Venture Capital Career Path: Roles, Pay, and How to Choose Your Entry Point

How the VC career ladder works—from analyst to partner—with pay ranges, day-to-day role duties, and a framework to pick the right entry path for your background.

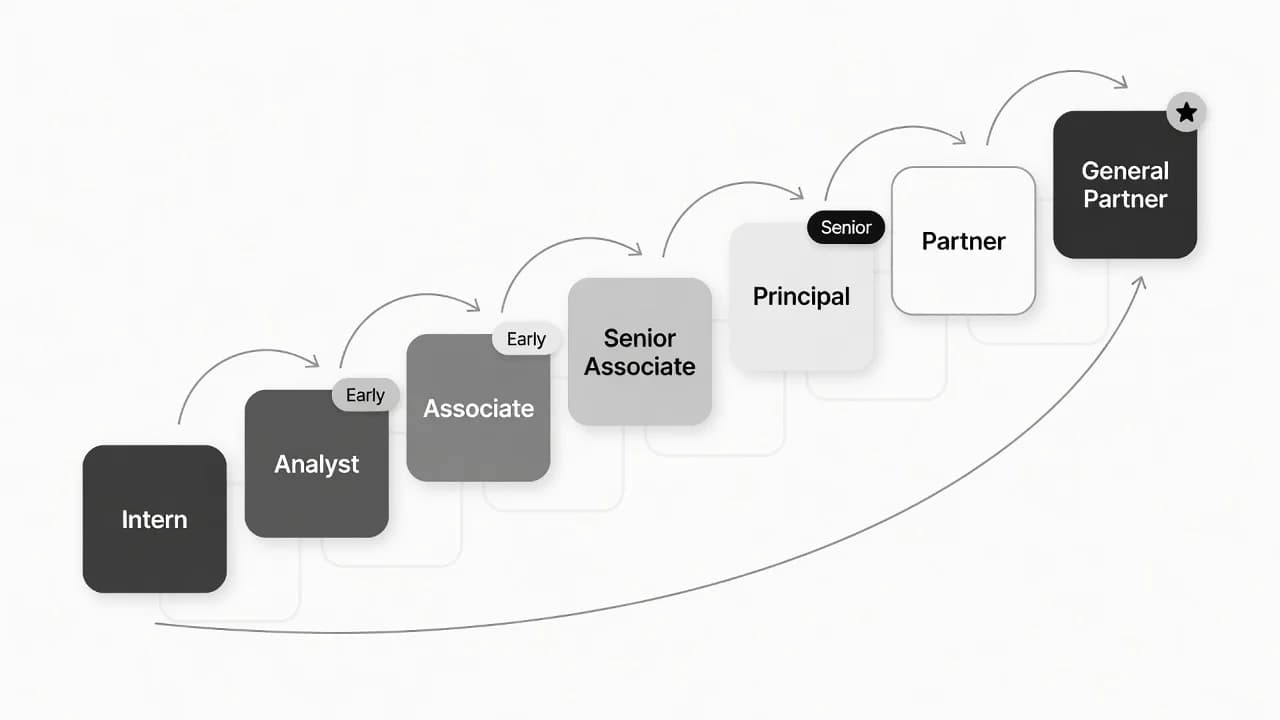

The venture capital career path runs from analyst or intern at the bottom to partner or general partner at the top. Between those poles sit associate, senior associate, and principal roles that carry more deal ownership, board exposure, and carried interest as you move up.

That ladder is real, but the path into venture capital is not linear. Most firms hire through networks, not job boards. Many analyst and associate seats are two-year programs, not default partner tracks. Compensation at the junior end is mostly cash; carry only becomes meaningful at principal level and above for most people.

If you are weighing venture capital roles, start with two questions: which entry point matches your background today, and what you want this job to set up over the next five years—not whether you can memorize a title hierarchy.

How the venture capital career ladder works

At a typical institutional fund, investment professionals progress through a layered hierarchy. Titles vary by firm size, geography, and stage focus, but the underlying work changes in predictable ways: more sourcing autonomy, more time on boards, more weight in investment committee decisions, and more economics tied to fund performance.

