Venture Capital Due Diligence: Process, Checklist, and Analyst Framework

A practical VC due diligence framework covering the process, evidence, stage-specific checklist, red flags, and analyst work products.

Venture capital due diligence is the structured investigation a VC firm uses to test whether a startup fits its investment thesis, whether the evidence supports the founder's claims, and whether the expected return justifies the risks. The output is not a folder of documents. It is a defendable investment recommendation, a record of unresolved questions, and a plan for any terms, closing conditions, or post-investment monitoring.

Good diligence is proportional. A pre-seed company cannot provide the operating history of a Series B company, while a growth-stage business should not receive a pass on revenue quality, controls, or customer concentration. The investor's job is to identify the few assumptions that make or break the investment and test those assumptions with the best available evidence.

What venture capital due diligence is—and is not

Initial screening asks whether a company is worth more time: Does it fit the fund's stage, sector, check size, geography, ownership target, and return model? Diligence begins once the firm has a plausible investment hypothesis. It verifies the upside case, searches for reasons the thesis could fail, and determines which uncertainties are acceptable.

VC diligence differs from a checklist-driven audit in two ways. First, venture investors underwrite an uncertain future, especially at the earliest stages. A clean historical record matters, but it cannot prove that a new market will develop or that a product will become dominant. Second, most VC investments are minority positions. Investors therefore care not only about enterprise value, but also about governance, information rights, ownership, dilution, follow-on capital, and the ability to support the company after closing.

It also differs from acquisition diligence. A buyer taking control may inspect every material contract, asset, liability, and integration dependency. A VC firm still needs legal, financial, technical, and commercial confidence, but the depth should follow the deal's stage, sector, check size, and decisive risks.

The most useful operating principle is simple: do not ask for a document unless you know which claim it tests and what decision could change because of it.

Where diligence fits in the VC investment process

Firms sequence deals differently. Some issue a term sheet before confirmatory legal and financial diligence; others complete substantial business diligence before making an offer. The common structure looks like this:

