Venture Capital Salary Guide: Roles, Bonuses, Carry, and Progression

Venture capital salary ranges by role, bonus, carry, fund size, and career progression, with a practical framework for evaluating VC compensation offers.

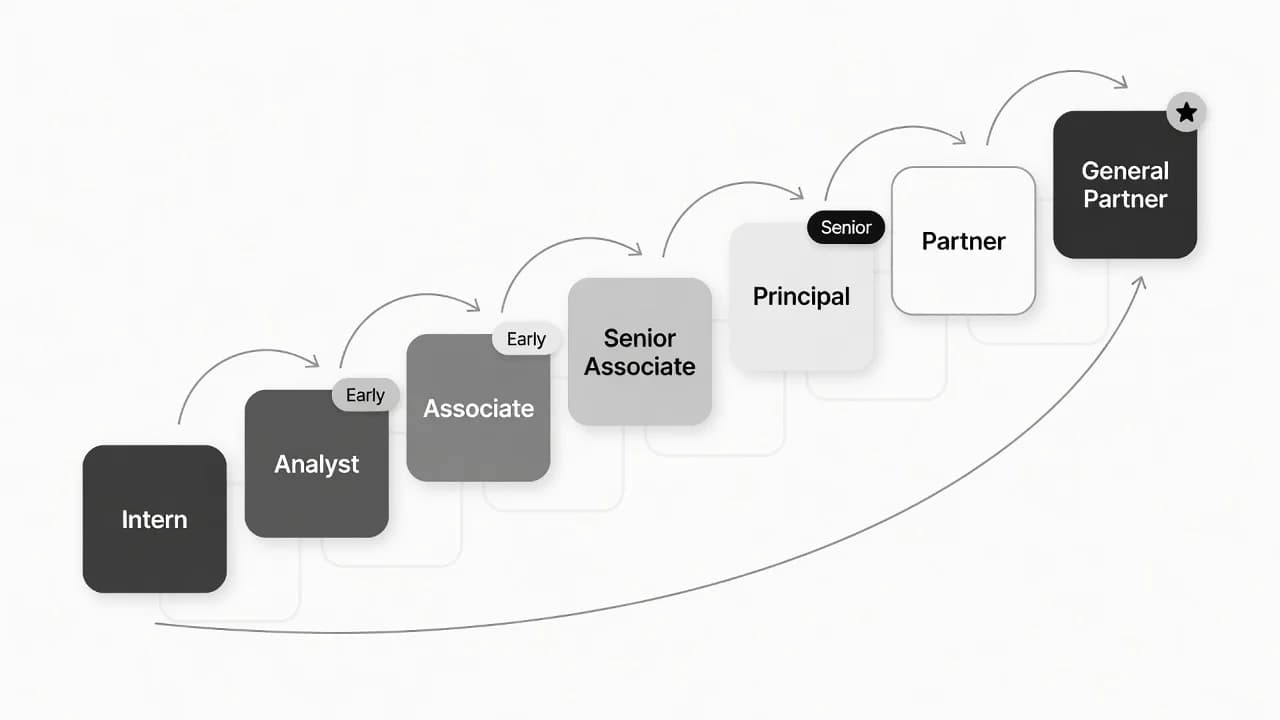

Venture capital salaries usually progress from analyst and associate cash compensation to principal-level responsibility and, eventually, partner-level carry. For most candidates, the practical question is not "how much do venture capitalists make?" It is which part of the package is dependable cash, which part is performance-based bonus, and which part is long-dated fund upside.

In the US market, junior VC investment roles often sit below investment banking or private equity cash pay, especially at smaller funds. The tradeoff is earlier exposure to startups, sourcing, investment judgment, portfolio work, and a possible path toward carry. That tradeoff can be attractive, but it should be evaluated with clear numbers.

The ranges below are directional. Venture capital compensation changes by fund size, stage focus, city, role scope, carry policy, and market cycle. Current survey pages such as Venture5's 2025 VC Salary Survey also show that cash compensation can soften below partner level when hiring slows or firms automate more junior work.

