Venture Capital Principal Job Description: Responsibilities, Skills, and Template

A practical guide to the VC Principal role, including decision authority, responsibilities, qualifications, compensation, a copy-ready job description, and a hiring scorecard.

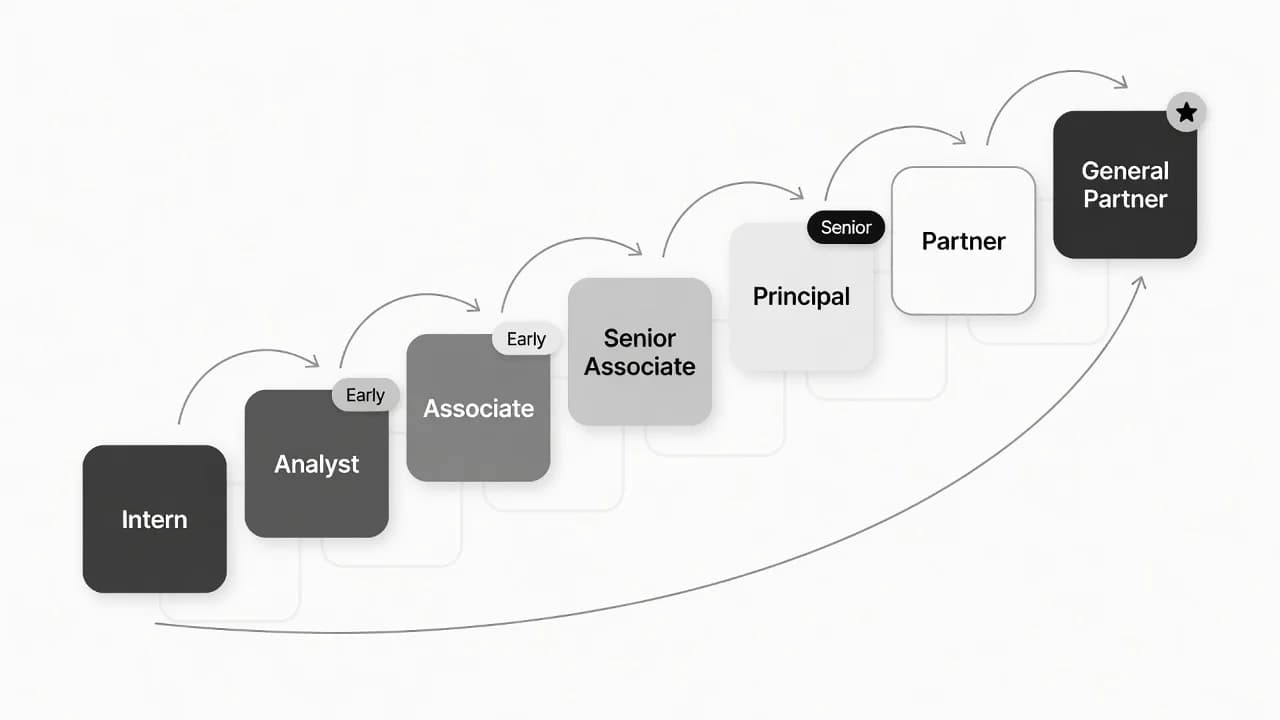

A venture capital Principal is a senior investment professional who typically sits between Associate and Partner. Principals source opportunities, lead diligence and deal execution, support portfolio companies, and help turn a fund's investment thesis into decisions. They usually have more ownership than Associates but less final authority than General Partners.

