Private Credit vs Venture Capital: Careers, Work, and How to Choose

Private credit and venture capital both fund private companies, but the work rewards different instincts. Compare the models, daily job, recruiting evidence, and career fit.

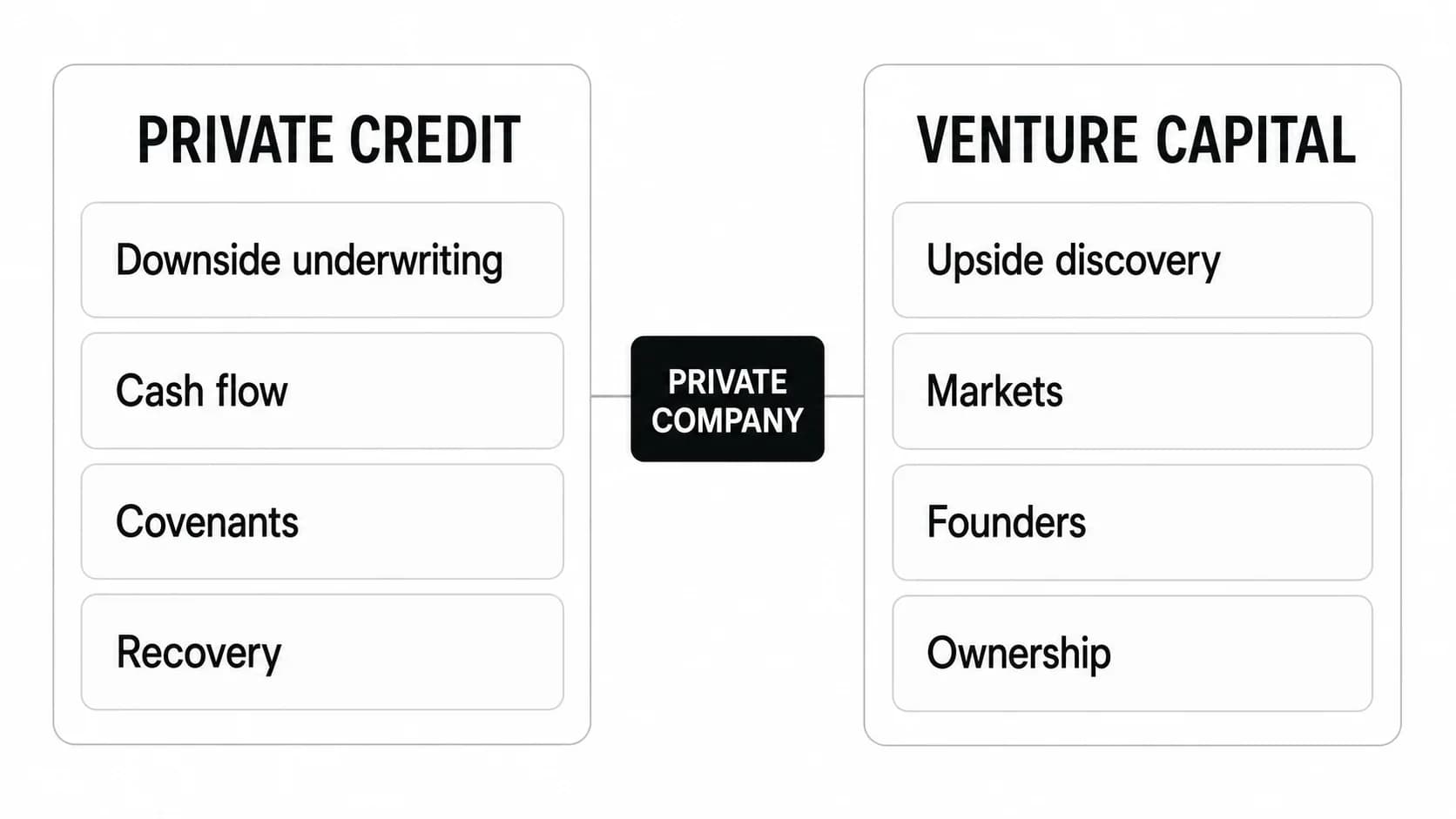

Private credit and venture capital both put money into private companies, but they reward different investing instincts. Private credit is primarily a downside-underwriting job: can the borrower pay interest and repay principal under a range of scenarios? Venture capital is primarily an upside-discovery job: can this company become valuable enough that a minority equity stake returns a meaningful share of the fund?

