What Is a Follow-on Investment?

A follow-on investment is additional capital invested after an initial round. Learn how follow-on funding works, why pro rata rights matter, and how founders and investors should evaluate the next check.

A follow-on investment is additional capital invested in a company after an earlier investment has already been made. In venture capital, it usually means an existing investor puts more money into a portfolio company in a later financing round, or a new investor joins a later round after the company has already raised seed, Series A, or other funding.

The phrase matters because follow-on funding is not just "more money." It affects ownership, dilution, investor signaling, runway, and the company's ability to raise the next round on credible terms.

What is a follow-on investment?

A follow-on investment is a later investment in a company that has already raised capital. If a VC fund invested in a startup's seed round and then invests again in the Series A, the Series A check is a follow-on investment for that fund.

Follow-on investments can happen in several ways:

- An existing investor exercises pro rata rights to maintain its ownership percentage.

- An existing investor invests more than pro rata to increase conviction in the company.

- A new investor joins a later round after another investor leads or prices the financing.

- Insider investors support a bridge, extension, down round, or recapitalization when the company needs more runway.

In private startup financing, follow-on investment is different from a public-company follow-on offering. A public follow-on offering happens after a company is already public. A startup follow-on investment usually happens while the company is still private and is negotiated through venture financing documents, side letters, SAFEs, convertible notes, or preferred stock rounds.

How follow-on investment works in venture capital

Venture-backed companies usually raise capital in stages. A founder might start with pre-seed or seed funding, then raise Series A funding once the company has stronger evidence of product-market fit, and later raise Series B or growth rounds to scale.