Venture capital salary progression by role

Use this table as a practical US-market benchmark for investment roles. It is not a promise of what any single fund will pay.

| Role | Typical base salary | Typical bonus | Carry access | What usually drives the range |

|---|---|---|---|---|

| Analyst | $70K-$115K | $5K-$25K | Rare | Market research, sourcing, CRM work, memo support, fund size, city |

| Associate | $100K-$175K | $10K-$50K | Sometimes small or deferred | Deal screening, diligence, founder calls, prior banking, consulting, startup, or MBA experience |

| Senior associate | $140K-$210K | $20K-$75K | More possible, still not guaranteed | Independent sourcing, investment memos, portfolio support, promotion path |

| Principal or VP | $175K-$275K | $30K-$125K | Often meaningful if the role is partner-track | Ownership of sectors, deals, boards, founder relationships, and internal conviction |

| Partner or GP | $250K-$600K+ cash, with wide variation | Highly variable | Core economics | Fund size, management fees, ownership in the GP, carry split, realized exits |

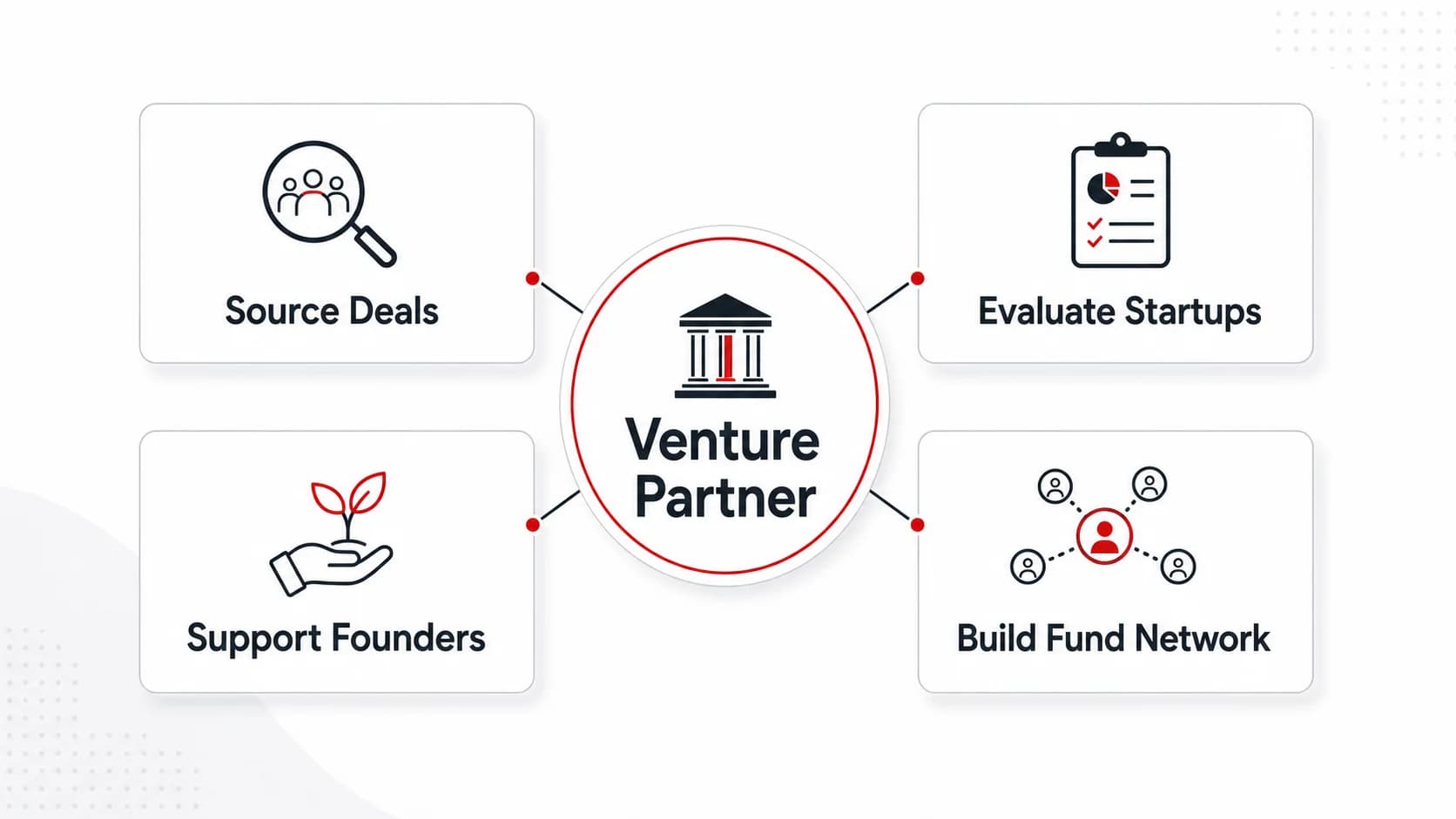

| Venture partner | Highly variable | Highly variable | Deal-by-deal or fund-specific | Part-time versus full-time role, sourcing expectations, operating background |