Choose private credit if you enjoy cash-flow models, capital structures, legal documents, covenants, and recurring portfolio monitoring. Choose venture capital if you enjoy markets, founders, sourcing, product judgment, reference calls, and decisions made with sparse data. Neither is universally better. The better career is the one whose repeated work matches how you like to think.

Private credit vs venture capital at a glance

| Dimension | Private credit | Venture capital |

|---|---|---|

| Security | Debt: a contractual claim | Equity: an ownership stake |

| Core question | How do we get repaid, and what protects us if the case weakens? | How large could the company become, and why might it win? |

| Return pattern | Interest, fees, principal repayment, sometimes equity participation | Gains at acquisition, secondary sale, or IPO |

| Downside protection | Seniority, collateral, covenants, pricing, documentation | Limited contractual protection; portfolio diversification and ownership terms matter |

| Typical evidence | Historical financials, leverage, cash flow, collateral, debt capacity | Market size, product, team, growth, retention, competition, ownership |

| Feedback cadence | Monthly or quarterly operating and covenant signals | Milestones arrive unevenly; decisive outcomes can take years |

| Common analyst output | Credit model, downside cases, credit memo, covenant monitoring | Market map, investment memo, cap-table analysis, reference notes |

| Relationship model | Lender–borrower | Investor–founder and board/portfolio partner |

| Career fit | Precision, skepticism, documentation, risk control | Curiosity, synthesis, networks, comfort with ambiguity |

What private credit and venture capital actually finance

The Federal Reserve defines private credit as loans originated by nonbanks and negotiated bilaterally between borrowers and lenders. Direct lending to middle-market companies is the most familiar form, but the label can also include asset-based finance, mezzanine debt, special situations, distressed credit, and venture debt. Those strategies do not produce identical jobs. An analyst underwriting recurring-revenue software loans will do different work from one evaluating aircraft collateral or a distressed restructuring.

Venture capital funds make long-duration equity investments in young, high-growth companies. The National Venture Capital Association's description of VC emphasizes the partnership model: funds make initial investments, reserve capital for follow-ons, and work with companies over several years. A seed investor may spend heavily on sourcing and founder assessment; a later-stage investor may do more cohort, market, and ownership modeling.

Venture debt sits in the overlap. It is debt extended to VC-backed companies, often after an equity round, and is commonly a complement to equity rather than a simple replacement. Carta's private-credit overview is useful on this boundary. A venture-debt role can blend credit underwriting with startup and sponsor analysis, but it remains a lending job: repayment, runway, covenants, collateral, and downside still matter.

The real career difference: downside underwriting vs upside discovery

The cleanest way to compare the careers is to ask what must be true for each investment to work.

In private credit, a strong outcome usually means the borrower pays the agreed interest and returns principal. Extra upside may exist through fees, call protection, warrants, or equity kickers, but a lender does not need the company to become the category winner. The analyst therefore works backward from loss: what breaks the repayment case, how early would the lender know, and what rights or assets are available if performance deteriorates?

That leads to questions such as:

- How durable are revenue and margins through a downside case?

- How much leverage can the business support?

- What are fixed-charge coverage, liquidity, and cash-burn constraints?

- Where does the loan sit in the capital structure?

- Which covenants create an early warning or a negotiating point?

- What recovery could the lender expect if the company defaults?

In venture capital, the maximum loss on a single equity investment is usually easier to state: the invested capital can go to zero. The harder problem is estimating a wide and asymmetric upside. The analyst asks whether a market, product, distribution advantage, team, and ownership position can produce an outcome large enough to matter to the fund.

That leads to a different question set:

- Is the market capable of supporting a very large company?

- Why is this product materially better or newly possible?

- Is growth efficient and retention durable?

- Does the team have an unusual advantage in this problem?

- What would the fund own after this and future rounds?

- Could a plausible exit return the fund, not merely produce a respectable company?

This distinction affects temperament. Credit rewards people who notice what can go wrong before it becomes obvious. VC rewards people who can form conviction before the evidence is complete. Both require judgment; they place judgment on opposite sides of the distribution.

