SAFE vs Convertible Note: Key Differences and When to Use Each

Compare SAFEs and convertible notes by debt status, interest, maturity, conversion mechanics, dilution, investor leverage, and founder use cases.

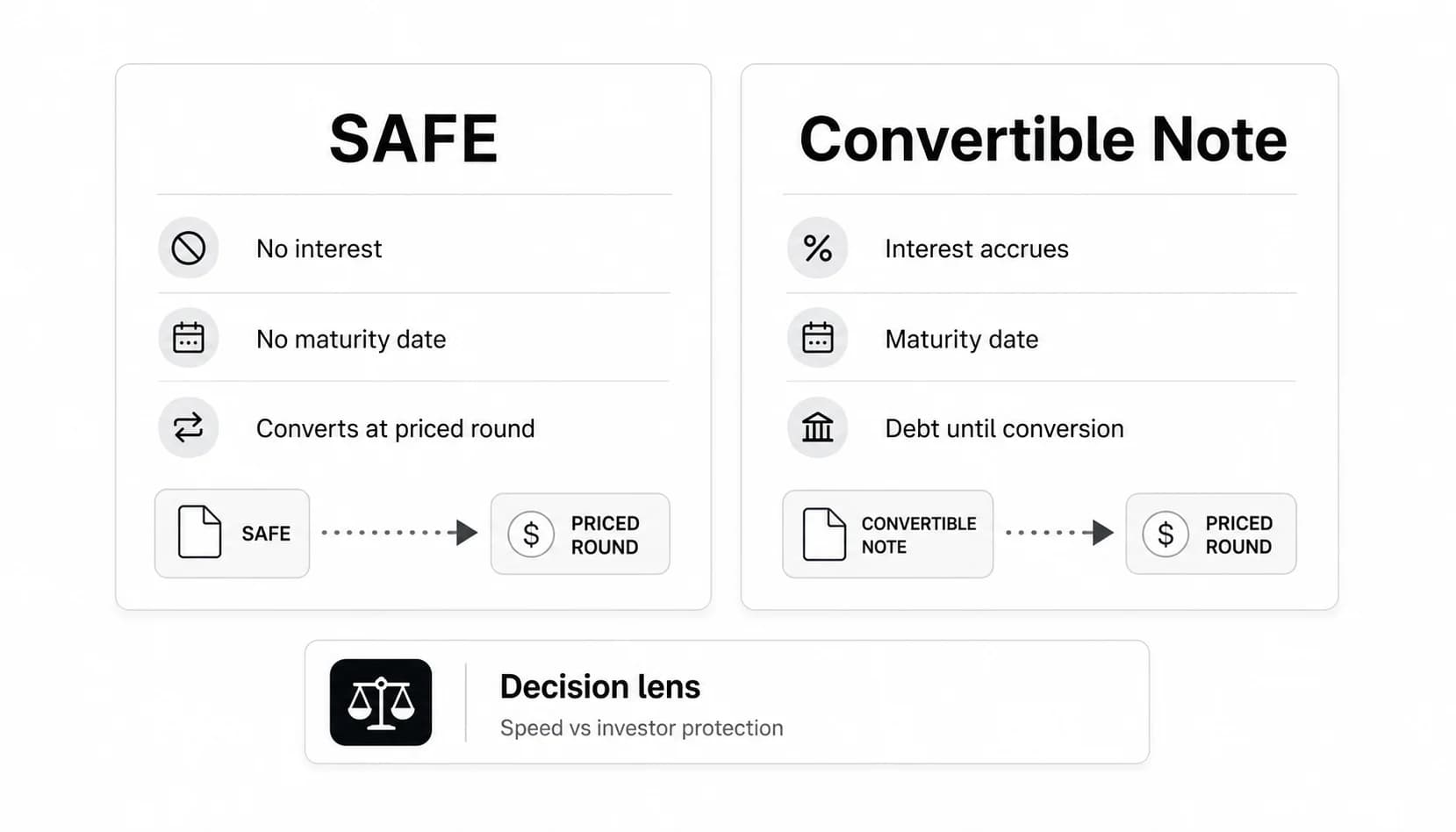

A SAFE is usually simpler for a startup because it is not debt, does not accrue interest, and normally has no maturity date. A convertible note is debt until it converts, so it usually includes interest, a maturity date, and more investor leverage if the next priced round takes longer than expected.

