Venture Capital Deal Flow: Sourcing, Tracking, and Screening Deals

Learn how venture capital deal flow works, how VCs source startups, what to track in a pipeline, and how candidates can speak credibly about sourcing work.

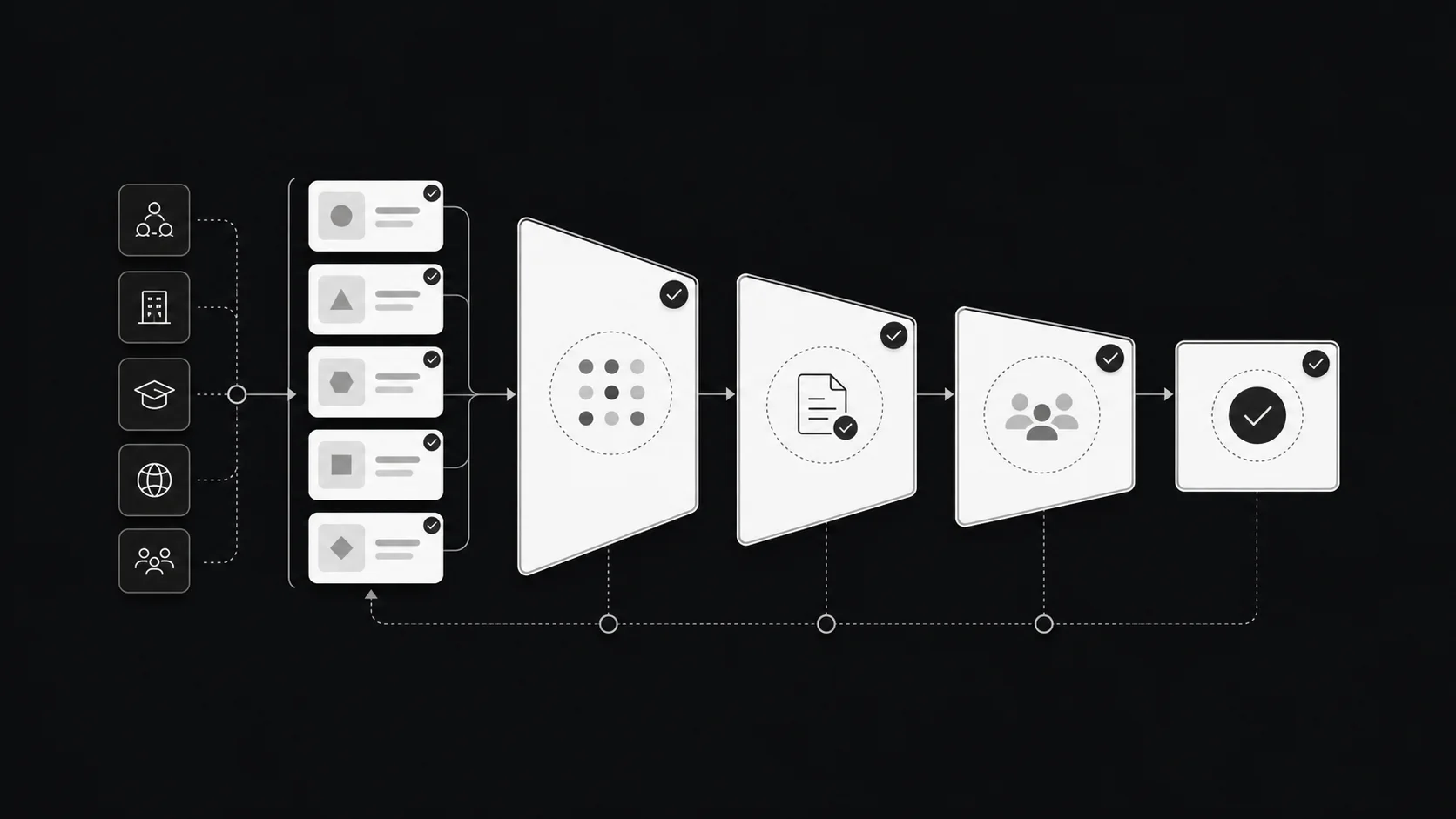

Venture capital deal flow is the stream of startup investment opportunities a VC firm sees, tracks, screens, and decides whether to pursue. Strong deal flow is not just a high number of founder introductions. It is a repeatable system for finding companies that fit the fund's thesis, moving the right ones through diligence, and maintaining relationships with founders before and after a decision.

