What is a Lead Investor? Definition, Responsibilities, FAQs

A lead investor anchors a startup funding round, negotiates terms, coordinates diligence, and helps other investors decide whether to follow.

A lead investor is the investor who anchors a startup funding round. The lead usually commits meaningful capital, negotiates the main terms, coordinates diligence, and gives other investors enough confidence to join the round on the same terms.

For founders, the lead investor is more than the first name on the cap table. The lead can determine valuation, shape governance, set the pace for legal work, and influence whether the rest of the syndicate closes. For candidates and operators studying venture capital, the lead role is also a useful window into how deals actually get done inside a fund. If you are researching active VC firms, start with the Venture Capital Careers company directory and compare firms by stage, sector, and portfolio pattern.

What is a lead investor?

A lead investor is the primary investor responsible for leading a financing round. In a venture round, that usually means the lead negotiates the term sheet, performs or coordinates diligence, commits a large enough check to anchor the raise, and helps bring in follow-on investors.

The lead investor does not always invest the most money, but they usually take the most responsibility. If another investor writes a large check but does not negotiate terms, coordinate the round, or stand behind the diligence process, that investor may be an anchor investor or a major participant rather than the true lead.

The lead matters because startup fundraising is a coordination problem. Founders need capital, investors need conviction, and everyone needs common terms. A credible lead reduces uncertainty by saying, in effect: we have done the work, we are willing to set the deal, and we are prepared to help the company after the round closes.

