Hedge Fund vs Venture Capital: Careers, Work, and How to Choose

Hedge funds and venture capital both allocate risk capital, but the work feels radically different. Compare the daily job, skills, recruiting paths, feedback loops, and career fit.

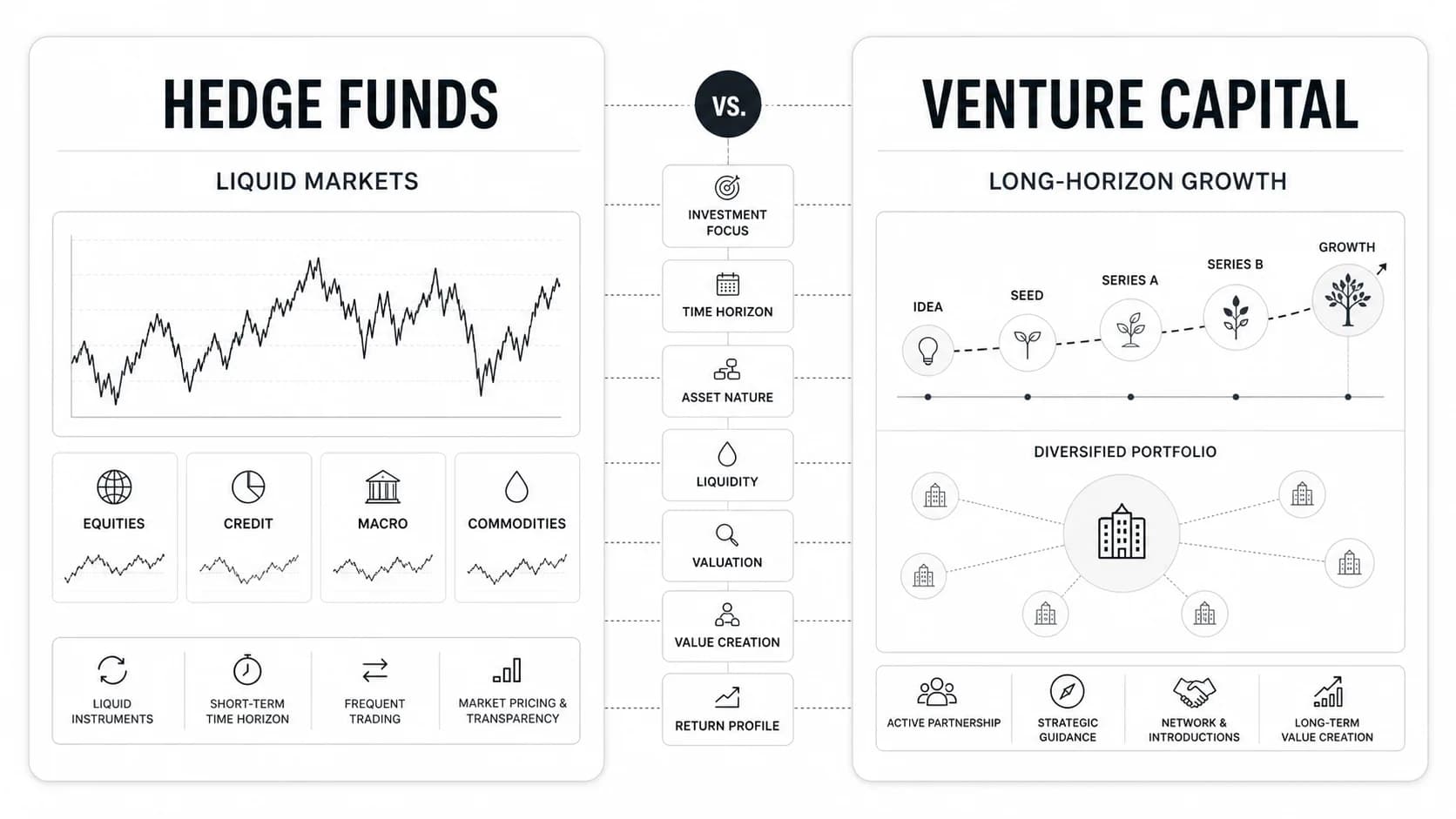

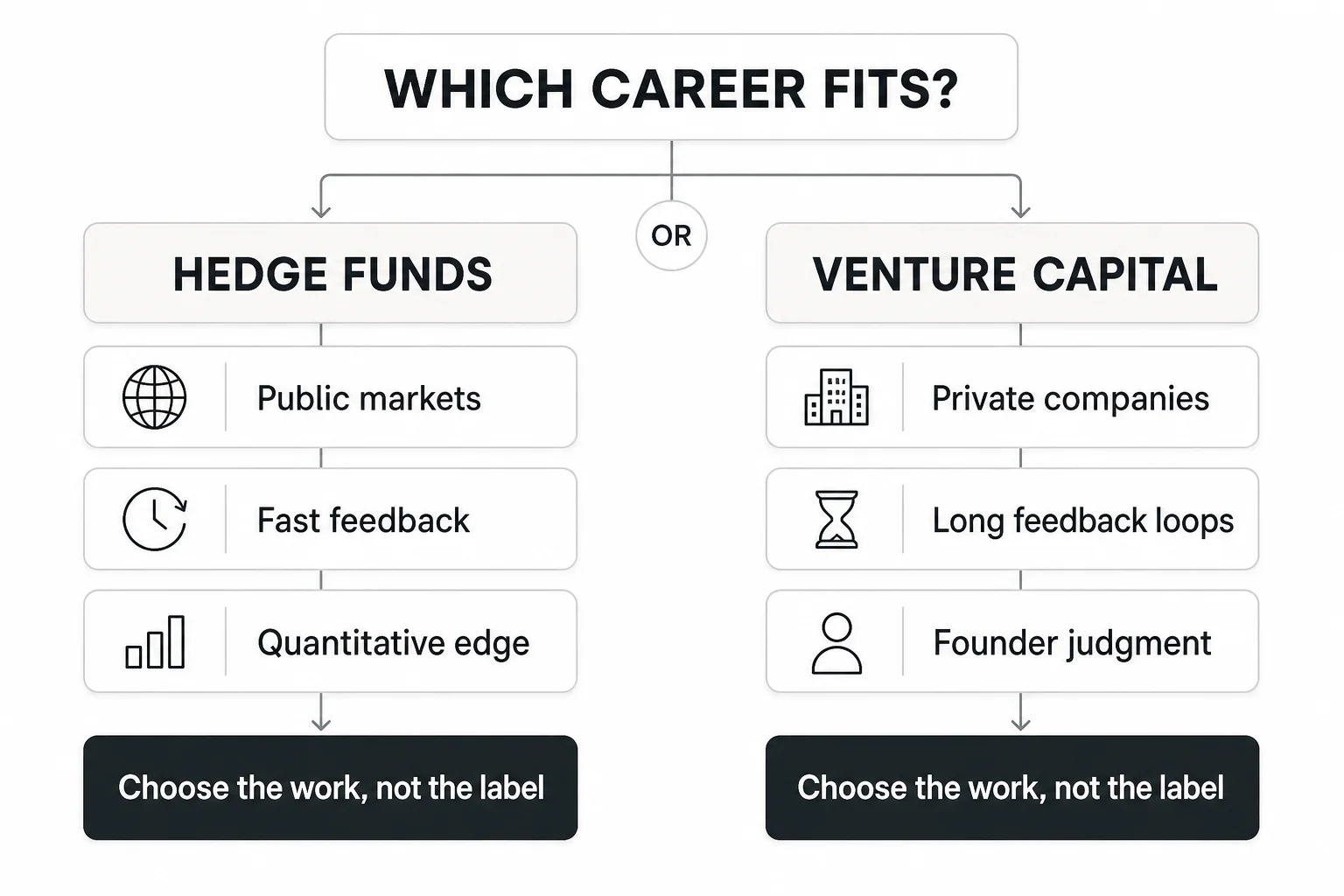

Hedge funds and venture capital firms both invest other people's money, but the jobs reward different instincts. A hedge fund career usually fits someone who enjoys liquid markets, repeated research cycles, measurable performance, and fast feedback. A venture capital career usually fits someone who enjoys private companies, ambiguous data, sourcing, founder judgment, and decisions that may take years to prove right or wrong.

The most useful question is not which industry sounds more prestigious. It is which feedback loop you want to live inside every week.

Hedge fund vs venture capital at a glance

| Dimension | Hedge funds | Venture capital |

|---|---|---|

| Primary assets | Public securities and other tradable instruments | Equity in private, usually high-growth companies |

| Typical decision | Buy, sell, short, size, or hedge a position | Source, evaluate, invest, reserve, or support a company |

| Information set | Market prices, filings, models, data, news, management access | Founder meetings, product evidence, market research, references, limited operating history |

| Feedback loop | Often days, weeks, or quarters | Often years |

| Core craft | Forming and updating a differentiated view faster or better than the market | Finding exceptional companies and judging teams, markets, and upside under uncertainty |

| Portfolio relationship | Usually a security position, though strategies vary | Often an ongoing relationship with founders and boards |

| Candidate evidence | Investment pitches, models, research notes, data work, risk thinking | Sourcing proof, market maps, investment memos, founder references, product judgment |

| Best fit | You like public markets, iteration, numbers, and explicit performance signals | You like startups, people, networks, narrative judgment, and long-duration uncertainty |

These are tendencies, not universal rules. A quantitative hedge fund, an activist fund, and a credit fund can feel like different industries. A pre-seed generalist VC and a late-stage sector specialist can too. Compare actual roles, not labels.

