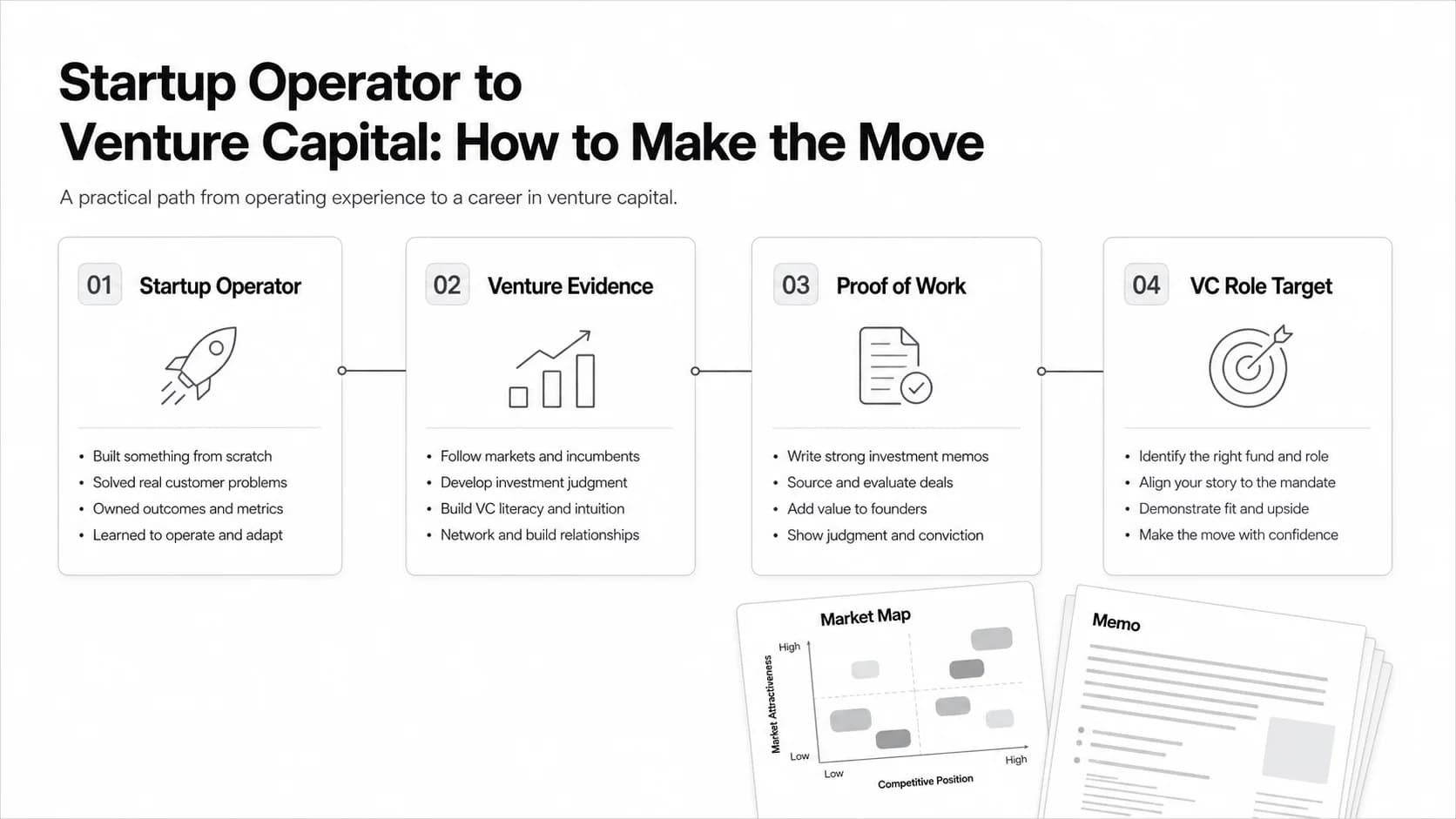

Startup Operator to Venture Capital: How to Make the Move

Learn how startup operators can move into venture capital, choose the right VC role, build proof of work, and position operating experience for VC jobs.