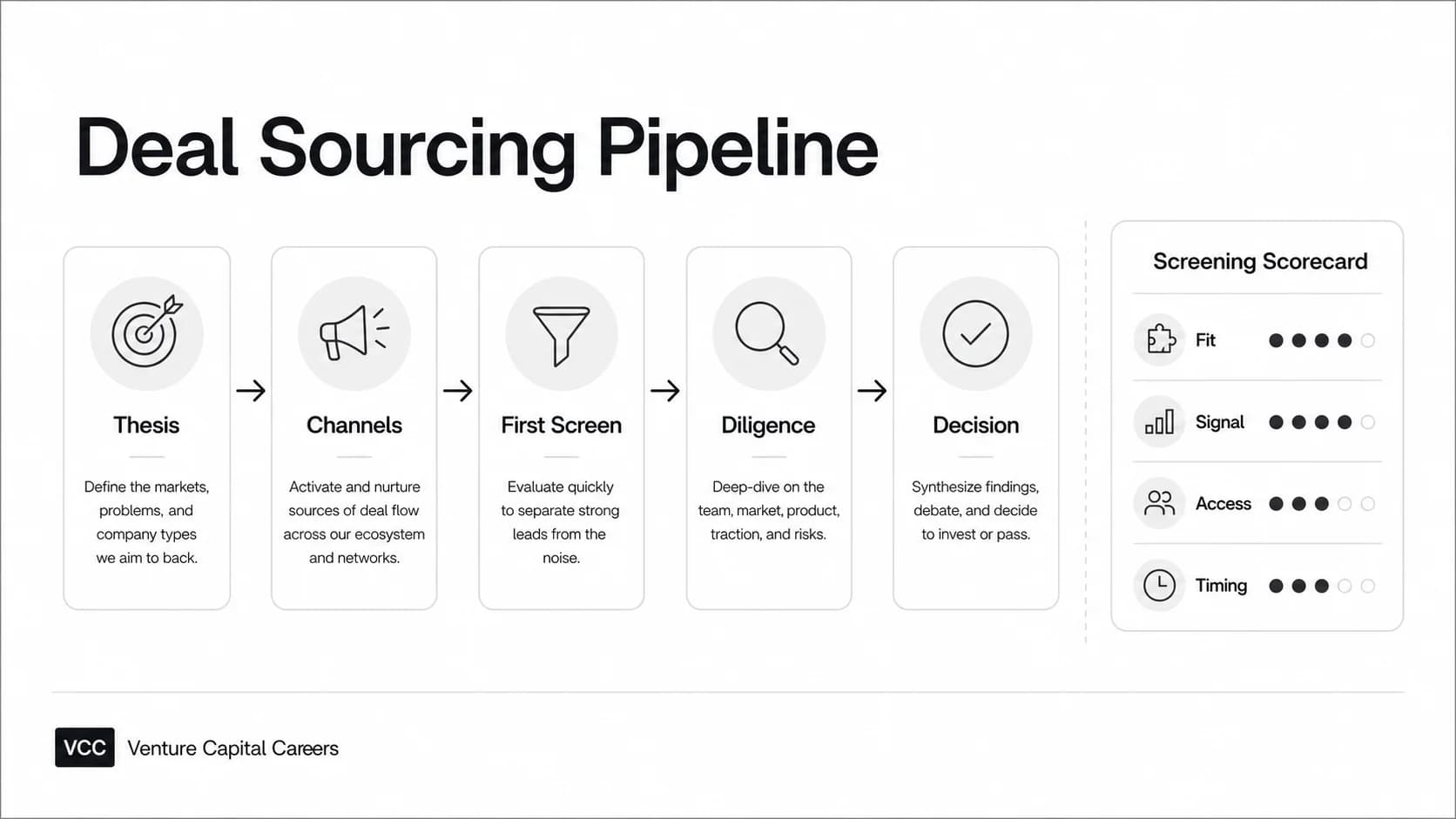

Sourcing and screening

The team determines whether the opportunity fits the fund. An analyst may summarize the company, market, round, existing investors, and obvious conflicts or disqualifiers. This is triage, not full diligence. The goal is to avoid spending specialist time on a deal the fund cannot or should not pursue.

Preliminary investment thesis

A deal lead states why the company might produce an outlier return. The investment thesis should identify the key drivers—such as founder insight, market timing, retention, distribution advantage, or technical differentiation—and the conditions that would invalidate the case. Without explicit kill criteria, diligence tends to collect facts that confirm enthusiasm.

Business, technical, financial, and legal workstreams

Associates and principals often coordinate the process, with partners leading founder assessment and the final judgment. Customers, industry experts, technical advisers, accountants, and legal counsel contribute where their expertise changes the decision. Specialists provide evidence; they do not own the investment thesis.

