Venture Capital Deal Sourcing: Process, Channels, and Screening Framework

A practical VC deal sourcing framework: how firms define a thesis, build channels, screen startups, track deal flow, and decide what deserves diligence.

Venture capital deal sourcing is the work of finding startup investment opportunities before they are obvious, crowded, or already committed to another investor. Good sourcing is not just "having a network." It is a repeatable system: define what the fund wants to back, build channels that surface those companies, screen quickly, track every interaction, and learn which sources produce investable opportunities.

For a VC analyst, associate, scout, or emerging manager, sourcing is where judgment starts. A sourced company is not a deal yet. It becomes useful only when the investor can explain why it fits the fund, why the timing matters, and what should happen next.

What venture capital deal sourcing means

In venture capital, deal sourcing is the front end of the investment process. It is how a firm identifies companies that may fit its fund strategy.

| Term | Meaning | Practical output |

|---|---|---|

| Deal sourcing | Finding and qualifying potential startup investments | Company leads, founder introductions, market maps |

| Deal origination | Another term for creating or finding new investment opportunities | Sourced opportunities entering the pipeline |

| Deal flow | The total stream of opportunities a firm sees | Pipeline volume and quality |

| Screening | A quick first-pass judgment before deeper work | Pass, track, meet, or diligence |

| Due diligence | Deeper analysis after a company looks promising | Market, team, product, traction, legal, and financial work |

| Investment committee | The formal decision forum for many firms | Invest, decline, or continue work |

Deal sourcing feeds deal flow, but the two are not identical. A fund can have high deal flow and poor sourcing if the opportunities are noisy, misaligned, or too late. Strong sourcing is narrower: it produces companies that match the fund's investment thesis and are worth a real investor conversation.