Both instruments let a startup raise money before setting a full equity valuation. The practical difference is what happens while everyone waits for the next financing event. A SAFE keeps the round fast and light. A convertible note creates a loan that later converts into equity, often with a valuation cap, discount, and accrued interest.

| Feature | SAFE | Convertible note |

|---|---|---|

| Legal form | Contract for future equity | Debt that can convert into equity |

| Interest | Usually none | Usually accrues until conversion or repayment |

| Maturity date | Usually none | Usually has a deadline |

| Repayment pressure | Lower unless the agreement has special terms | Higher if the note matures before conversion |

| Typical use | Fast pre-seed or seed rounds with standard terms | Bridge rounds or investor-led rounds where debt terms matter |

| Main founder risk | Underestimating future dilution, especially with stacked SAFEs | Interest, maturity, extension negotiation, and repayment pressure |

| Main investor benefit | Simple path to future equity | More downside leverage and clearer deadline |

What a SAFE is

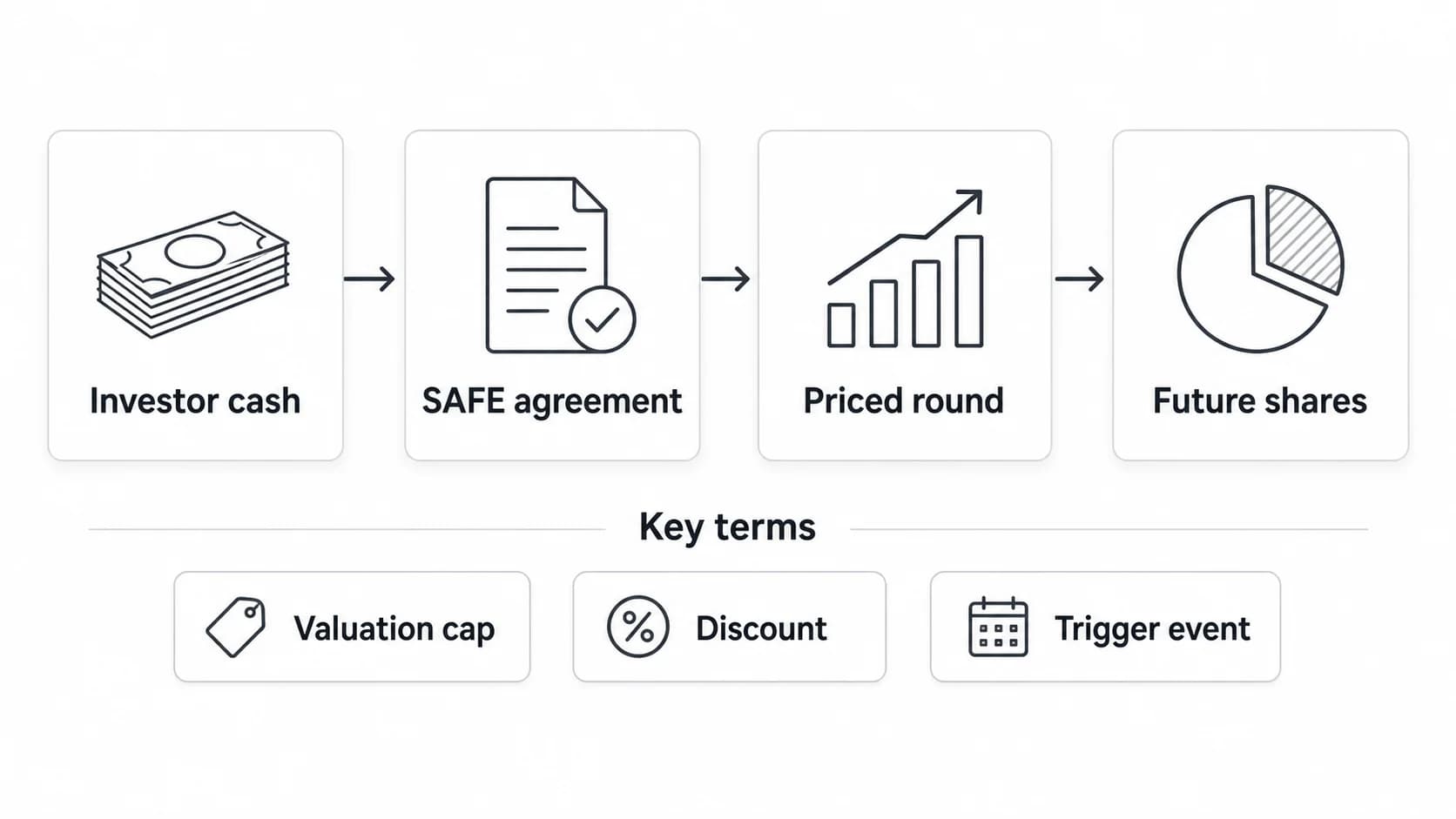

A SAFE, or Simple Agreement for Future Equity, gives an investor the right to receive equity in a future financing or exit event. It was popularized by Y Combinator, which maintains SAFE financing document templates for startups and investors.

A SAFE is not stock when it is signed. The investor does not immediately receive shares, voting rights, or a priced ownership percentage. Instead, the SAFE sits as a contractual right that converts later, usually when the company raises a priced equity round.

The most important SAFE terms are:

- Valuation cap: the maximum valuation used to calculate the investor's conversion price.

- Discount: a reduction from the price paid by new investors in the priced round.

- Most favored nation, or MFN: a provision that may let earlier SAFE investors receive better terms if the company later issues SAFEs with better economics.