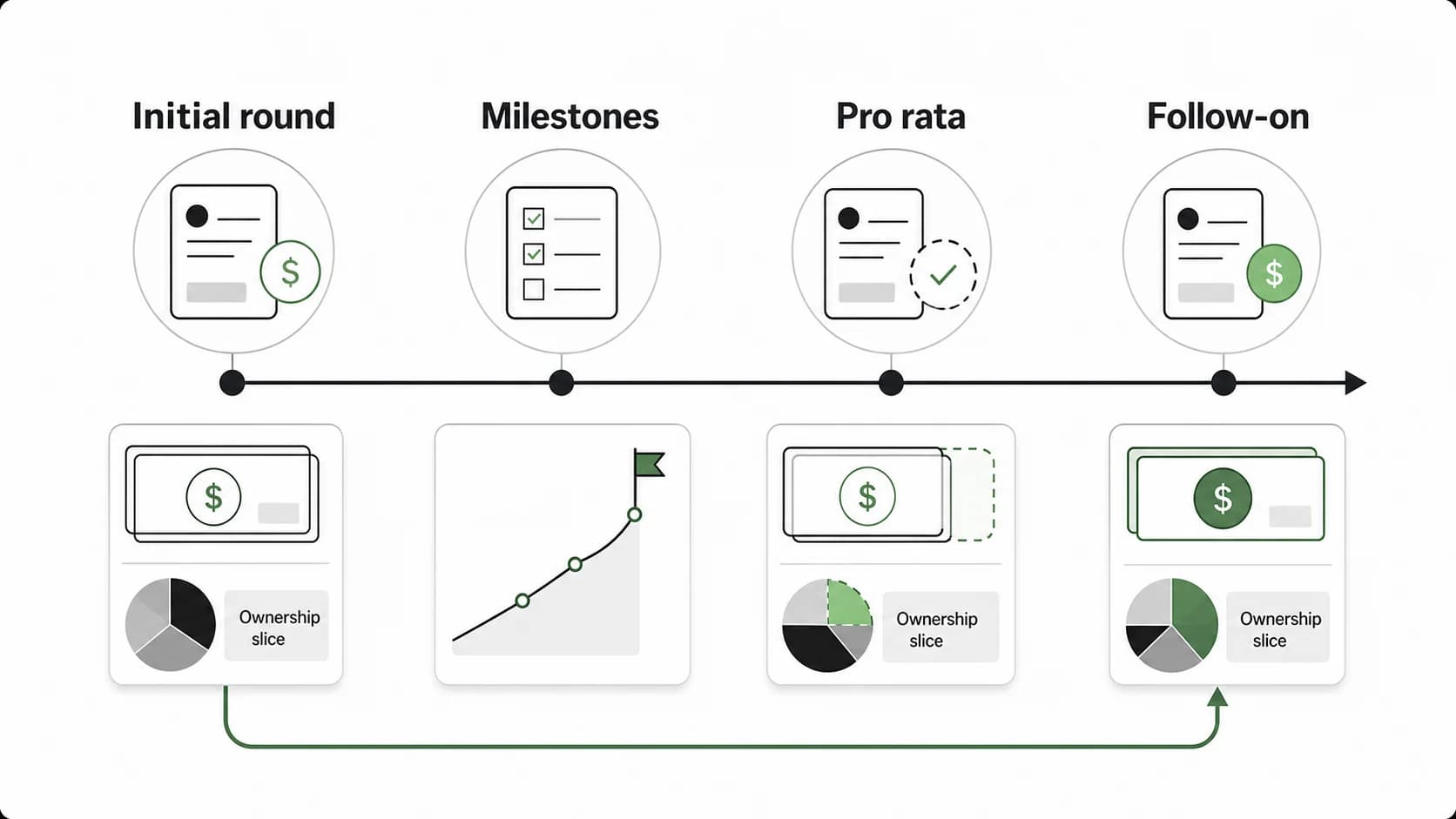

Follow-on investment sits inside that staged model:

- The company raises an initial round.

- Investors receive equity, a SAFE, a convertible note, or preferred stock.

- The company uses the money to hit milestones.

- The company raises another financing round.

- Existing investors decide whether to participate again.

- New investors evaluate whether insider support is strong enough to trust the round.

The exact documents depend on the round. The NVCA model legal documents are a common reference point for venture financings, including documents such as the Investors' Rights Agreement. At the earliest stages, many startups use YC-style SAFEs; Y Combinator's SAFE document set includes post-money SAFE forms and optional pro rata side letters.