For candidates, deal flow matters because sourcing and first-pass screening are often the first real investment jobs analysts, associates, scouts, and interns are trusted to do. If you can explain how a fund sources, filters, and tracks opportunities, you sound closer to the work than someone who only says they "like startups."

What venture capital deal flow means

Deal flow is the managed pipeline of companies a VC firm might invest in. It starts before a pitch deck arrives and continues after the firm passes, because a founder who is too early today may become a better fit later.

A VC firm with strong deal flow has three advantages:

- It sees more relevant companies before competitors do.

- It can compare opportunities across a market instead of evaluating each pitch in isolation.

- It can spend partner time on the few companies that fit the fund's stage, sector, ownership target, and return profile.

The Stanford GSB case on venture capital deal sourcing and screening frames the work as an associate-level evaluation problem: decide whether incoming opportunities should be rejected, researched further, or escalated. That is a practical way to think about deal flow. The goal is not to love every startup. The goal is to route each company to the right next step.

Deal flow versus deal sourcing

Deal sourcing and deal flow are related, but they are not the same thing.

| Term | Meaning | Practical output |

|---|---|---|

| Deal sourcing | Finding potential investment opportunities | Founder intro, market map, company list, inbound pitch, outbound target |

| Deal flow | Managing those opportunities through a pipeline | Stage, owner, notes, next step, diligence status, decision |

| Deal flow analysis | Measuring quality, conversion, and fit across the pipeline | Channel performance, stage conversion, reasons for pass, thesis coverage |

Sourcing is how opportunities enter the system. Deal flow management is how the firm decides what deserves attention. A fund can be good at sourcing but poor at deal flow if every company sits in a messy spreadsheet with no owner or next step. It can also be organized but under-sourced if the pipeline is tidy and empty.

How VCs source deals

VC sourcing usually blends warm networks, thesis-led research, founder community building, and targeted outbound. The mix depends on the fund's stage and strategy.

| Sourcing channel | Best use | Main risk | Analyst or associate work |

|---|---|---|---|

| Founder and operator referrals | High-trust introductions | Network homogeneity | Maintain connector notes and follow up quickly |

| Co-investors and angels | Signals from people already seeing deals | Consensus and crowded rounds | Track who sees which markets early |

| Accelerators and demo days | Seed and pre-seed discovery | Too many similar pitches | Build watchlists before the event |

| Universities and labs | Deep tech and technical founders | Long commercialization timelines | Map labs, grants, professors, and spinouts |

| Product communities | Developer tools, open source, prosumer, AI, vertical SaaS | Hard to separate usage from company quality | Monitor launches, usage signals, and founder profiles |

| Market maps | Thesis-driven sourcing | Can become static research theater | Define categories and identify non-obvious companies |

| Cold outbound | Narrow theses and under-networked founders | Low response if generic | Write specific, evidence-based founder notes |

| Inbound pitch forms | Broad top-of-funnel coverage | Low signal-to-noise | Apply clear triage criteria |

