What is a SAFE in Venture Capital?

Learn what a SAFE is in venture capital, how SAFE notes convert, key terms such as valuation caps and discounts, and when startups should use one.

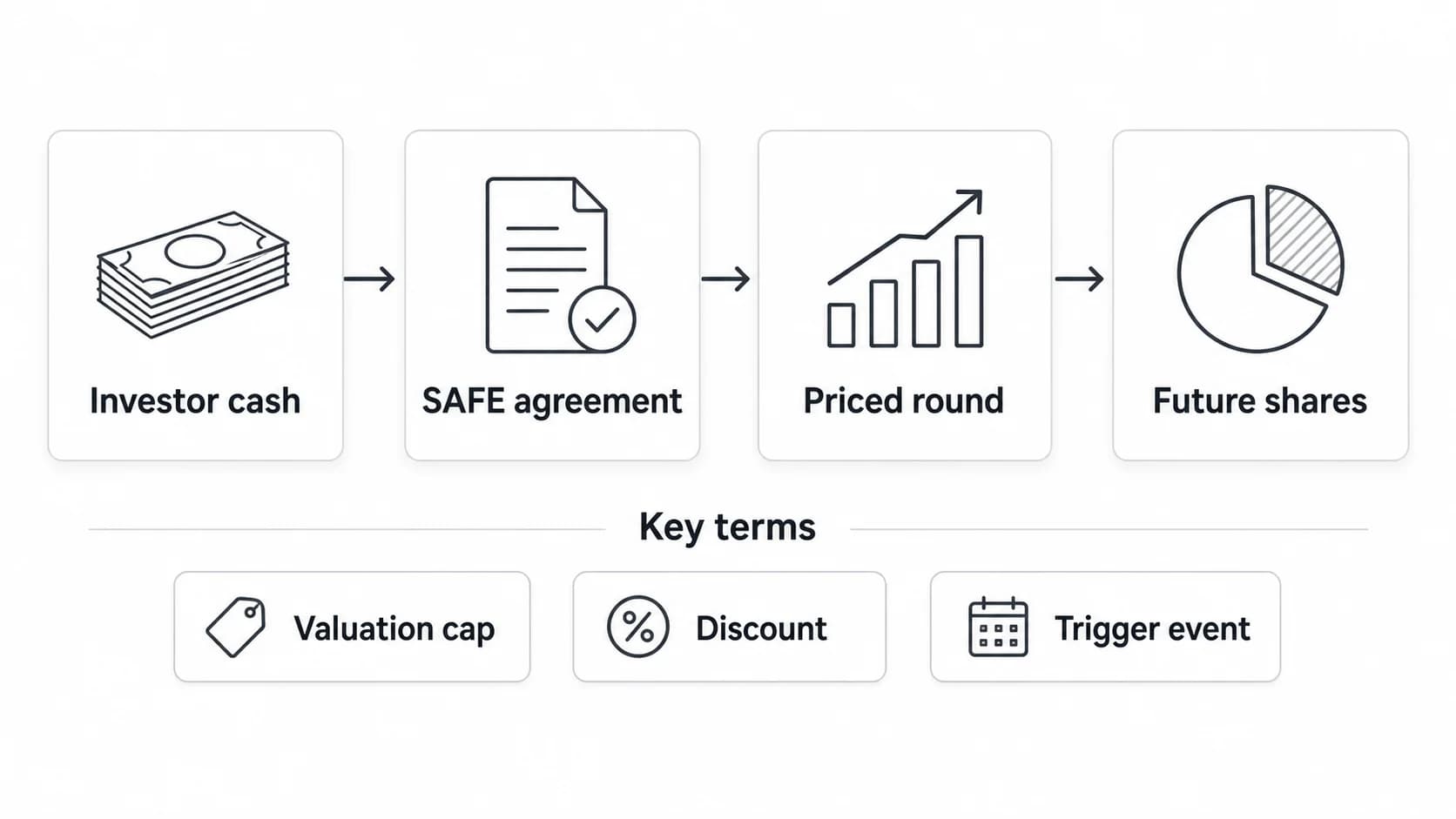

A SAFE, or Simple Agreement for Future Equity, is an early-stage startup financing agreement that gives an investor the right to receive equity later if a specified event happens. In venture capital, that event is usually a future priced equity round, such as a seed or Series A financing.

