Growth Equity vs Venture Capital: Key Differences for Founders and Candidates

Growth equity backs proven companies ready to scale; venture capital backs earlier startups still proving the market. Compare stage, risk, control, exits, and career fit.

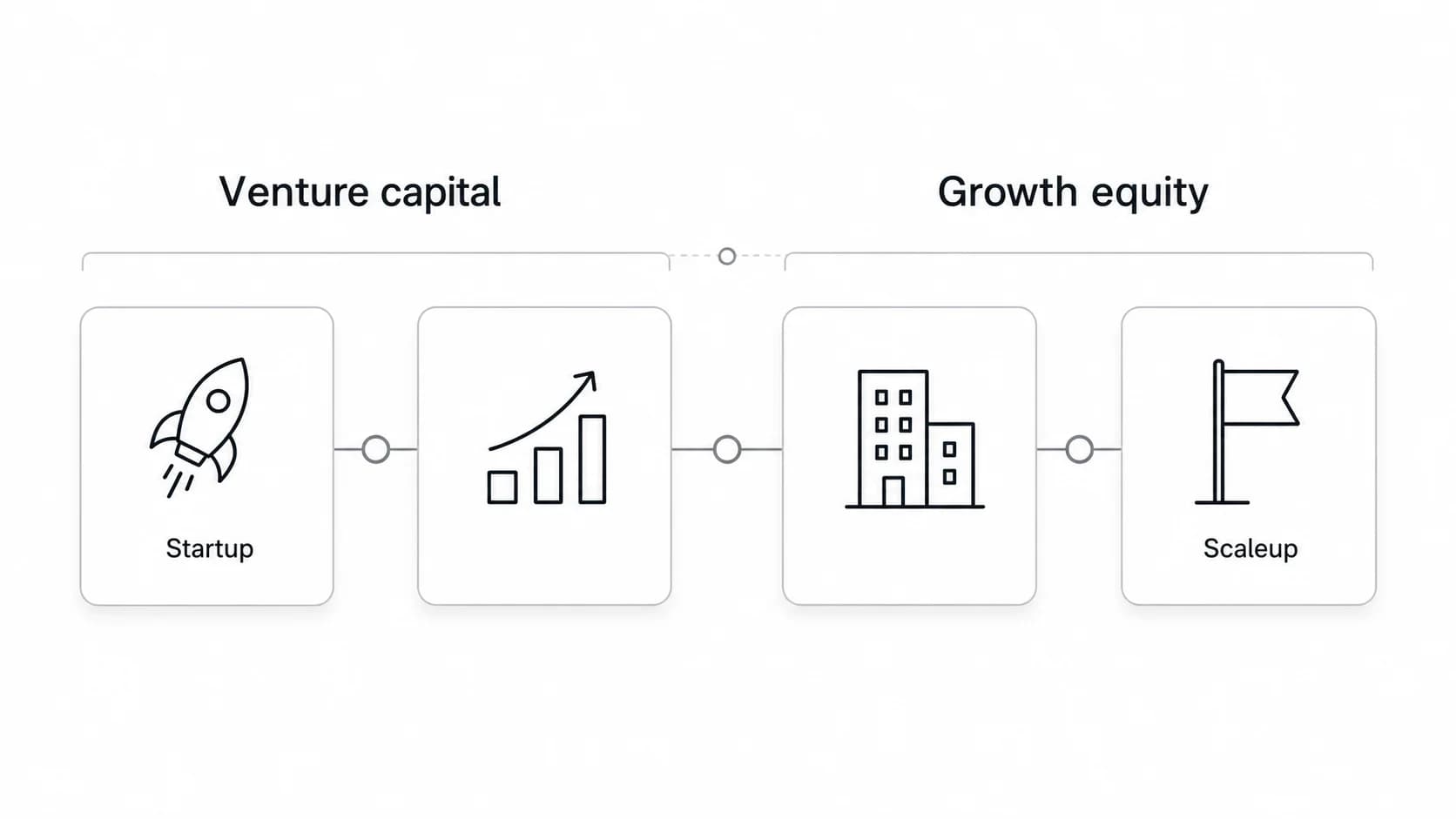

Growth equity and venture capital both fund private companies, but they are built for different risk profiles. Venture capital usually backs startups that are still proving the market, product, and business model. Growth equity usually backs companies that already have meaningful revenue, repeatable sales motion, and a clearer path to scale.

