Post-Money Valuation: Formula, Examples, and VC Round Mechanics

Learn post-money valuation, the formula, ownership math, option-pool impact, SAFE caveats, and VC round examples for founders and investors.

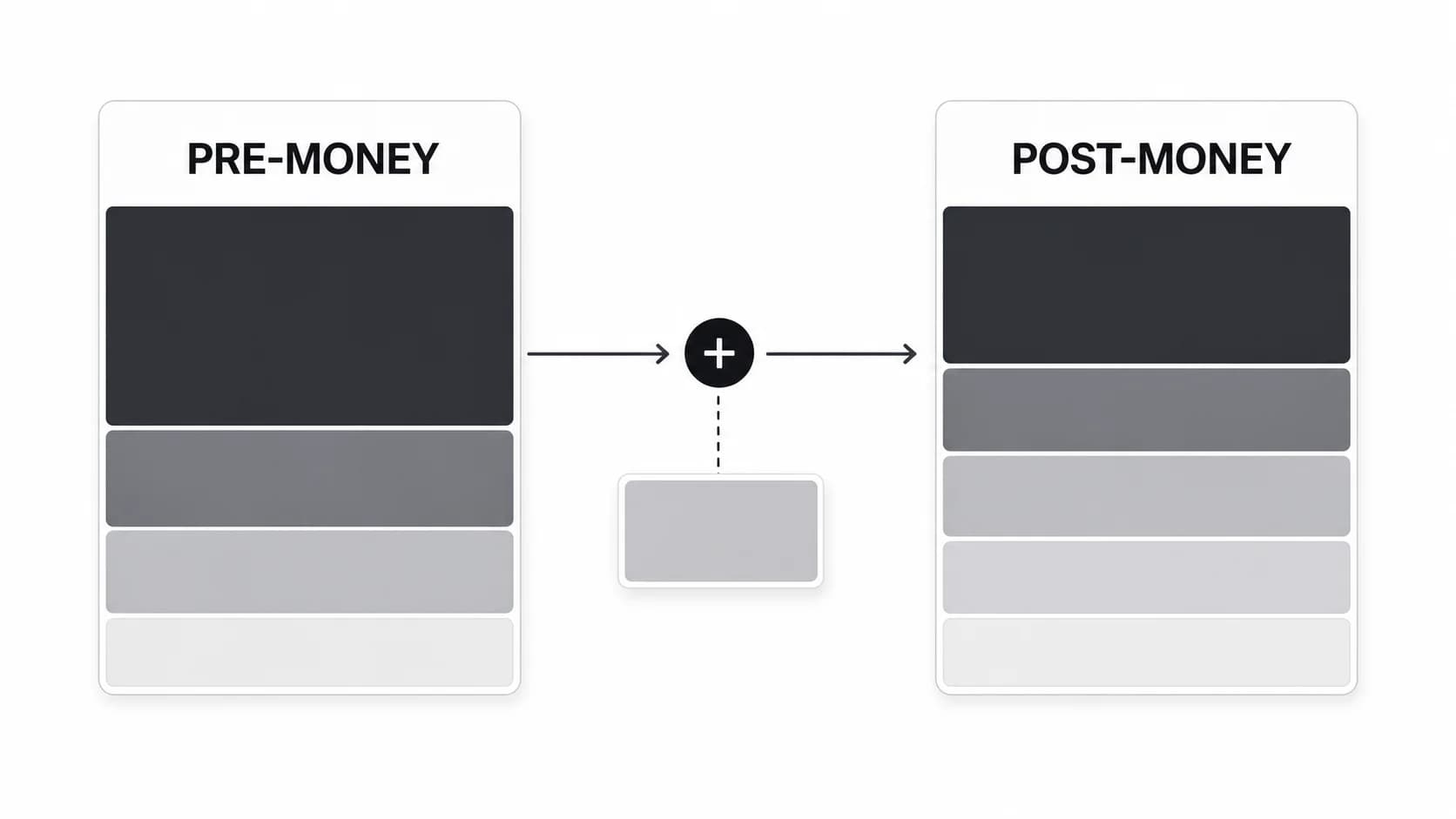

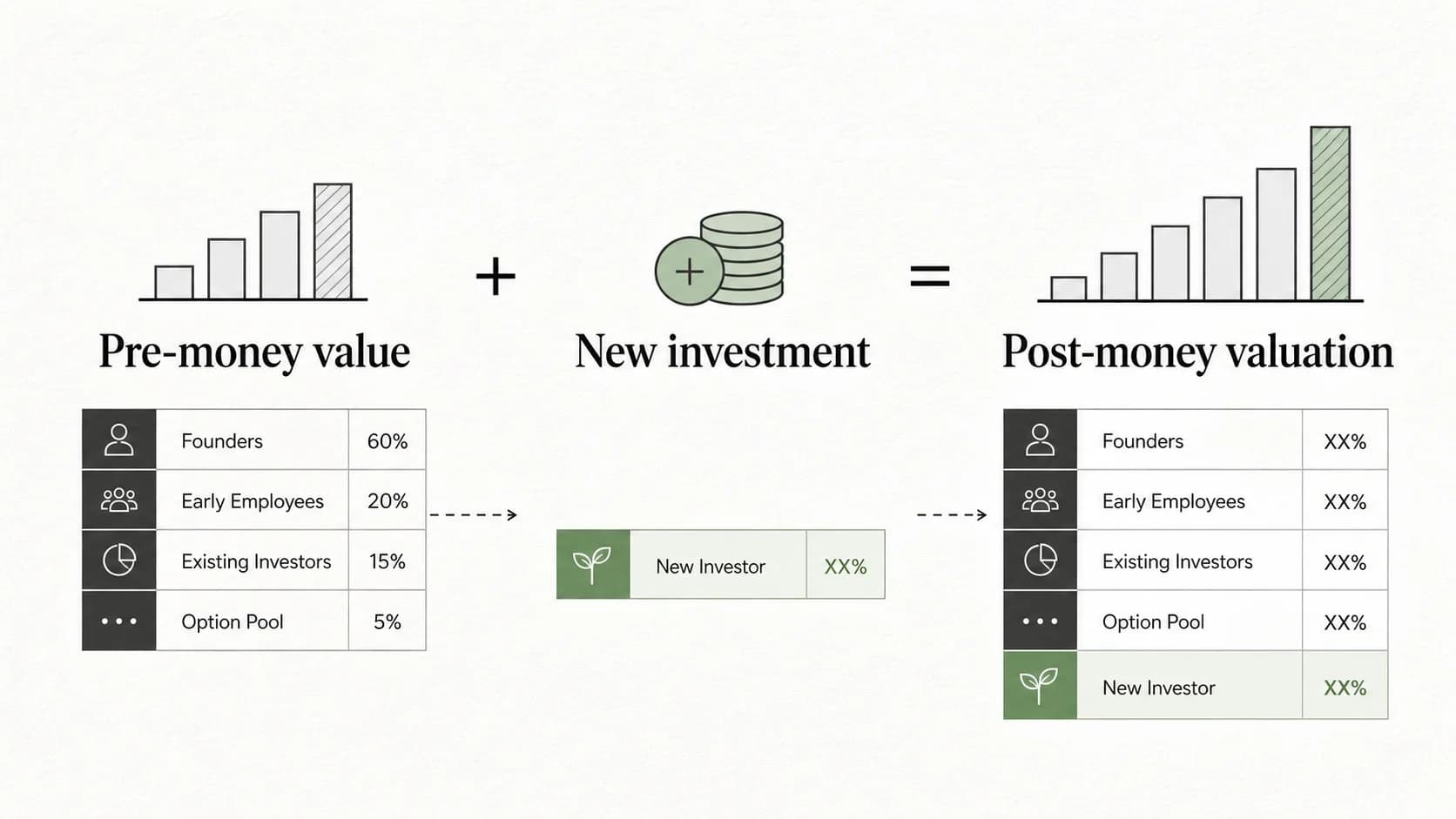

Post-money valuation is the value of a company immediately after a financing round closes. The simplest formula is:

Post-money valuation = pre-money valuation + new investment

If a startup raises $2 million at an $8 million pre-money valuation, the post-money valuation is $10 million. The investor who puts in the full $2 million owns 20% of the company after the round, before considering any more detailed terms.

