Venture Capital Scout Job Description: Role, Pay, and Template

A practical venture capital scout job description with responsibilities, compensation models, hiring criteria, candidate questions, and fair-program rules.

A venture capital scout is an external or internal deal sourcer who helps a VC fund find startups that fit its investment thesis. The scout usually works through a particular network, sector or geography, screens opportunities and introduces the strongest fits to the fund. The fund—not the scout—makes the investment decision.

The title is easy to misunderstand. It does not refer to youth Venturer Scouts, a recruitment “talent scout,” or a company with Scout in its name. It also does not describe one standard employment arrangement. Some scouts are salaried members of an investment team. Many are part-time operators, founders, students or domain experts who receive a cash bounty, deal-specific carry or no guaranteed cash compensation.

That distinction belongs at the top of every venture capital scout job description. A credible posting should tell candidates what authority they have, how much time the work requires, what happens after an introduction and exactly how compensation is calculated.

What a venture capital scout does

The core job is not “find exciting startups.” It is to find companies that match a fund’s actual mandate and give the investment team enough context to decide whether to engage.

Typical responsibilities include:

- Build relationships with founders, operators, angels, accelerators and specialist communities.

- Source companies within defined stage, sector, geography, traction and check-size criteria.

- Run an initial screen for thesis fit, founder quality, market, product, traction and financing needs.

- Explain the fund’s process honestly and avoid implying that an introduction guarantees funding.

- Submit qualified opportunities through the fund’s agreed channel.

- Write a short referral note or investment memo when the program requires one.

- Support reference calls, market research or light diligence when explicitly in scope.

- Track attribution, status and feedback for every submitted company.

- Disclose conflicts, personal investments and relationships with founders.

The boundary matters. Scouts should not promise a term sheet, present themselves as a partner, charge founders without clear legal and fund approval, or perform open-ended diligence that the agreement never contemplated.

Choose the scout model before writing the job description

“VC scout” can describe three materially different arrangements. Pick one before you advertise the role.

| Model | Employment and time | Authority | Typical economics | Best when |

|---|---|---|---|---|

| Internal sourcing employee | Full-time or substantial part-time employee | Sources and screens; may join diligence and investment meetings | Salary and benefits, sometimes bonus or fund carry | The fund needs consistent coverage and can manage a team member |

| External scout | Independent, usually part-time and network-led | Refers or recommends; fund retains the investment decision | Cash bounty, deal-specific carry, retainer, or a combination | The fund wants access to a community, sector or geography it does not reach well |

| Scout with delegated capital | Independent but operating under a written allocation and limits | May recommend or execute small investments subject to fund rules or veto | Share of deal or program economics; terms vary | The fund trusts experienced operators or angels to extend its earliest-stage reach |

Do not combine the obligations of an employee with the economics of a casual referral program. If the fund expects fixed hours, weekly pipeline meetings, substantial diligence, CRM administration and ongoing portfolio work, it should evaluate whether the role is really an analyst, associate or employee-level sourcing position.

External scouts need a narrower brief. Their advantage is access: founders and communities the core team would not otherwise see. A long generic responsibility list can erase that advantage and turn the program into unpaid junior investment work.

Venture capital scout job description template

Replace the bracketed text before publishing. Delete any responsibility or benefit that the fund will not actually provide.

About the fund

[Fund name] is a [pre-seed / seed / Series A / multi-stage] venture capital firm investing in [sectors] across [geographies]. We typically invest [check-size range] in companies with [traction or company-profile requirements]. Our current portfolio and investment approach are available at [stable firm URL].

Engagement model

We are appointing a [part-time external scout / employee scout / scout with delegated capital] to expand our reach within [specific community, sector or geography]. The role reports to [partner or investment-team role] and is expected to require approximately [hours or referrals per month]. This is a [fixed-term / ongoing] [employment / contractor / program-participant] arrangement.

Investment mandate

The scout should introduce companies that meet these criteria:

- Stage: [stage]

- Sector: [included sectors]

- Geography: [geography]

- Typical check: [range]

- Traction: [requirements, if any]

- Exclusions: [out-of-scope sectors, structures or stages]

- Round role: [lead / follow / either]

Responsibilities

- Build trusted relationships with founders and ecosystem participants in [target network].

- Identify and initially screen companies against the mandate above.

- Submit [referral note / structured form / short memo] covering the team, problem, product, market, traction, round and why the opportunity fits.

- Set accurate expectations with founders about the fund’s process and response time.