What a lead investor actually does

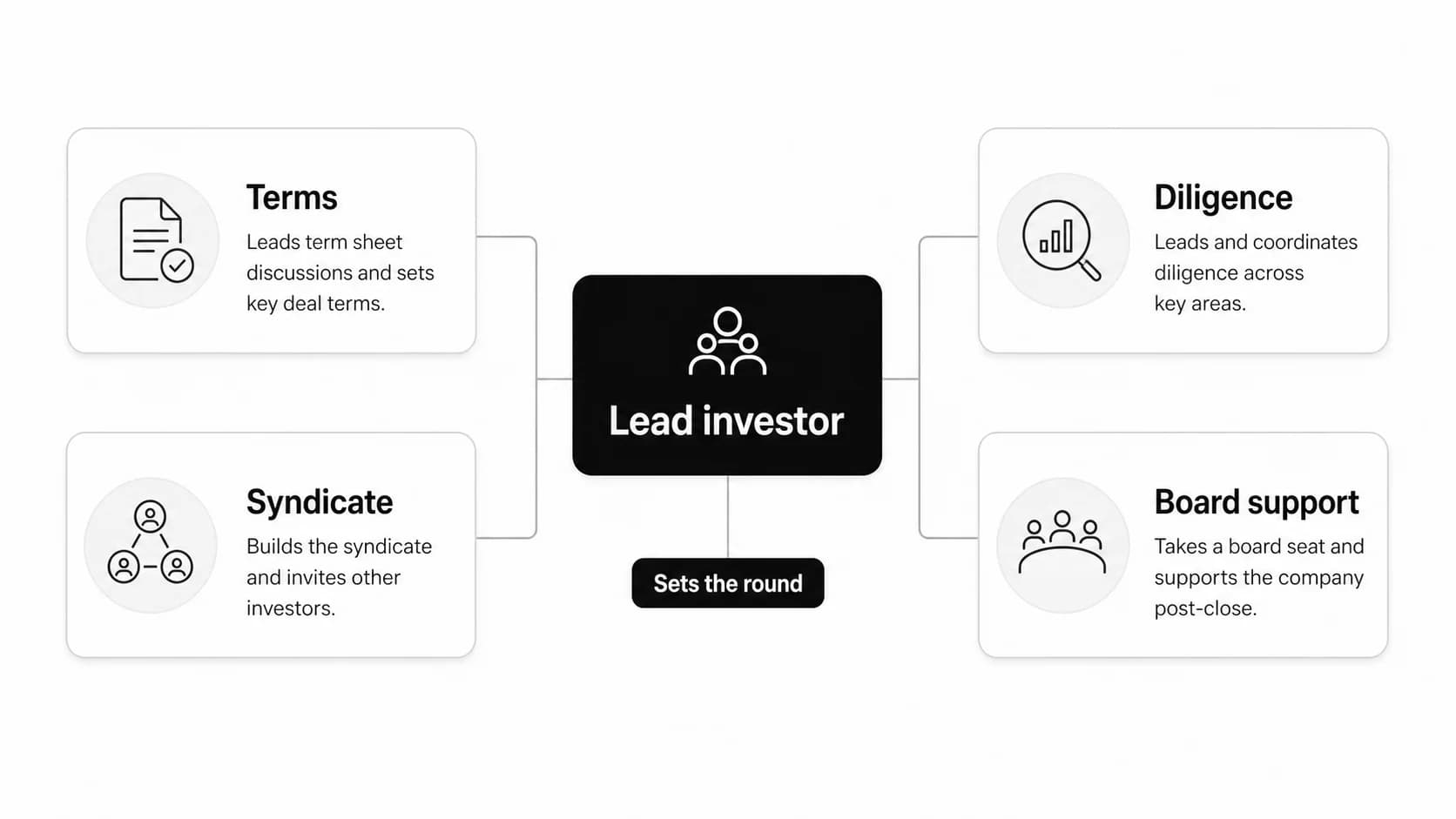

The lead investor's job changes by round and deal structure, but most lead roles include four responsibilities: terms, diligence, syndicate building, and post-close support.

| Responsibility | What the lead does | Why it matters |

|---|---|---|

| Terms | Negotiates valuation, security type, pro rata rights, board rights, and other key economic or control terms | Creates the deal structure that follow investors can accept |

| Diligence | Reviews the market, product, team, financial model, legal posture, customer proof, and risks | Gives the round a credible investment case |

| Syndicate | Helps fill the round with follow investors, angels, strategic investors, or other funds | Converts one commitment into a complete financing |

| Allocation | Works with the founder on how much room each investor receives | Keeps ownership, investor mix, and future financing needs aligned |

| Post-close support | Often takes a board seat or observer role and helps with hiring, customers, future fundraising, and strategy | Makes the investor useful after the wire hits |

The lead does not replace founder judgment. A strong founder still needs counsel, clean process, and a clear view of what they are giving up. But a serious lead investor should make the round easier to understand, not more chaotic. If diligence is vague, terms keep changing, or the lead cannot explain why the deal should clear, the company may not have a real lead yet.

For a deeper look at the diligence work behind venture rounds, see Venture Capital Careers' venture capital due diligence breakdown.

Lead investor vs follow investor vs anchor investor

Lead, follow, and anchor investor are often used loosely. They can overlap, but they are not the same role.

| Investor type | Primary role | Typical behavior | Common confusion |

|---|---|---|---|

| Lead investor | Leads the round | Negotiates terms, drives diligence, anchors the syndicate, may take board rights | Can be mistaken for any large investor |

| Follow investor | Joins the round | Invests on terms already set by the lead, often with lighter diligence | May still be valuable even without leading |

| Anchor investor | Provides a large or early commitment | Signals momentum and may help attract other investors | May or may not negotiate terms or lead diligence |

A lead investor can also be an anchor investor if they commit early and write a meaningful check. An anchor investor is not automatically the lead if another investor owns the term sheet and the diligence process.

In angel rounds, the distinction can be looser. A respected angel may coordinate other angels, help set terms, and act like the lead even without a formal fund structure. In institutional venture rounds, the lead role is usually more formal because board rights, information rights, pro rata rights, and future financing expectations matter more.

What changes in a seed round or Series A

In a seed funding round, the lead investor often gives the company its first major outside validation. The founder may still have limited revenue, a small team, or an early product. A good seed lead is underwriting the market, founder quality, early traction, and the possibility that the company can raise again.