Typical progression: Intern → Analyst → Associate → Senior Associate → Principal → Partner → General Partner (titles and tenure vary by fund size and stage).

At mega-funds, titles tend to be more standardized and promotion timelines more structured. At seed-stage and emerging managers, the same person may draft a memo, join a founder call, and sit in a partner meeting in the same week. Partners at smaller firms often step into analyst-level work when the team is thin.

Analyst and intern roles

The analyst role is the most common entry point for people joining a fund directly out of college or with one to two years of experience. Analysts source deals, map markets, build models, and write investment memos that senior investors use to decide whether to take a meeting or pass. See the venture capital analyst job description for a full duties breakdown.

Hugh Bowen, an analyst at SOSV, described a typical week split roughly as 40% ad-hoc tasks, 40% research, and 20% networking and personal development. Ad-hoc work can mean sitting in on portfolio board meetings as an observer, drafting LP update materials, or pulling competitive intel for a live deal. Research time goes to sector deep dives and outbound sourcing. The remaining slice is conferences, events, and building the relationships that eventually produce deal flow.

Most analyst programs at larger U.S. funds run two years, similar in spirit to investment banking analyst programs. Union Square Ventures reopened its analyst program for 2026: two hires, a fixed two-year term, full investment-team participation, and applications due June 14, 2026. That kind of structured opening is still the exception—most funds hire one-off when a partner leaves or a new fund closes—but it signals that top firms continue to use analysts as a deliberate pipeline, not a permanent junior class.

Internships, usually 10–12 weeks in the summer, are the other common entry ramp. They mirror analyst work at a lighter scope and often feed full-time analyst offers.

Associate and senior associate

Associates are the deal-execution layer at most funds. They run diligence processes, lead reference calls, build valuations, write the memos that go to the partnership, and often become the day-to-day contact for founders after a round closes. The venture capital associate job description spells out typical responsibilities in more detail.

There is an important split between pre-MBA and post-MBA associates. Pre-MBA associates often arrive from investment banking, consulting, or operating roles at startups. Post-MBA associates are more frequently on a partnership trajectory at larger firms, with more external visibility and early carry allocations at some shops.

At the associate level, you are also a gatekeeper. Balderton partner Suranga Chandratillake has described associates as the first filter on inbound companies—the people who decide which meetings reach principals and partners. That means relationship quality matters as much as spreadsheet skill.

Senior associates begin sourcing and leading processes with less hand-holding. They may take board observer seats and start developing a sector thesis that will define whether they advance to principal or rotate out.