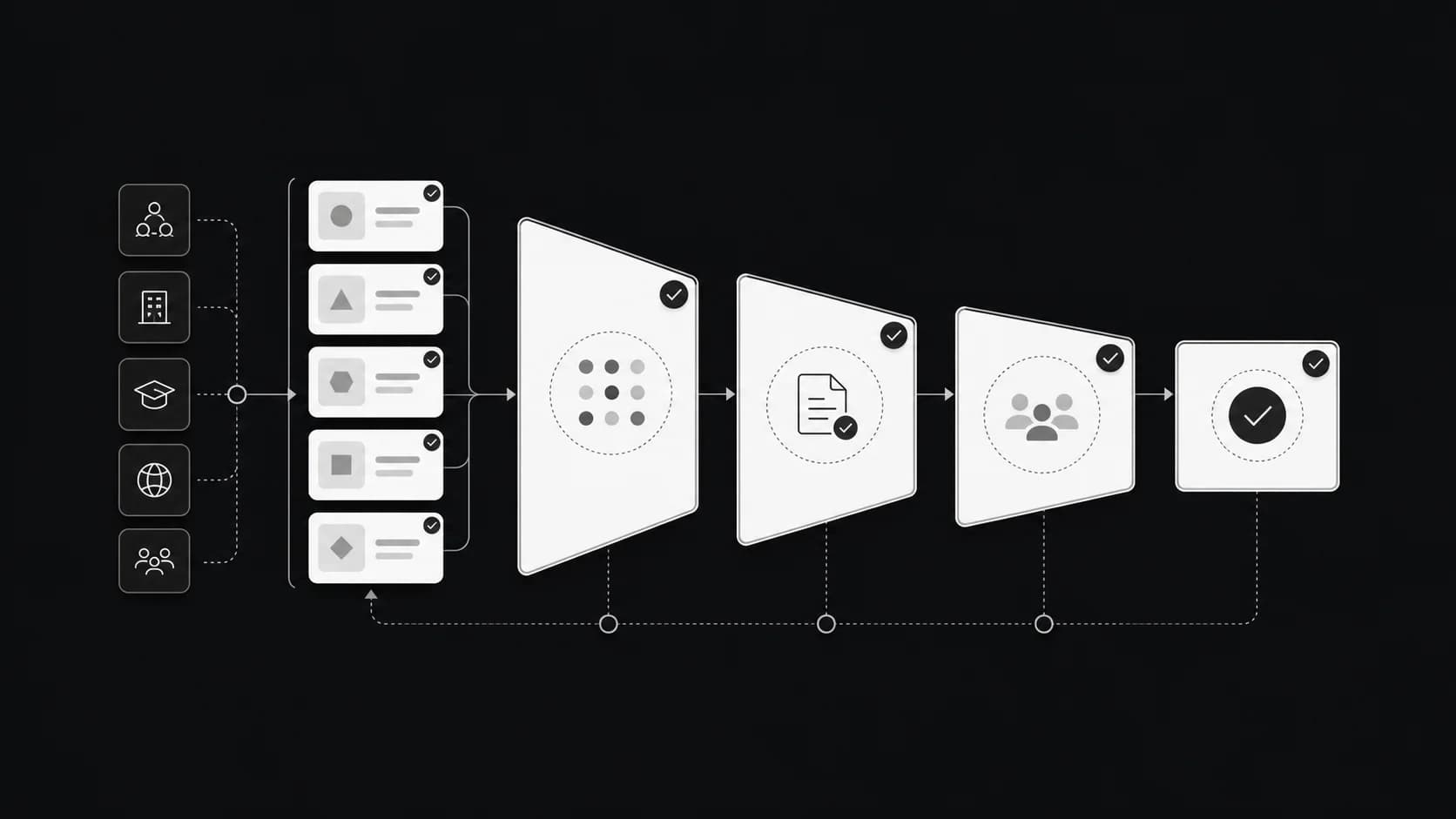

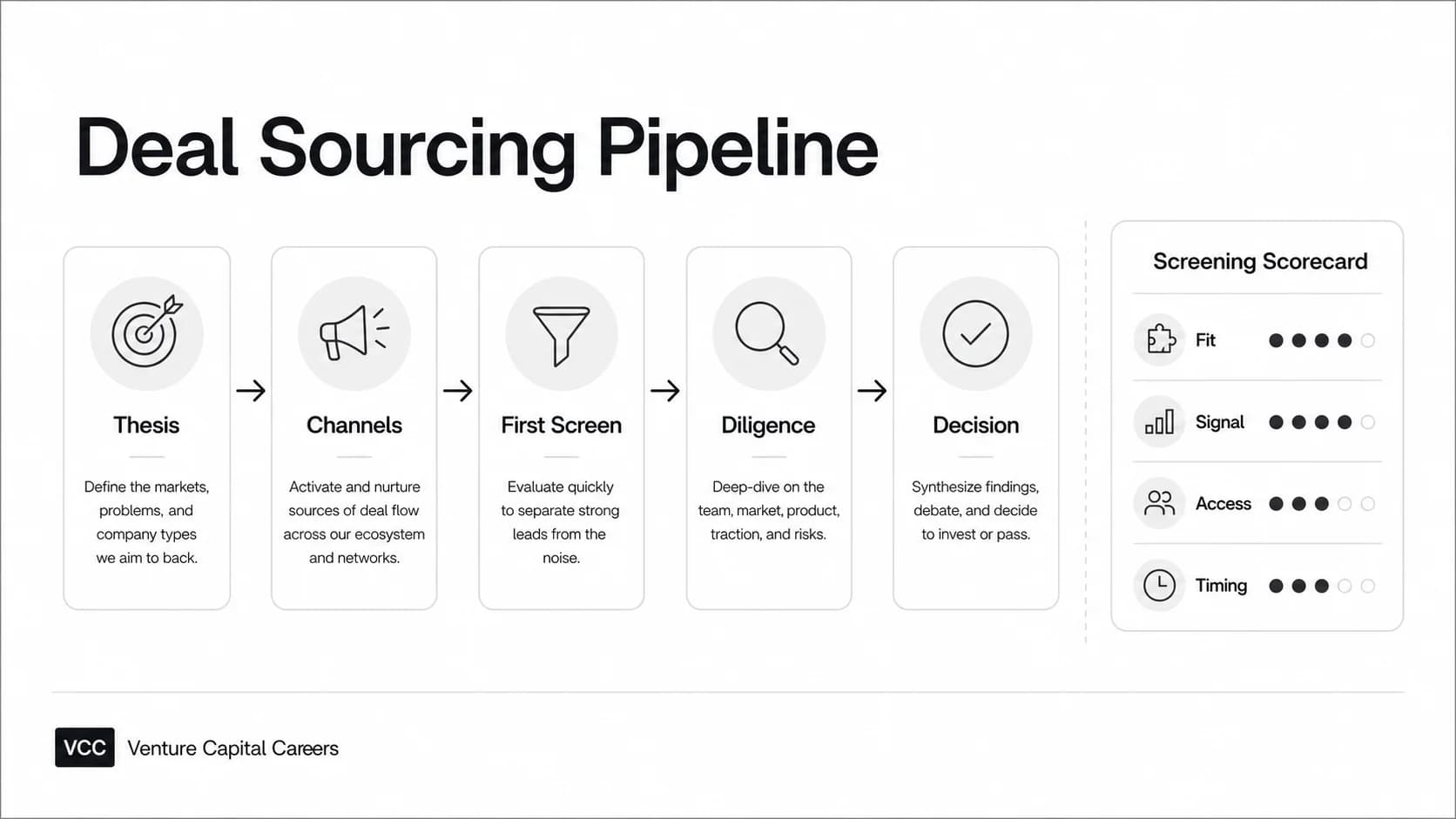

The VC deal sourcing process

A useful sourcing process has six steps.

| Step | What happens | Output |

|---|---|---|

| 1. Define the thesis | Translate fund strategy into sectors, stages, geographies, business models, and signals | Sourcing criteria |

| 2. Build channel coverage | Decide where relevant founders, operators, angels, scouts, and companies can be found | Channel map |

| 3. Capture every company | Log source, contact, stage, round, notes, and next action | Clean CRM or tracker |

| 4. Run the first screen | Decide whether the company fits enough to deserve time | Pass, track, meet, or diligence |

| 5. Hand off serious opportunities | Move strong companies into deeper research and partner review | Diligence memo or meeting notes |

| 6. Review source quality | Compare channels by quality, conversion, and missed deals | Better sourcing allocation |

The process starts with a thesis because sourcing without criteria becomes browsing. A seed fintech fund, a climate growth fund, and a B2B infrastructure fund should not run the same sourcing motion. They may use some of the same channels, but they should not define "interesting company" the same way.

Once the thesis is clear, the job is to build enough channel coverage that the firm sees relevant companies early. That usually means a blend of relationships, outbound research, content visibility, community presence, and data tools.

Deal sourcing channels that belong in a VC pipeline

No single channel is enough. The best channel depends on the fund's stage, reputation, geography, and sector depth.

| Channel | Best for | Watch-outs |

|---|---|---|

| Founder referrals | Warm access to credible founders in a known ecosystem | Can become too narrow if the network lacks diversity |

| Portfolio founders | High-trust introductions and market context | Requires real founder support, not transactional asks |

| Co-investors and angels | Early signals, round dynamics, and syndicate access | Competitive tension if the deal is already hot |