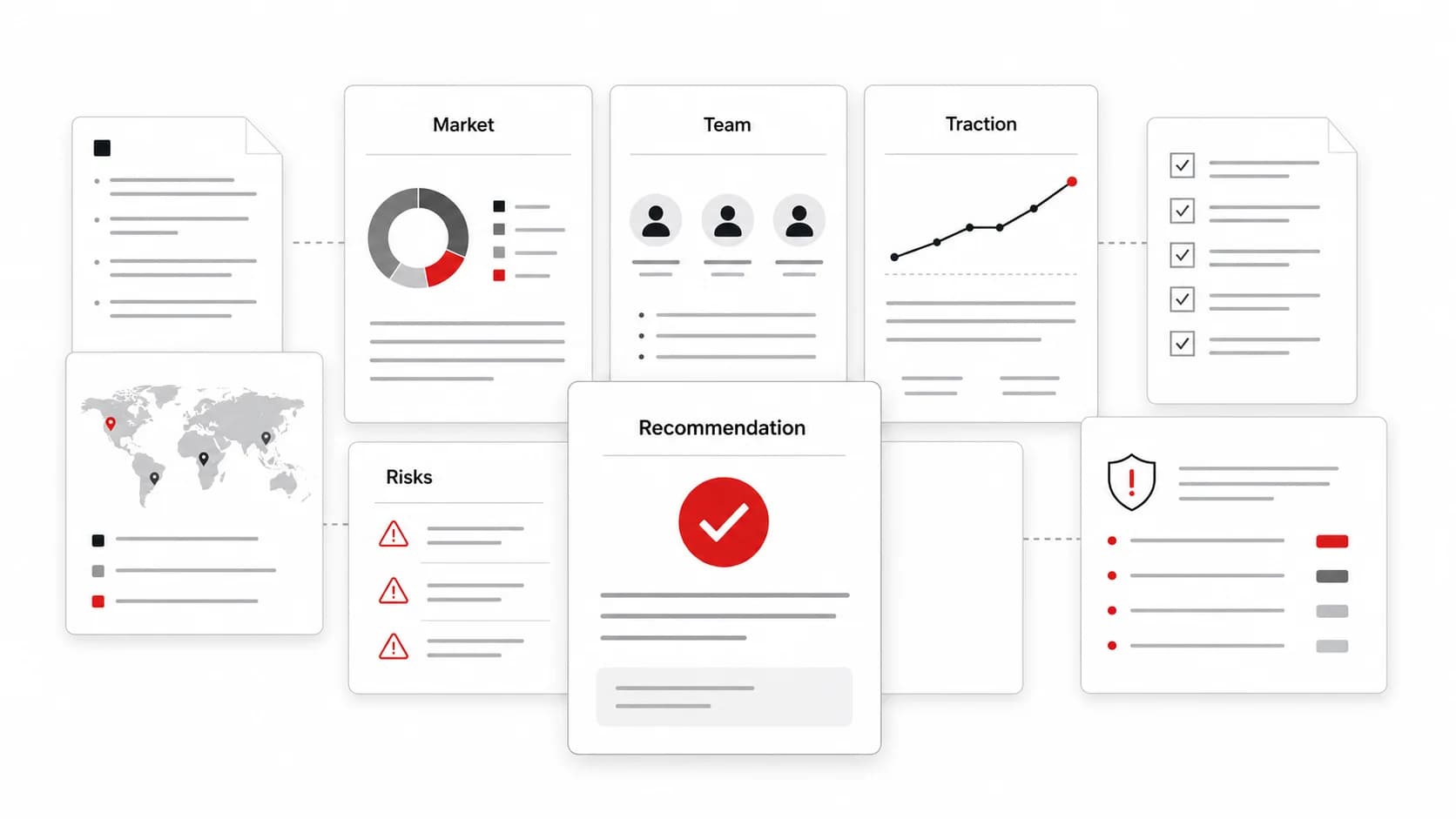

Investment memo and investment committee

The deal team synthesizes findings into a recommendation. Bessemer Venture Partners publishes historical investment recommendation memos partly to study the reasoning behind successful decisions, which illustrates a second purpose of the memo: it creates a record that a firm can revisit after the outcome is known.

A useful memo separates facts, inferences, assumptions, and unknowns. It explains the upside, downside, decisive risks, proposed ownership and terms, and what the team still needs to resolve. The investment committee should be able to challenge the thesis without reopening every file in the data room.

Term sheet, confirmatory diligence, and closing

Diligence findings can change valuation, investment size, governance, protective terms, closing conditions, or the decision itself. Legal counsel then verifies corporate authority, securities, intellectual property ownership, material contracts, and other transaction-specific matters. The NVCA model legal documents are useful reference points for common US venture financing documents, but they are starting points—not substitutes for transaction-specific legal advice.

Post-investment handoff

Open risks should become an operating plan, not disappear after the wire. The board and deal team need named indicators, reporting cadence, and escalation triggers for the assumptions that remain unproven.

A six-step VC due diligence workflow

1. Write the investment hypothesis and kill criteria

State the thesis in falsifiable terms. “Large market and strong team” is too vague. A better hypothesis might be: “Mid-market finance teams will adopt this product without services-heavy implementation, producing strong retention and a payback period the company can finance.”

Then write the kill criteria. Examples include no evidence of repeat usage, a market too small for the fund's return target, unresolved IP ownership, a cap table that prevents acceptable ownership, or a regulatory dependency the company cannot satisfy.

2. Build the diligence plan and assign owners

Convert each thesis claim into a question, evidence request, owner, and deadline. Put the highest-decision-impact questions first. The team should know which workstreams can run in parallel and which depend on access to customers, product telemetry, counsel, or a technical expert.

3. Request evidence and grade its quality

Source quality matters. Audited or system-generated records are generally stronger than a manually prepared slide. A signed customer contract answers a different question from a founder's pipeline spreadsheet. Customer interviews can validate urgency and alternatives, while product analytics can test whether stated usage is durable.

Label evidence as primary, corroborating, management-provided, or unverified. When two sources conflict, record the conflict rather than silently choosing the more attractive number.