Startup operators can move into venture capital, but the transition works best when you prove more than "I have worked at startups." VC firms need evidence that you can find strong companies, understand markets, earn founder trust, and support portfolio companies without needing a long ramp.

The strongest operator-to-VC candidates usually do three things well. They choose the right type of VC role, translate operating experience into venture-relevant evidence, and build proof of work before they ask for interviews.

If you are a product, growth, sales, talent, BizOps, chief of staff, founder-success, partnerships, or startup finance operator, your operating background can be valuable. The question is where it fits.

The short answer

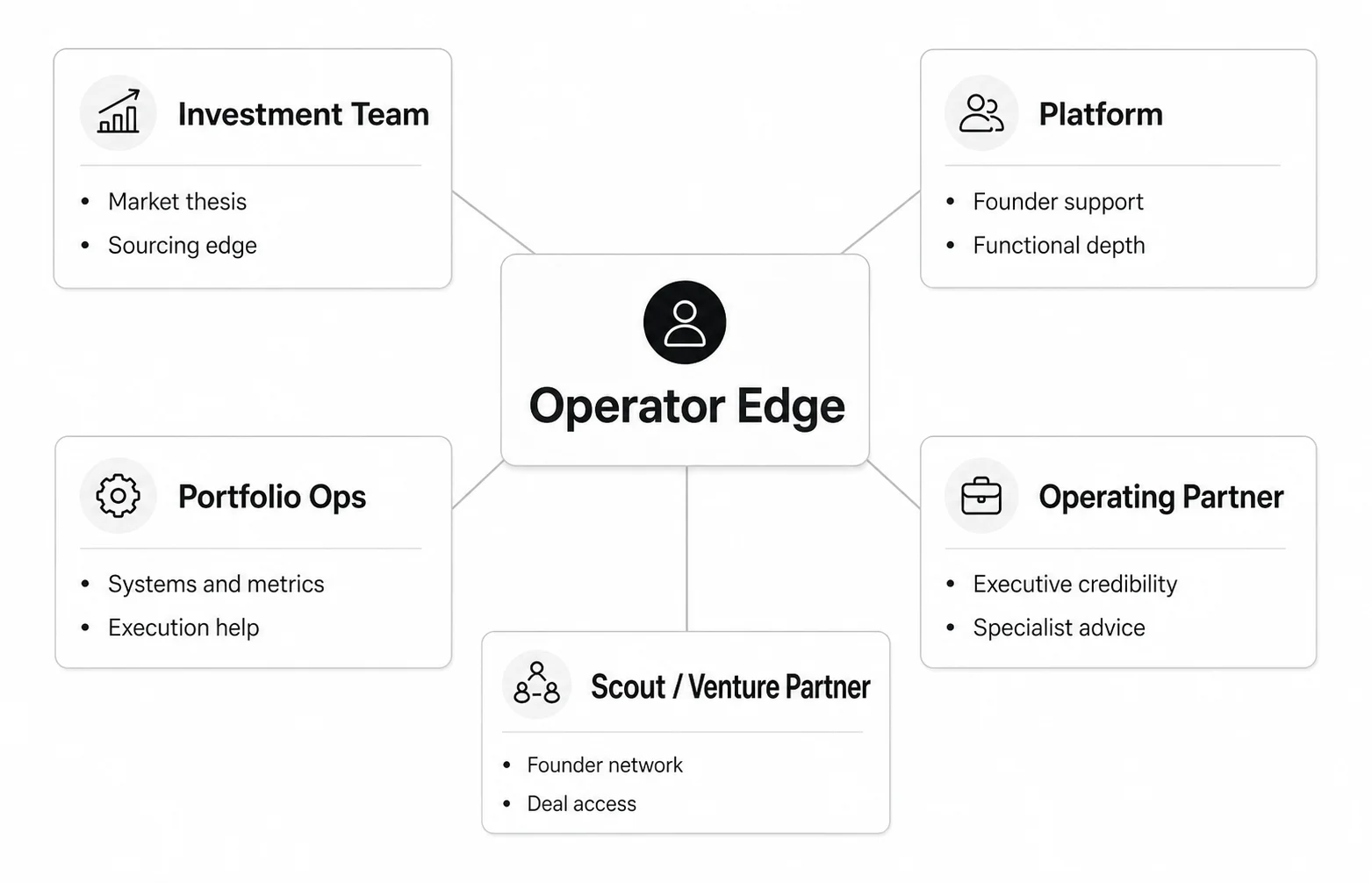

A startup operator can get into venture capital by targeting roles where their operating edge matters: investment roles in a sector they know, platform roles tied to their function, portfolio operations roles, operating partner roles, scout programs, or fund roles that need deep founder and market access.

Operating experience helps most when it gives you one of these advantages:

- access to founders before they are obvious;

- pattern recognition in a specific market or customer segment;

- functional depth that portfolio companies need;

- credibility with operators, buyers, or technical teams;

- a point of view on what makes a startup venture-backable.

It helps less when it is presented as generic startup exposure. "I worked at a startup" is not a VC hiring argument. "I built a GTM motion for developer-tool companies and can identify which early traction signals matter before a Series A" is much stronger.

What VC firms actually value from operators

VC firms do not hire operators because operators have been busy. They hire operators when that experience creates leverage for the fund.

| Operator advantage | Why it matters in VC | How to show it |

|---|---|---|

| Market proximity | You understand customer pain, buying behavior, and product timing in a specific category | Publish a market map or thesis on a sector you know well |

| Founder empathy | You know how founders make tradeoffs under pressure | Show examples of helping founders, executives, or startup teams make hard decisions |

| Functional depth | You can help portfolio companies with a real problem | Translate achievements in product, GTM, talent, growth, or ops into portfolio-support value |