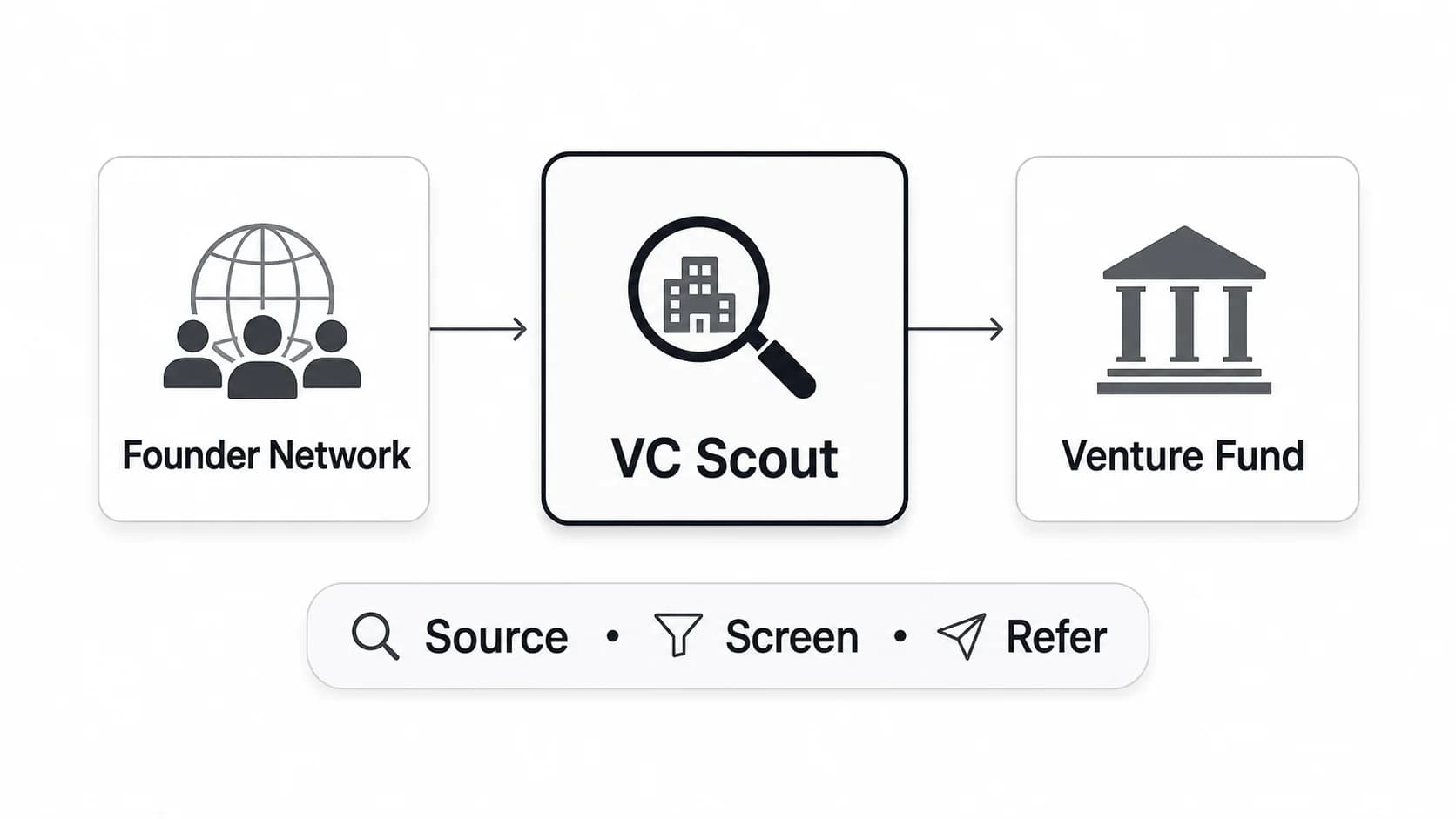

| Scouts and operators | Distributed coverage in communities the fund cannot reach alone | Needs clear criteria and feedback loops; use a written VC scout program mandate |

| Accelerators and demo days | Broad early-stage coverage | Many investors see the same companies at the same time |

| Universities and labs | Technical founders and frontier research | Commercial readiness can be uneven |

| Outbound market mapping | Thesis-led discovery before fundraising | Time intensive; cold access is harder |

| Content and community | Inbound from founders who trust the firm's point of view | Takes consistency and real expertise |

| Platforms and databases | Coverage, alerts, and company discovery | Data does not replace founder access or judgment |