A SAFE is not common stock, and it is not a traditional loan. The investor sends money now. The company promises future equity treatment under the terms of the SAFE. The actual share price, share class, and ownership mechanics are settled later when the SAFE converts.

That simplicity is why SAFEs are common in seed financing. It is also why founders and investors need to understand the tradeoff: a SAFE can move quickly, but it still changes the company's future ownership.

What is a SAFE?

A SAFE is a contract between a startup and an investor. The investor provides capital, and the startup agrees that the investment will convert into stock if a future trigger event occurs.

Y Combinator introduced the SAFE in 2013 as a simpler alternative to convertible notes. YC's current SAFE financing documents are post-money SAFE forms for U.S. companies, with separate versions for valuation-cap, discount, and uncapped MFN structures.

The important distinction is timing. A priced equity round sets the company's valuation and sells shares immediately. A SAFE delays that pricing decision. The investor does not receive stock on the signing date; the investor receives a contractual right to future equity if the SAFE converts.

For a founder, that can make a small seed round faster to close. For an investor, it can create exposure to a startup before the next priced financing. For both sides, the economics depend on the exact SAFE terms.

How a SAFE works

A typical SAFE follows this sequence:

- The startup and investor agree on the investment amount and SAFE terms.

- The investor wires the purchase amount to the company.

- The SAFE sits on the company's cap table as a convertible security, not as issued stock.

- A trigger event occurs, most often a priced equity financing.

- The SAFE converts into shares based on the SAFE's conversion terms.

The most common conversion event is an equity financing where the company sells preferred stock to new investors. A SAFE may also address liquidity events, such as an acquisition or IPO, and dissolution events, such as the company winding down.

Until one of those events happens, the SAFE holder usually does not have the same rights as a stockholder. That is one reason the SEC's Investor.gov bulletin warns crowdfunding investors that SAFE holders are not receiving a current equity stake and that conversion depends on future triggers actually occurring.

SAFE ownership example

The cleanest way to understand a modern post-money SAFE is to start with ownership.

| SAFE term | Example |

|---|---|

| Investment amount | $500,000 |

| Post-money valuation cap | $10,000,000 |

| Implied ownership before the next priced round | 5.0% |

The simple calculation is:

| Formula | Result |

|---|---|

| $500,000 / $10,000,000 | 5.0% |

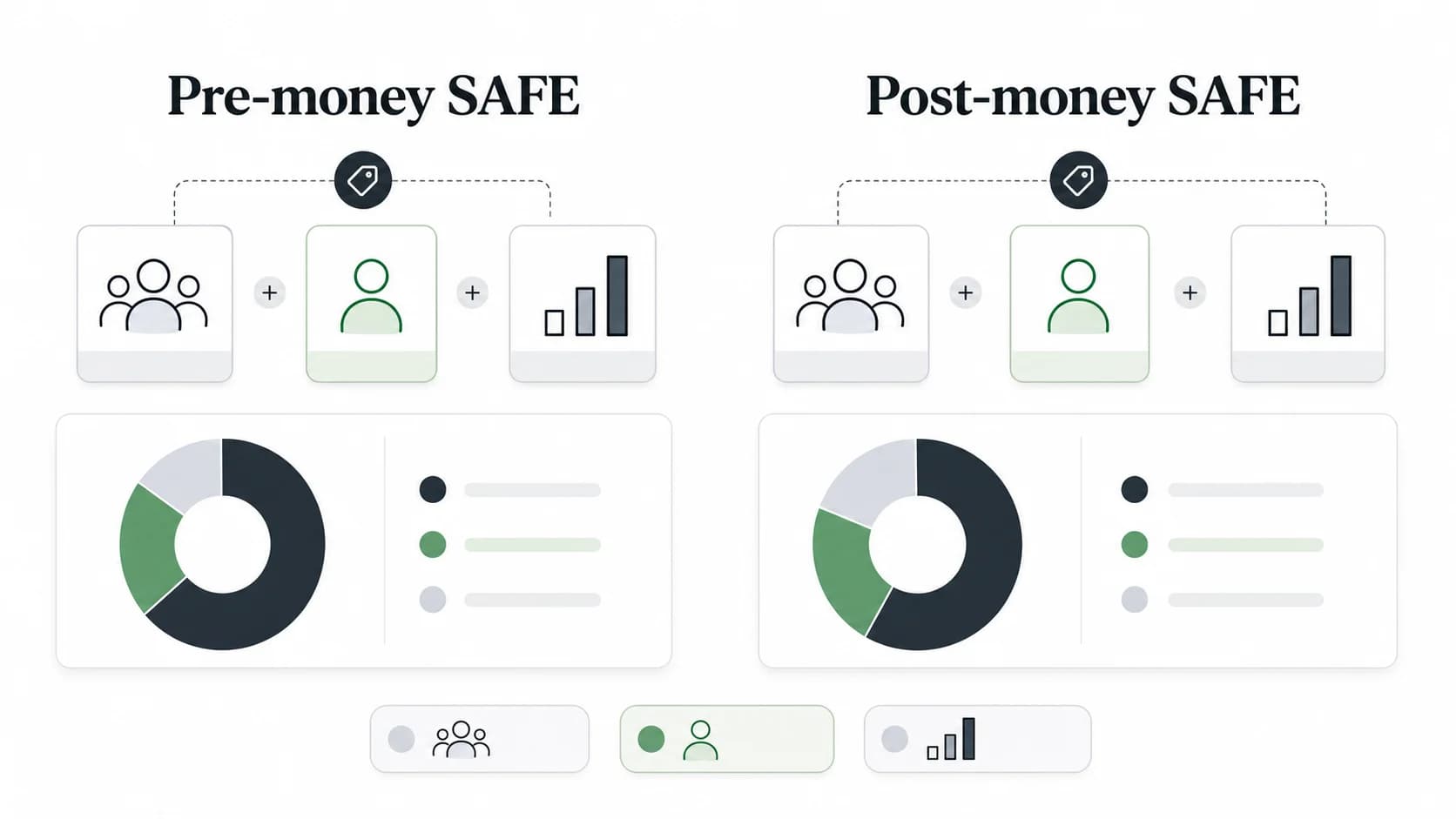

That 5.0% is not the investor's final post-Series A ownership. In YC's post-money SAFE user guide, the post-money cap is "post" all SAFE money but not "post" the later equity financing money. In plain English: the SAFE round can be modeled as its own financing, then everyone is diluted by the next priced round.

For founders, this makes planning easier than older pre-money SAFE structures. If you raise $1 million on a $10 million post-money cap, you have sold roughly 10% before the next priced round. If you raise $2 million on the same cap, you have sold roughly 20%. The danger is also obvious: a pile of small SAFE checks can become a large ownership sale.

Key SAFE terms

SAFE forms can look short compared with priced equity documents, but a few terms drive most of the economics.

| Term | What it means | Why it matters |

|---|---|---|

| Purchase amount | The cash the investor puts in | Sets the base amount that converts or is considered in liquidity/dissolution treatment |

| Valuation cap | The maximum valuation used to calculate the investor's conversion price | Lower cap usually means more shares for the SAFE investor |

| Discount | A percentage discount to the price paid by new investors in the priced round | Rewards early risk if the priced round happens at a higher valuation |

| MFN | Most favored nation treatment, usually allowing the investor to adopt better terms from later SAFEs | Protects an investor when the company later issues SAFEs on more favorable terms |

| Equity financing | A priced preferred stock round that triggers conversion | Determines when the investor becomes a stockholder |

| Liquidity event | Sale, merger, or IPO treatment | Determines what happens if the company exits before a priced round |

| Dissolution event | Company shutdown treatment | Determines priority and recovery if the company fails |

| Pro rata side letter | Separate agreement giving an investor the right to invest in a later round | Can matter for funds that need to maintain ownership |

The valuation cap is usually the first negotiation point. A high cap is better for founders because it sells less implied ownership. A low cap is better for investors because it can produce more shares if the company raises its next round at a higher valuation.