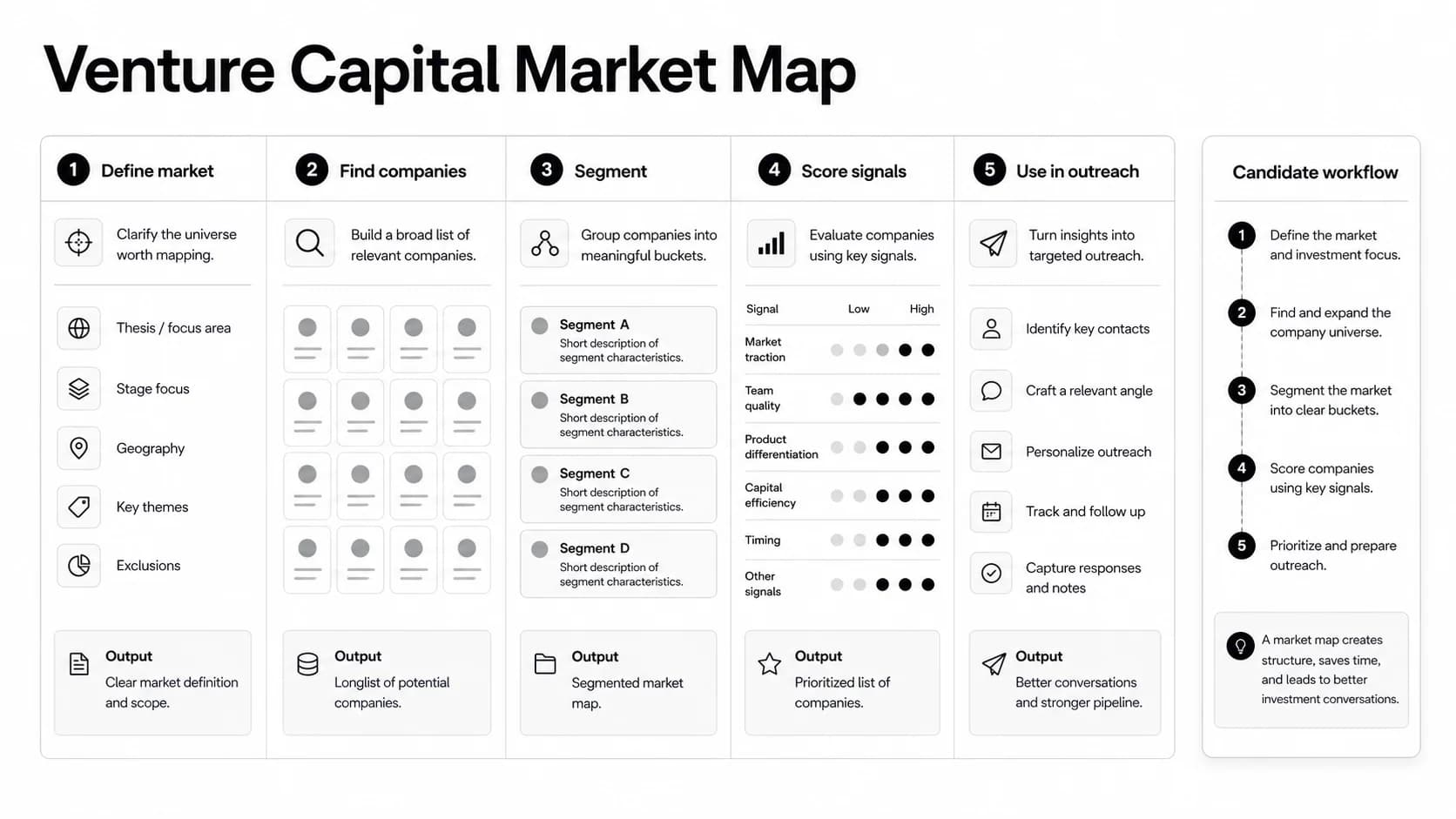

The strongest sourcing systems are thesis-led. A fund that invests in seed-stage vertical AI for healthcare operations should not simply collect "AI startups." It should define buyer pain, workflow urgency, data access, distribution motion, regulation exposure, and founder-market fit. That thesis turns sourcing into a search for specific signals.