| Network access | You know founders, operators, customers, or technical communities | Build a targeted list of companies and explain why they fit a fund's mandate |

| Commercial judgment | You can tell the difference between usage, revenue quality, and real demand | Write a short investment memo or customer-backed diligence note |

| Execution credibility | You know how messy startups actually work | Use examples with constraints, tradeoffs, and outcomes, not vague "fast-paced environment" language |

The main shift is from doing the work inside one company to judging many companies from the outside. Your edge is not that you know every answer. It is that you know which questions matter in a market you understand.

Which operator backgrounds translate best

Different operator backgrounds point toward different VC roles. Start with the work you can credibly do on day one.

| Operator background | Strong VC angle | Likely role targets |

|---|---|---|

| Product leader or PM | Product judgment, user pain, roadmap tradeoffs, technical customer insight | investment team in a known sector, platform, portfolio support |

| GTM, sales, or partnerships | Customer discovery, sales motion, pricing, channel strategy, buyer access | investment team for B2B funds, GTM platform, portfolio operations |

| Growth or marketing | Acquisition channels, activation, retention, category positioning | platform, growth support, consumer or SaaS investing roles |

| Talent or people ops | Hiring systems, executive search, compensation process, founder coaching | talent platform, portfolio talent, operating partner track |

| BizOps or chief of staff | Cross-functional problem solving, board materials, metrics, operating cadence | portfolio operations, platform, investment associate roles |

| Founder or early executive | Founder empathy, company-building pattern recognition, network access | investment team, venture partner, scout, operating partner |

| Finance or revenue operations | Metrics, forecasting, pipeline quality, operating dashboards | portfolio operations, fund operations, growth-stage investing |

Do not over-index on title. A senior operator with no investing evidence may be less compelling for an investment role than a mid-level operator who has built a strong thesis, sourced relevant companies, and written thoughtful memos.

