deeper ownership is justified because the studio acts as a co-founder and creates value before institutional financing. Some investors and founders worry that studio-heavy ownership can weaken the operating team's incentive or make later financing harder. Treat both positions as diligence hypotheses, not universal facts.

Use this rule:

Decision rule: High studio ownership is not automatically a red flag. Unexplained ownership, weak founder incentives, stacked economics, unclear authority, or a cap table that has not been tested with credible follow-on investors are red flags.

For a job candidate, the same principle applies to compensation. “Equity” can mean studio-level ownership, fund carry, company-level options, profit share, or a discretionary grant. Ask which entity issues it, what must happen for it to vest, how dilution works, and whether you participate in one build or the broader portfolio.

These questions are commercial diligence, not legal or tax advice. Founders should have qualified counsel review the actual formation, financing, IP, employment, and equity documents before signing.

Six questions to ask before joining a venture studio or taking its deal

Studio quality varies because the model bundles several promises: insight, talent, product capacity, capital, and follow-on support. Replace those promises with evidence.

| Question | Evidence to request | Strong signal | Red flag |

|---|---|---|---|

| 1. Where do ideas originate? | Thesis process, customer research, IP policy, prior formation examples | Clear rules for external ideas, studio ideas, and pre-existing IP | Ownership is claimed before contributions or IP boundaries are defined |

| 2. What resources are committed? | Named team, allocation, budget, service scope, duration | Dedicated people and time tied to formation milestones | A logo wall or advisor network substitutes for committed execution capacity |

| 3. Who makes decisions? | Governance map, stage gates, budget authority, founder hiring/firing rights | Explicit build, pivot, stop, hiring, and financing authority | The operating founder is accountable without meaningful authority |

| 4. How are the economics structured? | Formation cap table, security types, vesting, option pool, fees, dilution examples | Contributions and risks map visibly to ownership and control | Stacked fees and equity are difficult to explain or model |

| 5. How does follow-on financing work? | Prior rounds, investor references, reserve policy, pro-rata terms, fundraising responsibility | External investors have financed prior companies on workable terms | The model depends entirely on uncommitted internal funding |

| 6. What happens after launch? | Transition plan, shared-service terms, founder autonomy, team incentives, studio board role | The company gains independence without losing critical support overnight | Roles, IP, staff, or incentives become ambiguous once the company is formed |

Score each answer from zero to two:

- 0 — claim only: no document, owner, example, or reference supports the answer.

- 1 — partial evidence: the process exists but responsibilities or economics remain unclear.

- 2 — verified: documents, named owners, prior-company evidence, and references align.

The total is less important than the pattern. A studio can be early and have few exits, but it should still be able to document who does the work, who decides, and how incentives remain aligned. A high score on brand, network, or senior advisors does not compensate for a zero on economics or decision rights.

Candidates should run the same scorecard on a role. Replace “founder” with “employee” and request the 90-day outcomes, reporting line, decision rights, project allocation, and exact equity or carry instrument. If the role spans both studio operations and a fund, ask how time and performance are measured across the two systems.

Which model fits you?

Choose a venture studio when you want to operate repeatedly at the point where a company is least defined. You should enjoy customer discovery, incomplete teams, product ambiguity, short experiment cycles, and the possibility that disciplined work ends with a decision not to build.

Choose a VC firm when you want to compare companies, develop an investment thesis, build founder relationships, make allocation decisions, and support a portfolio over a long horizon. You should enjoy saying no frequently, defending recommendations, and living with delayed feedback.

Neither model is inherently more entrepreneurial. A studio can become bureaucratic if stage gates replace judgment. A VC firm can be deeply operational if partners and platform teams work closely with founders. Diligence the actual work:

| If you prefer... | Lean studio | Lean VC |

|---|---|---|

| Building one proposition until evidence changes it | ✓ | |

| Comparing many companies against a thesis | ✓ | |

| Recruiting a founding team and shaping product scope | ✓ | |

| Negotiating an investment and ownership position | ✓ | |

| Fast operating feedback and frequent kill decisions | ✓ | |

| Long relationships and portfolio-level tradeoffs | ✓ | |

| Company-level equity and formation responsibility | ✓ | |

| Fund carry and investment-decision responsibility | ✓ |

How to research firms and roles

Start with the firm's own portfolio and team pages, then verify the model through evidence.

- Classify the firm. Use the Venture Capital Careers companies directory to build a shortlist, then record where ideas originate, how companies enter the portfolio, and whether the firm has a separate fund.

- Inspect formation evidence. For a studio, look for companies formed from internal theses, named founding teams, launch dates, and evidence of external financing. For a VC firm, look for investment stage, check size, sector focus, portfolio, exits, and team track record.

- Read roles for outputs. Ignore broad phrases such as “wear many hats.” Identify the first 90-day deliverables, number of companies covered, manager, budget or investment authority, and expected split between analysis and execution.

- Map the incentive instrument. Ask whether the role includes salary, bonus, company options, studio equity, fund carry, or a combination. Confirm which entity grants it and what performance unlocks it.

- Compare live work. Browse open roles on Venture Capital Careers and compare investment, platform, EIR, product, growth, and venture-building positions. Link titles back to the actual mandate instead of assuming they are standardized.

For studio roles, strong job descriptions name the build stage, functional ownership, portfolio load, decision rights, and equity context. For VC roles, they name sourcing expectations, diligence responsibility, sector or stage, investment-committee exposure, portfolio work, and promotion logic.

The best interview question is the same in both models: What decision will I be trusted to improve, and what evidence will prove I improved it? A clear answer reveals the real job.

Frequently asked questions

Is a venture studio the same as a VC fund?

No. A venture studio is an operating model for creating companies. A VC fund is a pool of capital used to invest in companies. A studio may manage a fund, and a VC firm may run an incubation program, but the two functions remain distinct. Ask where ideas originate, who builds, where capital comes from, and who decides.

Is a venture studio a good place to start a VC career?

It can be a strong route into venture work, especially for candidates who want market research, founder assessment, validation, and portfolio exposure. It is not automatically training for an investment role. To move into a traditional VC firm, you will need to translate operating evidence into sourcing, comparative judgment, investment writing, and fund-level thinking.

Do venture studios take more equity than VC firms?

Studios often seek founder-like ownership because they may contribute the idea, team, product work, services, and initial capital. A VC firm normally buys a minority stake in an existing company at a negotiated valuation. Do not compare percentages without comparing the contribution, security type, vesting, option pool, governance rights, and expected dilution.

Can a studio-backed company raise from traditional VCs?

Yes, many do. The practical question is whether the founding team remains motivated, the cap table has room for employees and new investors, governance is workable, IP is clean, and the studio can provide credible references from later financing rounds. Ask for actual examples and investor references.

Can you move from a venture studio to a VC firm?

Yes. The most transferable evidence includes market mapping, founder assessment, thesis development, written recommendations, portfolio exposure, and clear decisions under uncertainty. Strengthen the move by showing that you can compare multiple companies and opportunities, not only advocate for a build you helped create.

Choose the operating model, not the label

Venture studios and VC firms both deploy capital and judgment around startups, but their central products differ. A studio repeatedly forms companies. A VC firm repeatedly selects investments. The work, incentives, career evidence, and failure modes follow from that distinction.

Classify a prospective firm using the four-question model test, then run the six-question diligence scorecard. If the answers are clear, compare the actual role with the work loop you prefer: building evidence inside a company or selecting among companies. Your next step is to shortlist firms and test the model in interviews.