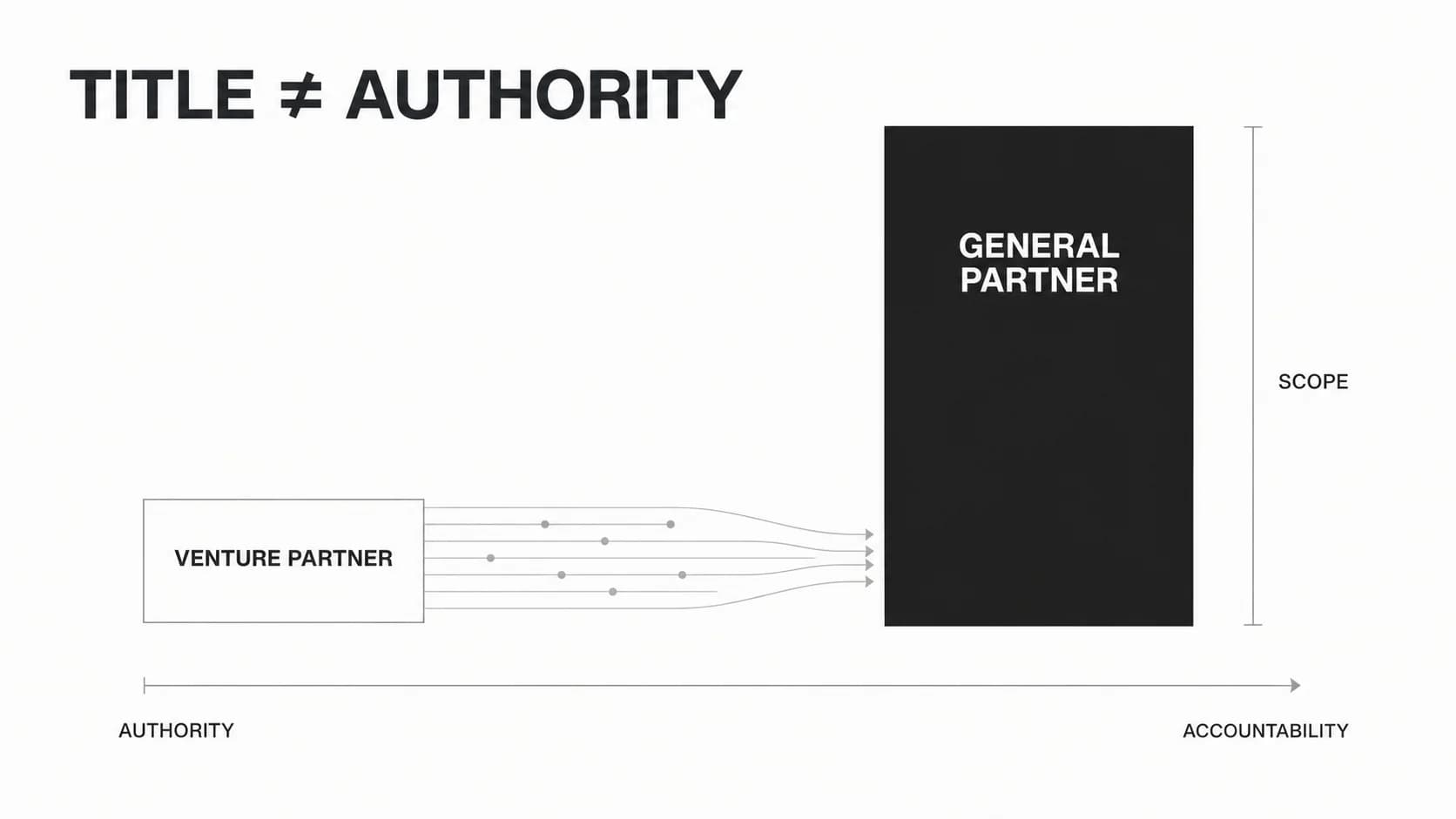

The title is not standardized. At one firm, a Principal may vote in investment committee meetings, negotiate term sheets, and hold board seats. At another, the same title may mean senior execution work without approval authority. Candidates should judge the mandate by decision rights, carry, and promotion criteria—not the title alone. Hiring firms should make those terms explicit.

Candidates can browse current VC roles and research venture firms. Firms hiring at this level can use the template and scorecard below.