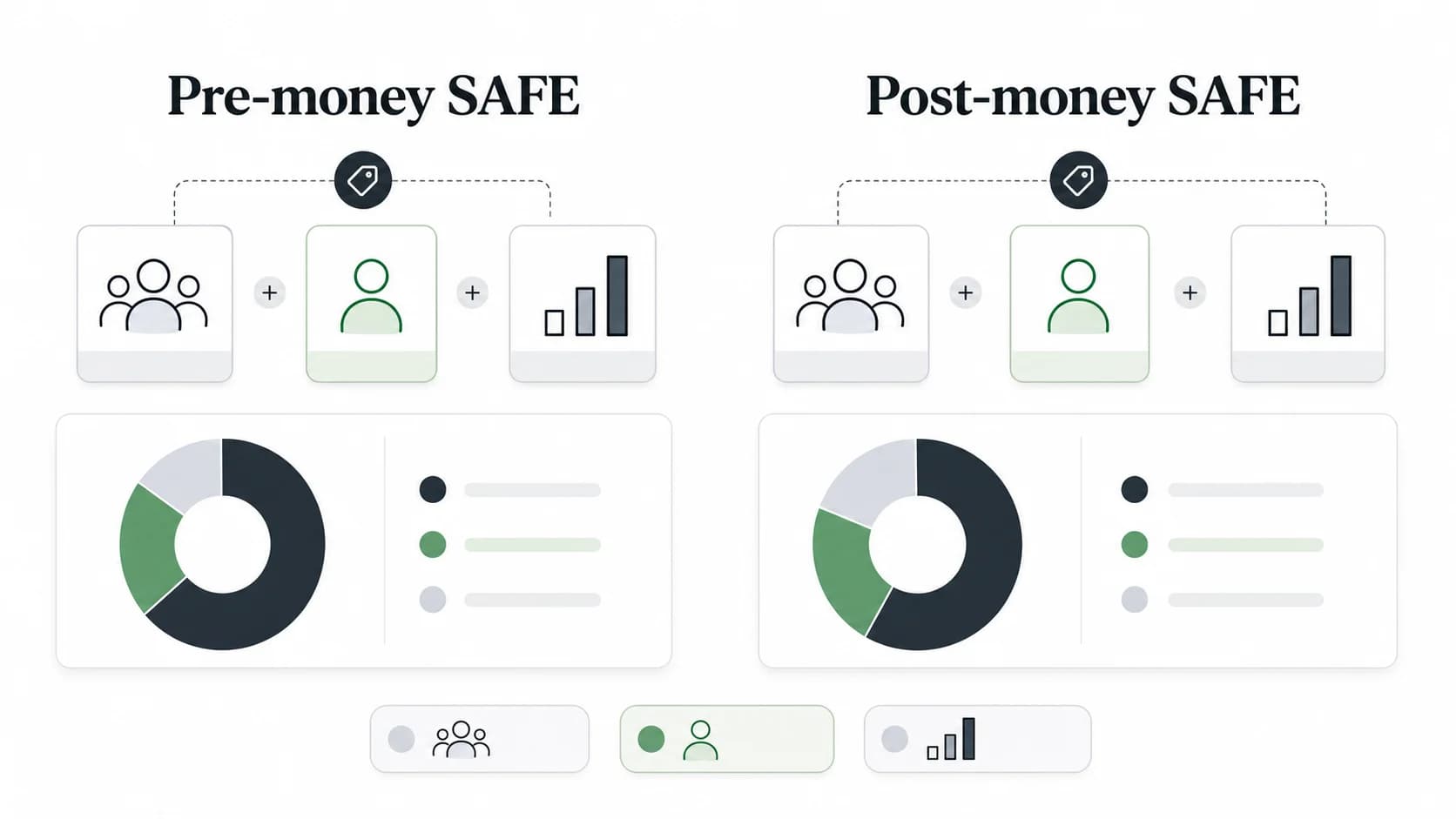

- Pre-money or post-money structure: a distinction that changes how predictable dilution is for founders and SAFE holders.

If the details are unfamiliar, start with the VCC guide to SAFE in venture capital and the separate comparison of pre-money vs post-money SAFE. The short version is that post-money SAFEs usually make ownership impact easier to model per instrument, while pre-money SAFEs can make the final cap table harder to predict when multiple SAFEs stack up.

What a convertible note is

A convertible note is a loan that is intended to convert into equity later. The investor lends money to the company. If a qualifying financing happens, the principal and usually accrued interest convert into shares under the note's conversion terms.

Carta's convertible securities explainer describes convertible securities as instruments that can convert into ownership later, and notes that convertible notes typically include interest and a maturity date. That is the core difference from a SAFE: a note is debt while it is outstanding.

The most important note terms are:

- Principal: the amount invested.

- Interest rate: the rate that accrues until conversion or repayment.

- Maturity date: the deadline when the note must be repaid, extended, or converted by agreement.

- Valuation cap: the maximum valuation used for conversion.

- Discount: the reduction from the next priced round price.

- Qualified financing threshold: the size or type of financing that triggers conversion.

The note may never be intended to be repaid in cash, but the debt form still matters. If the maturity date arrives before a priced round, the company and noteholders need to negotiate. That gives investors a pressure point that SAFE holders usually do not have.

