Investment Banking vs Venture Capital: Careers, Work, and How to Choose

Investment banking and venture capital both reward analytical judgment, but the work, feedback loops, recruiting paths, and career risks differ. Use this framework to choose.

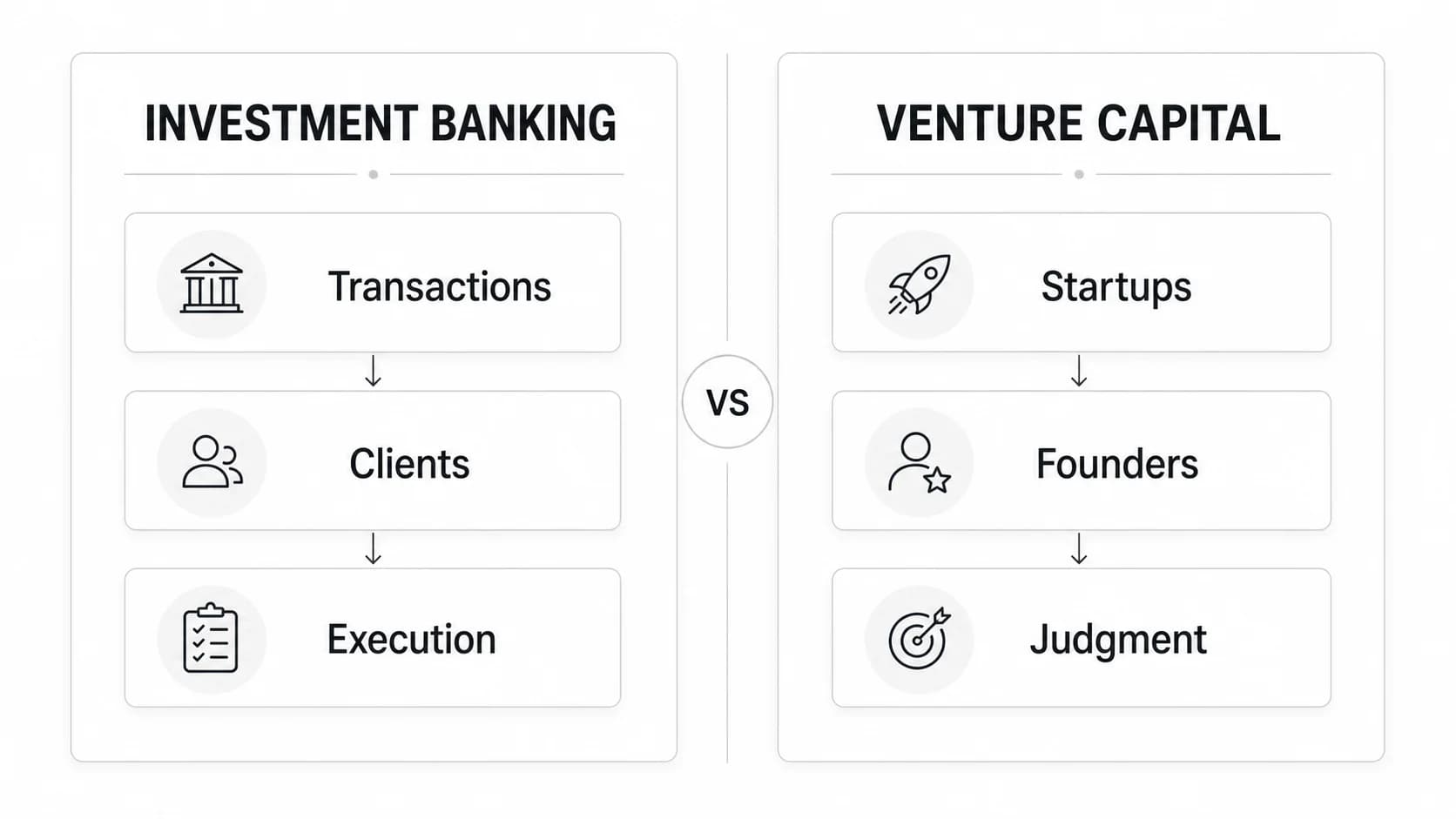

Investment banking and venture capital both sit close to important financing decisions, but they are different jobs. Investment bankers advise clients and execute transactions. Venture capital investors choose startups, deploy a fund's capital, and live with those decisions for years.