The cleanest way to separate them is this: venture capital funds the search for a breakout company; growth equity funds the scaling of a company that already looks like one.

That distinction matters if you are raising capital, evaluating an investment, or deciding which side of the private-markets career path fits you. A seed-stage SaaS company with a promising product but limited revenue needs a different investor than a profitable vertical software company using outside capital to expand sales, enter a new geography, or acquire a smaller competitor.

Growth equity vs venture capital at a glance

| Dimension | Venture capital | Growth equity |

|---|---|---|

| Typical company stage | Startup, early-stage, or emerging company | Proven growth company, often later-stage or scaleup |

| Core bet | The market, product, and team can become much larger than they are today | A working business can scale faster with outside capital |

| Revenue profile | Often pre-revenue or early revenue at seed/Series A; more revenue at later rounds | Meaningful revenue, often with stronger visibility into retention, margins, and unit economics |

| Profitability | Usually not required | Often profitable, cash-flow positive, or close to it |

| Risk | Higher company-failure and market-risk profile | Lower venture-style failure risk, but still exposed to execution, valuation, and exit risk |

| Ownership | Minority stakes are common, especially across a portfolio of startups | Minority stakes are also common, often with more negotiated rights |

| Investor involvement | Sourcing, founder support, hiring help, fundraising help, product-market-fit judgment | Financial diligence, go-to-market scaling, operational support, M&A, board-level planning |

| Return path | A few outliers can drive fund returns | Returns depend more on growth, entry valuation, execution, and exit discipline |

| Career work | Ambiguous market judgment, founder assessment, early deal sourcing | Financial analysis, market mapping, operating metrics, later-stage diligence |

Growth capital is commonly described as capital for relatively mature companies seeking expansion, restructuring, market entry, or acquisitions without a change of control (Growth capital). Venture capital is commonly described as private equity financing for startup, early-stage, and emerging companies with high growth potential (Venture capital).

Those definitions overlap in the middle. A strong Series C company can look like a venture deal to one fund and a growth equity deal to another. The more useful question is not "what label does the round use?" It is "what risk is the investor underwriting?"

What venture capital is built to fund

Venture capital exists for companies where the upside is large enough to compensate for high uncertainty. At the earliest stages, the investor may be underwriting a founder, a market thesis, an early product, or a small amount of user traction. The business may not yet have reliable revenue, mature financial reporting, or a proven acquisition channel.

That uncertainty shapes the work. A venture investor spends a lot of time on founder quality, market size, product insight, category timing, and whether the company can become one of the few outcomes that matter for the fund. Financial models still matter, but they often matter less than judgment about the market and the team.

For founders, venture capital is usually the better fit when the company needs risk capital before the business can support debt or a later-stage private equity investor. It can fund product development, early hiring, customer acquisition, and the path toward product-market fit. The tradeoff is dilution, investor governance, and the pressure to pursue a venture-scale outcome.

What growth equity is built to fund

Growth equity is closer to expansion capital. The company has usually moved beyond "can this work?" and is asking "how fast can this scale?" The business may already have a repeatable sales motion, retention data, a management team, and enough financial history for deeper diligence.

That does not make growth equity risk-free. A growth investor can still overpay, misread market saturation, underestimate competition, or back a company whose unit economics weaken at scale. But the underwriting is different. Instead of betting mainly on invention and discovery, the investor is betting on execution against a proven base.