The feedback loop matters more than the prestige label

Private-credit analysts often receive frequent evidence. Financial reporting, borrowing-base certificates, covenant calculations, amendments, interest payments, and sponsor conversations reveal whether the thesis is holding. That does not make the work easy—the signals can be noisy or delayed—but the investment is repeatedly tested against contractual expectations.

VC feedback is less regular. A company can look strong for several quarters and then stall, or appear mediocre before finding product-market fit. Markups are not cash returns, and a good company can still be a poor fund investment if entry price or ownership is wrong. Candidates who need fast, objective feedback may find early-stage venture frustrating. Candidates who dislike document-heavy monitoring may find credit constraining.

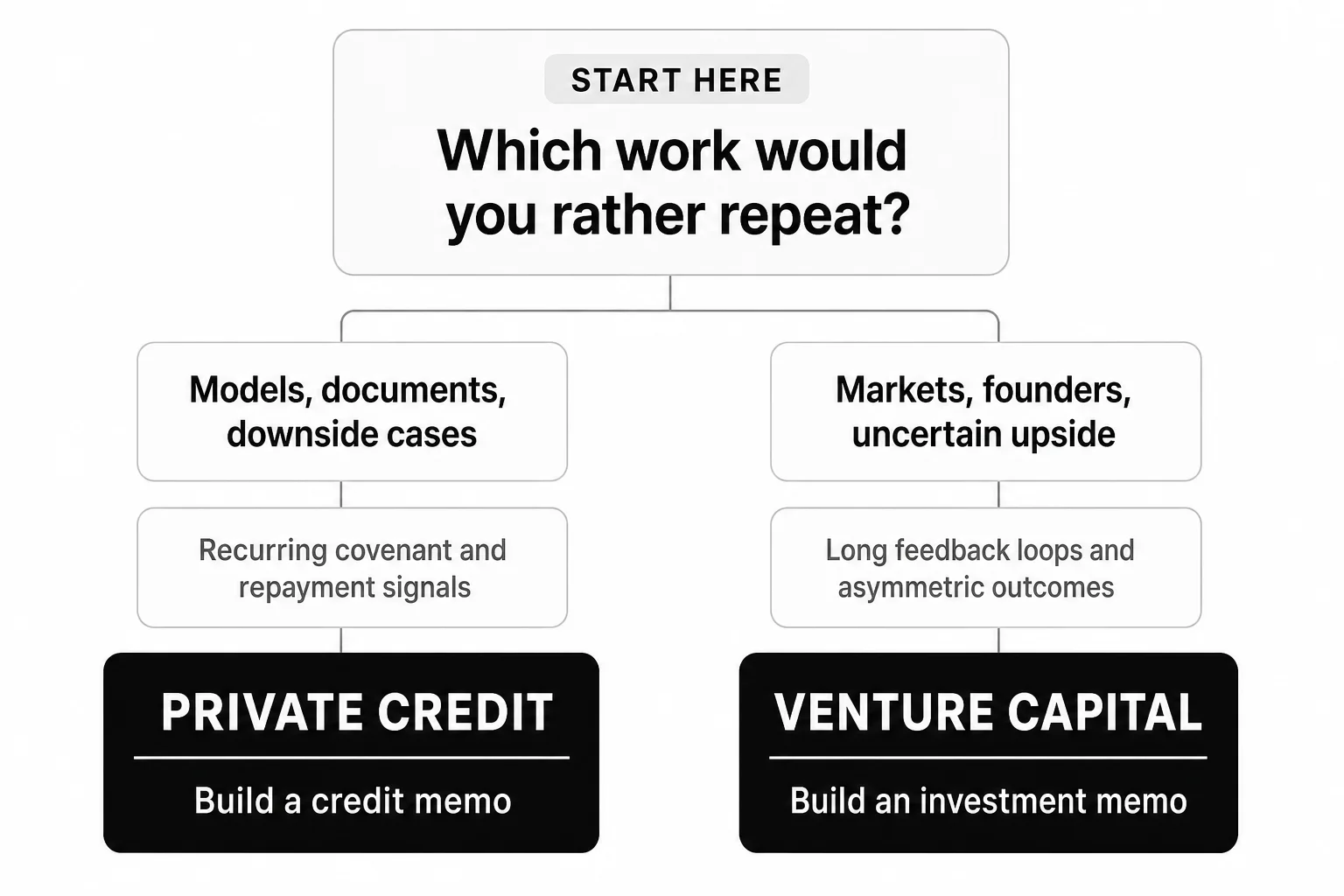

The practical decision rule is simple: would you rather be repeatedly right about repayment or occasionally very right about scale?