Choose investment banking if you want structured technical training, transaction deadlines, client service, and broad conventional finance exits. Choose venture capital if you want to form views on young markets, source companies, judge founders, and work inside a slower, less certain feedback loop.

| Dimension | Investment banking | Venture capital |

|---|---|---|

| Core business | Advising and executing transactions for fees | Investing a fund's capital for long-term returns |

| Typical junior output | Financial models, valuations, pitch books, process materials | Market maps, sourcing notes, investment memos, diligence, portfolio work |

| Primary stakeholder | Client and deal team | Investment team, founders, and portfolio companies |

| Feedback loop | Deadlines and completed transactions | Investment decisions and outcomes measured over years |

| Best fit | Detail-oriented executor who likes structure and pace | Curious investor who likes ambiguity, networks, and independent judgment |

| Common early-career exits | Private equity, corporate development, investing, finance roles | Other VC funds, startups, corporate venture, operating or ecosystem roles |

Neither path is universally better. The better choice is the work system that makes you sharper: repeated execution under pressure in banking, or repeated judgment under uncertainty in venture.

What investment bankers and venture capital investors actually do

FINRA's description of capital markets and investment banking includes M&A advice, underwriting, restructuring, valuation, IPOs, and capital-raising alternatives. That business model is transaction-driven. The bank wins mandates, serves clients, manages a process, and earns fees when work is performed or a deal closes.

A venture firm raises money from limited partners, builds a portfolio, and seeks returns from a relatively small number of successful outcomes. The National Venture Capital Association's explanation of the VC model emphasizes separate funds, long holding periods, limited liquidity, follow-on capital, and years of work with portfolio companies.

That distinction changes the employee experience. In banking, your work product helps a client make or complete a transaction. In VC, your work product helps the firm decide whether to own part of a company, how much conviction to express, and what to do after investing.