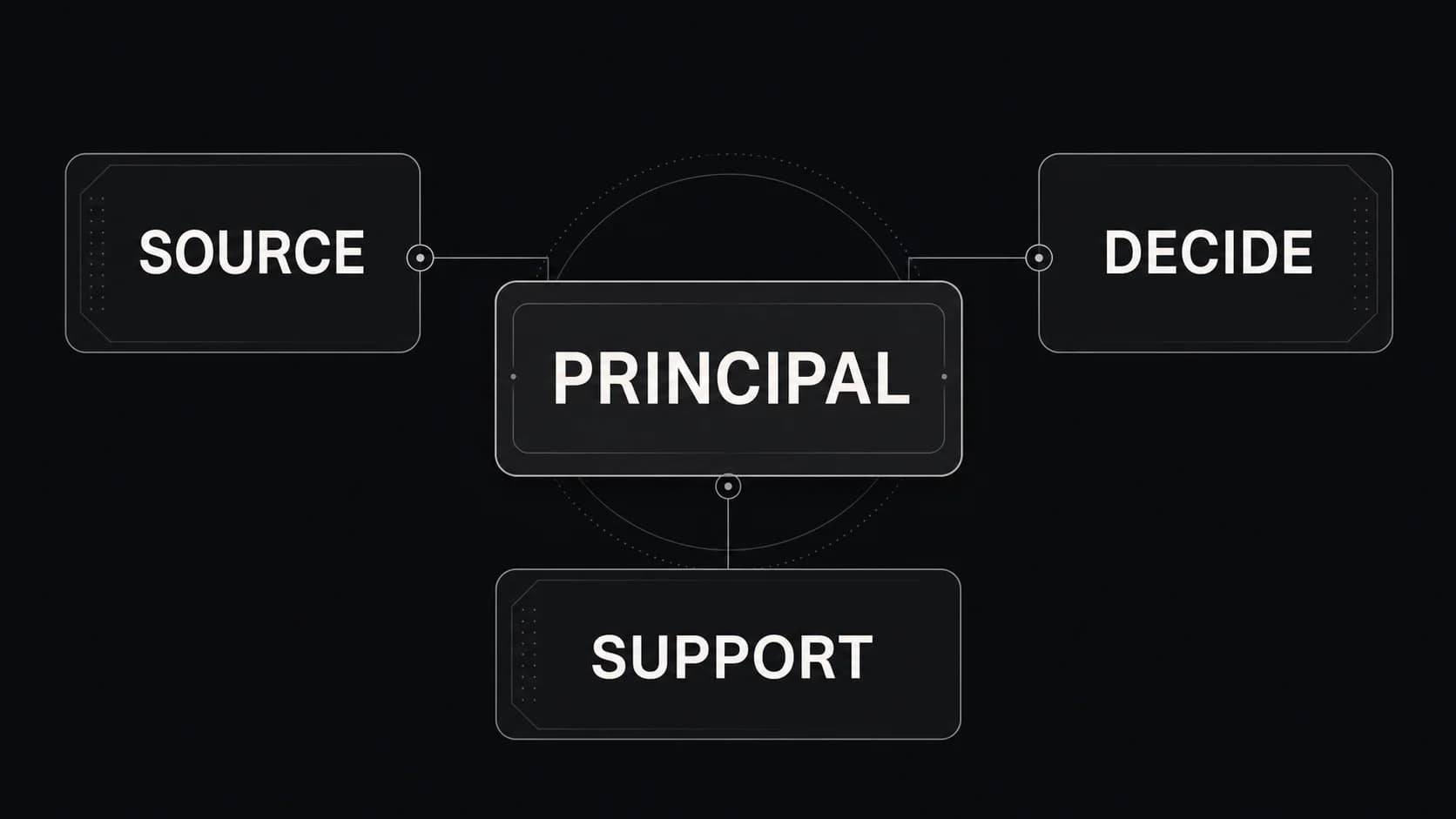

Principal and vice president

Principal (sometimes VP or director) is the first senior investment seat at many firms. Principals lead deals end-to-end, negotiate term sheets, sit on portfolio boards, and shape sector strategy within the partnership.

This is where compensation shifts toward carried interest as a meaningful wealth driver. Cash comp rises sharply, but the step-change is carry pool participation—often a few percent of the pool at this level at funds that offer it.

Not every principal makes partner. Advancement depends on realized returns on deals you sourced or led, LP relationship skills for future fundraises, and whether the firm needs another GP-level voice in your sector.

Partner and general partner

Partners are the owners and decision-makers at a VC firm. They sponsor deals at partner meetings, raise capital from limited partners, set firm strategy, and carry the reputational weight that founders evaluate when they choose an investor.

Cash compensation at partner level can reach high six or seven figures at established firms, but the economic center of gravity is carry—typically a 20% share of fund profits above a hurdle, allocated across the GP team. A partner with a mid-teens carry percentage in a successful $500M fund can earn multiples of lifetime cash comp from a single vintage. That math explains why the path is competitive; it also explains why most junior hires never see carry at all.