Warm referrals still matter because trust travels through people. But cold sourcing can work when the outreach is specific. A bad cold email says the market is exciting. A good one shows the investor understands the founder's product, customer, timing, and the reason the company may fit the fund.

VC Lab's sourcing article is right to emphasize systems, relationships, and channel iteration. The missing step for many junior investors is translating that into a weekly operating rhythm: identify companies, qualify fit, log the source, set the next step, and revisit the market map.

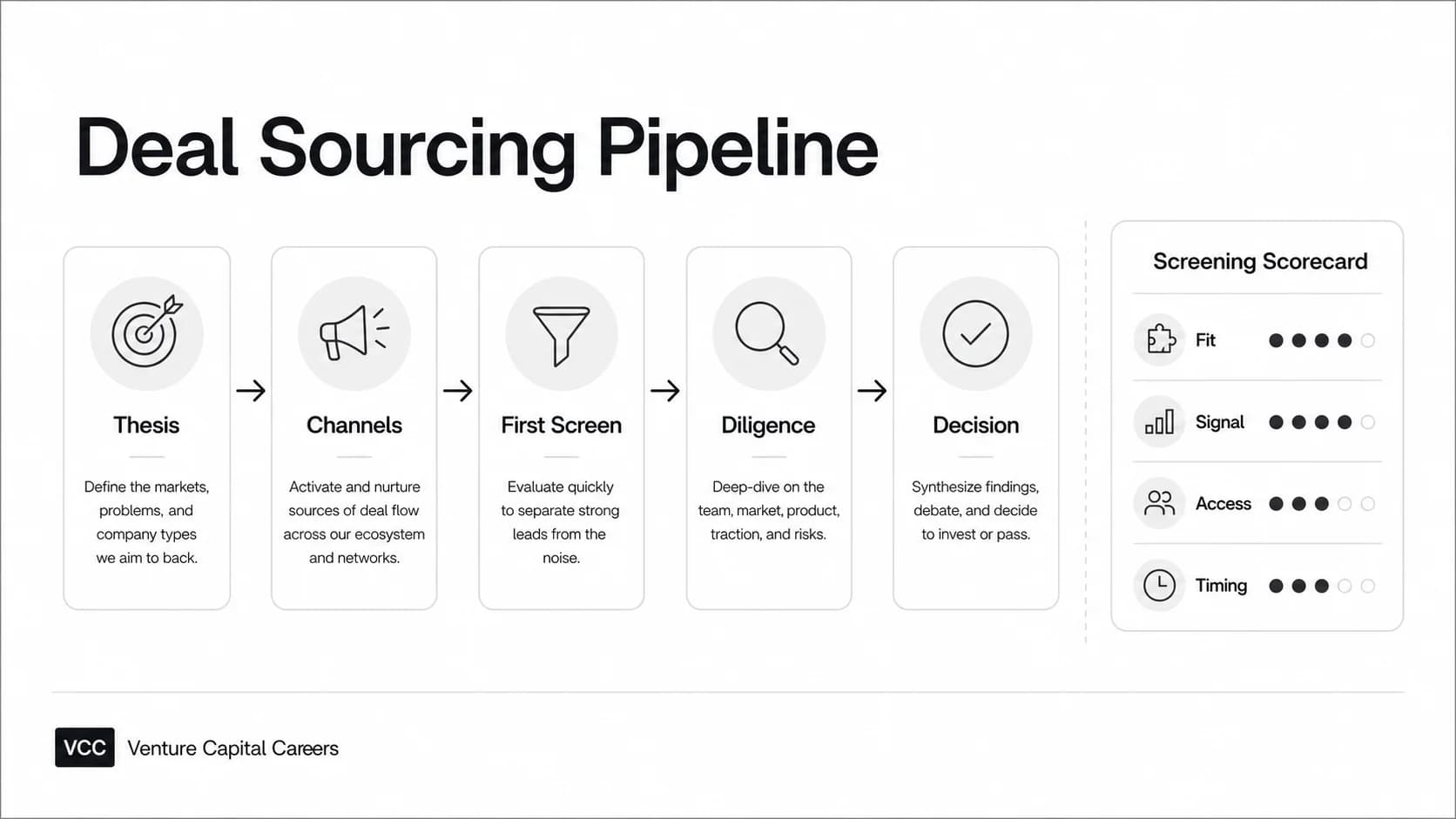

How to track venture capital deal flow

A VC pipeline should make the next action obvious. At minimum, every opportunity needs:

- Company name and website

- Founder names and contact source

- Sector, stage, geography, and business model

- Source channel

- Fund thesis fit

- One-line company description

- Current traction or proof point

- Stage in the pipeline

- Owner inside the fund

- Next step and due date

- Decision reason if passed

A simple stage model is enough for most teams:

| Stage | Meaning | Decision question |

|---|---|---|

| Sourced | Company identified but not yet qualified | Does it fit the fund's mandate? |

| Qualified | Basic fit is plausible | Is there enough signal for a first meeting? |

| First meeting | Founder conversation scheduled or completed | Is this worth more diligence? |

| Diligence | Market, product, customer, team, and financial work underway | What would need to be true to invest? |

| Partner review | Internal discussion or investment committee prep | Is conviction high enough? |

| Invest / pass / nurture | Decision made | What relationship should continue? |

The important part is consistency. A fund that defines "qualified" differently every week cannot measure whether sourcing is improving. A clean pipeline also helps partners avoid duplicate outreach, missed follow-ups, and fuzzy pass decisions.

Deal flow analysis: metrics that matter

Deal flow analysis is the process of evaluating pipeline quality, not just counting how many companies entered the CRM. Volume matters only if it creates better decisions.

| Metric | What it tells you | Better question |

|---|---|---|

| Sourced companies | Top-of-funnel activity | Are these companies relevant to the thesis? |

| Qualified rate | Screening accuracy | Are we sourcing too broadly or too narrowly? |

| First-meeting conversion | Founder interest and fund fit | Are our intros and outreach credible? |

| Diligence conversion | Quality of qualified opportunities | Are we escalating the right companies? |

| Investment conversion | Final selectivity | Are we seeing enough companies to build conviction? |

| Source quality by channel | Which channels produce strong opportunities | Which channels produce diligence-worthy companies, not just names? |

| Time in stage | Pipeline friction | Where are we slow or unclear? |

| Pass reason distribution | Pattern recognition | Are most passes about stage, market, team, traction, or valuation? |

The best metric for a junior investor is often not "deals sourced." It is "qualified companies that became useful partner conversations." That metric rewards judgment, not spray-and-pray activity.

Screening: what makes a deal worth time

Initial screening should be fast but disciplined. Before a full diligence process, ask:

- Does the company fit the fund's stage and check size?

- Is the market large enough for venture-scale outcomes?

- Is there a clear customer pain or workflow urgency?

- Does the founder have a credible wedge into the market?

- Is there early evidence of pull, such as usage, revenue, pilots, retention, community, or waitlist quality?

- Does the round timing match the fund's ability to invest?

- What would make the fund uniquely helpful?

The answer does not need to be perfect. Early-stage investing is uncertain by design. The point is to decide whether uncertainty is interesting enough to investigate.

Strong screening notes are short and opinionated. Instead of writing, "Interesting AI healthcare company," write:

"Seed-stage company automating prior authorization follow-up for specialty clinics. Fits healthcare operations thesis. Need to test whether the product is workflow-critical or just an analytics layer. Next diligence: customer references, denial-rate impact, implementation time, and budget owner."

That style of note gives a partner something to react to.

When deal flow software helps

Deal flow software helps when relationship history, source attribution, collaboration, and pipeline visibility matter more than a simple list. The software intent is real: VC Stack's deal sourcing tools directory shows a broad market of investor tools and startup databases.