How the daily work differs

Fund strategy and seniority change the calendar, but junior investors usually spend their time on a recurring set of activities.

| Workstream | Private-credit analyst or associate | VC analyst or associate |

|---|---|---|

| New opportunities | Screen teasers, lender presentations, data rooms, sponsor materials | Source companies, map markets, take founder meetings, triage introductions |

| Modeling | Debt schedule, cash flow, leverage, coverage, liquidity, downside and recovery cases | Market and unit economics, cohorts where available, dilution, ownership, exit scenarios |

| Diligence | Quality of earnings, customer concentration, collateral, documents, management and sponsor calls | Product, market, team, customer references, competition, technical or sector diligence |

| Memo | Recommend structure, pricing, covenants, risks, and mitigants | Explain thesis, risks, ownership, return potential, and why the company can win |

| Closing | Negotiate terms with legal counsel and monitor conditions precedent | Support term sheet, ownership and governance analysis, references, and closing |

| Portfolio | Review reporting, covenants, liquidity, amendments, watch-list credits | Track milestones, help with hiring or introductions, prepare follow-ons and board materials |

Private-credit work is usually more model- and document-intensive. Small wording changes can alter lender rights; a model must reconcile sources and uses, cash flow, debt capacity, interest, and maturity. The role can also become highly situational when a company misses plan and requests an amendment.

VC work is usually more sourcing- and judgment-intensive, especially at seed and Series A. A junior investor may spend more time building a network, meeting companies, mapping a theme, and collecting evidence from customers or experts. Later-stage VC can be quantitatively demanding, but it still evaluates equity upside rather than contractual repayment.

One company, two investment memos

Consider a growing B2B software company with $30 million of recurring revenue, modest burn, strong retention, and a plan to expand internationally.

The private-credit memo might start with the base and downside cases. The analyst tests renewal rates, customer concentration, margin compression, hiring plans, minimum cash, debt service, and runway. The recommendation specifies loan size, interest, maturity, amortization, collateral, reporting, covenants, and conditions for additional borrowing. The crucial paragraph explains how the lender gets repaid if growth slows.

The VC memo starts somewhere else. The analyst tests whether the category is large, the product can become a system of record, retention supports compounding, distribution can scale, and the team can build an enduring company. The model examines ownership today, dilution in future rounds, and exit outcomes. The crucial paragraph explains why this company can become much larger than the current plan implies.

Both analysts review the same retention and cash data. They assign it different jobs. The lender uses it to bound loss and repayment capacity. The VC investor uses it to estimate durability and nonlinear upside. That is the work difference in miniature.

Skills and work samples firms hire for

Both paths require financial fluency, clear writing, commercial judgment, and the ability to defend a recommendation. The weighting differs.

Private-credit evidence

Private-credit teams typically value accounting, cash-flow modeling, debt mechanics, attention to documentation, and disciplined risk communication. Banking, leveraged finance, transaction advisory, rating-agency, restructuring, and credit-research backgrounds transfer naturally because candidates have seen how companies finance and service obligations.

A strong self-directed work sample is a five-page credit memo on a public company or well-documented private-company case. Include:

- Business and industry overview.

- Historical financial summary and cash conversion.

- Proposed debt structure and sources and uses.

- Base, downside, and severe-downside cases.

- Leverage, coverage, liquidity, covenants, and recovery analysis.

- Recommendation, risks, and mitigants.

The memo should make a decision. A beautifully formatted model that never states the risk limit is weaker than a simpler analysis with a clear “lend, resize, reprice, or decline” conclusion.

Venture-capital evidence

VC teams typically value market curiosity, startup judgment, sourcing ability, concise writing, networks, and comfort building a view from incomplete evidence. Banking and consulting can help, but founders, operators, product managers, researchers, and sector specialists can be credible because lived market knowledge matters.

Two work samples are especially useful:

- A venture capital investment memo that explains the problem, product, market, competition, team, risks, ownership, and return path.