SAFE vs convertible note: key differences

The choice is not just "simple document vs complicated document." It changes who has leverage if the fundraising plan slips.

| Difference | Why it matters for founders | Why it matters for investors |

|---|---|---|

| Debt status | A SAFE avoids putting a loan on the company at signing. A note creates debt. | Debt can give investors more negotiating leverage if the company misses milestones. |

| Interest | SAFEs usually do not increase the amount that converts. | Note interest increases the converting balance and can improve investor economics. |

| Maturity | SAFEs usually stay outstanding until a trigger or exit. | A note maturity date creates a deadline for repayment, extension, or renegotiation. |

| Conversion trigger | Both usually convert at a priced round, but exact triggers matter. | Investors care whether small rounds, acquisitions, or shutdowns are covered. |

| Legal cost and speed | SAFEs are often faster because standard forms are common. | Notes can justify more negotiation when investor protections matter. |

| Dilution predictability | Post-money SAFEs can be easier to model; stacked instruments still create surprises. | Notes require modeling principal plus interest, cap, discount, and maturity. |

For early seed funding, the founder-friendly answer is often a SAFE. For a bridge round, a strategic investor, or a round where the investor wants a deadline, a convertible note may fit better.

Example: why the same round can convert differently

Assume a startup raises $500,000 before its next priced round.

Scenario A: the company raises on a SAFE with an $8 million valuation cap and no discount.

Scenario B: the company raises on a convertible note with the same $8 million cap, 6% annual interest, and an 18-month period before the priced round.

At conversion, the SAFE converts based on the $500,000 investment amount. The note converts based on the principal plus accrued interest. At 6% annual interest for 18 months, the note balance is roughly $545,000 before any cap or discount math.

That extra $45,000 may not look dramatic in isolation. The issue is what happens when a company has several notes, extensions, side letters, or bridge rounds. The cap table can look manageable at signing and very different by the time the company prices the next round.

The exact share count depends on the priced round, the post-money valuation, the cap, the discount, the option pool, and other instruments. Model the fully diluted outcome before treating either instrument as "cheap capital."