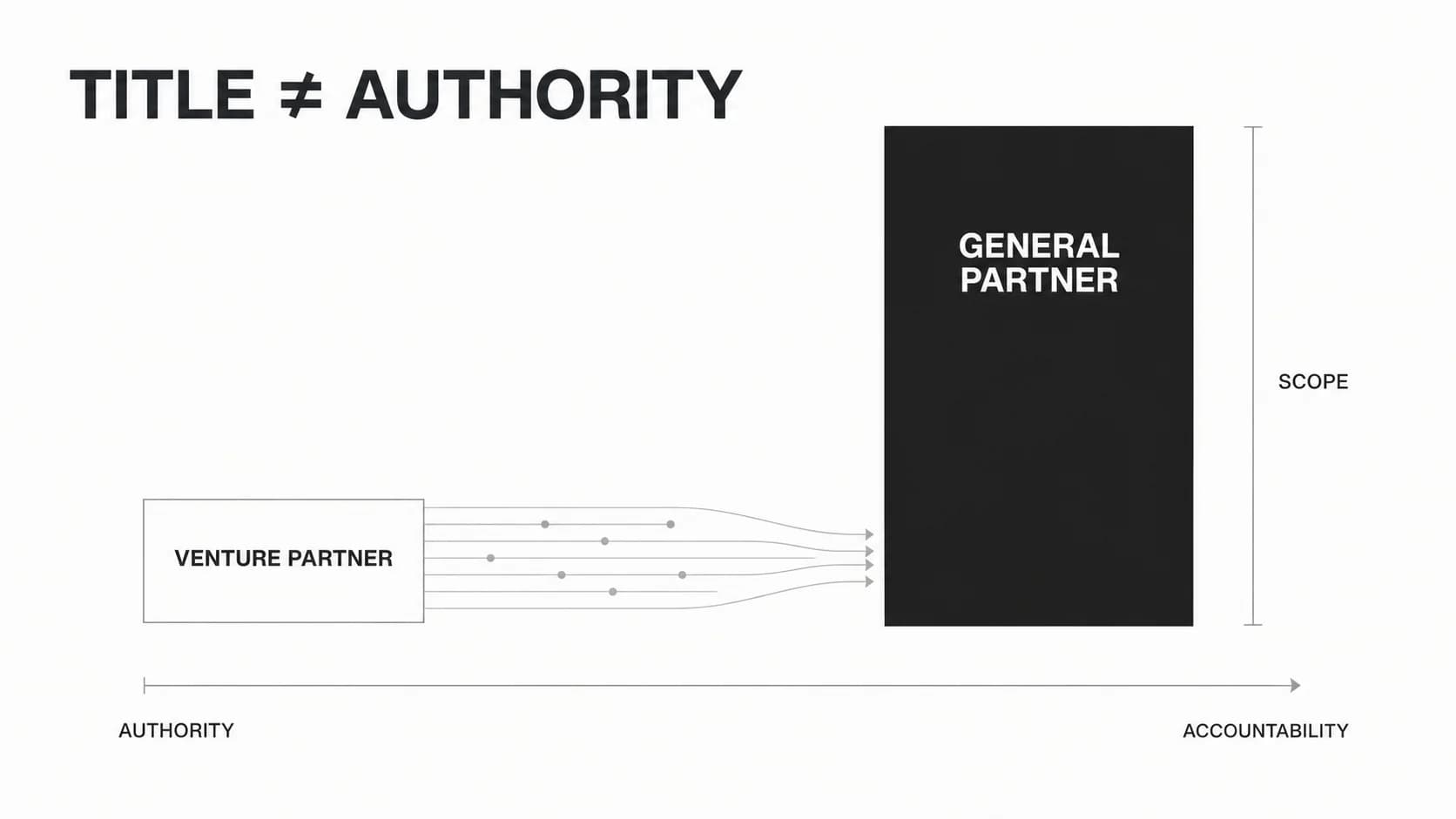

Managing partner or general partner titles usually indicate ownership and final authority over fund strategy and economics.

Entrepreneur in residence

Some firms host entrepreneurs in residence—experienced operators or founders who advise portfolio companies while exploring their next company. EIR roles are often unadvertised, filled through coinvestor relationships or prior founder rapport, and typically run at least six months before a new venture launch.