Use this decision rule:

| Situation | Lightweight option | More robust option |

|---|---|---|

| Solo scout or new angel | Spreadsheet plus calendar reminders | Lightweight CRM |

| Emerging manager with repeatable sourcing | CRM with source, owner, stage, and next step fields | VC-focused deal-flow platform |

| Multi-partner fund | Shared CRM and contact history | Purpose-built platform with relationship intelligence and permissions |

| Thesis-heavy fund | Market maps and research databases | Tools that support company discovery, enrichment, and collaboration |

Do not buy software to compensate for a weak sourcing thesis. A better CRM will not tell the team which markets matter, which founders are worth meeting, or why a company fits the fund. Software should make a good process visible, searchable, and repeatable.

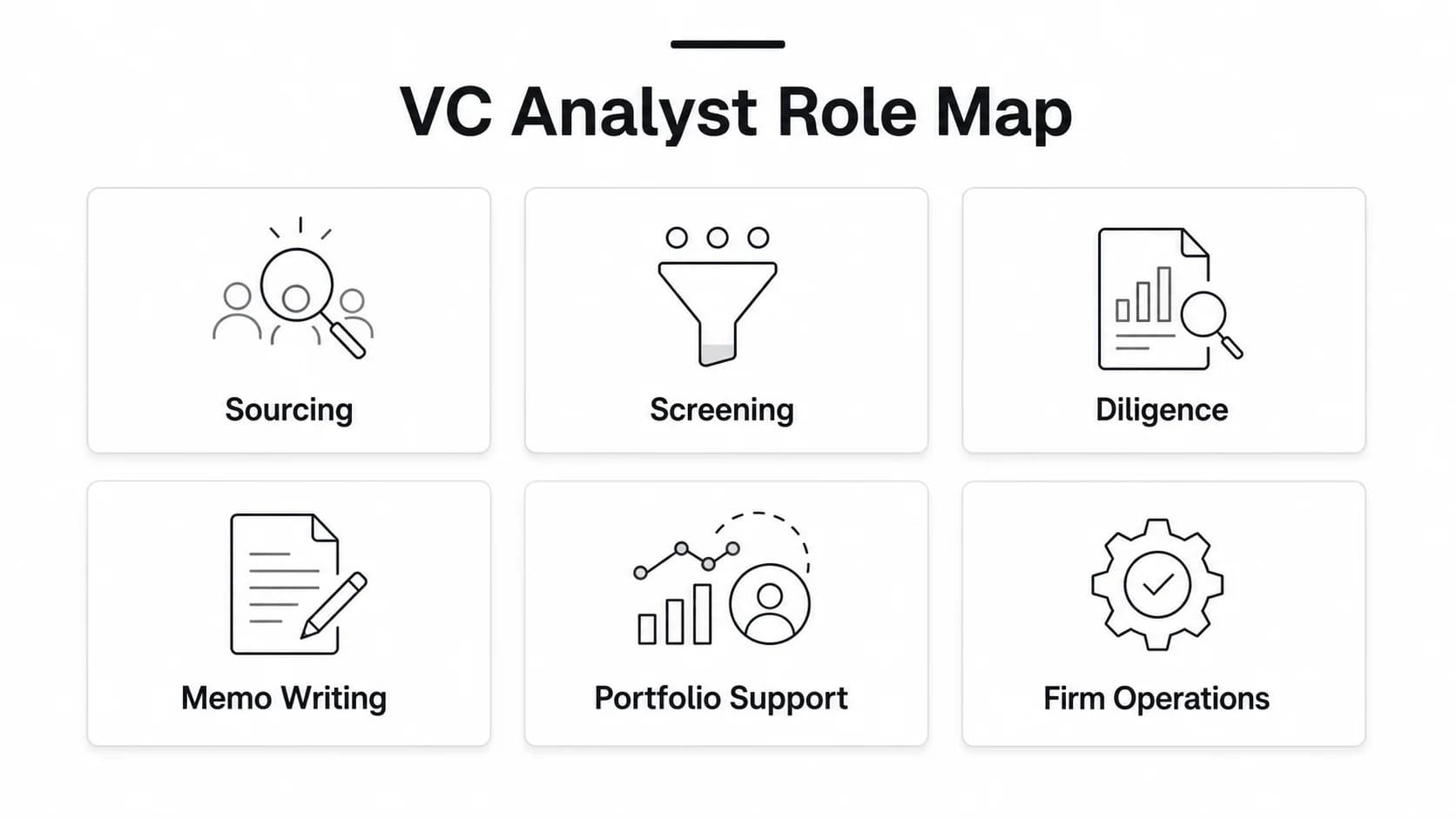

How candidates can use deal flow knowledge

Deal flow is a useful interview and on-the-job topic because it connects research, judgment, networking, and writing. If you are applying for a VC analyst, associate, scout, or internship role, prepare examples that show you can help the pipeline.

Good examples include:

- A market map with categories, company names, stage, geography, and rationale

- A sourcing list for a specific thesis

- A short founder outreach note

- A first-pass screen with invest, pass, or monitor recommendation

- A memo explaining why a market is becoming investable now

- A relationship map of angels, operators, founders, and accelerators in a niche

Use Venture Capital Careers in two practical ways. Browse the VC job board to see how funds describe sourcing, research, portfolio support, and diligence responsibilities in live roles. Then use the companies directory to research firm stage, geography, and focus before you choose market examples for interviews.

For deeper preparation, pair this article with the guides to venture capital deal sourcing, venture capital due diligence, investment thesis, and venture capital skills.

Common mistakes in VC deal flow

Mistaking volume for quality

More pitches do not automatically produce better investments. The stronger question is whether the fund is seeing more companies that match its thesis before they become obvious to everyone else.

Letting the pipeline become a graveyard