What is a venture capital principal?

The Principal is the hinge between analysis and partnership-level accountability. Associates often gather evidence, build models, and draft investment materials. Partners set fund strategy, raise capital, and carry final responsibility for investment and management-company decisions. Principals increasingly own the judgment and coordination between those layers.

That usually means a Principal can take a company from first meeting to an investment-committee recommendation. The Principal may direct the diligence plan, challenge the market thesis, negotiate major terms, coordinate counsel, and become the founder's day-to-day investor after closing. Whether that person can approve or sign the investment depends on the firm.

The most reliable way to understand the role is an authority test:

| Area | Typical Principal ownership | What varies by firm | Question to ask |

|---|---|---|---|

| Sourcing | Builds sector relationships and originates credible opportunities | Individual sourcing targets and attribution rules | What counts as a sourced deal, and how is credit assigned? |

| Investment committee | Presents recommendations and defends the investment case | Observer, non-binding voice, formal vote, or delegated approval | Does the Principal vote, recommend, or only present? |

| Deal authority | Leads diligence, term-sheet work, and closing coordination | Check-writing limit, signature authority, and Partner oversight | What can the Principal approve without a Partner? |

| Portfolio governance | Owns founder relationships and operating follow-through | Informal support, board observer, or director seat | Which companies and governance rights will the Principal hold? |

| Fund economics | Usually earns salary, bonus, and some form of long-term upside | Carry pool, vesting, co-invest, clawback, and departure treatment | What does the carry percentage refer to, and when does it vest? |

| Firm building | Mentors junior investors and develops a sector or thesis | LP exposure, fundraising, hiring, and budget ownership | Which firm-level outcomes determine promotion? |

Some funds use Vice President or Director for substantially the same level. Others split those titles into separate rungs. “Junior Partner” can also describe a Principal with more authority or economics, but it may still fall short of full General Partner status. A useful VC career path should therefore be read as a common pattern, not an industry-wide org chart.