Growth equity can fund sales expansion, new product lines, international growth, acquisitions, hiring, infrastructure, or shareholder liquidity. It often sits inside the broader private equity universe, but it differs from a classic buyout because the investor is not usually buying control and using heavy leverage to transform the business. Private equity includes multiple strategies, including venture capital, growth capital, and buyouts (Private equity).

The six practical differences that matter

1. Company stage

Venture capital comes earlier. It is appropriate when the company still needs capital to prove product-market fit, build the first go-to-market motion, or turn early traction into a repeatable business.

Growth equity comes later. It is appropriate when a company has already proven demand and needs capital to accelerate a business that is working.

2. Revenue and profitability

VC-backed companies can raise before meaningful revenue, especially at pre-seed and seed. By Series A and later, investors expect more evidence, but the company can still be unprofitable if growth is strong enough.

Growth equity investors usually need more proof. They want revenue quality, retention, gross margin, sales efficiency, customer concentration, and a credible path to durable cash generation. Profitability is not always required, but the company usually cannot look like a science project.

3. Use of proceeds

Venture capital often funds discovery: product development, early team building, initial sales hires, category creation, and the next financing milestone.

Growth equity often funds acceleration: sales capacity, customer success, international expansion, acquisitions, product-line extension, or partial liquidity for existing shareholders.

4. Ownership and control

Both venture capital and growth equity often involve minority stakes. The difference is how much negotiating leverage the company has and what the investor needs to protect.

In venture, governance can include board seats, preferred stock rights, pro rata rights, information rights, and protective provisions. The NVCA model legal documents are a common industry reference for venture financings (NVCA model legal documents).

In growth equity, the rights package can be more heavily negotiated around downside protection, information access, liquidity, and operational milestones. The company may have more leverage if it is profitable and has multiple capital options.

5. Diligence style

Venture diligence is often thesis-heavy. The investor asks whether the team has unusual insight, whether the market can become large enough, whether the product has early pull, and whether the timing is right.

Growth equity diligence is usually more financial and operational. The investor has more company data to inspect: cohorts, retention, sales productivity, margins, pipeline quality, customer concentration, working capital, and management depth.

6. Exit path

VC funds can tolerate many losses if a small number of companies produce exceptional exits. That is why venture investors push for large outcomes.

Growth equity investors still need strong returns, but they are usually underwriting from a more established base. Exit paths can include strategic acquisition, sponsor sale, secondary sale, recapitalization, or IPO. The entry valuation and execution plan matter a lot because there is less room to rely on a single moonshot outcome.

When a founder should choose venture capital

Venture capital is usually the better fit when the company has a big market, high uncertainty, and a need to invest before the economics are fully proven.

Choose VC if:

- You are still proving product-market fit.

- You need capital for product, engineering, early sales, or category creation.

- The company can plausibly become much larger than a normal profitable business.

- You are comfortable with dilution and venture-style growth expectations.

- Your next milestone is another financing round, a major revenue inflection, or a step-change in market proof.

VC is not the right capital for every company. If the business can become a strong, profitable company but not a venture-scale outcome, venture funding can force the wrong strategy. The company may end up chasing growth that does not fit the market.

When a founder should choose growth equity

Growth equity is usually the better fit when the company already works and the main question is how to scale it faster without selling control.

Choose growth equity if:

- You have meaningful revenue and a repeatable sales motion.

- Your unit economics are visible enough for serious diligence.

- You need capital for expansion rather than basic proof.

- You want strategic support without necessarily selling the whole company.

- You may want to provide some liquidity to early shareholders or employees.

Growth equity can be attractive because it often avoids the binary feel of early venture. But it also comes with a higher diligence bar. A founder who cannot explain retention, margins, sales efficiency, pipeline conversion, and the use of proceeds will struggle with growth investors.

Where late-stage VC and growth equity overlap

The hardest cases sit between Series B and pre-IPO. A high-growth software company with strong retention, large revenue scale, and negative EBITDA could attract late-stage VC, growth equity, crossover investors, or traditional private equity growth funds.