What venture capital firms actually hire for

Credentials matter on paper. In practice, early-stage firms hire for access and judgment under uncertainty.

Sajith Pai, a partner at Blume Ventures, frames top-tier venture capital as sell-side work, not buy-side asset management. You are distributing your firm's brand of capital to founders in exchange for equity. The hiring bar is therefore less "can you model a cap table" and more "can you earn the trust of sharp founders before your competitors do."

That shows up in interviews and on the job as:

- Relationship velocity — warm intros beat cold outreach; quality of your network matters more than its LinkedIn count

- Taste under sparsity — forming a view when financials are thin and the product is half-built

- Founder empathy without softness — direct feedback that still makes founders want you in the room

Finance skills help, especially at growth-stage funds. At seed and Series A, pattern recognition and founder rapport often dominate. For tactical break-in advice beyond the ladder, read how to get a job in venture capital and how to become a venture capitalist.

Amy Wu Martin, a consumer partner at Menlo Ventures, puts the practical bar even more bluntly: send good deal flow, not coffee chats. Build a founder network, develop a point of view on companies you would back, and earn operating experience where you can—then let that judgment surface in intros and memos, not generic networking volume.

Mike Dauber, a two-decade VC hiring veteran at Amplify Partners, writes that where you start your venture career can make or break the long arc. A prestigious logo on your LinkedIn matters less than whether the fund's stage, sector, and team size let you build attribution and founder relationships that compound.

Which entry path fits your background

Use the paths below as a starting point, not a guarantee. Fund size, sector, and your specific network will move outcomes.

| Background | Typical entry | Realistic 5-year outcome | Best next move |

|---|---|---|---|

| Undergrad + 0–2 yrs (finance/tech) | Analyst or intern | Associate elsewhere, MBA, startup operator, or adjacent fund | Target analyst programs; build a shadow portfolio of companies you would back |

| Investment banking / consulting (pre-MBA) | Pre-MBA associate (less common) or analyst | MBA, associate, portfolio company, or growth equity | Use banking/consulting to learn diligence speed; develop a sector point of view |

| MBA (top program) | Post-MBA associate | Principal track at same fund or lateral to another | Pick fund stage and sector deliberately—post-MBA seats are scarce |

| Startup operator / product / eng | Associate or senior associate | Principal or operating partner path | Join a venture-backed company in a role with founder proximity |

| Successful founder / C-suite | Principal or partner | GP at own fund or senior seat at new fund | Often skips junior ladder entirely |

| Scout / angel / community builder | Part-time scout → analyst/associate | Platform or investing seat | Convert visible deal judgment into warm intros at target funds |

Finance path (IB, PE, consulting)

Investment banking and management consulting remain common feeders because you learn to process volume, build models quickly, and survive ambiguous mandates. They are less magical than a decade ago—several senior VCs have publicly called template finance paths uninspiring on their own—but they still signal you can do the work.

If you are on this path, differentiate with a sector wedge: one market map, one shadow portfolio, one public write-up that shows how you think about investments, not just how you format slides.

Operator and founder path

Stanford GSB professor Ilya Strebulaev's research on 12,627 U.S. venture careers between 1996 and 2025 finds that investors with startup operating experience—especially at venture-backed companies—are more likely to reach senior levels. Experience at failed startups also correlates with promotion, likely because live exposure to what breaks teaches pattern recognition you cannot get from reading.

If your goal is eventual partnership, the data suggests earning operator credibility first, then entering at associate or principal rather than treating a junior analyst seat as the obvious first step.

That does not mean operators should skip venture entirely. It means you should be intentional about level of entry and whether the fund you join will let you lead deals, not only support them.

Pre-MBA analyst path

An analyst role is a strong first exposure to venture if you are early in your career and want to learn how funds source, diligence, and support portfolios. It is a weaker bet if you are already optimizing for partner economics within ten years.