- A market map of 25–50 companies with a non-obvious segmentation and a short thesis on where value will accrue.

The strongest work samples show judgment, not research volume. A list of facts is not a thesis. Name what you believe, what would disconfirm it, and which company you would meet first.

Recruiting and interviews

Private-credit recruiting is usually more structured. Firms can test technical skills through accounting questions, debt schedules, leverage and coverage analysis, a timed model, or a credit case. Candidates should expect to defend assumptions under a downside scenario and explain how documentation or structure changes the risk.

VC recruiting varies more by firm. Interviews may test market judgment, sourcing, company evaluation, founder empathy, and written communication. A VC case-study interview may ask for a memo, presentation, market map, or live investment-committee discussion. Small funds may recruit opportunistically rather than on an annual timetable.

For either path, tailor your venture capital resume or investment resume to evidence, not adjectives. “Strong analytical skills” is weak. “Built downside and liquidity cases for a $200 million refinancing” or “mapped 80 vertical-software companies and sourced three founder meetings” tells the interviewer what you can already do.

Which background has the easier path?

- Leveraged finance or sponsor banking: usually the cleanest private-credit entry; viable for later-stage VC with added product and market evidence.

- M&A or generalist investment banking: viable for both; credit needs debt fluency, VC needs sourcing and startup judgment.

- Consulting: viable for VC and some sector-focused credit teams; build accounting and modeling depth for credit.

- Startup operating role: strong for VC when the experience is relevant; private credit requires explicit underwriting and financial-statement evidence.

- Public credit or ratings: strong for private credit; VC transition requires evidence of comfort with young companies and asymmetric upside.

Review the broader venture capital career path and skills VC firms look for before treating any single background as a rule.

Compensation and career risk

Do not choose between private credit and VC from a single salary table. Cash compensation changes by geography, firm size, strategy, seniority, fundraising cycle, and individual performance. Long-term economics are even less comparable: bonus formulas, carried interest, vesting, co-investment, deal attribution, and the probability of realization differ by firm.

Private-credit compensation often reflects deployment, portfolio performance, and realized credit outcomes. A larger platform may offer a clearer promotion ladder and more stable staffing, but distressed periods can create intense workloads and reputational risk around problem credits. A strong lender can build a durable career without needing one investment to become a hundredfold winner.

VC compensation can be less standardized, particularly at small or emerging funds. Carry can be valuable, but only if it is meaningfully granted, vests, the fund performs, and exits return cash. The current venture market illustrates why those conditions matter: the NVCA 2026 Yearbook describes strong headline deployment alongside concentrated capital and a persistent liquidity problem. A prestigious platform does not eliminate fund-vintage, fundraising, or exit risk.

Use the Venture Capital Careers salary guide for role-level context, then diligence the actual offer.

Six questions that reveal the real role

“Private credit associate” and “VC associate” are not precise job descriptions. Ask:

- What strategy and stage drive most new deployment? Direct lending, asset-based finance, special situations, venture debt, seed, and growth VC create different work.

- How is time split across sourcing, underwriting, execution, and portfolio work? Ask for a percentage estimate and a recent-week example.

- What does the junior investor own? Model, memo, documents, founder calls, customer references, investment committee, board materials, or portfolio monitoring?

- How is performance measured in the first 12 months? Output volume, decision quality, sourcing, portfolio outcomes, relationship development, or something else?

- What happened to the last two people in the role? Promotion and exits reveal more than the stated career path.

- How do bonus, carry, co-investment, vesting, and clawbacks work? Request mechanics, not a headline percentage.

A candidate who skips these questions may compare industry stereotypes while choosing a very specific job.

How to choose: a candidate scorecard

Score each statement from 1 (not me) to 5 (strongly me). Do not score the perceived prestige of the industry.

| Preference | Points toward private credit | Points toward VC |

|---|---|---|

| I like reconciling financial statements and tracing cash | +2 | 0 |

| I enjoy legal terms, structure, and negotiating protections | +2 | 0 |

| I instinctively ask how an investment can lose money | +2 | +1 |

| I want recurring, measurable portfolio signals | +2 | 0 |

| I enjoy meeting new companies before data is complete | 0 | +2 |

| I build strong views on markets, products, and teams | 0 | +2 |

| I like sourcing and relationship-building as core work | +1 | +2 |

| I can wait years for a thesis to resolve | +1 | +2 |

| I prefer bounded returns with contractual protection | +2 | 0 |

| I prefer asymmetric outcomes and can tolerate many misses | 0 | +2 |

The result is a prompt, not a verdict. A sourcing-heavy direct-lending role may suit a relationship builder; a late-stage VC role may involve substantial modeling. Use your score to generate better questions for specific firms.