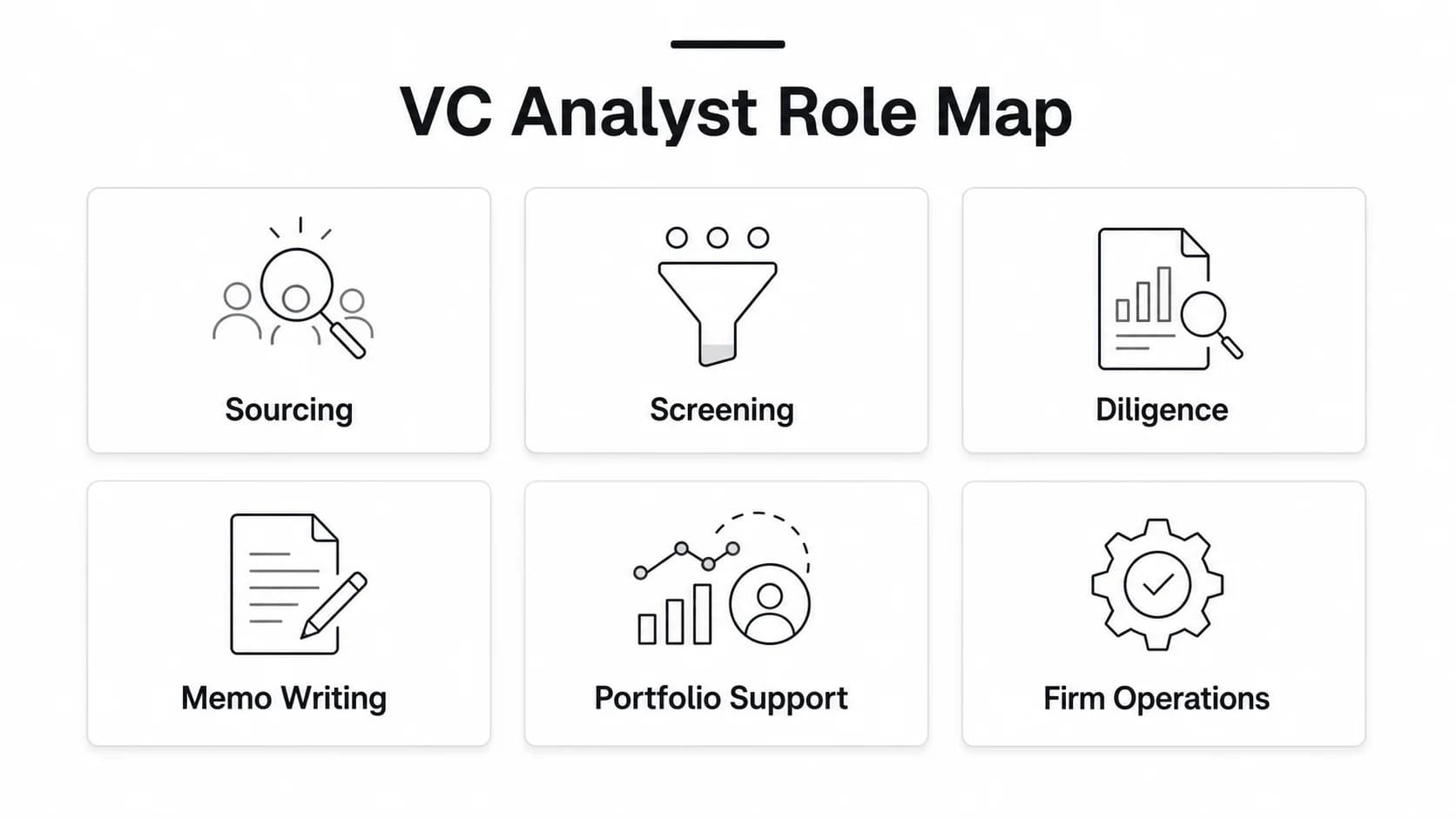

Venture capital principal responsibilities

A strong job description should distinguish work the Principal owns from work the person merely supports. “Assist with sourcing and diligence” is too junior and too vague. “Originate qualified opportunities, set the diligence plan, and lead recommendations to the investment committee” defines accountability.

Build a differentiated sourcing engine

Principals are expected to create access, not simply process inbound decks. That can include developing a sector thesis, building relationships with founders before they raise, maintaining trusted connections with operators and co-investors, and representing the fund in a focused ecosystem.

The output is not meeting volume. It is a pipeline of opportunities that fit the fund's stage, geography, ownership targets, check size, and return model. A posting should clarify whether success means proprietary origination, sector coverage, local ecosystem presence, or conversion from first meeting to Partner review. For practical methods, see the VC deal-sourcing framework.

Lead investment analysis and due diligence

The Principal converts interest into an investable recommendation. They define the open questions, assign work across the deal team, and decide which evidence would change the recommendation. Typical areas include market structure, customer pain, product differentiation, founder-market fit, unit economics, financing needs, ownership, downside cases, and exit potential.

At this level, the job is not to perform every analysis personally. It is to design a decision-quality process, inspect the work, and make the judgment legible to the partnership. The Principal should be able to turn that work into a concise investment memo and defend what remains uncertain. The venture capital due-diligence process is a useful adjacent workflow.

Drive investment-committee decisions and deal execution

Principals commonly present the investment case, address objections, and maintain the link between diligence findings and proposed terms. Once the firm decides to proceed, they may lead term-sheet negotiation, coordinate legal and financial workstreams, manage syndicate relationships, and keep the deal moving toward close.

The posting must say where authority stops. A Principal who can negotiate within an approved range has a different mandate from one who only prepares the Partner for negotiations. Neither model is inherently wrong; ambiguity is.