Follow-on investment example

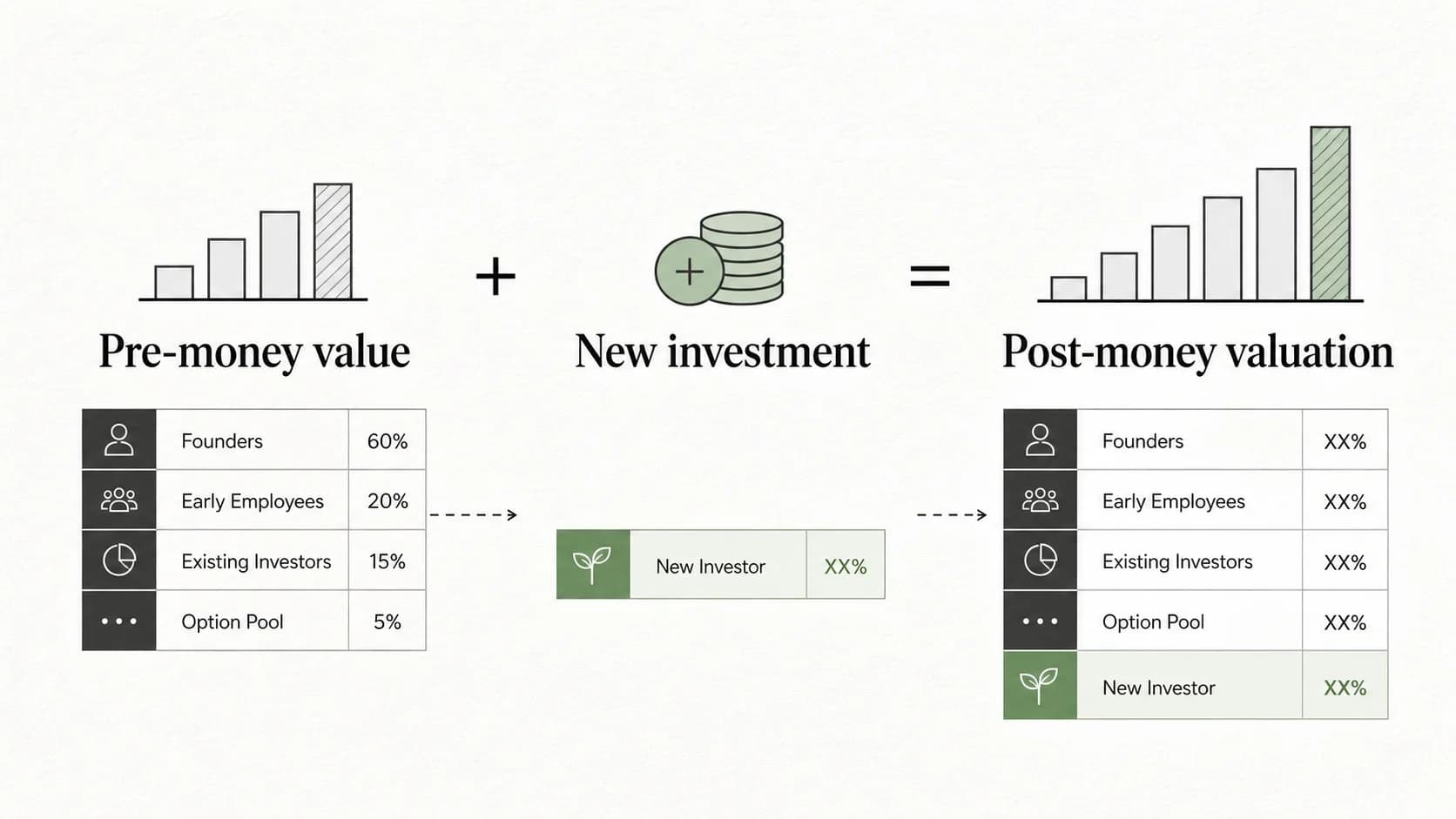

Assume a startup raises a $2 million seed round at a $10 million post-money valuation.

An investor puts in $500,000. After the seed round, that investor owns 5% of the company.

One year later, the company raises a $6 million Series A at a $30 million pre-money valuation and $36 million post-money valuation.

If the seed investor has pro rata rights and wants to maintain 5% ownership, it needs to own 5% of the company after the Series A. Five percent of the $36 million post-money valuation equals $1.8 million of ownership value. The investor already holds roughly $1.5 million of implied value at the new pre-money valuation, so it would invest about $300,000 in the Series A to maintain its stake.

That $300,000 is the follow-on investment.

If the investor does not participate, its ownership percentage falls. That is dilution. Dilution is not automatically bad; a smaller percentage of a more valuable company can still be a better outcome. But for investors, declining to follow on means giving up ownership in a company they already know.

Why investors make follow-on investments

VC funds do not usually deploy all their capital into first checks. They reserve capital for later rounds so they can keep supporting the strongest companies in the portfolio.

Investors make follow-on investments for several reasons:

- Maintain ownership. Pro rata participation keeps the investor from being diluted below its target stake.

- Double down on winners. A fund may want more exposure to a company that is outperforming expectations.

- Signal confidence. Insider participation can make it easier for a new lead investor to underwrite the round.

- Protect prior capital. In a difficult market, a bridge or inside round may give the company enough time to reach the next milestone.

- Preserve influence. Larger ownership can support board, information, or major-investor rights, depending on the documents.

The harder decision is not whether follow-ons matter. It is which companies deserve more capital. A VC fund that follows on indiscriminately can trap too much capital in weaker companies. A fund that never follows on may get diluted out of its best investments.

Why founders seek follow-on funding

For founders, follow-on funding can be useful because existing investors already know the company. They have seen the board materials, product progress, hiring plan, customer pipeline, and cash burn. That context can shorten the fundraising process.

Follow-on funding can help when:

- The company has hit real milestones and wants to raise a larger priced round.

- Existing investors want to support the company before a new lead commits.

- The startup needs a bridge to reach a revenue, product, regulatory, or hiring milestone.

- Insider support will make the round more credible to outside investors.

- The company needs strategic help from investors with sector knowledge.

But founders should not treat insider money as automatically founder-friendly. Follow-on capital can come with valuation pressure, new protective terms, a pay-to-play provision, or signaling risk if important insiders decline to participate.

The key question is whether the follow-on round improves the company's odds of reaching a stronger next milestone, or merely delays a hard reset.

Follow-on investor vs lead investor vs existing investor

The term "follow investor" can mean different things depending on context.

| Role | Meaning | What they usually do |

|---|---|---|

| Existing investor | Already invested in a prior round | Decides whether to invest again, exercise pro rata, or support a bridge |

| Follow-on investor | Invests after an earlier investment or joins a later round | Adds capital after the company has more history |

| Follow investor | Often used informally for a non-lead investor that follows another investor into a round | Participates in the syndicate but usually does not set terms |

| Lead investor | Negotiates price, terms, and often board/governance rights | Anchors the round and helps other investors underwrite it |

A follow-on investor is not always a passive follower. An existing investor can lead a follow-on round. A new investor can follow a lead investor into the round. A small angel can follow on pro rata without shaping the terms. The role depends on who sets the price, who negotiates documents, and who writes the meaningful check.