How the daily work differs

Investment banking: coordinated execution

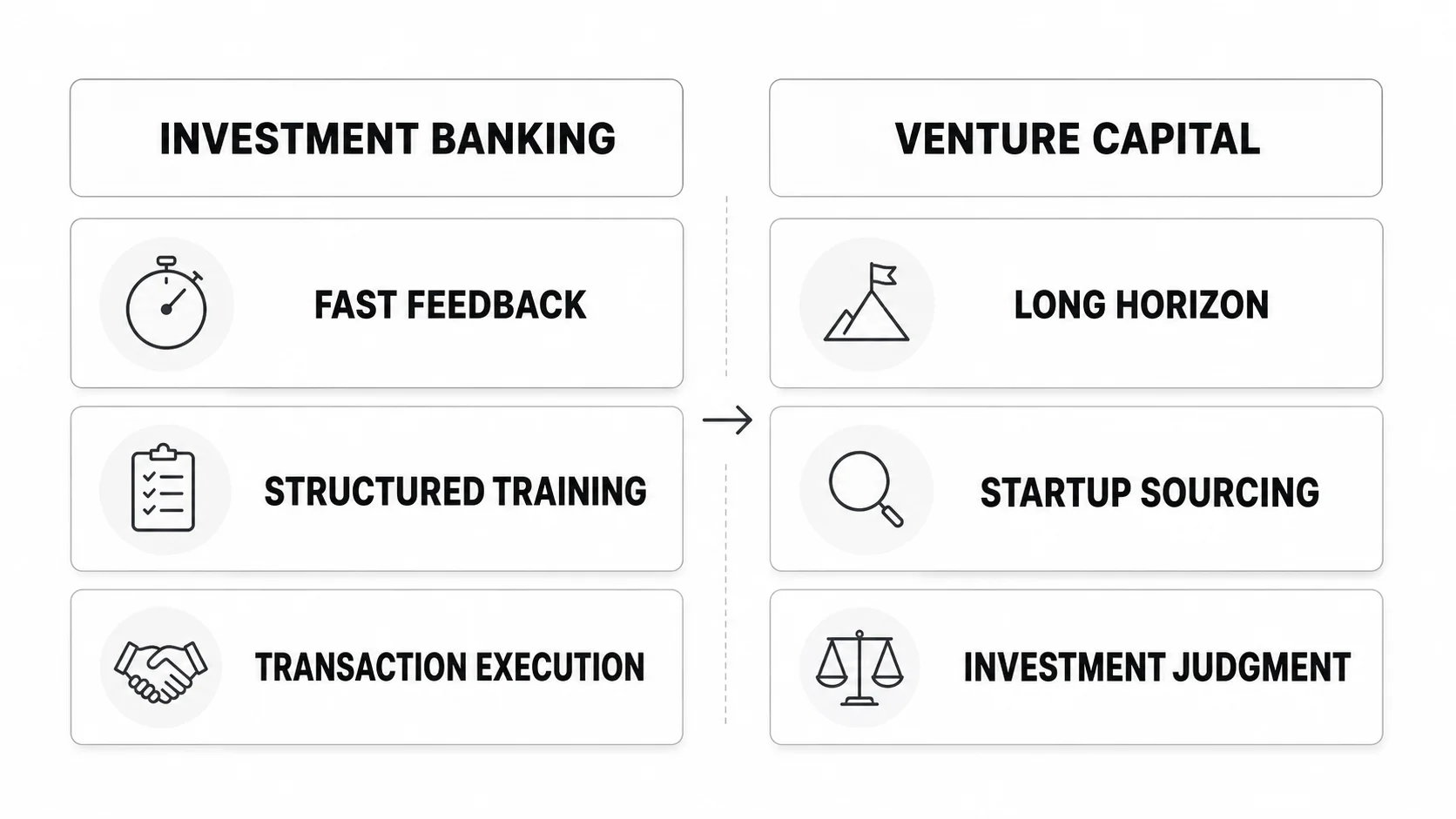

A banking analyst's calendar is shaped by live deals and senior requests. You may update a valuation, check a model, revise a management presentation, build buyer materials, coordinate diligence, or turn comments across several workstreams. The task changes, but the operating principle is consistent: accurate output, delivered on time, through a hierarchy.

The work is often highly reviewable. A formula ties or it does not. A slide matches the latest numbers or it does not. A process has a deadline. That creates fast feedback and a steep learning curve, even when the work is repetitive.

Venture capital: continuous judgment

A VC analyst or associate may source founders, screen inbound opportunities, research a market, take calls, write an investment memo, support diligence, prepare an investment committee discussion, or help a portfolio company. The mix depends heavily on fund stage and strategy.

At an early-stage fund, sourcing, market insight, founder assessment, and product judgment can outweigh complex financial modeling. At a growth-stage fund, cohort analysis, scenario modeling, ownership, dilution, and exit assumptions may look more familiar to a banker. "Venture capital" is not one job; a seed generalist and a growth investor can have very different weeks.

The hidden variable: feedback-loop speed

Banking gives frequent process feedback. Your team knows whether the model, deck, or transaction step is ready. Venture gives frequent feedback on the quality of your thinking, but slow feedback on whether the original investment was right. A company may look weak for several quarters before breaking out, or look exceptional before failing.

If you need short cycles to stay motivated, banking can feel clearer. If you enjoy updating a thesis while the answer remains unknowable, VC can feel more engaging. Many candidates mistake "interest in startups" for comfort with that long feedback loop. They are not the same.

Skills and evidence firms hire for

Both careers value analytical ability, communication, reliability, and commercial judgment. The weighting differs.

| Evidence to build | Investment banking | Venture capital |

|---|---|---|

| Analytical work | Three-statement model, valuation, transaction analysis | Market map, cap table, scenario model, investment memo |

| Written communication | Tight slides and defensible assumptions | Clear thesis, concise memo, specific risk framing |

| External skill | Client readiness and process discipline | Founder access, sourcing, expert network, relationship judgment |

| Interview proof | Technical accuracy and structured answers | Point of view, company judgment, sector curiosity, deal discussion |

| Execution signal | Detail control under deadline | Ability to find, assess, and advance an opportunity |

Banking rewards precision that survives review. You need to make a large process more reliable: catch inconsistencies, understand valuation, communicate changes, and keep workstreams moving.