The table is intentionally broad because VC firms are not standardized employers. A small seed fund with $25 million under management cannot pay like a multibillion-dollar platform. A corporate venture capital team may pay more like a corporate finance or strategy role. A growth fund may pay closer to private equity because it manages larger checks and later-stage companies.

The strongest compensation packages are usually attached to one of three things: a larger fee base, a clear partner track, or valuable carry. A higher base salary can be helpful, but it is not the whole answer if the role has no promotion path, no carry participation, and little responsibility close to investment decisions.

What changes as you move up the VC ladder

At the analyst level, pay is mostly cash because the work is mostly support. Analysts build market maps, update deal pipelines, research sectors, help with memos, and track startup activity. The role can be valuable, but it rarely creates enough investment ownership to justify meaningful carry.

Associates usually move closer to investment judgment. They screen companies, talk to founders, prepare diligence materials, and help partners decide which companies deserve more time. Associate compensation rises when the person can source credible opportunities, write useful memos, and support a partner without constant direction.

Senior associates, principals, and VPs start to get paid for judgment rather than only output. They may own themes, build founder relationships, lead parts of diligence, and represent the firm in the market. At this point, the question becomes whether the role is genuinely partner-track or simply a senior execution role with limited economics.

Partner compensation is different. Partners are paid for raising capital, winning allocation into competitive rounds, making investment decisions, supporting portfolio companies, and returning capital to LPs. Cash compensation can be high at established funds, but the real upside is usually carried interest.

For a fuller view of titles and promotion paths, pair this article with the venture capital career path guide.

How VC bonuses and carry work

VC bonuses are usually less formulaic than investment banking bonuses. A junior investor may receive a bonus based on firm performance, individual contribution, sourcing quality, investment activity, or a discretionary year-end decision. The range is often smaller than banking, and some emerging funds keep bonuses modest to preserve fee budget.