Run a two-week work-sample test

You can test both paths before committing to recruiting.

Week one: think like a lender

Choose a public software, healthcare, services, or industrial company with accessible filings.

- Build a three-statement-light cash-flow and debt schedule.

- Create base, downside, and severe-downside cases.

- Calculate leverage, interest coverage, fixed-charge coverage, and minimum liquidity.

- Propose a debt size, maturity, pricing range, collateral package, and two covenants.

- Write a two-page credit recommendation.

Notice where you gain energy. Was it tracing cash, finding the breaking point, and tightening the structure—or did the bounded outcome feel unsatisfying?

Week two: think like a VC investor

Choose a private startup sector you understand.

- Map at least 25 companies into a useful segmentation.

- Interview two customers, operators, or domain experts if possible.

- Select one company and write a two-page investment memo.

- Estimate market size, ownership after investment, dilution, and three exit outcomes.

- State one non-consensus belief and what evidence would disprove it.

Notice a different signal. Did ambiguity make you curious—or did the lack of hard evidence feel like hand-waving?

At the end, compare the quality of your decisions, not which document looked more impressive. You will also have two artifacts that make future networking conversations more substantive.

Can you move between private credit and venture capital?

Yes, but the move is easiest when the destination strategy values what you already know.

A private-credit investor can be credible for growth-stage VC, fintech, capital-intensive sectors, turnaround-oriented investing, or venture debt. The transferable strengths are accounting, downside analysis, deal execution, management diligence, and investment-committee writing. The gaps are usually sourcing, product judgment, startup networks, and comfort underwriting outcomes that cannot repay from current cash flow.

A VC investor can be credible for venture debt, technology direct lending, or growth-credit teams. The transferable strengths are sector knowledge, company access, management assessment, market work, and portfolio relationships. The gaps are usually debt mechanics, legal documentation, covenant design, recovery analysis, and the discipline to reject an exciting company that cannot support the proposed obligation.

To switch, build the missing work sample before applying. A credit investor should produce a VC memo and market map. A VC investor should build a debt model, downside case, and credit memo. Then target firms where the bridge is part of the strategy, not merely a story in your cover letter.

Frequently asked questions

Is private credit the same as venture debt?

No. Venture debt is one private-credit strategy focused on VC-backed companies. Private credit is broader and includes direct lending, asset-based finance, mezzanine, special situations, and distressed strategies.

Which career uses more financial modeling?

Private credit usually requires more recurring cash-flow, leverage, debt-schedule, coverage, liquidity, and downside modeling. Later-stage VC can be model-heavy, but early-stage VC often relies more on market, ownership, scenario, and unit-economics analysis because historical data are limited.

Is private credit less risky than venture capital?

At the security level, senior debt generally has contractual payments and priority over equity, which can provide more downside protection. That does not make every private-credit investment or job safe. Leverage, weak documentation, poor underwriting, concentration, illiquidity, and defaults can produce losses. VC accepts a higher probability of loss on individual companies in pursuit of large winners.

Is private credit or VC better for work-life balance?

The label is not enough to answer. Deal volume, live transactions, portfolio problems, sourcing expectations, fund size, and team staffing matter more. Credit can become intense during documentation and restructurings; VC can involve constant networking, travel, founder meetings, and urgent portfolio work. Ask how the team spent the last month.

Where should I look for firms and roles?

Use the Venture Capital Careers companies directory to research investment platforms, then browse open VC and private-markets roles. Compare job descriptions against the role-diligence questions above instead of filtering by title alone.

Pick the work you want to repeat

Private credit and venture capital sit in the same private-markets ecosystem, but they train different reflexes. Credit teaches you to protect principal, structure claims, and act before downside becomes irreversible. VC teaches you to recognize exceptional companies early, build conviction with incomplete information, and live with a long path to proof.

Choose the loop that fits you, produce evidence that you can do the work, and evaluate the specific team behind the label.