Support portfolio companies and boards

After investment, Principals often become the most frequent contact between the firm and the company. They may help with executive hiring, follow-on financing, customer introductions, strategic planning, metrics, governance preparation, or acquisition discussions. They also surface risks to the partnership and recommend reserve or follow-on decisions.

Avoid promising that the Principal will “add value” across every operating function. Define the fund's actual support model, expected portfolio load, and whether the person will hold board-observer or director seats.

Develop the team, thesis, and firm

A partner-track Principal should make the investment platform better, not just complete personal deals. Common responsibilities include coaching Analysts and Associates, improving memo and pipeline standards, publishing credible sector work, recruiting investment talent, contributing to portfolio reviews, and representing the firm with founders, co-investors, and sometimes LPs.

Fundraising responsibility should be stated carefully. A Principal may contribute case studies, data, or sector expertise to LP conversations without owning the fundraise. If LP relationship development is part of the promotion case, say so.

Principal vs Associate vs Partner

The practical difference is not who attends the meeting. It is who owns the recommendation, who can commit the firm, and who carries the consequences.

| Dimension | Associate | Principal | Partner / General Partner |

|---|---|---|---|

| Primary job | Research, diligence, sourcing support, and execution | Origination, judgment, deal leadership, and portfolio ownership | Fund strategy, final decisions, fundraising, and partnership leadership |

| Deal autonomy | Runs defined workstreams | Designs and leads the full process, usually with Partner oversight | Sets approval boundaries and commits the firm |

| Investment committee | Prepares analysis; may present sections | Leads the recommendation; vote varies | Holds formal decision authority in most firms |

| Founder relationship | Supports meetings and follow-up | Often the day-to-day senior investor | Owns the highest-stakes relationship and firm commitment |

| Board work | Limited; sometimes observer exposure | Observer or director depending on mandate | Commonly director or senior sponsor |

| Team leadership | May guide Analysts or interns | Manages and develops the deal team | Builds the organization and partnership |

| Fundraising / LP work | Rare | Selective exposure or supporting role | Core responsibility |

| Economics | Salary and bonus; carry varies | Salary, bonus, and typically more meaningful carry | Management-company economics and the largest carry allocation |

| Success test | Quality and reliability of work | Investment judgment, sourced opportunities, portfolio outcomes, and leadership | Fund performance, fundraising, franchise strength, and succession |

A Principal is usually senior to an Associate and junior to a Partner. VP and Director cannot be placed reliably without firm-specific context. The same warning applies to Venture Partner, which is often a part-time or specialized affiliation rather than a rung immediately above Principal. For the senior role, compare the venture capital Partner job description.

Qualifications and skills firms should require

Principal hiring often fails when a firm screens for pedigree instead of evidence. An MBA, investment-banking background, or brand-name employer can be useful, but none proves that a person can originate a venture opportunity, make a decision under uncertainty, earn founder trust, or lead a deal team.

Evidence of investment judgment

Ask for two or three decisions the candidate can unpack: one pursued, one declined, and one that changed after new evidence. Strong candidates explain the original thesis, the disconfirming evidence they sought, the decision they made, and what later outcomes taught them. They do not hide behind a firm's track record or claim sole credit for a team decision.

Repeatable sourcing and relationship depth

“Strong network” is not a qualification until the candidate can show how it produces relevant access. Look for a clear market map, trusted relationships in the fund's focus area, examples of pre-process founder engagement, and a repeatable method for maintaining those relationships. The evidence should match the mandate: a seed fund may value early technical communities; a growth fund may require executive and later-stage investor networks.

Deal leadership and written thinking

The candidate should be able to scope diligence, prioritize the few questions that drive the return case, review quantitative work, write a sharp recommendation, and negotiate without damaging the founder relationship. A sanitized investment memo or live case discussion reveals more than finance trivia.