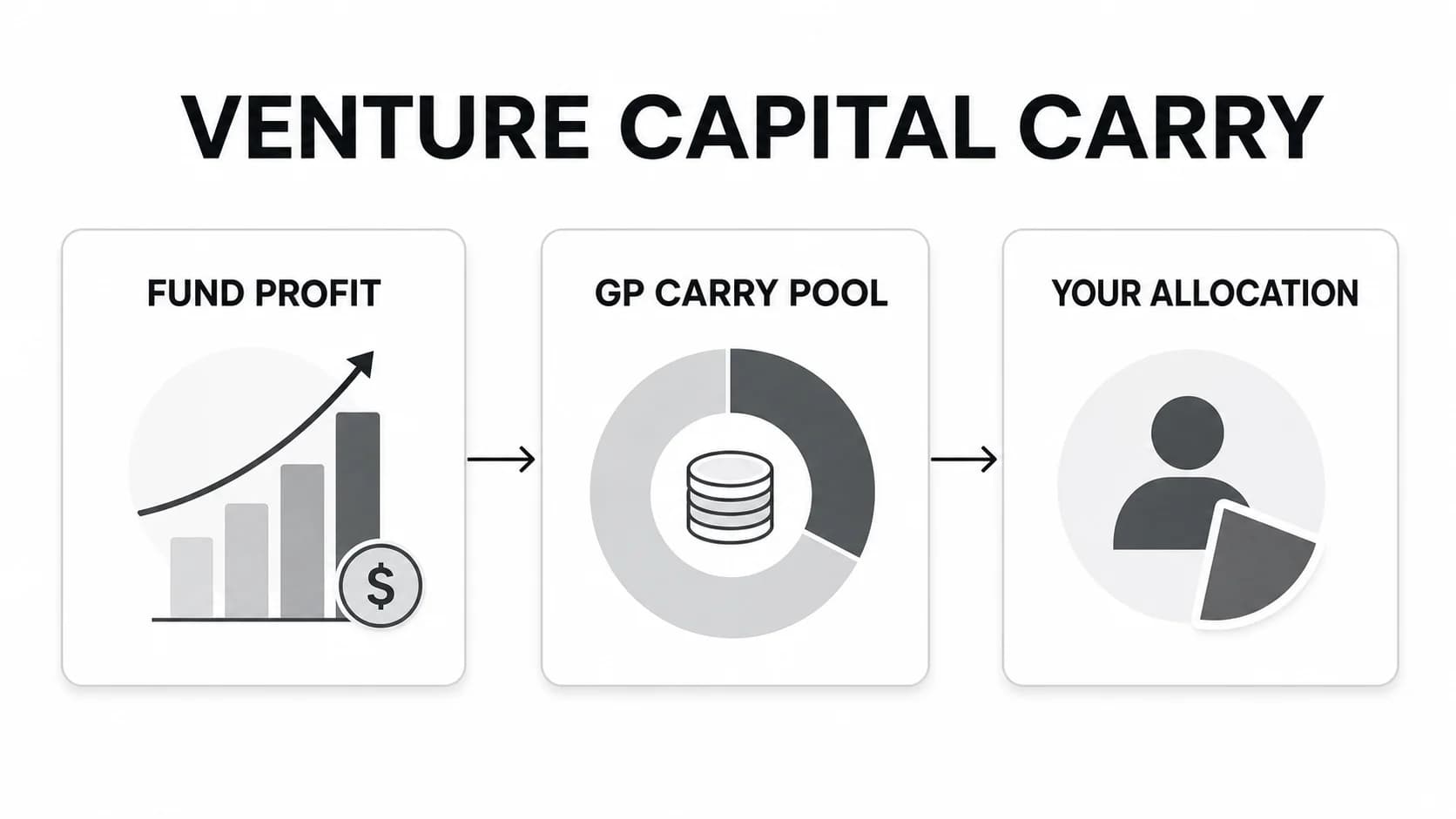

Carry is the more misunderstood part of VC pay. Carried interest is a share of fund profits after investors receive their capital back and the fund clears its economic hurdles. It can be very valuable, but it is not the same as annual cash compensation.

Three carry questions matter more than the headline percentage:

- When does it vest? Carry may vest over several years and may be tied to staying at the firm.

- What fund does it apply to? Carry in an older fund may be less valuable if most investments are already marked or allocated.

- How likely is it to pay out? Paper gains do not pay rent. Realized exits, fund performance, and timing matter.

Junior employees sometimes receive small carry allocations, but they should not treat carry as guaranteed compensation. At many funds, analyst and associate carry is symbolic, deferred, or absent. At principal level and above, carry can become a real part of the package if the person is on a credible investment-track path.

Venture capital partner compensation

Venture capital partner compensation is best understood through fund economics. A fund typically charges management fees to run the firm and pays carry if the fund produces profits. The public explanation from SaaStr is useful because it starts with the fee base: a small fund has a much smaller annual budget for salaries, rent, travel, software, and operations than a large fund.

That is why two partners with the same title can have very different compensation. A partner at a large, established firm may earn a substantial cash salary and have meaningful carry across multiple funds. An emerging manager may take much less cash because management fees are thin and the real upside depends on future exits.

For partner roles, ask four questions:

- What is the current fund size and fee structure?

- Is the partner an employee, venture partner, junior partner, general partner, or owner of the management company?

- How is carry split across the partnership?

- Is the carry tied to one deal, one fund, or multiple funds?

The headline "VC partner salary" is often misleading because the largest outcomes come from carry, not salary. A partner can have modest annual cash relative to a tech executive and still build meaningful wealth if the fund produces exceptional realized returns. The reverse is also true: a high-status title without carry may be less attractive than it looks.

What affects VC compensation

The same title can mean different things at different funds. Before comparing offers, adjust for the variables that actually drive pay.

| Factor | Why it matters |

|---|---|

| Fund size | Larger funds usually have more management-fee budget and can support higher cash compensation. |

| Stage focus | Growth and late-stage funds often pay more cash than small pre-seed funds, but may offer different upside. |

| Geography | San Francisco, New York, Boston, and other major VC hubs often pay more, partly because competition and cost of living are higher. |

| Firm maturity | Established firms may offer better cash stability; emerging managers may offer faster responsibility and more asymmetric carry. |

| Role scope | A sourcing-only title is different from a role that owns diligence, memos, boards, and portfolio work. |

| Market cycle | Hiring slowdowns, fund performance, and automation can pressure junior cash compensation. |

Venture5's public 2025 survey summary says its survey included 700+ professionals and 50+ firms, and it highlights softer cash compensation below partner level. That does not mean every junior offer is down. It does mean candidates should avoid anchoring on peak-market numbers or anonymous forum anecdotes.