4. Test the claims across workstreams

Triangulate. A claim of strong product-market fit might be tested through cohort retention, product usage, renewal behavior, customer calls, discounting, support burden, and the competitive alternative. A market-size claim should connect identifiable customers, willingness to pay, sales capacity, and realistic penetration—not just a top-down industry figure.

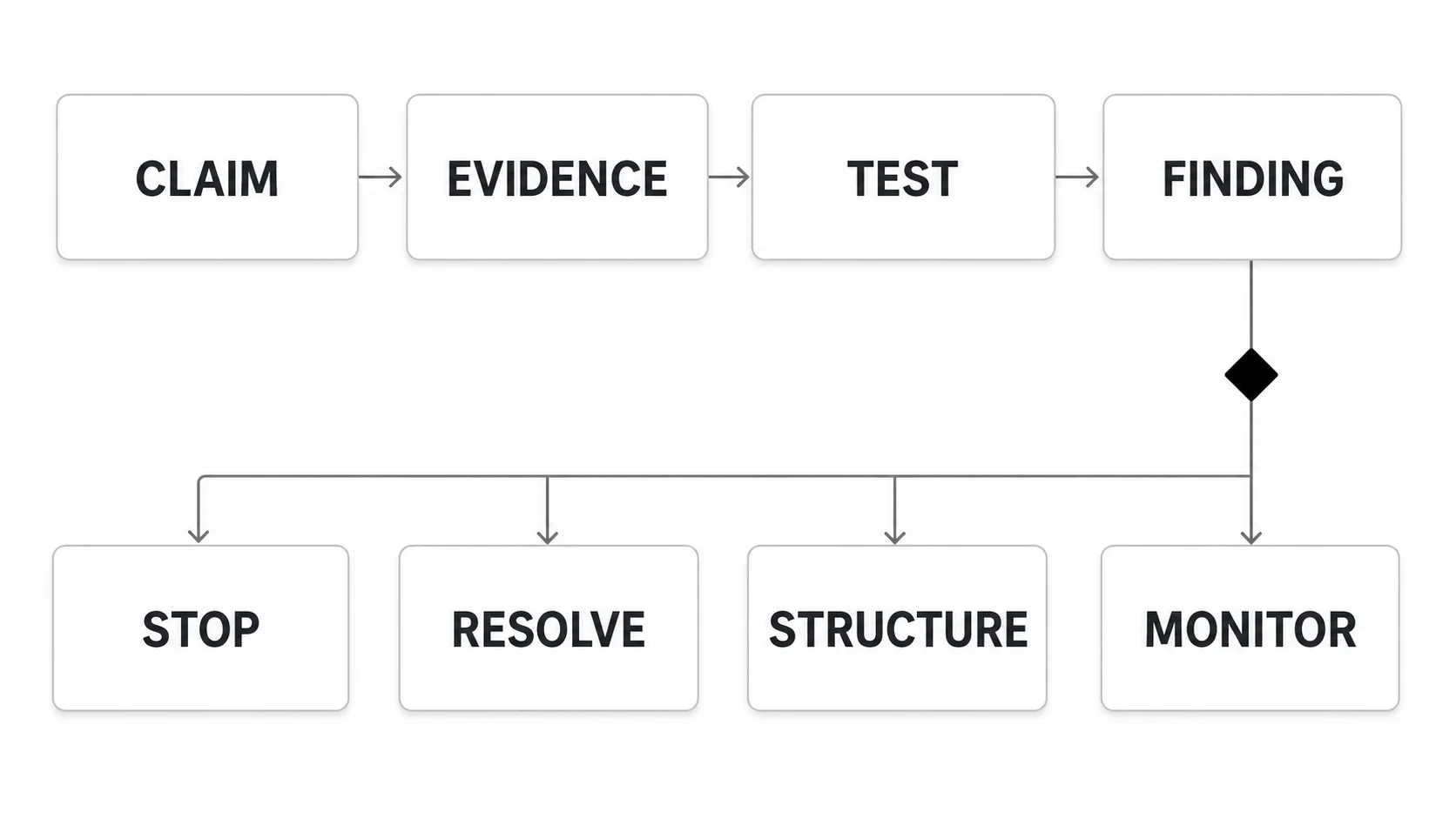

5. Maintain an issue log and red-team the deal

Every material issue needs an owner, evidence, severity, next action, and resolution date. Ask an uninvolved team member to articulate the strongest case against the investment. Red-teaming is especially important when the firm has moved quickly, a prominent investor is leading the round, or partner conviction formed before the evidence was available.