Follow-on investment vs follow-on offering

These terms are easy to confuse.

A follow-on investment in venture capital usually refers to additional private investment in a startup after an earlier round.

A follow-on offering or FPO usually refers to a public company issuing or selling additional shares after its IPO. Public-market follow-on offerings can be dilutive or non-dilutive depending on whether new shares are issued or existing holders sell shares.

For most founders, startup operators, and VC candidates, the private-company meaning is the more relevant one. If a startup is raising a Series A, Series B, bridge round, or insider extension, the useful questions are about runway, ownership, valuation, investor support, and terms.

When follow-on investment is a warning sign

Follow-on funding is not always positive. It can signal strength when existing investors are increasing ownership in a company with real momentum. It can signal stress when insiders are the only available capital and the company cannot attract an outside lead.

Watch for these issues:

- Weak insider support. If major existing investors do not participate, new investors may ask why.

- Bridge-to-nowhere risk. A bridge round should fund a specific milestone, not just postpone the next hard conversation.

- Overly punitive terms. Down rounds, pay-to-play provisions, and heavy preferences can help close a financing but damage future incentives.

- Overcapitalization. Too much money at too high a valuation can make the next round harder.

- No clear use of proceeds. Follow-on funding should tie to hiring, product, revenue, regulatory progress, market expansion, or a concrete operating plan.

A good follow-on round buys progress. A weak one buys time without changing the company's financing story.

How to evaluate a follow-on round

Founders and investors should evaluate follow-on investment with different lenses, but the core questions overlap.

| Question | Why it matters |

|---|---|

| What milestone does this money fund? | The round should move the company to a stronger financing or operating position. |

| Who is leading or validating the round? | Insider-only support and outside-led rounds send different signals. |

| Are existing investors using pro rata rights? | Participation can indicate conviction; non-participation can create questions. |

| How much dilution does the round create? | New money may be worth it, but ownership tradeoffs should be explicit. |

| Are the terms clean enough for the next round? | Heavy preferences or harsh investor protections may create future friction. |

| Does the investor fit the next stage? | A seed investor, Series A lead, growth investor, and strategic investor may help in different ways. |

If you are researching which firms invest by stage, sector, or geography, the Venture Capital Careers VC companies directory can help you scan thousands of VC and growth investors before building a target list.

What follow-on investment means in VC careers

For analysts and associates, follow-on decisions show up in portfolio reviews, investment committee memos, reserve planning, and board prep. The work is less about memorizing the definition and more about answering a sharper question: should the fund put more money behind this company now?

That analysis usually covers:

- Original investment thesis versus actual progress.

- Revenue, product, hiring, and customer milestones.

- Cash runway and burn multiple.

- New round valuation and ownership impact.

- Whether the company can attract a credible lead.

- How much reserve capital the fund has left.

- What happens if the fund does not participate.

In other words, follow-on investment is where conviction gets tested after the first check.

FAQ

What is follow-on investment meaning?

Follow-on investment means additional investment in a company after an initial investment has already been made. In venture capital, it often refers to an existing investor participating in a later startup funding round.

Is follow-on funding the same as a bridge round?

No. A bridge round is one type of follow-on funding. It usually gives the company enough runway to reach a specific milestone before a larger financing. A follow-on investment can also happen in a normal Series A, Series B, or growth round.

Is follow-on investment dilutive?

Usually, yes, if the company issues new equity. Existing shareholders who do not participate may own a smaller percentage after the round. Investors with pro rata rights may invest more to maintain their ownership percentage.

Can a new investor make a follow-on investment?

Yes, if the phrase is being used to describe a later financing after the company has already raised capital. More commonly, though, "follow-on" refers to an existing investor investing again in a portfolio company.

Why would an investor not follow on?

An investor may decline because the company missed milestones, the valuation is too high, the fund lacks reserves, the company no longer fits the fund's strategy, or the investor wants to reserve capital for stronger portfolio companies.

What is a follow investor?

A follow investor is usually a non-lead investor that joins a round after another investor has set or validated the terms. The phrase can also be used loosely for an investor participating in a later round.

What should founders ask before taking follow-on capital?

Founders should ask whether the money funds a specific milestone, whether the terms will create future friction, whether insider participation sends the right signal, and whether the investor can help with the company's next stage.