The discount is a different mechanism. Instead of setting a maximum valuation, it lets the SAFE investor convert at a lower price than the new money investors pay. Some SAFEs use a cap, some use a discount, and some use both or neither depending on the form.

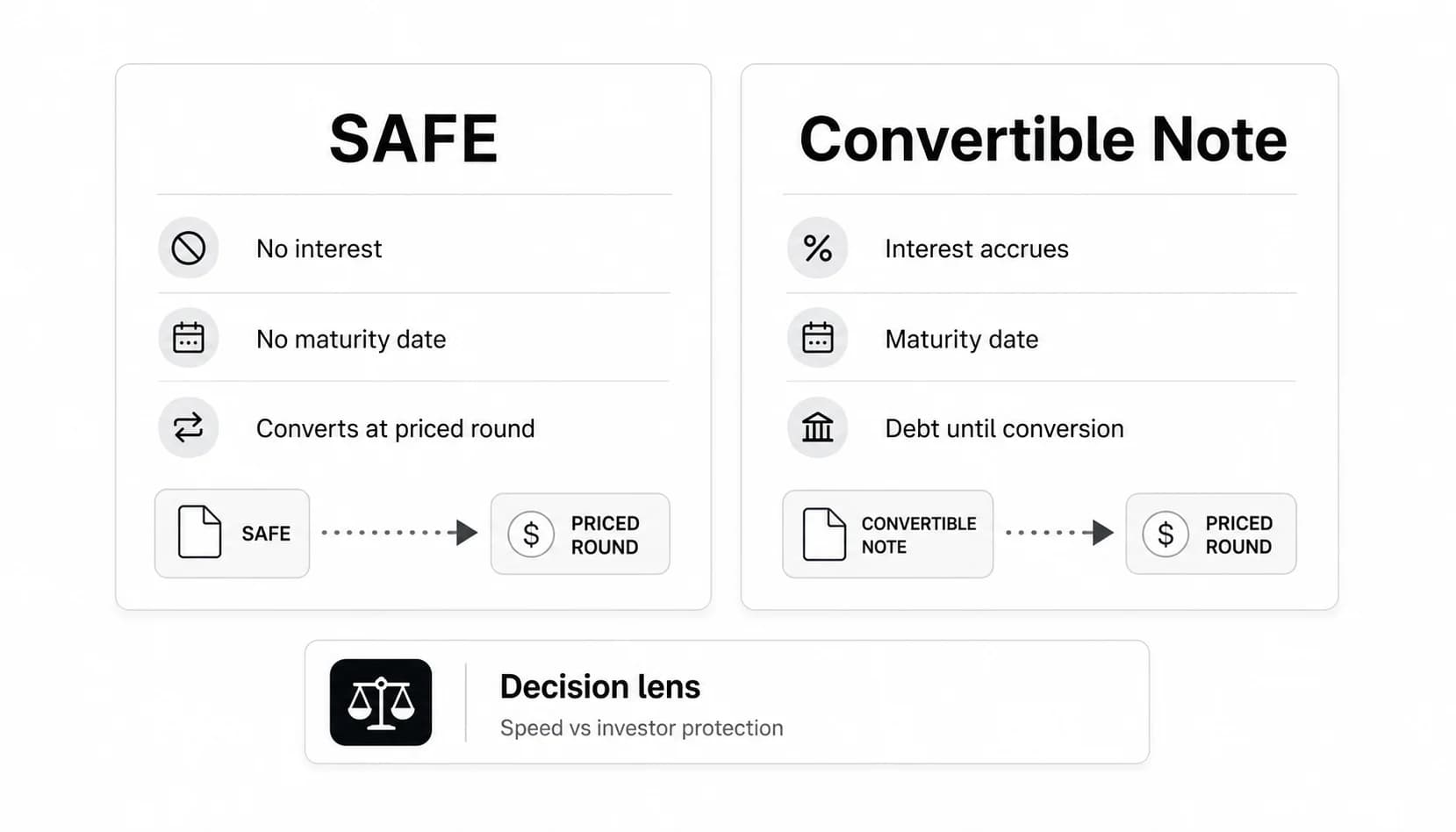

SAFE vs convertible note vs priced round

SAFEs, convertible notes, and priced equity rounds all fund startups, but they solve different problems.

| Instrument | Best fit | Key advantage | Main tradeoff |

|---|---|---|---|

| SAFE | Early seed financing before the company is ready for a priced round | Fast, standardized, no maturity date or interest | Investor does not receive current equity and rights can be limited |

| Convertible note | Bridge financing where debt-like features are acceptable | Can include maturity date, interest, and noteholder remedies | More complexity than a SAFE and can create maturity-date pressure |

| Priced equity round | Larger seed, Series A, or institutional round | Clear valuation, share issuance, governance rights, and investor protections | Slower, more expensive, and more heavily negotiated |

The simplest distinction is that a convertible note is debt that may convert into equity, while a SAFE is intended to be a future-equity agreement without a maturity date or interest rate. For a deeper comparison, see Venture Capital Careers' guide to SAFE vs convertible note.

A priced round is cleaner once the company is ready to set valuation and negotiate a full preferred-stock financing. It also usually gives investors more rights: board rights, information rights, protective provisions, pro rata rights, and a defined class of preferred stock. That extra structure can be useful, but it costs time and legal budget.

Advantages of SAFEs

The main benefit of a SAFE is speed. A startup can close one investor at a time instead of coordinating a single close across every participant in the round. That matters when a founder is still validating the company, needs runway, and is not ready for a full priced financing.

SAFEs also reduce some of the friction that comes with convertible notes. There is no maturity date to extend and no interest calculation to handle at conversion. For small checks, friends-and-family rounds, angel rounds, or accelerator financings, that can be the difference between a workable process and a legal project that consumes too much time.