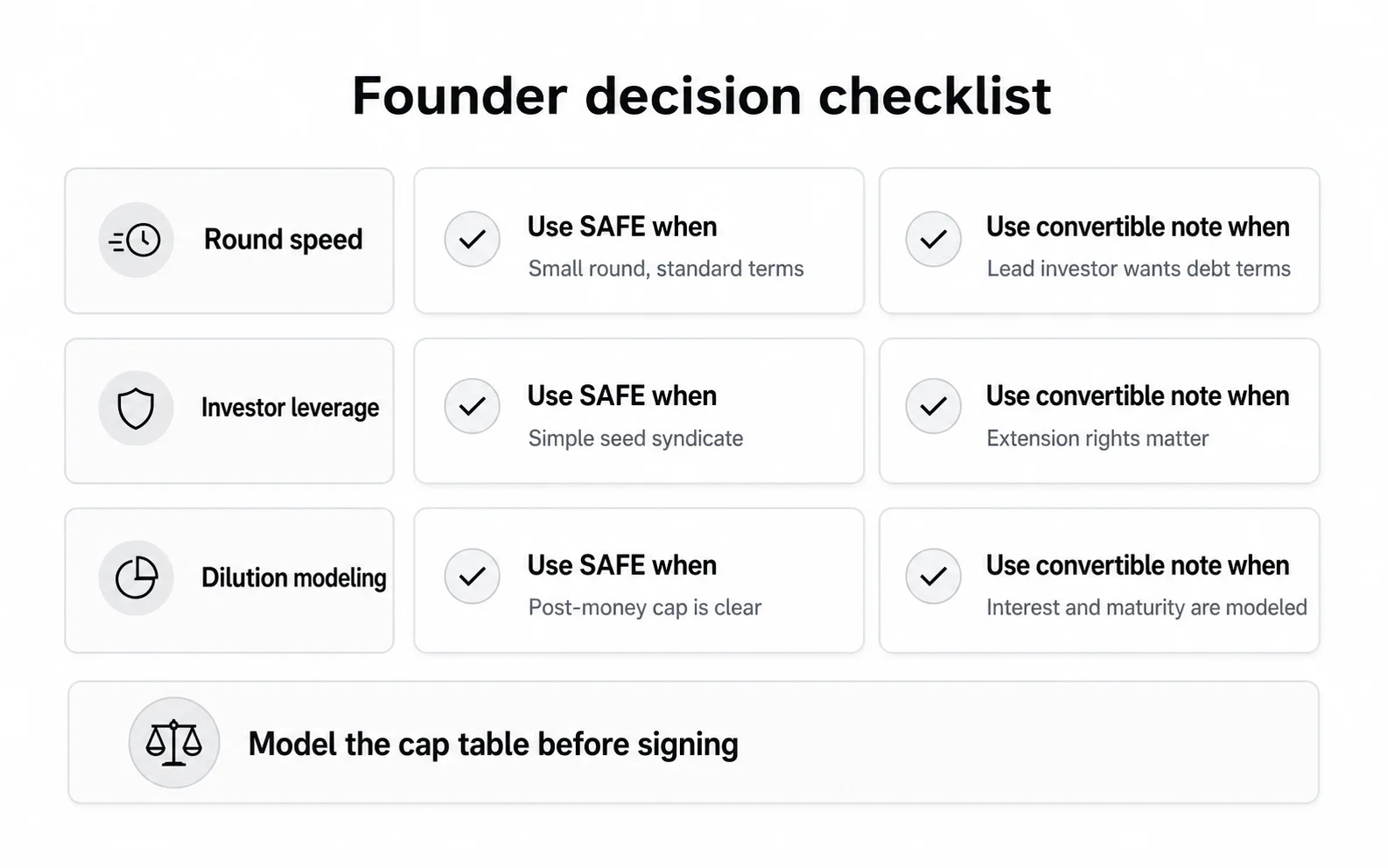

When to use a SAFE

A SAFE usually works best when the goal is speed and standardization.

Use a SAFE when:

- The round is a pre-seed or seed raise with familiar startup investors.

- The investor syndicate is broad and no single investor needs heavy control rights.

- The company wants to avoid debt, interest, and maturity pressure.

- The parties can use a standard form without heavy negotiation.

- The founder has modeled the post-money impact of every outstanding SAFE.

SAFEs are not automatically harmless. The document can be short, but the economics still matter. A low valuation cap, an MFN clause, or several SAFEs issued over time can create more dilution than founders expect.

When to use a convertible note

A convertible note can make sense when the investor needs more structure or when the financing is really a bridge.

Use a convertible note when:

- A lead investor wants debt treatment, interest, or a maturity date.

- The round is meant to bridge the company to a specific milestone or Series A funding.

- A strategic investor, nontraditional investor, or lender-style investor is involved.

- The company expects to renegotiate or extend if the next round slips.

- The parties want a defined deadline instead of an open-ended future equity right.

Notes are not automatically worse for founders. A clean note with a reasonable cap, modest interest, and a realistic maturity date can be more transparent than a stack of SAFEs issued at different caps.

What founders should model before signing

Before signing a SAFE or convertible note, build a simple financing memo. It does not need to be a full legal analysis, but it should answer the questions that change ownership.

| Question | Why it matters |

|---|---|

| What is the valuation cap? | The cap usually drives the investor's conversion price if the company grows quickly. |

| Is there a discount? | A discount can matter when the priced round valuation is below or near the cap. |

| Is the SAFE pre-money or post-money? | The structure changes dilution predictability. |

| Is there an MFN? | Future better terms may flow back to earlier investors. |

| Does the note accrue interest? | Interest increases the amount converting into shares. |

| When does the note mature? | Maturity creates a negotiation deadline. |

| What counts as a qualified financing? | Small or unusual rounds may not trigger automatic conversion. |

| Are pro rata rights included? | Investors may have the right to buy more in the next round. |

If the financing is part of a broader term sheet negotiation, do not review the instrument in isolation. The option pool, board rights, information rights, pro rata rights, and liquidation terms can matter as much as the cap or discount.