Founder empathy and portfolio effectiveness

Portfolio work requires judgment about when to advise, when to introduce, when to challenge, and when to stay out of the way. References from founders and former colleagues should test whether the candidate follows through, handles difficult news, and can distinguish governance from operating the company.

Team leadership and firm contribution

Principals multiply—or consume—junior-team capacity. Look for evidence that the candidate sets clear workstreams, improves analysis, gives useful feedback, and shares credit. Partner-track hires should also show a credible point of view the firm needs: a sector, geography, network, operating capability, or investment approach.

Relevant investing experience is usually the cleanest preparation, but it is not the only route. Senior operators, founders, product leaders, scientists, clinicians, or other domain experts can enter at Principal when their investment judgment and relationship advantage are already visible. Make prior VC experience mandatory only when the role truly requires immediate fluency in fund process and deal leadership.

Compensation, carry, and the path to Partner

Principal compensation usually combines base salary, a cash bonus, and long-term economics such as carry. Some firms also offer co-invest rights or deal-specific participation. The mix can change materially with fund size, geography, strategy, seniority, and whether the firm treats Principal as a terminal role or a partnership pipeline.

That variation makes a single headline salary range less useful than a complete offer. Firms should disclose or explain:

- The base-salary range and location policy.

- The target bonus, how it is determined, and whether it depends on individual or fund performance.

- Whether carry is included, which fund or pool it covers, and whether the quoted percentage is of the total fund, the carry pool, or a role-level pool.

- The vesting schedule, cliff, treatment of vested and unvested carry on departure, and any clawback or non-compete interaction.

- Co-invest rights, required capital commitment, and financing support, if any.

- The criteria, decision process, and economic change associated with promotion to Partner.

Candidates should model carry as uncertain, illiquid, and long-dated. A large-looking percentage can be less valuable than a smaller interest in a better-aligned fund, and the label is meaningless until the denominator and vesting terms are clear. For broader market context, use the Venture Capital Salary Guide rather than treating one posting as the market.

“Partner track” should come with observable milestones. Examples include originating investments the partnership approves, leading portfolio work effectively, demonstrating sound markups and write-offs over time, building a differentiated sector franchise, developing junior talent, supporting fundraising, and earning the partnership's trust. A promised timeline without criteria, available partnership economics, or evidence of prior promotions is not a progression plan.

Copy-ready venture capital principal job description template

Replace every bracketed field. Delete responsibilities the role will not own. The finished posting should make the fund's mandate, decision rights, success measures, and economics understandable to a qualified candidate.

About [Fund name]

[Fund name] is a [stage] venture capital firm investing in [sectors] across [geography]. We typically invest [initial check range] in [company profile] and reserve capital for [follow-on strategy]. Our current portfolio includes [representative companies or themes], and our team works from [location / working model].

We believe our advantage comes from [specific sourcing, domain, operating, geographic, or network edge]. Avoid claims such as “leading fund” unless the posting can substantiate them.

The mandate

We are hiring a Principal to own [sector / geography / stage] investment activity from origination through portfolio support. You will report to [role], lead [team or resources], and work with the partnership to turn [fund thesis] into a focused pipeline and high-conviction investments.

This role has [describe IC participation or vote], [describe authority to negotiate or approve terms], and [describe board observer/director expectations]. It is [partner-track / a senior investing role with a distinct path], with performance assessed against the outcomes below.

Responsibilities

- Build and maintain a differentiated pipeline in [focus area], with clear ownership of sourcing relationships and attribution.

- Develop investment theses and market maps that identify where the fund should—and should not—spend time.

- Lead founder meetings and quickly assess fit with the fund's stage, ownership, check-size, and return requirements.

- Design and manage commercial, product, technical, financial, legal, and reference diligence with internal and external specialists.

- Produce clear investment recommendations, present them to the investment committee, and respond directly to the strongest counterarguments.

- Lead term-sheet development and negotiation within [approved authority], coordinating counsel, co-investors, and the deal team through close.