- Participate in [introductory calls / light diligence / reference calls] when requested and agreed.

- Maintain an attribution record for submitted companies.

- Disclose personal investments, advisory roles and other conflicts before referral.

- Protect confidential founder and fund information.

Evidence and qualifications

- Demonstrated access to [founder community, sector or geography].

- Clear point of view on [investment theme], supported by companies, market work or operating experience.

- Ability to explain why a company fits the mandate in concise written form.

- Sound judgment with confidential information and founder relationships.

- Experience as a [founder / operator / angel / investor / researcher / community builder] is helpful but not automatically required.

- Prior venture capital employment is [required / preferred / not required].

Compensation and attribution

Compensation is [salary / retainer / cash bounty / deal-specific carry / pooled carry / combination]. For carry-based compensation, the written agreement will define:

- the percentage and its denominator;

- which investment or pool it applies to;

- when a referral earns attribution;

- vesting, forfeiture and departure treatment;

- whether fund-level netting, expenses or follow-on investments affect payment;

- reporting and payment timing.

We will acknowledge or reject attribution within [number] business days and provide [monthly / quarterly] status updates on active referrals.

Application process

Send [resume or LinkedIn profile], a short explanation of your network edge and [one or two] example companies that fit the mandate. Do not share confidential information or contact founders on our behalf before acceptance. Shortlisted candidates will complete [a sourcing exercise / short memo / partner conversation].

Funds hiring a true employee or paid contractor can post the role on Venture Capital Careers. The employer page explains the VC-specific hiring audience and posting options.

Responsibilities and success measures

Measure a scout on qualified judgment, not a pile of founder names. Raw referral volume encourages weak introductions and damages trust on both sides.