6. Convert findings into the memo, terms, and monitoring plan

The final synthesis should show which claims held, which failed, and which remain uncertain. A term can allocate or limit some risks; it cannot repair a broken market, weak retention, or a team the firm does not trust.

Worked example: from claim to decision

| Step | Example |

|---|---|

| Founder claim | “Customers expand rapidly after the first deployment.” |

| Evidence | Contract values, invoices, product usage, account-level revenue history, renewal records, and customer calls |

| Test | Build cohorts by start quarter; separate price increases, services, and acquired revenue from product expansion |

| Finding | Expansion is strong in enterprise accounts but flat in mid-market accounts, which are most of the pipeline |

| Implication | The current go-to-market plan overstates near-term efficiency and may require a more expensive enterprise sales motion |

| Decision response | Revise the base case, test hiring and cash needs, adjust valuation or check size if needed, and monitor enterprise pipeline conversion |

The discipline is the traceability. An investment committee should be able to move from the recommendation back to the evidence without reconstructing the analysis.

VC due diligence checklist by workstream

A useful checklist is organized by decisions, not folders. The exact requests depend on the company, but these questions cover the recurring workstreams.

| Workstream | Decision question | Evidence to test | Illustrative red flags |

|---|---|---|---|

| Team and references | Can this team recruit, learn, allocate capital, and execute through uncertainty? | Founder interviews, role history, references, hiring record, org design, founder equity and vesting | Material inconsistencies, unresolved founder conflict, weak ownership of critical functions, poor reference patterns |

| Market and competition | Is the obtainable market large enough, urgent enough, and open at the right time? | Customer segmentation, market map, budgets, buyer interviews, competitor wins/losses, regulatory or technology shifts | Top-down TAM with no buyer path, incumbent response ignored, weak urgency, market dependent on one unproven change |

| Product and technology | Does the product solve the problem, and can it scale defensibly? | Demo, roadmap, architecture review, usage, reliability, security practices, technical-debt assessment, IP provenance | Demo does not match production, critical single-person dependency, unclear IP ownership, unmanageable reliability or security exposure |

| Customer and commercial | Is demand repeatable and economically attractive? | Customer calls, contracts, pipeline, win/loss data, retention cohorts, pricing, discounts, sales cycle, channel performance | Reference selection bias, concentration, churn hidden by new sales, non-repeatable founder-led deals, services masking software revenue |

| Financial and unit economics | Can the company finance the plan, and do the economics improve with scale? | Income statement, balance sheet, cash flow, bank records, budget versus actual, model assumptions, gross margin, CAC, payback, burn, runway | Statements do not reconcile, aggressive recognition, blended metrics hide weak cohorts, cash need understated, model disconnected from hiring and pipeline |

| Legal, cap table, and IP | Does the company own what it sells, and can the proposed financing close cleanly? | Formation records, board approvals, cap table, SAFEs/notes, option grants, IP assignments, material contracts, disputes, permits | Missing approvals, unassigned founder or contractor IP, undocumented equity promises, unexpected preferences or dilution, material compliance gaps |

| Operations, security, and regulation | Can the organization support the promised growth without unacceptable exposure? | Policies, key vendors, insurance, data flows, access controls, incident history, licenses, sector-specific compliance | Critical vendor dependency, weak data controls, missing licenses, no owner for regulated activity, scaling plan that breaks service quality |

Use specialist pages when a workstream becomes the main task. VCC's financial due diligence explainer covers the financial review in more depth, while the cap table guide explains ownership records and dilution. For market work, a venture capital market map helps an analyst structure categories, incumbents, substitutes, and whitespace.

The checklist should shrink as well as expand. If a question cannot change the recommendation, terms, closing readiness, or monitoring plan, it is probably lower priority than an unresolved thesis risk.