How to evaluate a VC compensation offer

Do not evaluate a VC offer only by base salary. A lower base can be reasonable if the role is closer to investment decisions, has credible promotion potential, and includes meaningful economics. A higher base can still be a poor offer if the role is mostly support work with no path to carry.

Use this checklist before accepting:

| Question | Why it matters |

|---|---|

| What is the base salary and expected bonus range? | Separates dependable cash from discretionary upside. |

| Is bonus formulaic or discretionary? | Tells you whether performance has a clear payout mechanism. |

| Is there carry? | Determines whether long-term fund upside exists. |

| If there is carry, what fund, vesting schedule, and forfeiture terms apply? | Prevents confusing theoretical carry with practical value. |

| What investment work will you own in the first year? | Salary matters less if the role does not build investment judgment. |

| Who sponsors promotion decisions? | VC firms are small, and advancement often depends on partner sponsorship. |

| How does the firm define success for this role? | Sourcing volume, memo quality, portfolio support, and network building imply different career paths. |

If the firm will not discuss bonus range, carry eligibility, or promotion criteria, treat that as useful information. Small funds may not have perfect compensation infrastructure, but they should still be able to explain how the role creates value and how strong performance is rewarded.

How salary should shape your VC job search

Salary research should narrow your search, not replace it. A candidate optimizing for immediate cash may prefer growth equity, late-stage VC, corporate venture, investment banking, or private equity. A candidate optimizing for startup exposure, thematic investing, founder relationships, and long-term carry may accept a lower cash package for a better investing seat.

Use Venture Capital Careers to browse open VC roles and compare titles, responsibilities, and firm types. When reading job descriptions, look for clues that affect compensation:

- Analyst roles that mention sourcing, market maps, and CRM ownership are likely more junior and cash-heavy.

- Associate roles that mention diligence, investment memos, and founder calls may build faster toward investment judgment.

- Principal or VP roles should show ownership of sectors, deals, portfolio work, or partner-level leverage.

- Platform, talent, operating, and portfolio support roles may have different compensation bands than investment roles.

You can also use the companies directory to research firms before comparing offers. Fund stage, geography, and firm maturity often explain more about compensation than the title alone.

For role-specific context, review the venture capital analyst job description and venture capital associate job description before negotiating.

Frequently asked questions

What is the average VC associate salary?

A US VC associate commonly lands somewhere around the low six figures to the mid-$100Ks in base salary, with bonus potential on top. Total cash can move higher at large institutional funds, growth funds, and major VC hubs. Smaller seed funds may pay less but offer faster responsibility or some carry participation.

How much do VC principals make?

VC principals and VPs often earn meaningfully more than associates because they are closer to investment ownership. Directionally, base salary may sit in the high-$100Ks to mid-$200Ks, with bonus and carry varying widely. The real question is whether the role is partner-track.

What is a typical VC bonus?

VC bonuses are often discretionary and can range from modest to meaningful depending on role, firm performance, and individual contribution. Junior bonuses may be smaller than investment banking bonuses. Senior bonuses can be larger, but carry and fund economics become more important than annual bonus alone.

Do junior VC employees get carry?

Sometimes, but it is not guaranteed. Analysts rarely receive meaningful carry. Associates may receive small allocations at some firms. Principals, VPs, and partners are more likely to receive carry, but the terms matter: vesting, fund vintage, forfeiture, and expected exit timing can change the value dramatically.

Is venture capital compensation higher than private equity?

Usually not at the junior level. Private equity and investment banking often pay more predictable cash compensation. Venture capital may offer better startup exposure, more qualitative investing work, and long-term carry upside, but candidates should be honest about the cash tradeoff.

How do venture partners get paid?

Venture partner compensation varies widely. Some venture partners receive cash retainers, some receive deal-by-deal economics, some receive carry allocations, and some are part-time advisors with limited guaranteed compensation. Always clarify whether the title is full-time, part-time, sourcing-focused, operating-focused, or partner-track.