Choose the right VC role target

Many operators say they want to "break into VC" before deciding which VC job they actually want. That creates weak applications.

| Role target | Best fit for | What you need to prove |

|---|---|---|

| Investment team | Operators with market insight, founder access, and clear investment judgment | Sourcing ability, market thesis, diligence thinking, memo writing |

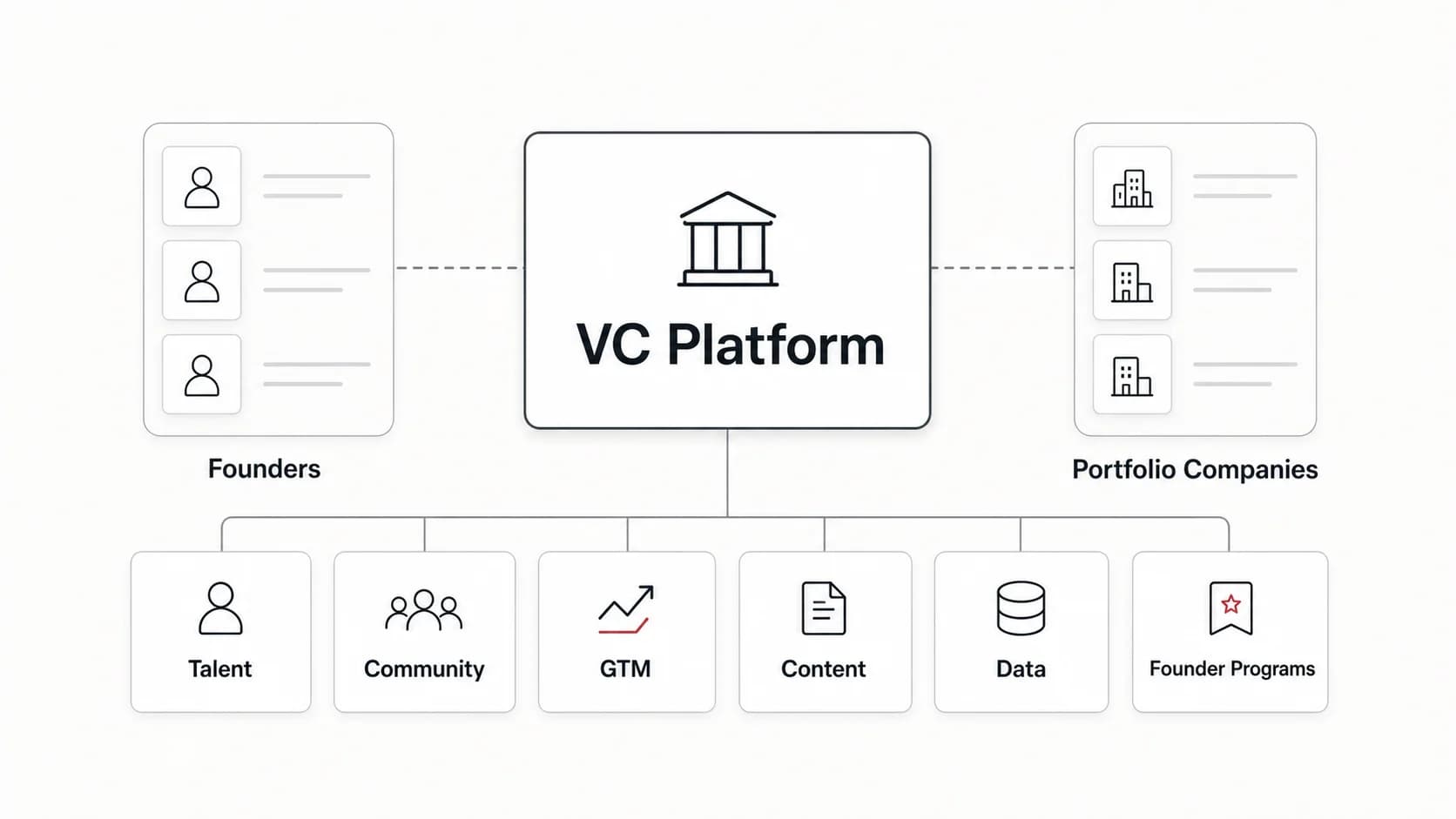

| Platform role | Operators who like helping many portfolio companies at once | Functional depth, program design, founder support, network building |

| Portfolio operations | Operators who can improve systems, metrics, hiring, GTM, or execution across companies | Repeatable playbooks, stakeholder management, measurable operating results |