How diligence changes by funding stage

The company stage changes both the available evidence and the burden of proof. A stage-calibrated process avoids punishing a young company for lacking history while demanding more than narrative from a mature one.

| Workstream | Pre-seed / seed | Series A | Growth stage |

|---|---|---|---|

| Team | Founder insight, commitment, complementary skills, ability to recruit | Leadership gaps, recruiting velocity, functional ownership, references | Executive depth, succession, controls, board effectiveness, ability to manage complexity |

| Market | Problem urgency, credible customer set, bottom-up wedge, timing | Repeatable segment, competitive position, expansion path | Share, category durability, international or adjacent expansion, downside market scenarios |

| Product | Prototype or MVP, user learning, technical feasibility | Engagement, retention, roadmap, scalability, security foundations | Reliability, platform architecture, technical debt, security and compliance at scale |

| Commercial | Design partners, early willingness to pay, founder-led sales learning | Cohort retention, pricing, pipeline quality, repeatable sales motion, CAC/payback | Revenue quality, concentration, expansion, churn, channel economics, forecast accuracy |

| Financial | Use of funds, burn, runway, basic model, clean entity/accounting setup | GAAP-quality statements, budget versus actual, unit economics, hiring-linked model | Controls, audits or audit readiness, scenario sensitivity, margin durability, capital efficiency |

| Legal and cap table | Formation, founder equity, SAFEs/notes, option grants, IP assignment | Material contracts, employment and invention agreements, financing history, compliance | Governance, litigation, multi-jurisdiction exposure, complex securities, regulatory depth |

| Decision emphasis | Is there a credible reason this team can discover and own a large opportunity? | Is there enough repeatability to finance scaling? | Is growth durable, governable, and valuable at the proposed price? |

This progression is consistent with the stage-specific practice described in Kruze Consulting's VC due diligence checklist: early rounds emphasize team, market, core product, and basic financial/legal hygiene, while later rounds demand deeper evidence on retention, go-to-market, operations, controls, and compliance.

Two rules prevent false conclusions:

- Absence of mature data at seed is not automatically a red flag. The question is whether the company has generated the evidence appropriate to its age and used it honestly.

- A large growth-stage dataset is not automatically strong evidence. Aggregated metrics can conceal deteriorating cohorts, discounting, concentration, or acquired growth.

The best analysts adjust the test, not the standard of intellectual honesty.

Turn findings into an investment decision

An issue log becomes useful when every material finding has a decision consequence. A practical severity rubric is:

- Stop: the core thesis is broken, trust is impaired, the company cannot lawfully operate as assumed, or the risk cannot be made acceptable.

- Resolve before close: a fix or verification is required before funds move, such as board approval, IP assignment, a corrected cap table, or a specialist opinion.

- Price or structure: the deal may proceed, but the finding changes valuation, investment size, ownership, governance, protective terms, milestones, or syndicate needs.

- Monitor: uncertainty is acceptable today, but the board needs a metric, owner, threshold, and review cadence.

| Finding | Possible decision response |

|---|---|

| Market is attractive, but adoption is slower than the base case | Rebuild scenarios; reduce price or check; require more runway; monitor leading adoption indicators |

| Strong usage but weak gross margin because implementation is services-heavy | Reclassify the business model, test delivery capacity, revise margin and cash assumptions |

| Customer concentration is high but contracts and reference calls are strong | Stress-test churn; size the round for concentration risk; track renewal and diversification milestones |

| Critical contractor has not assigned IP | Resolve with counsel before close; do not treat a representation alone as a cure |

| Cap table contains unexpected SAFEs, notes, or option commitments | Reconcile fully; recalculate ownership and dilution; revise round economics if needed |

| Founder reference pattern raises integrity concerns | Escalate and corroborate; if trust cannot be restored, stop |

The recommendation should explain why the expected return remains attractive after realistic dilution, follow-on capital, and downside cases. It should also distinguish a fixable transaction issue from a broken business thesis. Protective terms can allocate governance and economic rights; they cannot manufacture customer demand.

The final decision belongs in a concise venture capital investment memo that records the thesis, evidence, risks, scenarios, proposed terms, and open questions. If the deal proceeds, those findings inform the term sheet and any relevant governance or protective provisions. Legal counsel should determine which provisions are appropriate for the transaction and jurisdiction.

What VC analysts and candidates are expected to produce

Analysts rarely own every specialist conclusion, but they often make the process legible. The core work products are:

- A one-page diligence plan tied to the investment thesis and kill criteria.

- A prioritized request list with owners and deadlines.

- A market map and competitor analysis that distinguish direct competitors, substitutes, and internal build.

- Customer and expert call notes with source context and contradictions.

- A financial model with transparent assumptions, sensitivities, and downside cases.

- An issue log that separates facts, inferences, unknowns, and next actions.

- An investment memo and IC presentation that make a recommendation rather than hiding behind research volume.