Every company needs an owner, stage, and next step. If the team cannot tell whether a founder should be contacted, passed, or nurtured, the pipeline is not being managed.

Over-indexing on warm introductions

Warm introductions are valuable, but they can make a fund's network narrower over time. Thesis-led cold sourcing, community research, and market maps help a fund find founders outside its existing circles.

Screening for what is easy to measure

Revenue, round size, and logos are useful signals, but early-stage investing often depends on market timing, customer pain, founder insight, and distribution. A good screen makes room for qualitative judgment.

Ignoring why deals are passed

Pass reasons are data. If most passes are about stage mismatch, the sourcing strategy may be targeting the wrong maturity. If most passes are about weak customer pain, the market thesis may be too broad.

FAQ

What is venture capital deal flow?

Venture capital deal flow is the pipeline of startup investment opportunities a VC firm sources, tracks, screens, diligences, and decides whether to invest in, pass on, or monitor for later.

What is venture capital sourcing?

Venture capital sourcing is the process of finding potential startup investments through referrals, founder networks, accelerators, universities, communities, market maps, databases, inbound pitches, and targeted outbound.

How do VCs track deal flow?

VCs track deal flow in spreadsheets, CRMs, or VC-focused platforms. The system should record the company, source, sector, stage, owner, thesis fit, next step, diligence notes, and final decision.

What is deal flow analysis?

Deal flow analysis measures the quality and movement of opportunities through the pipeline. Useful metrics include qualified rate, first-meeting conversion, diligence conversion, source quality by channel, time in stage, and pass reasons.

What is good deal flow?

Good deal flow is relevant, high-signal, and aligned with the fund's strategy. It gives a VC enough qualified opportunities to build conviction without wasting time on companies the fund would never invest in.

How should a VC candidate talk about deal flow?

Talk about the work product. Explain how you would build a market map, qualify companies against a thesis, write concise screening notes, track follow-ups, and recommend whether a company should be passed, monitored, or escalated.