The post-money SAFE adds another practical benefit: ownership math. A founder can estimate how much of the company has been sold by dividing the SAFE amount by the post-money valuation cap. That does not remove dilution, but it makes dilution easier to see before signing the next SAFE.

Risks and tradeoffs

A SAFE is simple, but it is not risk-free.

For founders, the biggest risk is hidden dilution. A $100,000 SAFE might feel small in isolation. Ten similar checks across different caps can become a meaningful ownership sale before the company reaches a priced round. Founders should keep an updated cap table that models every outstanding SAFE, not just issued shares.

For investors, the biggest risk is that the SAFE is not current equity. If the company never raises a qualifying priced round and never has a liquidity event, conversion may not occur. A SAFE may also provide fewer governance rights than preferred stock.

There is also a priority issue. If a company shuts down or sells before conversion, the SAFE's treatment depends on the document. Investors should understand how the SAFE ranks relative to debt, preferred stock, common stock, and other SAFEs.

Finally, SAFEs are legal instruments. Tax treatment, securities rules, jurisdiction, investor accreditation, crowdfunding disclosures, and company-specific drafting can matter. A short form does not replace legal review.

When a SAFE makes sense

Use this as a practical screen, not legal advice.

| Situation | SAFE fit? | Why |

|---|---|---|

| Two angels are investing before a priced seed round is practical | Strong fit | Speed and low transaction complexity matter |

| A startup wants to raise small checks over time | Strong fit | SAFEs support rolling closes and high-resolution fundraising |

| A company needs bridge capital before a priced round already in process | Possible fit | Convertible note or priced bridge may also work, depending on investor expectations |

| A lead investor wants board rights and detailed protective provisions | Weak fit | A priced round may fit better |

| The company is unlikely to raise future equity capital | Weak fit | The SAFE may never convert |

| The investor needs a maturity date or interest | Weak fit | A convertible note is more natural |

The decision point is not "SAFE good, priced round bad." The decision is whether speed and simplicity are more important than immediate pricing, stockholder rights, and full financing documents.