- Support [number or range] portfolio companies through [board work, hiring, financing, customer introductions, strategy, M&A, or other actual support].

- Recommend reserves, follow-on participation, and portfolio actions using current company evidence and the fund's construction model.

- Coach [Analysts / Associates] and improve the quality of sourcing, diligence, memo, and portfolio-review processes.

- Contribute to [sector content, events, recruiting, portfolio reviews, LP materials, fundraising, or other firm-building work].

Required qualifications

- Evidence of sound investment or strategic judgment in [relevant stage / sector], including the ability to explain decisions, uncertainty, and lessons without overstating personal credit.

- Experience leading complex workstreams and influencing senior decision-makers under time pressure.

- A repeatable sourcing approach and trusted relationships relevant to [fund focus].

- Ability to assess markets, products, teams, business models, financing needs, ownership, and venture-return potential.

- Clear written and verbal communication with founders, investment committees, colleagues, co-investors, and advisers.

- Leadership that raises the quality of junior-team work and maintains high standards without unnecessary process.

- [Work authorization, location, travel, regulatory, or language requirement that is genuinely necessary].

Preferred qualifications

- Prior venture investing experience at [stage / strategy].

- Operating, founding, technical, scientific, clinical, or commercial depth in [focus area].

- Experience negotiating venture financings and working with outside counsel.

- Board-observer or director experience.

- Experience supporting follow-on financings, strategic transactions, or exits.

- [Degree or credential] only if it reflects a real requirement rather than a pedigree filter.

How success will be measured

In the first 12 months, success means:

- Establishing a qualified pipeline in [focus] and advancing [appropriate target] opportunities to substantive Partner or IC review.

- Leading [target or description] diligence processes and producing recommendations that are concise, decision-ready, and intellectually honest.

- Taking ownership of [portfolio scope] with strong founder feedback and reliable internal reporting.

- Improving [specific team process] and developing [junior-team expectation].

- Defining a differentiated thesis or network position the firm can continue to compound.

Do not set investment count or markup targets that reward weak decisions or short-term valuation movement. Use a balanced scorecard that recognizes disciplined passes, process quality, and portfolio outcomes alongside completed deals.

Compensation and benefits

The base-salary range is [range] for [location basis]. The role is eligible for [target bonus and basis], [carry description with denominator and fund], [vesting summary], and [co-invest terms if applicable]. Benefits include [health, retirement, leave, learning, travel, or other benefits].

If the role is partner-track, describe the review cadence, criteria, decision-makers, and expected economic change. If it is not, say what advancement can look like.

Hiring process

- Introductory conversation focused on mandate, motivations, and relevant track record.

- Investment discussion using one pursued, one declined, and one changed-view example.

- Structured case or sanitized memo review that tests judgment, prioritization, writing, and communication.

- Meetings with the investment team and relevant operating or portfolio colleagues.

- References that include a founder, a senior decision-maker, and someone the candidate managed or developed where possible.

- Final conversation covering role authority, scorecard, compensation, carry, and progression in writing.

Equal opportunity statement

[Insert the firm's approved equal opportunity and accommodation language.]

Before publishing, have the partnership confirm the authority language and have employment counsel review location-specific compensation, privacy, equal-opportunity, and hiring-process requirements.

When the mandate is ready, post the Principal role on Venture Capital Careers to reach candidates focused on venture investing.

Venture capital principal hiring scorecard

Score candidates against the mandate before interviews begin. The weights below are a starting point for an institutional investment role; a thesis-heavy seed fund, sector-specialist fund, or portfolio-intensive platform should change them.