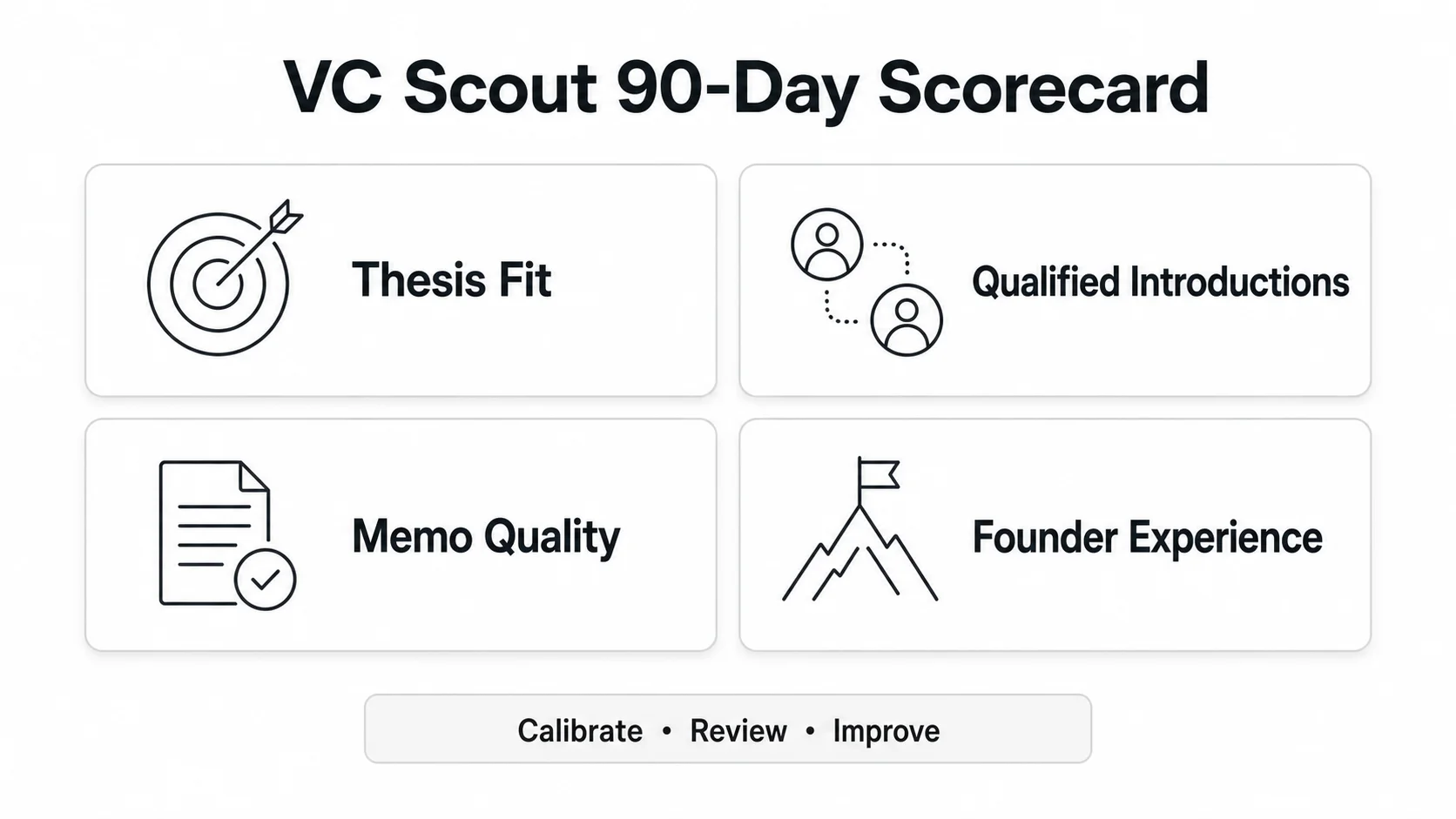

Use a scorecard with four leading indicators:

1. Thesis fit: How often do submissions match the stated stage, sector, geography, check size and exclusions? 2. Qualified introductions: Does the scout have a real relationship with the founder, and has the founder agreed to the introduction? 3. Memo quality: Can the scout explain the opportunity, risk and reason to engage without copying a pitch deck? 4. Founder experience: Does the scout communicate the fund’s authority, timing and decision honestly?

Track outcomes separately: partner meetings, diligence, investments and eventual returns. Those results matter, but small samples and long venture timelines make them poor short-term quotas. A scout can make a high-quality introduction that the fund passes on for portfolio construction or timing reasons. Conversely, one lucky investment does not excuse a pattern of irrelevant referrals.

For the first 90 days, agree on a calibration period: review a small set of example companies, compare the scout’s screening logic with the partner’s feedback and tighten the mandate. The fund should own the feedback loop. Without it, scouts cannot learn what “fit” means beyond a public thesis page.