Checklist before signing a SAFE

Founders should ask:

- How much ownership are we selling if every SAFE converts?

- Are all SAFEs on the same valuation cap, or are later investors getting different economics?

- Do we understand the difference between a pre-money vs post-money SAFE?

- Will pro rata rights create additional dilution in the next round?

- Does the SAFE help us reach the milestone needed for seed funding or Series A funding?

- Have counsel and the board reviewed the terms?

Investors should ask:

- What ownership does the purchase amount imply at the valuation cap?

- What happens if the next round price is below the cap?

- What rights do we have before conversion?

- What happens in a sale, IPO, or dissolution before conversion?

- Do we need pro rata rights to support our strategy?

- Are the company's existing SAFEs, notes, option pool, and priced round plans reflected in the model?

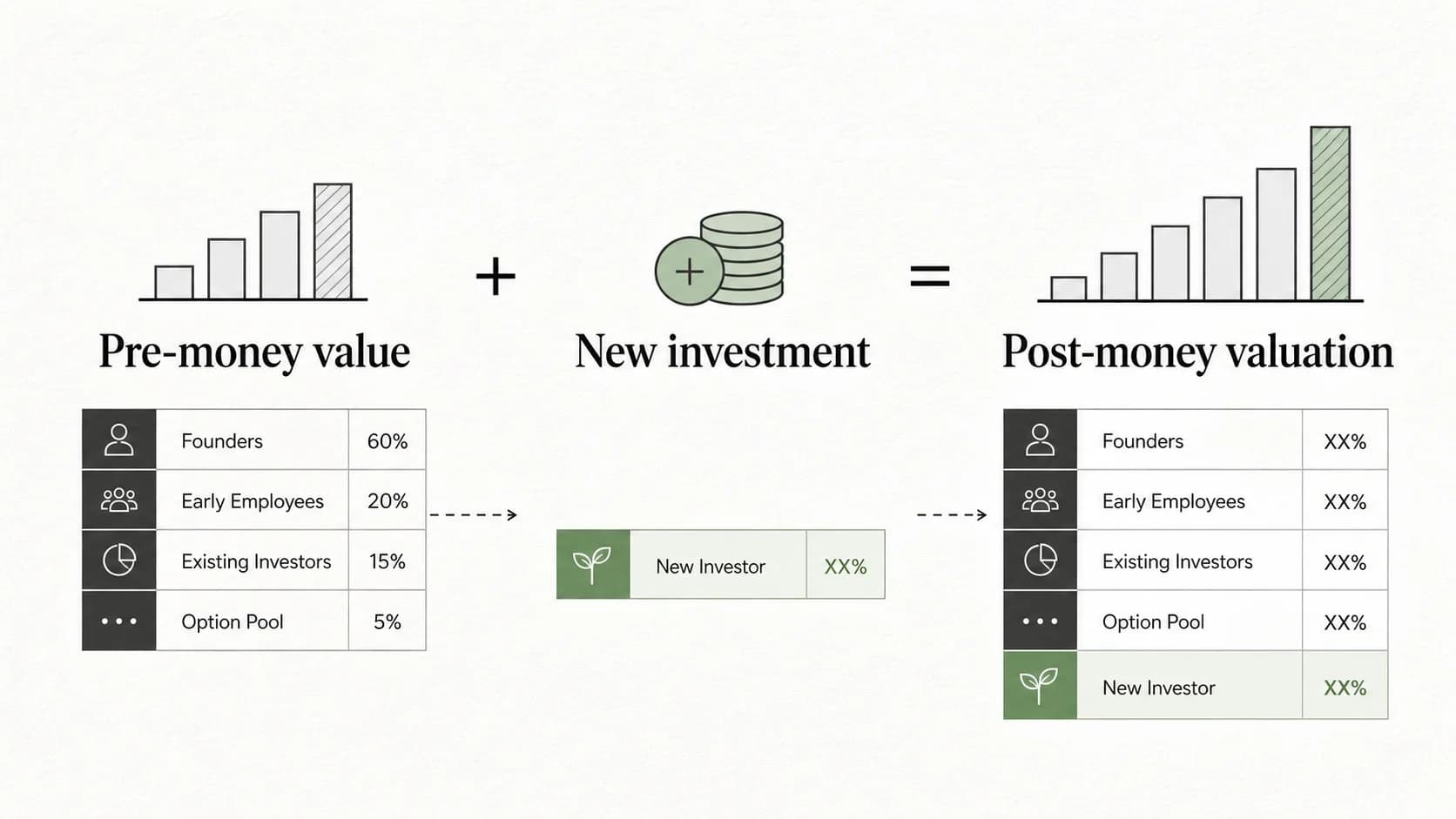

Both sides should understand the pre-money valuation and post-money valuation language being used. Misunderstanding that distinction is one of the easiest ways to misread ownership.

Why SAFE knowledge matters for VC careers

SAFEs are not only founder paperwork. They are part of how seed deals are sourced, evaluated, and modeled.

If you are interviewing for analyst or associate roles, you should be able to explain why a founder might choose a SAFE, how a valuation cap affects ownership, and how outstanding SAFEs affect a future financing. That knowledge shows up in cap table reviews, seed-stage investment memos, and term-sheet discussions.

Venture Capital Careers publishes practical explainers on term sheets, valuation, and fundraising mechanics because those concepts matter in actual VC work. If you are learning the language of seed investing, start with this SAFE overview, then read the deeper guides linked above. If you are ready to apply that knowledge, browse open venture capital roles and look for roles that mention deal execution, sourcing, portfolio support, or investment analysis.

FAQs about SAFEs

Is a SAFE debt or equity?

A SAFE is not traditional debt and does not usually have interest or a maturity date. It is also not current equity. It is a contract for future equity treatment if a trigger event occurs.