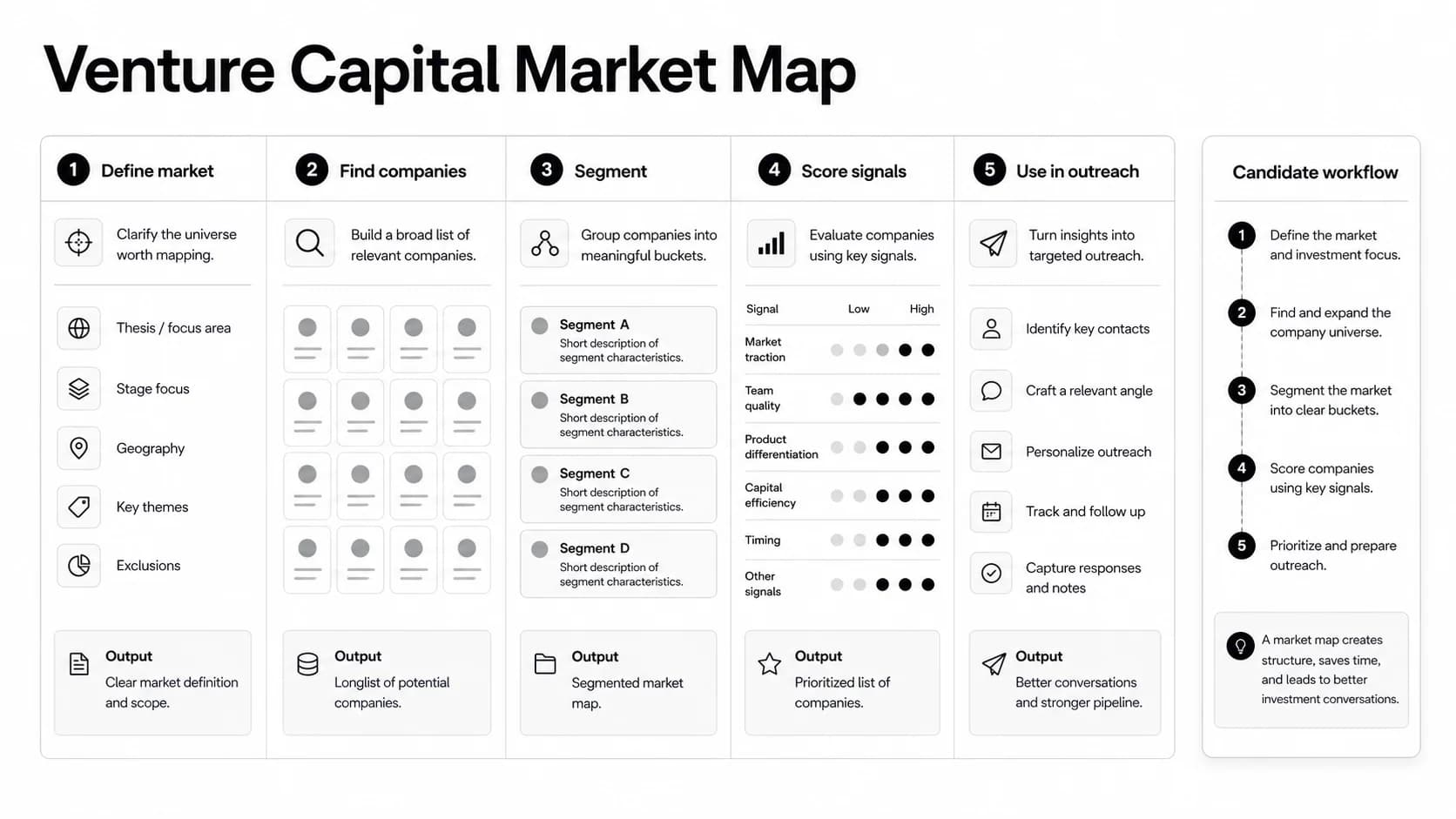

For candidates learning the market, the Venture Capital Careers companies directory is a useful research surface. You can map firms by sector, geography, and stage, then study how different investors describe their focus. That is the same muscle a junior investor uses when building a sourcing map.

How to screen a sourced startup before diligence

The first screen should be fast but not casual. Its job is to prevent two mistakes: ignoring a company that deserves attention, and spending diligence time on companies that clearly do not fit.

Use a simple scorecard.

| Screen | Question to answer | Advance when |

|---|---|---|

| Thesis fit | Does this company match the fund's stage, sector, geography, and business model focus? | The fit is clear enough to explain in one sentence |

| Market signal | Is there a market change, customer pain, regulatory shift, technical unlock, or buyer behavior that makes now plausible? | The company is riding a real tailwind, not a vague trend |

| Founder-market fit | Does the team have a reason to understand this problem better than most? | The founder has credible insight, experience, or access |

| Product and traction | Is there evidence that customers, users, or partners care? | Traction quality fits the company's stage |

| Access | Can the firm get a real conversation or trusted reference? | There is a path to founder engagement |

| Round dynamics | Is the round size, valuation expectation, and ownership target compatible with the fund? | The fund can plausibly participate |

| Timing | Is this a meet-now, track, or pass? | The next action is obvious |

For early-stage startups, the first screen should not pretend to be full venture capital due diligence. The question is not "is this company fully proven?" The question is "is there enough signal to justify scarce investor time?"