VC rewards selective conviction. You need to notice what matters before the evidence is complete, articulate why a market or company may be unusual, identify the strongest counterargument, and change your mind when new facts arrive. The most useful venture capital skills combine analysis with sourcing, communication, and judgment.

Do not use one generic resume for both paths. A banking resume should make execution and technical rigor visible. A VC resume should make your investing wedge visible: a sector you understand, companies you sourced, memos you wrote, founders you know, or operating experience that changes how you assess a market.

The same project can be framed differently. A fintech market study is evidence of modeling and transaction knowledge for banking; for VC it becomes useful only when it shows a non-obvious thesis, a company pipeline, and a decision about where value will accrue.

Recruiting and interviews

Investment banking recruiting is comparatively standardized. Large banks recruit on predictable campus calendars, test accounting and valuation concepts, and run structured interview processes. Candidates know the technical curriculum, even if the competition is intense.

VC recruiting is fragmented. A large multi-stage firm may run an organized process; a small seed fund may hire only when a partner needs leverage. Roles can arrive through job boards, recruiters, referrals, founder networks, or direct outreach. The title alone does not tell you whether the job is mostly sourcing, diligence, portfolio support, or platform work.

Expect banking interviews to test whether you can perform accurately inside a demanding transaction team. Expect VC interviews to test whether you can think like that specific fund. Common evidence includes:

- a company or sector you would invest in;

- a market map or sourcing exercise;

- an investment memo or case study;

- portfolio-company opinions;

- a clear explanation of why the fund's stage, sector, and strategy fit you;

- evidence that founders or experts will take your call.

Use the VC case study interview guide to prepare a decision, not just an analysis. A strong candidate can say what they would do, what would change their mind, and which risk deserves the next diligence hour.

For live VC opportunities, research firms through the Venture Capital Careers companies directory and compare job descriptions on the VC job board. Read the mandate carefully: a growth-equity role may prize banking experience, while a pre-seed role may value community access or operating depth more.

Compensation, career capital, and risk

Banking compensation is usually easier to understand early in a career: base salary plus an annual bonus, with a relatively visible promotion ladder. Venture compensation may include salary and bonus, and some roles include carried interest. Carry is not cash today. It is contingent on fund performance, vesting terms, and exits that may take years.

Avoid choosing between the careers using one headline salary comparison. Firm size, geography, seniority, fund economics, bonus year, and carry eligibility can move the result. For current VC role bands and the mechanics behind them, use the venture capital salary guide.

Career capital matters as much as first-year pay.

Banking builds a legible credential, transaction exposure, financial fluency, and a network across clients and deal professionals. That package can preserve conventional exits into private equity, corporate development, growth investing, and other finance roles.

VC builds a different asset base: founder relationships, sector pattern recognition, sourcing credibility, investment judgment, and a record of portfolio decisions. Those assets can compound inside venture and startups, but they may be less standardized to employers outside the ecosystem.

The risk tradeoff is therefore personal. Banking often asks for more predictable sacrifice in exchange for standardized training and signaling. VC can offer closer contact with innovation and more ownership of ideas, but the learning experience varies more by partner, fund quality, role design, and deal flow.

How to choose between investment banking and venture capital

Score each statement from 1 (not like me) to 5 (very like me).

| Statement | Points toward |

|---|---|

| I enjoy exact deliverables, rapid review, and hard deadlines. | Investment banking |

| I want structured training before specializing. | Investment banking |

| I prefer transactions with defined clients and processes. | Investment banking |

| I naturally track startups, products, founders, and emerging markets. | Venture capital |

| I can stay engaged when the answer may take years to emerge. | Venture capital |

| I enjoy forming a view from incomplete evidence and defending it. | Venture capital |

Do not total the scores blindly. Look for the strongest mismatch. If you love startups but dislike outbound relationship-building, many early-stage VC roles will frustrate you. If you want banking's credential but hate iteration, hierarchy, and deadline-driven client service, the training may not compensate for the daily experience.