Does a SAFE always convert?

No. A SAFE converts only if the events defined in the agreement occur. The most common trigger is a priced equity financing, but the agreement may also define treatment for a liquidity event or dissolution event.

What is a valuation cap in a SAFE?

A valuation cap is the maximum company valuation used to calculate the SAFE investor's conversion price. A lower cap generally gives the investor more potential ownership.

What is a discount in a SAFE?

A discount lets the SAFE investor convert at a lower price than the price paid by new investors in the priced round. For example, a 20% discount means the SAFE investor pays 80% of the new-money price, subject to the specific document terms.

What is a post-money SAFE?

A post-money SAFE states the valuation cap after accounting for the SAFE money. This makes it easier to estimate how much ownership has been sold in the SAFE financing before the later priced round dilutes everyone.

Can a SAFE include pro rata rights?

Yes, but pro rata rights are often handled through a side letter rather than the main SAFE form. The right matters when an investor wants the option to invest more capital in a future financing to maintain ownership.

Is a SAFE better than a convertible note?

It depends on the financing. A SAFE is usually simpler and has no maturity date or interest. A convertible note may fit better when investors want debt-like features, interest, maturity, or lender remedies.

Is a SAFE safe for investors?

The name can be misleading. A SAFE can be useful, but it does not guarantee repayment, ownership, conversion, or a return. Investors still bear startup risk, document risk, and conversion risk.

Bottom line

A SAFE is best understood as fast seed financing with delayed pricing. It can be the right instrument when a startup needs to raise early capital without running a full priced round, but the simplicity is only useful if both sides understand the ownership math.

Before signing one, model the dilution, read the conversion triggers, compare the SAFE with a convertible note or priced round, and get legal advice on the actual document. The form may be short; the future cap table impact is not.