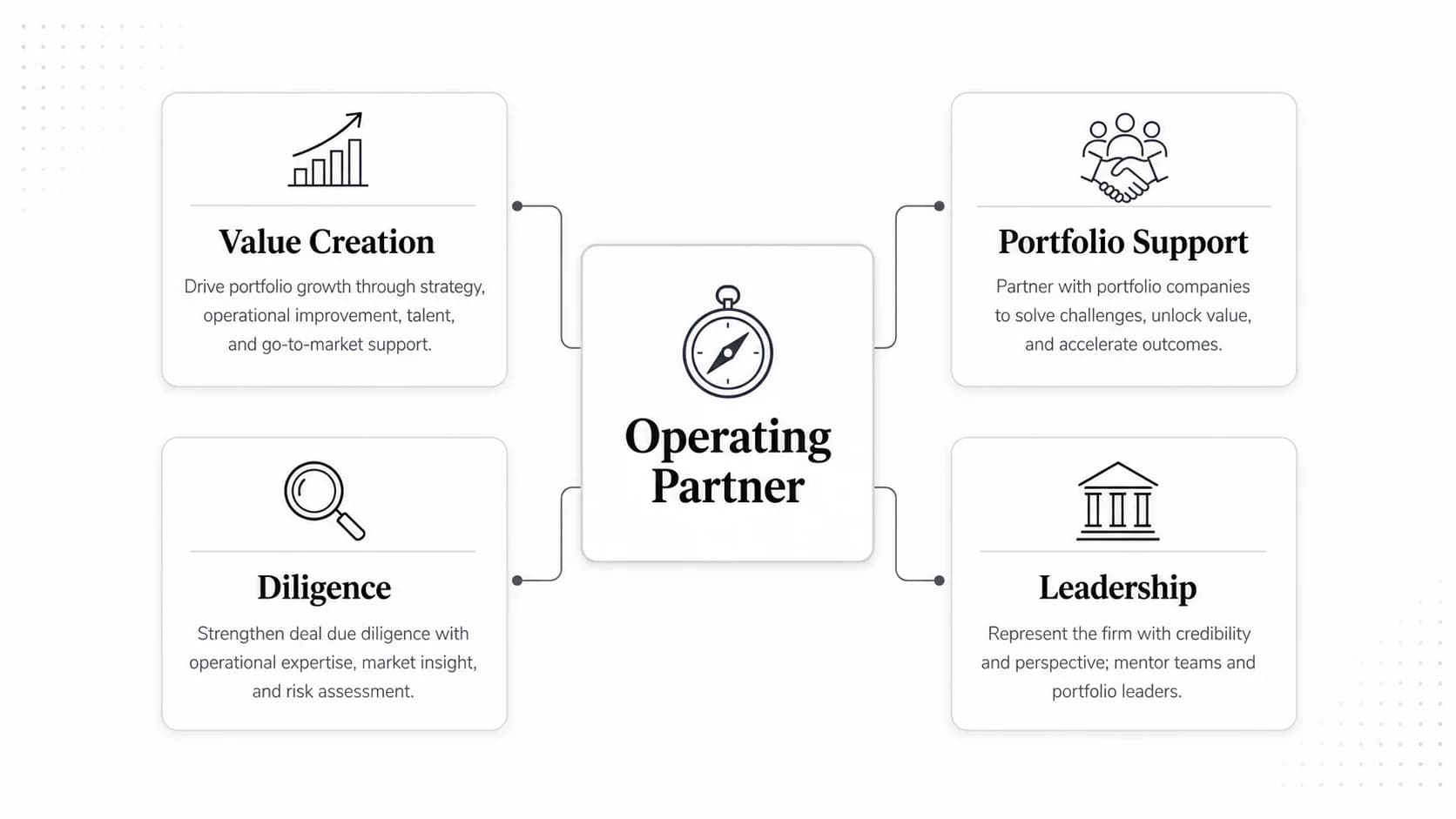

| Operating partner | Senior operators with deep executive credibility | Decades or highly concentrated functional expertise, founder trust, advisory range |

| Scout or venture partner | Operators with strong founder networks but limited full-time VC availability | Deal flow, judgment, trust with a fund, consistent sourcing |

| Fund operations or investor relations | Operators with finance, ops, reporting, or process strength | Data quality, reporting cadence, LP communication, internal systems |

If you are unsure, compare active postings on the Venture Capital Careers job board. Search for investment, platform, portfolio, talent, GTM, operations, chief of staff, scout, and operating partner roles. The job descriptions will show which funds want investors, which want functional operators, and which want hybrid profiles.