In that zone, the label matters less than the investor's mandate:

- A late-stage VC may still focus on market dominance, category leadership, and a large IPO or acquisition.

- A growth equity investor may focus more on revenue quality, operating leverage, downside protection, and exit discipline.

- A private equity growth investor may care more about profitability, capital efficiency, and strategic optionality.

Founders should look past the fund label and ask what the investor will optimize for after closing. If the investor wants a venture-style growth plan and the management team wants steady profitable expansion, the mismatch will show up quickly.

Career fit: VC vs growth equity

For candidates, the difference is not just technical. The work feels different.

Venture capital roles reward curiosity, sourcing ability, market taste, founder judgment, and comfort with incomplete information. If you enjoy mapping emerging categories, meeting founders early, and forming a view before the numbers are obvious, VC may fit.

Growth equity roles usually lean more into financial analysis, commercial diligence, unit economics, market mapping, and operating metrics. If you like businesses with real data, later-stage diligence, and a clearer link between numbers and investment decisions, growth equity may fit better.

Neither path is easier. Early-stage VC can be ambiguous and network-driven. Growth equity can be analytically demanding and competitive with private equity, banking, and consulting talent pools.

If you are comparing roles, use the Venture Capital Careers job board to see how firms describe analyst, associate, platform, finance, and investor roles. Use the companies directory to compare firms that describe themselves around venture capital, growth equity, growth capital, private equity, or multi-stage investing. The naming is useful, but the job description usually tells you more than the category label.

For role preparation, start with venture capital skills and the venture capital career path. If you are still sorting out the broader asset class, compare this article with private equity vs venture capital, what venture capital is, and the growth equity primer.

Quick decision checklist

Use this as a fast filter.

| Question | Points toward VC | Points toward growth equity |

|---|---|---|

| Is the company still proving product-market fit? | Yes | Usually no |

| Is there meaningful recurring or repeatable revenue? | Helpful but not always required | Usually required |

| Is the main need discovery or scaling? | Discovery | Scaling |

| Can the company support detailed financial diligence? | Sometimes limited | Usually yes |

| Is profitability visible? | Not necessary early | Often important |

| Is the investor underwriting a power-law outcome? | Usually | Less purely |

| Does management want to keep control? | Maybe, but dilution compounds across rounds | Often yes, with minority capital |

The simple rule: choose venture capital when the company needs high-risk capital to prove a large opportunity. Choose growth equity when the opportunity is already proven and the capital is meant to scale it.

Frequently asked questions

Is growth equity a type of private equity?

Yes. Growth equity is generally considered part of private equity, but it is different from a classic leveraged buyout. Growth equity typically backs expanding companies and often takes minority stakes, while buyout investors more often seek control.

Is growth equity less risky than venture capital?

Usually, but not always. Growth equity companies tend to have more operating history, revenue, and customer data, which reduces some early-stage risk. The remaining risk shifts toward valuation, execution, competition, margin durability, and exit timing.

Is late-stage venture capital the same as growth equity?

Not exactly. Late-stage VC and growth equity can target similar companies, but the underwriting lens can differ. Late-stage VC may still prioritize category-defining upside. Growth equity usually places more weight on proven revenue quality, operational scale, and downside protection.

Do growth equity investors take control of the company?

Often they do not. Many growth equity deals are minority investments. That said, minority investors can still negotiate board seats, consent rights, information rights, and other protections.

Which is better for a finance career, venture capital or growth equity?

It depends on the work you want. VC is often better for people who like early markets, founder assessment, sourcing, and ambiguity. Growth equity is often better for people who like later-stage companies, financial analysis, commercial diligence, and operating metrics.

Can a company raise both venture capital and growth equity?

Yes. A company might raise venture capital at seed, Series A, and Series B, then later raise growth equity once the business has enough scale and predictability. The investor base can change as the company matures.