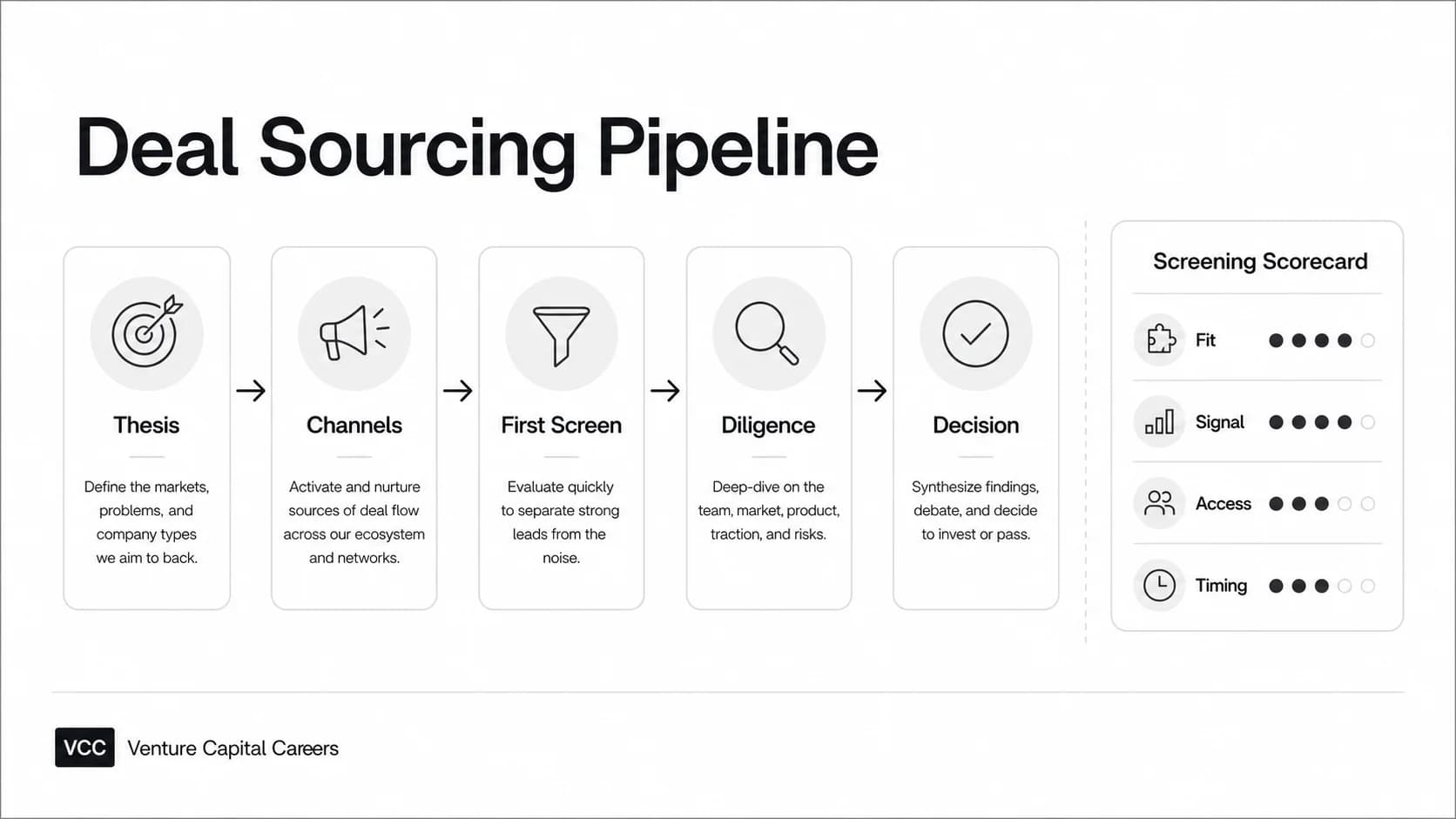

The sourcing workflow should connect to a documented venture capital deal-sourcing process, including consistent screening and handoff rules.

Skills and evidence to look for

The best scout is not necessarily the candidate with the longest finance resume. The hiring question is whether this person sees relevant companies early, earns founder trust and can exercise judgment before sending a deal to the fund.

| Candidate background | Useful evidence | What to test |

|---|---|---|

| Founder or operator | Trusted peer network, product/market judgment, real sector access | Can they separate friendship from investment quality and disclose conflicts? |

| Angel investor | Sourcing record, written theses, references from founders and co-investors | Do they understand the fund’s mandate rather than simply forwarding their own deal flow? |

| Domain expert | Deep technical or market knowledge, community credibility | Can they translate expertise into an investable view? |

| Student or community builder | Campus, accelerator or local-ecosystem access; consistent company tracking | Do they have supervision, realistic scope and a safe way to handle confidential information? |

| Aspiring investor | Market maps, memos, founder references, evidence of follow-through | Are they offering a genuine network edge or only seeking a credential? |

Ask candidates to submit a small “shadow pipeline”: three to five companies they would prioritize, why each fits and what they would need to learn next. The goal is not free diligence. It is to observe selection, reasoning and communication.

Strong evidence includes warm founder references, a focused market map, clear pass reasons, a history of making useful introductions and an ability to name risks. Weak evidence includes a large LinkedIn network with no relationship depth, generic enthusiasm for startups or a list of famous companies already known to every fund.

How VC scouts get paid

There is no reliable universal “VC scout salary.” The first question is whether the role is employment, contracted work or a success-based program.

| Model | Cash timing | Upside | Main risk for the scout |

|---|---|---|---|

| Salary or hourly pay | Regular payroll or invoices | Possible bonus or carry | Role may actually be broader than sourcing |

| Retainer | Monthly or project-based | May include success economics | Scope can expand unless hours and deliverables are written |

| Cash bounty | When a qualifying event occurs, such as an investment | Clearer near-term value than carry | No payment if the fund passes, even after substantial work |

| Deal-specific carry | Usually only after a profitable exit and distribution | Participation in a sourced winner | Payment may take years or never occur |

| Pooled or fund carry | After the relevant pool or fund produces distributable profits | Broader alignment | Netting and fund performance can reduce or eliminate payment |

| Delegated capital | Depends on the program agreement | Economics can resemble a small managed allocation | Greater responsibility, conflicts and program constraints |

Founders' Next Move notes that many scout arrangements are success-based and may not pay cash until an exit years later. That makes workload and scope as important as the headline percentage.

Read the denominator before the percentage

Suppose a fund invests $100,000, later receives $500,000 and, under a simplified example, earns 20% carry on the $400,000 profit. The fund’s carry would be $80,000 before any relevant expenses, netting or agreement terms. If a scout receives 20% of the fund’s carry on that deal, the illustrative scout payment is $16,000—not 20% of the $500,000 proceeds and not 20% of the investment.