| Competency | Starting weight | Evidence to request | Interview exercise | Warning sign |

|---|---|---|---|---|

| Investment judgment and thesis | 25% | Pursued, declined, and changed-view decisions; memo or thesis work | Defend a recommendation, then update it when given disconfirming evidence | Confuses confidence with certainty; cannot name a disciplined pass |

| Sourcing and relationships | 20% | Originated opportunities, network map, relationship-building method | Build a 90-day sourcing plan for the fund's mandate | Relies on meeting volume, databases, or a former firm's brand |

| Diligence and deal execution | 20% | Led workstreams, negotiated terms, counsel and syndicate coordination | Scope diligence under a fixed time and budget | Produces exhaustive checklists without prioritizing decision drivers |

| Portfolio and founder work | 20% | Founder references, board examples, follow-on or difficult-company decisions | Respond to a portfolio company missing plan with six months of runway | Defaults to operating the company or avoids difficult governance issues |

| Leadership and firm building | 15% | People developed, process improvements, sector franchise, LP or recruiting contribution | Give feedback on a flawed Associate memo and set a revision plan | Takes individual credit, delegates vaguely, or treats junior work as disposable |

Use the same core questions and anchored scoring scale for every candidate. Interviewers should record evidence before discussing impressions. A polished networker who cannot show judgment should not outrank a quieter candidate with a repeatable sourcing edge and strong decisions.

The case should resemble the work. A short deck, customer evidence, cap table, and ambiguous market question can test what the candidate prioritizes, which diligence they commission, how they frame ownership and return, and how they communicate a recommendation. It is more revealing than asking for a perfect model disconnected from the fund's investment process.

Questions candidates should ask before accepting

A Principal interview runs both ways. These questions expose whether the title, authority, resources, economics, and promotion story fit together:

- Does the Principal have an IC vote, a recommendation role, or presentation responsibility only?

- What investment, term, reserve, expense, or signature decisions can the Principal make without further approval?

- How does the firm define a sourced deal, and how is attribution handled when relationships are shared?

- Which board or observer responsibilities come with the role, and what is the expected portfolio load?

- What Analyst, Associate, platform, expert, and operating resources support the Principal?

- Which outcomes determine bonus and annual performance ratings? Are disciplined passes and portfolio work recognized?

- What exactly does the carry figure measure, which vehicles does it cover, and how do vesting and departure treatment work?

- What capital commitment or co-invest opportunity is expected, and how is it financed?

- What must be true for promotion to Partner, who makes the decision, and how have previous Principals progressed?

- How do the current fund's deployment pace, reserves, fundraising outlook, and partnership capacity affect the role?

Compare the answers with the written job description and offer. If the firm sells the position as partner-track but cannot define decision rights, economics, or prior promotion outcomes, treat the title as unverified. Candidates can use the Venture Capital companies directory to research firm focus before applying.

Frequently asked questions

Is Principal higher than VP in venture capital?

Sometimes, but there is no universal hierarchy. Some firms use VP and Principal interchangeably; others place VP below Principal or skip one title. Compare investment-committee role, deal authority, board responsibility, carry, and reporting line.

Is a VC Principal a Partner?

Usually not. A Principal is commonly the most senior non-Partner investor and may be on a path to the partnership. Some firms use Junior Partner for a similar mandate, but the economics and legal authority may still differ from a General Partner.

Can a Principal make investment decisions?

A Principal typically shapes the decision and leads the recommendation. Formal approval varies. The person may have a vote, delegated check authority, or no final approval at all. The job description should state the model.

Is an MBA required to become a VC Principal?

No industry rule requires one. An MBA can provide a network and structured finance exposure, but firms should prioritize demonstrated judgment, sourcing, deal leadership, domain knowledge, founder trust, and team leadership.

How long does it take to become Partner?

There is no reliable standard timeline. Promotion depends on investment evidence, portfolio outcomes, fundraising and firm-building contribution, partnership capacity, fund performance, and whether the firm is growing. Candidates should ask for milestones and examples rather than accepting a timeline alone.

The title matters less than the mandate. A well-scoped Principal owns judgment, relationships, and investment outcomes while operating inside clearly stated partnership boundaries. Candidates should verify those boundaries before joining; firms should put them in the posting before interviewing.