What hedge funds and venture capital firms actually do

The Investor.gov hedge-fund overview describes hedge funds as pooled private investment vehicles that can use strategies including leverage, short selling, derivatives, and investments that may be difficult to value. The practical implication for a candidate is breadth: “hedge fund” tells you less about the daily job than the fund's strategy, asset class, holding period, and team model.

A long/short equity analyst might build earnings scenarios, speak with industry sources, monitor catalysts, and continuously update position risk. A global macro analyst may study rates, currencies, commodities, and policy. A quant researcher may spend far more time on data, code, and statistical testing than on company meetings.

Venture capital firms finance private companies with high growth potential, typically through equity investments. An Investor.gov discussion of venture capital funds notes their exposure to private, often illiquid investments and their potential to assist portfolio companies. For candidates, that translates into work across sourcing, founder meetings, market research, diligence, investment memos, portfolio support, and fund operations.

Stage matters. A seed investor may make decisions with little revenue data and spend heavily on sourcing. A growth investor may build detailed cohort, unit-economics, and scenario analyses. A platform professional may focus on talent, go-to-market support, or community rather than investment selection. The Venture Capital Careers career-path guide maps those roles in more detail.

How the daily work differs

Hedge funds compress the learning cycle

Public markets keep producing signals. Prices move, earnings arrive, theses break, and position sizes force choices. That creates a demanding but legible learning environment: you can compare what you expected with what happened, diagnose the error, and update your process.

The downside is that the signal can become noise. A correct long-term thesis can lose money in the short term. A good result can come from a poor process. Many roles also require comfort with persistent scrutiny because performance is visible and capital can move quickly.

Venture capital stretches the learning cycle

VC decisions unfold slowly. A company can look weak before product-market fit and impressive before a collapse. The best early evidence is often qualitative: founder learning speed, customer urgency, product pull, or an unusual distribution advantage. You still need analytical discipline, but false precision is dangerous when the inputs are sparse.

The job is also more socially exposed. Sourcing depends on relationships. Diligence requires extracting signal from founders, customers, operators, and references. Winning an allocation can require persuading a founder that your firm should be on the cap table. Supporting a portfolio company means maintaining trust after the investment decision.

The skills each path rewards

Both careers require judgment, curiosity, and the ability to communicate an investment view. The weighting differs.

Hedge fund teams often value:

- A clear variant view: what you believe that the market is missing.

- Financial fluency: how operating changes reach earnings, cash flow, valuation, and risk.

- Updating discipline: what evidence would change your mind and how quickly.

- Position thinking: how conviction, downside, liquidity, correlation, and timing affect size.

- Strategy-specific capability: coding, statistics, credit work, channel research, macro analysis, or another edge.

VC investment teams often value:

- Sourcing: evidence that excellent founders will take your call or that you can find companies early.

- Market judgment: a structured view of timing, market size, competition, and potential power-law outcomes.

- Founder assessment: separating charisma from learning speed, resilience, recruiting ability, and insight.

- Product curiosity: understanding why users adopt, stay, pay, or switch.

- Memo clarity: making a decision under uncertainty while naming the risks honestly.

- Portfolio usefulness: knowing when to help, whom to introduce, and when to stay out of the way.

The Venture Capital Careers skills guide explains how VC firms assess these capabilities. The useful distinction is proof: hedge-fund candidates frequently prove a research and risk process; VC candidates must also prove access, judgment, and usefulness to founders.

Recruiting and interviews

There is no single hedge-fund recruiting funnel. Some large funds hire structured analyst classes; many smaller funds recruit opportunistically. Common entry points include equity research, investment banking, sales and trading, asset management, data science, and sector operating roles. Interviews often center on investment pitches, accounting, valuation, market mechanics, and how a thesis changes when new evidence arrives.

VC recruiting is similarly fragmented, but the opening is often narrower. Firms may hire from banking or consulting, yet they also value founders, operators, researchers, community builders, and sector experts. A candidate who has already built a relevant network or discovered compelling companies can beat someone with a more conventional résumé.

Expect VC processes to test several layers:

- Why this firm, stage, geography, and sector.

- Which companies or markets you find unusually promising.

- How you source and qualify opportunities.

- Whether you can write an investment memo with explicit risks.