Strebulaev finds junior entrants are 70–80 percentage points less likely to reach senior levels than those who enter at middle levels (principal/VP equivalents), controlling for other factors. Lateral moves to partner elsewhere count in his data; so does founding your own fund.

Treat a two-year analyst program as a structured apprenticeship with a planned exit: another fund, business school, or an operating role at a portfolio company.

Post-MBA associate path

Post-MBA associates at established firms are often the closest thing to a traditional partner track—more carry visibility, more partner facetime, more external representation. Seats are few and heavily networked.

Pick fund stage carefully. Growth funds reward financial fluency; seed funds reward founder access and narrative conviction.

Scout, angel, and adjacent roles

Scout programs and angel syndicates let you show judgment without a full-time offer. The conversion path is demonstrating you can bring founders who want to work with you, not just that you can attend demo days.

Before accepting a venture capital scout role, confirm the mandate, time commitment, attribution rules, feedback cadence, and whether compensation is cash, carry, or neither.

If you are breaking in without a traditional background, Nicole DeTommaso (Harlem Capital) describes a repeatable 2026 playbook: follow target funds, cold-DM junior investors first to build momentum through warm intros, and pitch with a bold deck that shows thesis fit, analysis, and why you specifically—not just why you want "a job in VC."

Partner-track expectations (read this before you apply)

"Partner track" appears in job posts more often than it exists in practice.

Practitioners with years of experience across junior seats, syndicates, and LP-facing work—Clay Norris and Rohit Mittal among them—consistently describe analyst and associate roles as two-year stepping stones, after which you are expected to join a portfolio company, start a company, move to another fund, or go to business school—not automatically ascend internally.

Some funds do advertise partner-track roles explicitly—Wischoff Ventures posted such a hire in June 2026—but those are exceptions. More common is the pattern Neal Mintz (Wischoff Ventures) described: a quiet exodus of non-partners into operating roles when deal volume thins and carry economics stay uncertain.

Carry at junior levels is rare. Industry observers often cite that most junior investors receive no carry; even where it exists, allocations are small enough that cash comp dominates your economics for years.

Fund economics reinforce the gap. Carry only matters when the fund returns well and you have been there long enough to vest through exits. A principal who helps return a fund may see life-changing upside; an analyst who helped source one seed deal usually will not.

None of this means venture is a bad career. It means you should enter with eyes open:

- If you want partnership, optimize for level of entry, deal attribution, and sector expertise—not title inflation.

- If you want optionality, a two-year analyst or associate stint plus a strong network can open operating, founding, or investing paths elsewhere.

- If you want wealth fastest, employee roles in VC are usually a poor bet versus operating equity, growth equity, or the right startup grant.

Strebulaev's work also documents persistent promotion gaps by gender in venture, even conditional on reaching junior and middle levels. The honest response is not to pretend the gap does not exist, but to choose firms and sponsors deliberately and build attribution that is visible inside the partnership.

Venture capital compensation by role

Venture pay blends base salary, annual bonus, and carried interest. Cash is paid annually; carry pays out over years as portfolio companies exit. Figures below are U.S.-oriented ranges from recent compensation surveys (Carta, PitchBook, NVCA-adjacent reporting) and vary sharply by fund size and city. For a deeper comp breakdown by role, see the venture capital salary guide.

| Role | Total cash (US) | Carry (typical) | Notes |

|---|---|---|---|

| Analyst | $85K–$180K | None | Median all-in near ~$125K at larger funds |

| Associate | $130K–$320K | None | Most associates receive no carry |

| Senior associate | $170K–$390K | 0–1% if any | Small allocations at some funds only |

| Principal / VP | $250K–$750K | ~0.5%–3% of carry pool | First level where carry matters for many |

| Partner | $400K–$1.4M+ | ~3%–12% of carry pool | Wide spread; founding/senior partners higher |

| Managing partner / GP | $550K–$2.2M+ | ~15%–30% of carry pool | Founding GPs at small funds can hold more |

Carry figures are each person's share of the GP carry pool (typically ~20% of fund profits), not a slice of total fund returns. Allocations must sum across the partnership, vest over years, and vary sharply by fund size and ownership.