How to approach a diligence case study

Start by naming the three to five questions that could change the decision. A seed-stage software case might prioritize founder-market fit, evidence of urgent demand, retention or repeat usage, distribution feasibility, and financing risk. A growth-stage case might prioritize revenue quality, cohort durability, sales efficiency, concentration, gross margin, and cash requirements.

For each question, show:

- What you know.

- What you infer.

- What remains unknown.

- Which evidence you would request next.

- What result would change your recommendation.

Make the downside concrete. If your base case assumes faster sales hiring, show what happens when ramp time doubles. If expansion revenue supports the thesis, separate expansion from price increases and services. If the market map implies a moat, explain why customers cannot easily choose an incumbent, substitute, or internal workflow.

Finish with a clear recommendation: invest, pass, or continue diligence subject to named conditions. State the strongest argument against your own conclusion. That is more credible than attaching an exhaustive checklist with no prioritization.

Candidates can practice this format with VCC's venture capital case study interview framework and then draft the memo structure described above. When you are ready to apply the work in a live process, browse open venture capital roles.

Common venture capital due diligence mistakes

Treating the data room as ground truth

The data room is a set of claims and records assembled for a transaction. Reconcile financial statements to bank or system records where appropriate, compare pipeline claims with contract and conversion evidence, and use customer calls to test the story behind the numbers.

Confusing market size with obtainable revenue

A large industry total does not establish a venture-scale opportunity. Connect the target segment, buyer, budget, sales motion, price, adoption rate, and competitive response to a bottom-up outcome.

Letting blended metrics hide the cohorts

Company-wide retention, CAC, or gross margin can improve while recent customers deteriorate. Segment by acquisition period, customer type, product, channel, or geography when those distinctions affect the thesis.

Outsourcing judgment to experts or AI

Experts can challenge technical, market, legal, or regulatory assumptions. AI can accelerate document review and question generation. Neither should become the source of record or make the investment decision. Verify material claims against primary documents, system data, and accountable people.

Leaving cap table, IP, and compliance questions until the end

These issues can change ownership, closing readiness, or the company's ability to operate. Surface them early enough for counsel and specialists to determine whether they are fixable.

Writing an advocacy memo

A memo that sells the deal while burying unknowns defeats the purpose of diligence. The decision record should make the strongest bear case visible, show scenario sensitivity, and state which facts would reverse the recommendation.

Frequently asked questions

How long does venture capital due diligence take?

There is no universal duration. Timing depends on company stage, sector, round complexity, data-room readiness, access to customers and experts, and the amount of legal or regulatory review. A focused seed process may be materially lighter than growth-stage diligence across multiple jurisdictions. Ask for a work plan and decision calendar rather than assuming a standard number of weeks.

Does due diligence happen before or after a term sheet?

Both patterns exist. Some firms complete substantial business diligence before issuing a term sheet and reserve confirmatory legal, financial, and technical work for afterward. Others will not issue terms until the key workstreams are substantially complete. The term sheet should state relevant conditions, and both sides should clarify what remains open.

Who performs due diligence at a VC firm?

The deal team coordinates the investment thesis and synthesis. Analysts and associates often handle research, models, references, and the issue log; partners assess the founders and own the final conviction. Lawyers, accountants, technical advisers, security specialists, and industry experts contribute transaction-specific expertise.

What should founders prepare for VC due diligence?

Prepare a clean cap table, financing history, core corporate records, founder and employee IP assignments, financial statements, budget and model, customer and pipeline evidence, product and security materials, key contracts, and a clear owner for requests. More importantly, make every number reconcilable and disclose known problems with a remediation plan.

What is different about technical or legal diligence?

Technical diligence tests architecture, product quality, security, scalability, technical debt, team capability, and IP provenance. Legal diligence verifies corporate authority, securities, ownership, contracts, employment and invention matters, disputes, and regulatory exposure. Both should be scoped by qualified specialists; a generic article checklist is not a legal or technical opinion.

The standard: proportional, traceable, decision-led

Strong VC due diligence does not eliminate uncertainty. It identifies which uncertainties matter, tests them with the best available evidence, and records how they affect the investment decision.

For analysts and candidates, the practical test is straightforward: take one important company claim and trace it through evidence, analysis, finding, downside, and recommendation. If that chain is clear, the diligence is doing useful work. If it ends at “documents reviewed,” it is not finished.