That example resembles the language on Allied Venture Partners' live scout page, which currently describes a program-specific 20% share of Allied’s carry on the first investment it makes in a sourced company. It is an example, not a market standard.

Every carry agreement should state the denominator, attribution trigger, eligible investments, follow-ons, netting, vesting, reporting and payment timing. “Generous carry” is not compensation clarity.

A fair scout program needs six written rules

The fund gets access to a scout’s relationships and judgment. The scout risks time, reputation and opportunity cost. Put the exchange in writing.

1. Mandate: State stage, sector, geography, check size, traction, exclusions and whether the fund leads or follows. 2. Scope: Define whether the scout only introduces, writes a referral note, supports diligence or helps the portfolio. Put a time expectation beside the work. 3. Attribution: Explain what happens when two people refer the same company, the fund already knows the founder or the investment happens months later. 4. Feedback: Set a response time and a cadence for explaining passes. A scout program without feedback is not an apprenticeship. 5. Economics: State cash, carry, denominator, vesting, netting, reporting and payout conditions in plain language. 6. Conflicts and conduct: Cover confidentiality, personal investments, advisory relationships, founder fees, use of the fund’s name and who may speak for the firm.

Red flags include unlimited sourcing expectations, no written attribution process, “carry” with no denominator, pressure to imply decision authority, requests to charge founders without approved terms, and promises that the program will automatically convert into a full-time investment role.

The sharpest test is simple: could a reasonable candidate estimate the time at risk, understand what success means and explain how a successful deal would pay them? If not, the program is not ready to recruit.

Is venture scouting a path into VC?

It can be an apprenticeship, but it is not a default promotion track. A scout role is most useful when it produces evidence that another fund can evaluate: companies sourced, written theses, concise memos, partner feedback, founder references and an honest record of passes as well as investments.

Candidates should compare the program with other entry routes. A structured analyst or fellowship role may offer more training and closer exposure to diligence. An operating role can build deeper sector credibility and founder relationships. The right choice depends on whether the scout program provides real access, feedback and documented economics—not the title alone.

Use the venture capital career path to compare scout, analyst, associate and operator entry points. If you are applying for formal roles, build a venture capital resume around investment evidence rather than treating “VC Scout” as self-explanatory. You can also browse the VC job board and research funds in the companies directory.

Questions to ask before accepting a scout role

1. Is this employment, contracting or participation in a scout program? 2. What stage, sector, geography, check size and exclusions define a fit? 3. How many hours or submissions do you expect each month? 4. Do I introduce only, or do you expect memos, diligence and portfolio work? 5. Who owns the investment decision, and how should I describe my authority to founders? 6. What triggers attribution, and how are duplicate or pre-existing relationships handled? 7. Is compensation cash, retainer, carry or a combination? 8. If carry is offered, what percentage of what pool or profit, and what can reduce it? 9. How often will I receive feedback and status updates? 10. Is there a documented path to more responsibility, or should I treat this as a standalone part-time role?

Do not quit a paid role based on a vague promise of carry. Model the expected time, the fund’s actual investment pace, the probability that it invests in your referrals and the years a payout could take.

FAQ

Do venture scouts get paid?

Some do, but payment structures vary. An employee scout may receive salary and benefits. An external scout may receive a retainer, cash bounty, deal-specific carry, pooled carry or no guaranteed cash. The written agreement matters more than the title.

Is a VC scout an employee?

Not necessarily. Many scouts operate outside the fund as part-time program participants or contractors. Employment status should be explicit and consistent with the actual hours, control and responsibilities.

What qualifications does a venture capital scout need?

The strongest qualification is a relevant network edge combined with investment judgment and founder trust. Finance experience can help, but a focused operator, founder, angel, domain expert or community builder may be more valuable than a generalist with a conventional resume.

How many hours does a VC scout work?

There is no standard. External scouting may fit around an existing role, while an internal sourcing job can be full-time. The posting should state a realistic monthly time or activity expectation.

Is a VC scout the same as a VC analyst?

Usually not. Analysts are typically employees who support broader sourcing, research, diligence, memos and fund operations. External scouts usually have a narrower sourcing mandate and less decision authority.

Can a venture scout promise funding?

No. A scout can make an introduction or recommendation within the authority granted by the fund. The fund controls diligence and the final investment decision unless a written delegated-capital program explicitly says otherwise.