Metrics to track by sourcing channel

Volume matters, but source quality matters more. Track enough data to know which channels are producing useful opportunities.

| Metric | Why it matters |

|---|---|

| Qualified companies added | Shows whether the channel produces thesis-fit opportunities |

| First meetings booked | Measures access, not just discovery |

| Meetings to diligence | Shows whether the channel creates real conviction |

| Diligence to investment | Tracks ultimate quality, while allowing for small sample sizes |

| Pass reasons | Reveals whether a source is off-thesis, too late, too early, or low quality |

| Time to first decision | Keeps the pipeline from becoming a graveyard |

| Relationship freshness | Prevents warm networks from going cold |

| Missed deals | Forces honest review of companies the firm saw but did not pursue |

A weekly sourcing review should ask four questions:

- Which new companies fit our thesis?

- Which existing tracked companies need a follow-up?

- Which sources are improving or degrading?

- Which misses suggest our criteria or channels are wrong?

That review is where sourcing becomes an operating system instead of a contact spreadsheet.

Where tools help and where they do not

VC deal sourcing tools can help with coverage, reminders, market maps, company enrichment, alerts, and CRM hygiene. They are useful when a firm needs to organize many weak signals across people, sectors, and time.

Tools are less useful when the underlying process is unclear. A database cannot tell a fund what it should believe about a market. A CRM cannot create founder trust. An alert cannot replace a thoughtful intro from someone a founder respects.

Use tools for:

- Capturing every company and source.

- Tracking follow-ups and stale relationships.

- Tagging companies by thesis, stage, sector, and geography.

- Recording pass reasons.

- Comparing channels by conversion.

- Finding companies adjacent to a market map.

Do not use tools to avoid writing down the fund's actual criteria. If the team cannot explain what it wants to see, software will only make the noise easier to store.

How VC candidates can show deal sourcing ability

Sourcing is one of the clearest ways for candidates to show investor judgment before they have a long investing track record.

Instead of saying "I am interested in startups," build a small sourcing packet:

| Candidate exercise | What it proves |

|---|---|

| Market map of 20-30 companies | You can define a space and find relevant startups |

| Short thesis paragraph | You understand why the market matters now |

| Five strongest company notes | You can prioritize, not just list |

| First-screen scorecard | You can separate signal from noise |

| Suggested intro path | You understand access and relationship dynamics |

| Risks and pass reasons | You can be skeptical without being dismissive |

This is useful for analyst, associate, scout, and platform roles. It also connects to broader VC skills such as market research, founder communication, memo writing, and judgment under uncertainty.

If you are researching where those skills fit, start with current VC firms and roles on Venture Capital Careers. Then use the companies directory to understand which firms match your sector interests before you write outreach or prepare interview examples.

Common mistakes in VC deal sourcing

Starting with tools before thesis

Software can expand coverage, but it cannot decide what the fund should care about. Start with the thesis, then choose channels and tools.

Measuring volume without quality

A large pipeline can hide poor sourcing. If few sourced companies become first meetings or diligence candidates, the issue is not effort. It is source fit.

Treating every warm intro as valuable

Warm introductions help, but a warm intro to an off-thesis company is still off-thesis. Track source quality, not just source warmth.

Failing to record pass reasons

Pass reasons are training data for the investment team. Without them, the firm cannot tell whether a source is wrong, the thesis is too narrow, or the team is missing a pattern.

Confusing a hot round with a fund-fit company

Competitive rounds can create urgency, but urgency is not conviction. A company should still fit the fund's stage, ownership target, and view of the market.

FAQ

What is the difference between deal sourcing and deal flow?

Deal sourcing is the work of finding and qualifying startup opportunities. Deal flow is the total stream of opportunities a firm sees. Strong sourcing improves the quality of deal flow.

Is cold outbound useful in venture capital?

Yes, when it is thesis-led and specific. Cold outreach works best when the investor can explain why the company is relevant to the fund and why a conversation is useful now.

What makes a deal proprietary?

A proprietary deal is usually one where the investor has differentiated access, timing, or insight. It does not always mean nobody else knows the company. It means the investor's path to the company is meaningfully better than the market's.

What should an analyst include in a sourcing note?

Include the company, source, thesis fit, market signal, founder-market fit, traction evidence, round context, reason to meet or pass, and recommended next action.

When does sourcing become due diligence?

Sourcing becomes diligence when the firm decides the company deserves deeper work: customer calls, market sizing, product review, financial analysis, reference checks, and partner debate. For more on the decision side, see how venture capitalists make investment decisions.