In Series A funding, the lead investor usually expects more evidence. Diligence becomes more formal. The lead may spend more time on retention, go-to-market efficiency, financial planning, hiring plan, customer concentration, and the company's ability to scale. Board structure also becomes more important because the Series A lead may join the board and shape future financing decisions.

| Round | What the lead is really underwriting | Founder question to ask |

|---|---|---|

| Pre-seed or seed | Founder-market fit, early product signal, speed of learning, investor demand | Can this investor help us reach the next proof point? |

| Series A | Repeatable growth, team quality, market size, financing plan, governance | Can this investor help us scale without distorting the company? |

| Later stage | Metrics quality, market leadership, exit path, financial controls | Can this investor support institutional-grade execution? |

Lead quality is partly about stage fit. A famous growth fund may not be the right seed lead if it cannot move quickly, size the check appropriately, or help with the messy early work. A strong seed fund may not be the right Series B lead if it cannot support later-stage governance and financing expectations.

How founders evaluate a potential lead investor

The best lead is not always the highest valuation or the most recognizable brand. The right question is: can this investor credibly lead this round and help the company after close?

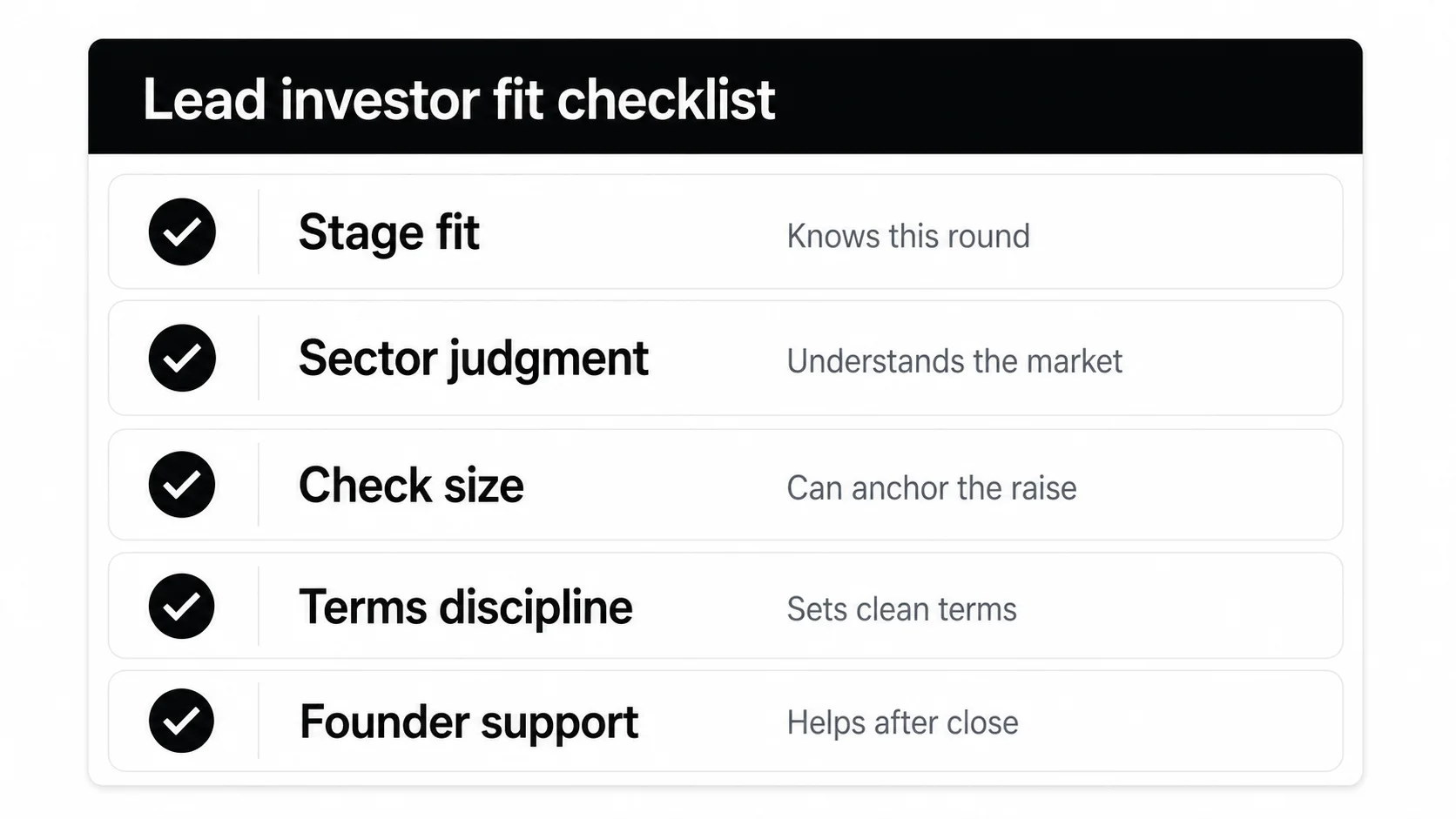

Use five tests before accepting a lead:

- Stage fit: They regularly lead rounds at your stage and know what proof points matter next.

- Sector judgment: They understand your market well enough to challenge assumptions, not just repeat your pitch.

- Check size: Their commitment is large enough to anchor the round without consuming too much ownership.

- Terms discipline: They can explain the proposed valuation, security, rights, and governance terms clearly.

- Founder support: Their references show they help after close, especially when the company misses plan.

Founder references are the fastest reality check. Ask portfolio founders how the investor behaved during diligence, after close, during hard quarters, and before the next round. A lead investor who is helpful only while the deal is competitive may not be the partner you want when the company is harder to finance.

Red flags in a would-be lead investor

A weak lead can create more risk than no lead at all. Watch for these signals:

- They want the title of lead investor but will not write or secure a meaningful check.

- They avoid putting real terms in writing.

- They keep reopening valuation, ownership, or governance after other investors have started diligence.

- Their diligence process is slow, unfocused, or repeatedly asks for information already provided.

- They cannot explain what follow investors should believe.

- Their founder references are thin, guarded, or consistently negative.