- How you behave with founders and colleagues.

- Whether your judgment improves when challenged.

Use the VC case study interview guide to prepare the investment exercise, then make your venture capital résumé prove the same skills rather than listing generic interest.

Compensation, advancement, and career risk

Avoid choosing between the industries from a headline salary range. Compensation varies too much by strategy, fund size, geography, seniority, individual performance, and whether long-term economics are real or merely discussed.

Hedge-fund compensation is often more tightly linked to annual or multi-year investment performance. That creates upside when a strategy and team perform, but it can also create sharp employment risk when returns, assets, or confidence deteriorate. Advancement depends on producing repeatable insight, earning risk, and eventually influencing or owning capital allocation.

VC compensation may combine salary, bonus, and, at senior levels, carried interest. Carry is not the same as cash compensation: vesting, fund performance, timing, dilution across the team, and departure terms matter. Advancement depends on sourcing access, investment judgment, portfolio contribution, fundraising credibility, and internal trust. Because outcomes take years, attribution can be less immediate and more political.

Ask every prospective employer concrete questions:

- What decisions would I own in the first year?

- How is performance evaluated, and over what period?

- What caused the last person in this role to succeed or struggle?

- How much time goes to research, sourcing, execution, portfolio work, or internal process?

- What is the path to greater decision authority?

- How are bonus, profit share, or carry calculated, vested, and affected by departure?

How to choose: a candidate scorecard

Score each statement from 1 (strongly disagree) to 5 (strongly agree).

| Statement | Points toward |

|---|---|

| I want prices and new data to challenge my view continuously | Hedge funds |

| I enjoy turning filings, datasets, and catalysts into a tradeable thesis | Hedge funds |

| I prefer a more measurable link between decisions and results | Hedge funds |

| I am comfortable abandoning a view quickly when evidence changes | Hedge funds |

| I enjoy meeting founders before the data is complete | Venture capital |

| I can stay curious through years of ambiguous progress | Venture capital |

| I like building networks and creating access, not only analyzing what arrives | Venture capital |

| I want company-building relationships to remain part of the job | Venture capital |

Do not treat the total as a personality test. Use it to identify which assumptions you need to test. A candidate attracted to VC but unwilling to source has a work mismatch. A candidate attracted to hedge funds but distressed by frequent performance feedback has one too.

Run a 30-day test before committing

Career decisions improve when you produce work from both systems.

Week 1: choose one company and one market

Pick a public company you can analyze and a private startup market you genuinely care about. Narrow both enough to develop a view.

Week 2: create a hedge-fund-style pitch

Write two pages covering the thesis, consensus view, variant view, catalysts, valuation, downside, and disconfirming evidence. Update it after one meaningful new data point. Notice whether the revision process energizes you.

Week 3: create a VC-style market map and memo

Map 15–25 companies in the private market, speak with at least three relevant people if possible, and write a two-page memo on one company. Cover the founder-market insight, customer urgency, market timing, competition, upside case, and reasons not to invest.

Week 4: compare your behavior

Which project pulled you back without external pressure? Where did you have better questions? Which uncertainty felt productive rather than draining? Share each piece with someone in the relevant field and ask what evidence was missing.

That comparison is more informative than another month of reading career descriptions.

Frequently asked questions

Is venture capital a type of hedge fund?

No. Both can be private pooled investment vehicles, but VC funds primarily invest in private companies over long horizons, while hedge-fund strategies commonly trade public securities and other instruments with different liquidity, risk, and return structures.

Is it harder to get into a hedge fund or venture capital?

Both are selective, but the bottleneck differs. Hedge funds often demand strategy-specific analytical proof. VC firms often demand a mix of judgment, sourcing access, sector credibility, and founder-facing ability. Your background may make one path materially more accessible.

Can you move from a hedge fund to venture capital?

Yes, especially when your hedge-fund work builds sector expertise relevant to a VC strategy. The missing proof is usually private-company sourcing, early-stage judgment, and founder usefulness. Build that evidence before presenting the move as a simple transfer of investing skill.

Which career has better work-life balance?

Neither label guarantees it. Team culture, fund strategy, seniority, portfolio intensity, fundraising, reporting cycles, and performance pressure matter more. Ask how people actually spend time and what happens during difficult periods.

Choose the work, then find the firm

Hedge funds and venture capital are not two versions of the same investing job. One usually compresses feedback around markets and positions; the other stretches feedback across people, products, and private-company outcomes. Choose the learning environment that fits you, build a small body of work that proves it, and then inspect firms individually.

When VC is the better fit, explore the Venture Capital Careers companies directory to build a target list, then use the VC job board to see how real roles describe the work.