Fund size is the largest driver of cash: mega-funds often pay 30–40% above median; emerging managers may pay below median but offer earlier responsibility. Geography adds another spread—San Francisco and New York at the top, with secondary markets somewhat below on cash but sometimes ahead on purchasing power when tax and housing are factored in.

Venture cash comp is usually below private equity at equivalent seniority until carry kicks in at senior levels. Most people who join VC trade early paycheck for optionality, learning, and proximity to company formation.

How fund size and stage change the job

At large funds, junior roles skew toward sourcing and screening. The partnership already has sector leads; you are building the top of the funnel and sharpening memos for decisions made above you.

At small funds, juniors are generalists. You may join founder calls, draft LP letters, and support portfolio hiring in the same month.

Stage matters too. Seed and pre-seed investing is narrative- and relationship-heavy; financial models are often simple. Growth and late-stage funds look more like private equity in diligence depth.

When comparing opportunities, browse firms by stage and sector on the Venture Capital Careers companies directory so you know whether a role will be sourcing-heavy, diligence-heavy, or platform-oriented before you apply.

Common mistakes when planning a VC career

Treating analyst as partner track by default. Many programs are designed to educate and rotate talent, not to mint GPs.

Optimizing for online audience before skillset. Visible thought leadership can help, but funds still hire people who can evaluate companies and earn founder trust—not just post threads.

Ignoring the two-year clock. If you join a fixed-term program, plan your next move at month six, not month twenty.

Chasing brand without sector fit. A tier-one name in fintech will not help if you want to spend the next decade in biotech.

Expecting carry as a junior. Assume cash only; treat any carry offer as a bonus.

Skipping operator experience when the data says it matters. If partnership is the goal, time in a venture-backed operating role is often a higher-ROI move than another junior investing seat.

Choosing VC as your first job straight out of college. Practitioners on X warn that jumping directly into venture without banking, consulting, or operating reps can leave you with thin networks and limited training—fine for exposure, weaker for long-term leverage.

FAQ

What is the most common entry-level VC role?

Analyst for undergrad and early-career hires; pre-MBA associate for people with banking, consulting, or startup experience. Internships are the main pipeline into analyst classes.

How long does it take to become a VC partner?

There is no fixed timeline. Some operators enter as partners; others spend a decade as associate and principal. Promotion depends on deal attribution, fund performance, and whether the partnership needs another GP.

Can you get into venture capital without an MBA?

Yes. Operators, founders, bankers, and consultants break in without MBAs every year. An MBA still opens doors at large firms because of network density and credentialing, but it is not required—especially at seed-focused funds.

Do VC analysts get carried interest?

Usually no. Some senior associates begin receiving small carry allocations; meaningful carry typically starts at principal level for employees who receive it at all.

Is venture capital a good career?

It can be if you want learning, founder exposure, and long-dated upside more than maximum early cash. It is a poor fit if you need predictable hours, fast wealth without carry, or highly repeatable work.

What should I do after a two-year analyst program?

Common paths: move to a portfolio company in an operating role, join another fund at associate level, pursue an MBA, or start a company. Decide based on whether you want more investing reps or operating credibility.

Your next step on Venture Capital Careers

If you know which rung you are targeting:

- Browse open roles on the Venture Capital Careers job board—filter by title in the UI, not via expiring deep links.

- Research funds on the companies directory to match stage, sector, and team size to your entry path.

- Create a candidate profile at venturecapitalcareers.com/auth/join so hiring managers and recruiters can find you.

- Read the break-in companion at How to Become a Venture Capitalist for networking tactics, resume positioning, and interview prep.

- Go deeper on role specifics with the venture capital analyst job description, associate job description, and venture capital salary guide.

- Prepare for interviews via venture capital interview questions and how to get a job in venture capital.

The venture capital career path rewards people who pick the right entry point, build founder relationships early, and plan past the first two-year stint—not people who collect titles on a ladder map.