- Their support expectations do not match your needs after close.

Some of these issues are normal negotiation friction. The pattern matters. A good lead brings clarity even when the terms are tough. A poor lead turns ambiguity into leverage and leaves the founder managing the round alone.

What candidates should understand about lead investors

For VC candidates, lead investor work is where many core investing skills come together: market mapping, company analysis, founder judgment, diligence, valuation, term negotiation, syndicate judgment, and portfolio support.

If you want to understand a venture firm's investing style, look at where it leads rather than only where it participates. A firm that repeatedly leads seed rounds is likely making early conviction calls. A firm that mostly follows later rounds may be optimizing for access, portfolio construction, or thematic exposure. Neither model is inherently better, but the work inside the fund can look very different.

Candidates can use Venture Capital Careers to browse open roles on the VC job board and research firms in the companies directory. When reading job descriptions, look for phrases like sourcing, diligence, investment memo, portfolio support, board materials, and market mapping. Those signals tell you whether the role sits close to lead-investor work or more toward platform, operations, or portfolio reporting.

Frequently asked questions

Does a lead investor always invest the most?

Not always. The lead usually commits a meaningful amount and takes responsibility for terms and diligence, but another investor may write a large check without leading the round. Control of the process matters as much as check size.

Does the lead investor always take a board seat?

No. Board rights depend on the round, security, ownership, company stage, and negotiation. A Series A lead often seeks a board seat. A seed lead may take a board observer role or no formal seat, especially in a smaller round.

Can a round have co-lead investors?

Yes. Co-leads can share the round when two investors split the check, diligence, or strategic value. Co-leads work best when responsibilities are clear. If every investor assumes someone else owns the hard work, the round can stall.

Is an anchor investor the same as a lead investor?

Sometimes, but not always. An anchor investor provides an important commitment that creates momentum. A lead investor sets or negotiates terms, coordinates diligence, and helps organize the syndicate. One investor can do both.

How do founders find a lead investor?

Founders usually find a lead through warm introductions, founder references, sector-focused research, accelerators, angel networks, and direct outreach to funds that already invest at the right stage. The better starting point is not the investor's brand; it is fit with stage, sector, check size, and support model. For the investor landscape, compare angel investors and venture capitalists and research active VC firms before beginning outreach.