For a deeper role breakdown, read the venture capital career path guide. If your operator background points toward founder support rather than deal execution, the VC platform role guide is the better next stop.

Translate operating experience into VC evidence

The biggest mistake operators make is describing their old job instead of translating it into VC evidence.

| Weak operator framing | Stronger VC framing |

|---|---|

| "I led product at a startup." | "I can evaluate product velocity, roadmap tradeoffs, user pain, and founder-product judgment in early-stage software companies." |

| "I ran sales." | "I can assess whether early revenue is founder-led, repeatable, or inflated by a few warm relationships." |

| "I worked in customer success." | "I can diligence retention quality, expansion potential, implementation risk, and customer references." |

| "I built a recruiting function." | "I can help portfolio companies design hiring systems and evaluate whether a founder can recruit above their weight." |

| "I was chief of staff." | "I can read operating metrics, synthesize messy information, and turn ambiguous problems into decisions." |

| "I have a founder network." | "I can source companies in a specific wedge, explain why they fit the fund, and earn founder responses." |

This translation should show up in your resume, networking emails, interview stories, and proof-of-work artifacts. Use the venture capital resume guide to rewrite bullets around evidence, not responsibilities.

Build proof of work before you apply

Operators often wait for permission to act like investors. Do the opposite. Build proof before applying.

A simple 30-day plan is enough:

| Week | Work | Output |

|---|---|---|

| 1 | Choose one sector you know from operating experience | A one-page market map with segments, buyer pain, incumbents, and startup wedges |

| 2 | Identify 20-30 startups in that sector | A ranked company list with why each could matter and which funds might care |

| 3 | Pick 2 companies and write short memos | Two 1-2 page memos with market, product, traction signals, risks, and fund fit |

| 4 | Start targeted conversations | Five thoughtful outreach emails to investors, founders, or operators tied to your thesis |

The goal is not to pretend you already have a fund. The goal is to show the behaviors that VC firms care about: curiosity, synthesis, market judgment, sourcing, and communication.

Strong proof-of-work artifacts include:

- a market map in a category where you have operating context;

- a short investment memo on a startup you know from public information and customer insight;

- a founder-support playbook tied to your function, such as hiring first sales reps or improving onboarding;

- a portfolio-support idea for a specific fund based on its stage and portfolio;

- a curated list of startups a fund should know about, with clear reasoning.

Keep the artifact concise. A five-page memo with sharp judgment is better than a 40-slide deck that hides the answer.

Position your resume and outreach

Your resume should make the operator-to-VC argument obvious. Do not force the reader to infer it.

For investment roles, emphasize:

- markets you understand deeply;

- companies or founders you can access;

- commercial judgment and customer insight;

- strategic analysis and memo-quality writing;

- examples of evaluating opportunities, not just executing tasks.

For platform or portfolio roles, emphasize:

- repeatable systems you built;

- founder or executive stakeholders you supported;

- functional results in talent, GTM, product, growth, data, or operations;

- playbooks that could help multiple portfolio companies;

- community, event, or network-building experience where relevant.

Your outreach should be equally specific. A weak email says you are passionate about VC. A strong email says why your operating background is relevant to that fund.

Example positioning: I have spent the last four years building GTM systems for vertical SaaS companies selling into healthcare buyers. I am exploring VC roles where that operator context can help with sourcing and diligence in healthcare software. I put together a short market map of 24 companies in the category and would value your feedback on whether the wedge is fundable.

Use the VC networking email templates guide to turn that positioning into concise outreach and follow-up messages.

Find operator-friendly VC roles

Operator-friendly VC jobs are not always labeled "operator." Search by function and responsibility, not just by title.