Use these decision rules:

- Choose banking when you are undecided and genuinely want its technical and transaction training, not merely because it appears safer.

- Choose VC when you already demonstrate a repeatable startup or sector edge, not merely because the industry looks interesting.

- Prefer growth-stage VC if you like private-company investing but want more quantitative diligence and financial analysis.

- Prefer early-stage VC if you like sourcing, product judgment, founder conversations, and market formation.

- Do not choose either path for prestige. Prestige will not make repetitive work interesting or a long feedback loop tolerable.

A 30-day test before you choose

You do not need an offer to sample the work. Run two small projects and compare your behavior, not your stated preference.

Banking track

Choose a public company and build a compact valuation pack:

- a simple operating forecast;

- trading comparables;

- a basic discounted cash flow or transaction-style valuation;

- a five-slide summary with assumptions, valuation range, and key sensitivities.

Set a deadline. Review every formula and number as if a senior banker will challenge it. Note whether the precision and revision process energizes you or drains you.

Venture track

Choose one early-stage market and build an investment pack:

- a market map of 25 to 40 relevant companies;

- a one-page thesis with a non-obvious view;

- three founder or expert conversations;

- a short memo on one company with a clear invest/pass recommendation;

- a list of facts that would change your decision.

Use the venture capital investment memo guide if you need a structure. Notice whether sourcing, ambiguity, and the need to take a position pull you forward.

At the end of the month, score both projects on four questions:

1. Which work did you continue after the planned time ended? 2. Which feedback made you want to improve rather than disengage? 3. Which output would you be proud to show a professional? 4. Which weaknesses are trainable, and which reflect a genuine dislike of the work?

This test cannot reproduce a live deal or investment committee. It can reveal whether you like the core loop enough to tolerate the difficult parts.

Can you move from investment banking to venture capital?

Yes. Banking to VC is a common enough transition because financial analysis, diligence, transaction exposure, and professional discipline transfer. The move is not automatic. Early-stage firms may still question your sourcing ability, product judgment, founder network, and willingness to make decisions without a mature financial history.

The reverse move—from VC into investment banking—is possible but less standardized. You may need to prove technical readiness, explain why you want client-service and transaction work, and enter through a role or level that matches your experience.

If you have already chosen the move, follow the dedicated investment banking to venture capital guide. It covers how to translate banking experience, close the sourcing gap, and target funds where your deal background is useful.

FAQ

Is investment banking or venture capital harder to get into?

Both are competitive. Banking has more structured entry points and a better-known interview curriculum. VC has fewer roles and more idiosyncratic hiring, so a strong candidate can still struggle if their sector, stage, geography, or network does not match the fund.

Does investment banking pay more than venture capital?

Banking often has a more standardized early-career cash-compensation structure. VC pay varies widely, and carry may add long-term upside without being guaranteed or liquid. Compare actual offers, responsibilities, learning, and vesting terms rather than industry averages.

Does venture capital have better hours than investment banking?

It often has fewer transaction-driven late nights, but that is not a promise. Fund culture, live deals, portfolio issues, travel, events, and sourcing expectations matter. Ask how the team works during diligence and how junior performance is measured.

Which path is better for entrepreneurship?

VC offers more exposure to founders and young companies; banking builds transaction and finance discipline. Neither replaces operating experience. The better preparation depends on whether your future company will benefit more from market pattern recognition and networks or from capital-markets and execution knowledge.

Which career keeps more options open?

Banking usually preserves more standardized finance exits early on. VC builds deeper startup and investing-specific capital. Optionality is useful only if you can perform well enough to earn it, so choose the path whose daily work you are more likely to master.

Your next step

If VC is the stronger fit, review the venture capital career path, research funds in the companies directory, and browse current roles on Venture Capital Careers. Create a profile and alerts through candidate sign-up so your search is not dependent on one recruiting cycle.

If banking is the stronger fit, commit to the technical and transaction curriculum instead of treating the role as a waiting room for VC. You can revisit venture later with real deal experience and a sharper explanation of where you add investing value.