Investor perspective

Investors often accept SAFEs because they are fast, familiar, and cheaper to paper than a priced round. That matters when the check is small and the company is too early for a detailed valuation negotiation.

Investors may prefer convertible notes when they want more protection. Interest compensates for time. Maturity creates a deadline. Debt treatment can create more leverage if the company does not raise the expected round.

The investor's preference can also reveal the financing situation. A small angel syndicate may be comfortable with a standard SAFE. A strategic investor, bridge investor, or investor writing a larger check may ask for a note because they want more control over what happens if the plan changes.

Founders should treat that preference as a negotiation signal, not as a moral judgment. The question is whether the requested protection matches the risk the investor is taking.

Legal and tax cautions

SAFEs and convertible notes are securities. They can affect tax treatment, financial statements, investor rights, and later financing documents. The right answer depends on jurisdiction, company structure, investor type, and the exact agreement.

Do not rely on a blog post to decide tax treatment or securities compliance. Use the article to understand the business tradeoff, then ask startup counsel to review the specific document, especially if the round includes non-U.S. investors, strategic investors, unusually low caps, side letters, or multiple outstanding instruments.

Common mistakes

Treating a SAFE as simple because it is short. The document may be standardized, but the cap table impact can be complicated.

Ignoring note maturity. A maturity date that looks far away at signing can arrive before the company is ready for a priced round.

Stacking instruments without one model. Several SAFEs or notes with different caps, discounts, and MFNs can create a confusing conversion waterfall.

Comparing only legal fees. Speed matters, but economics matter more. A fast document with poor terms is still expensive capital.

Forgetting the next round. The real audience for today's SAFE or note is often the next lead investor. If the documents are messy, the next financing can take longer.

Next steps

If you are choosing between a SAFE and a convertible note, start with the business reason for the round. If the round is a small, standard early raise, a SAFE may be the cleanest route. If the money is a bridge, the investor wants downside protection, or the timeline needs a hard deadline, a convertible note may be easier to justify.

Then model the cap table. Read the VCC guides to SAFE in venture capital, convertible notes, pre-money vs post-money SAFEs, and cap tables. If you are still mapping the fundraising process, continue with seed funding and Series A funding.

Founders researching potential investors can also use the Venture Capital Careers companies directory to understand which venture capital firms invest at the relevant stage.

FAQ

What is the main difference between a SAFE and a convertible note?

A SAFE is usually a contract for future equity, not debt. A convertible note is debt that can convert into equity later. That is why notes usually include interest and maturity dates, while SAFEs usually do not.

Is a SAFE better than a convertible note?

Neither is always better. A SAFE is often better for a fast, standard early-stage raise. A convertible note can be better when the investor wants a maturity date, interest, or more protection if the next round is delayed.

Do investors prefer SAFEs or convertible notes?

It depends on investor type and leverage. Many startup investors accept SAFEs for small early rounds because they are familiar and fast. Some investors prefer notes because debt, interest, and maturity create more protection.

What happens if a SAFE never converts?

The SAFE usually remains outstanding until a conversion trigger, liquidity event, dissolution event, or another contract-defined outcome. That can leave founders and investors with unresolved economics for a long time, so the trigger language matters.

What happens if a convertible note does not convert before maturity?

The company and noteholders need to follow the note terms. That may mean repayment, extension, amendment, or negotiated conversion. In practice, early-stage startups often negotiate an extension if repayment is unrealistic, but the maturity date gives noteholders leverage.

Can a startup use both SAFEs and convertible notes?

Yes, but it should be intentional. Mixing instruments can make the next round harder if each instrument has a different cap, discount, MFN, maturity, or side letter. Build one model that shows how every instrument converts.

Should a founder choose the highest valuation cap possible?

A higher cap usually reduces investor ownership at conversion, but it may also make the round harder to raise. The better question is whether the cap matches the company's traction, stage, investor demand, and next-round expectations.