Useful searches include:

- platform;

- portfolio operations;

- talent partner;

- GTM platform;

- founder success;

- operating partner;

- venture partner;

- investment associate plus your sector;

- chief of staff;

- ecosystem;

- partnerships.

Use the Venture Capital Careers companies directory to build a target list before applying. For each fund, check:

- stage focus;

- sector focus;

- portfolio companies that match your background;

- whether the firm already has platform or operating support;

- recent roles the firm has posted;

- partner backgrounds and public writing.

Then use the VC job board to compare live roles. A fund hiring a platform or portfolio role may value operator depth immediately. A fund hiring an investment associate may still value your background, but you need more evidence of sourcing and investment judgment.

Prepare for interviews as an operator

Operator candidates should prepare for two types of interview questions.

The first type tests your operating credibility:

- What did you actually own?

- What changed because of your work?

- What constraints did you face?

- How did you make decisions with incomplete information?

- Which founder or executive problems can you help with now?

The second type tests your investor potential:

- What market are you excited about and why?

- Which startup would you invest in?

- What would make you pass?

- How would you diligence this company?

- What customer signal matters most?

- What would have to be true for this company to return the fund?

Operators often do well on the first set and underprepare for the second. Do not assume operating credibility answers investment questions. Practice market sizing, thesis development, deal evaluation, and concise recommendations.

For investment-style interviews, use the venture capital case study interview guide. For broader interview prep, review common venture capital interview questions.

Common mistakes operators make

Treating startup experience as self-explanatory. VC firms need to know why your experience creates an edge for this fund and this role.

Targeting every VC role the same way. Investment, platform, portfolio, and operating partner roles have different scorecards.

Overstating investment readiness. Being close to startups is not the same as judging investments. Build proof of investment thinking.

Ignoring fund fit. A consumer growth operator may be more compelling to a consumer seed fund than to a deep-tech growth fund.

Sending generic networking emails. Operators should have better context than generic applicants. Show it.

Only applying to posted investment roles. Many operator-friendly paths come through platform, portfolio, scout, or sector-specialist roles.

Skipping writing. VC work is communication-heavy. A concise memo, thesis, or market map can do more than another coffee chat.

FAQ

Can startup operators get jobs in venture capital?

Yes. Startup operators can get VC jobs when their experience maps to a fund's needs and they show evidence of market judgment, founder access, portfolio support, or investment thinking. The transition is strongest when the operator targets a role where their function or sector expertise matters.

Is operating experience enough for an investment role?

Usually not by itself. Operating experience can be a strong edge, but investment roles also require sourcing, diligence, market analysis, memo writing, and judgment about fund-scale outcomes. Build proof of those skills before applying.

Are platform roles better for operators than investment roles?

Sometimes. Platform roles can be a better fit if your strongest value is helping portfolio companies with talent, GTM, product, growth, community, or operations. Investment roles can be a better fit if you have strong sector insight, founder access, and evidence of investment judgment.

What should an operator include in a VC resume?

Include operating achievements that translate into venture value: markets you know, customer segments you understand, founders or operators you can access, playbooks you built, and examples of judgment under uncertainty. Avoid generic startup responsibilities.

What proof of work is most useful?

A market map, investment memo, startup shortlist, or portfolio-support playbook is usually more useful than a broad personal essay. The best artifact should connect your operating experience to a fund's stage, sector, and portfolio.

Should founders move into VC?

Founders can move into VC, especially when they bring founder empathy, company-building pattern recognition, and a strong network. They still need to show they can evaluate other companies objectively and work inside a fund model.

Find VC roles that value operating experience

The operator-to-VC move is easier when you stop asking whether VC firms hire operators in general and start finding the funds that need your specific edge.

Build a shortlist of funds by stage, sector, and portfolio fit in the companies directory. Then compare open roles on the Venture Capital Careers job board and look for language that values founder support, GTM, product, talent, portfolio operations, or sector expertise.

Once you have a target list, tailor your resume, write a short proof-of-work artifact, and send outreach that shows why your operating experience is useful to that specific fund.