That simple math is why post-money valuation shows up in term sheets, cap tables, investment memos, and VC interview questions. It connects the round price to ownership, dilution, and the return a fund needs from the investment.

What is post-money valuation?

Post-money valuation is the implied company value after new money has been invested. It includes the cash from the financing round.

In a priced equity round, the post-money valuation helps answer three questions:

- How much is the company worth after the round?

- What percentage of the company does the new investor receive?

- How much dilution do founders, employees, and existing investors take?

The number is usually negotiated alongside the investment amount, share price, option pool, and investor rights. A founder should not evaluate the headline valuation without looking at those mechanics.

Post-money valuation formula

The core formula is:

| Input | Example |

|---|---|

| Pre-money valuation | $8,000,000 |

| New investment | $2,000,000 |

| Post-money valuation | $10,000,000 |

Investor ownership is calculated as:

Investor ownership = investment amount / post-money valuation

Using the same example:

| Calculation | Result |

|---|---|

| $2,000,000 / $10,000,000 | 20% investor ownership |

| Founder and existing holder ownership before option-pool changes | 80% |

The arithmetic is simple. The hard part is knowing which inputs are being used.

Pre-money vs post-money valuation

Pre-money valuation is the company's value before the new investment. Post-money valuation is the company's value after the investment.

| Term | Meaning | Example |

|---|---|---|

| Pre-money valuation | Company value before new capital | $8 million |

| New investment | Cash invested in the round | $2 million |

| Post-money valuation | Company value after new capital | $10 million |

The distinction matters because investor ownership is based on the post-money number. A $2 million investment at an $8 million pre-money valuation buys 20%. The same $2 million investment at an $8 million post-money valuation buys 25%.

For a deeper companion explanation, read the Venture Capital Careers guide to pre-money valuation.

A practical cap table example

Assume a startup has 8,000,000 fully diluted shares before a Series Seed round. The company raises $2 million at an $8 million pre-money valuation.

| Step | Calculation | Result |

|---|---|---|

| Pre-money share price | $8,000,000 / 8,000,000 shares | $1.00 |

| New investor shares | $2,000,000 / $1.00 | 2,000,000 shares |

| Fully diluted shares after round | 8,000,000 + 2,000,000 | 10,000,000 shares |

| Post-money valuation | 10,000,000 shares x $1.00 | $10,000,000 |

| Investor ownership | 2,000,000 / 10,000,000 | 20% |

This is the version of the concept a founder, investor, or VC candidate should be able to explain without hiding behind the formula.

What post-money valuation tells founders and investors

Post-money valuation is useful because it turns a financing round into ownership math.

For founders, it shows how much of the company is sold in exchange for the new capital. A higher pre-money valuation usually means less dilution for the same investment amount, but a high price can also create pressure for the next round.

For investors, it shows the entry price. If a VC fund invests at a $50 million post-money valuation and wants a 10x outcome, the company likely needs to create hundreds of millions of dollars of exit value after future dilution. The higher the entry valuation, the more the investor must believe in the market, team, growth rate, and exit path.

For employees, post-money valuation can help frame what an equity grant might be worth, but only with caution. Option grants depend on strike price, common-stock value, future dilution, vesting, taxes, and exit terms.

What post-money valuation does not tell you

Post-money valuation is not the same as cash in the bank, enterprise value, or guaranteed exit value.

It also does not tell you how sale proceeds will be divided. Venture rounds often include preferred stock. Preferred stock can carry rights that common stock does not, including liquidation preferences, anti-dilution protection, information rights, and voting rights. Those terms can change outcomes in a downside sale even when the headline post-money valuation looked attractive.

If you are evaluating investor economics, pair the valuation with the term sheet, the liquidation preference, the anti-dilution provision, and the company's cap table.

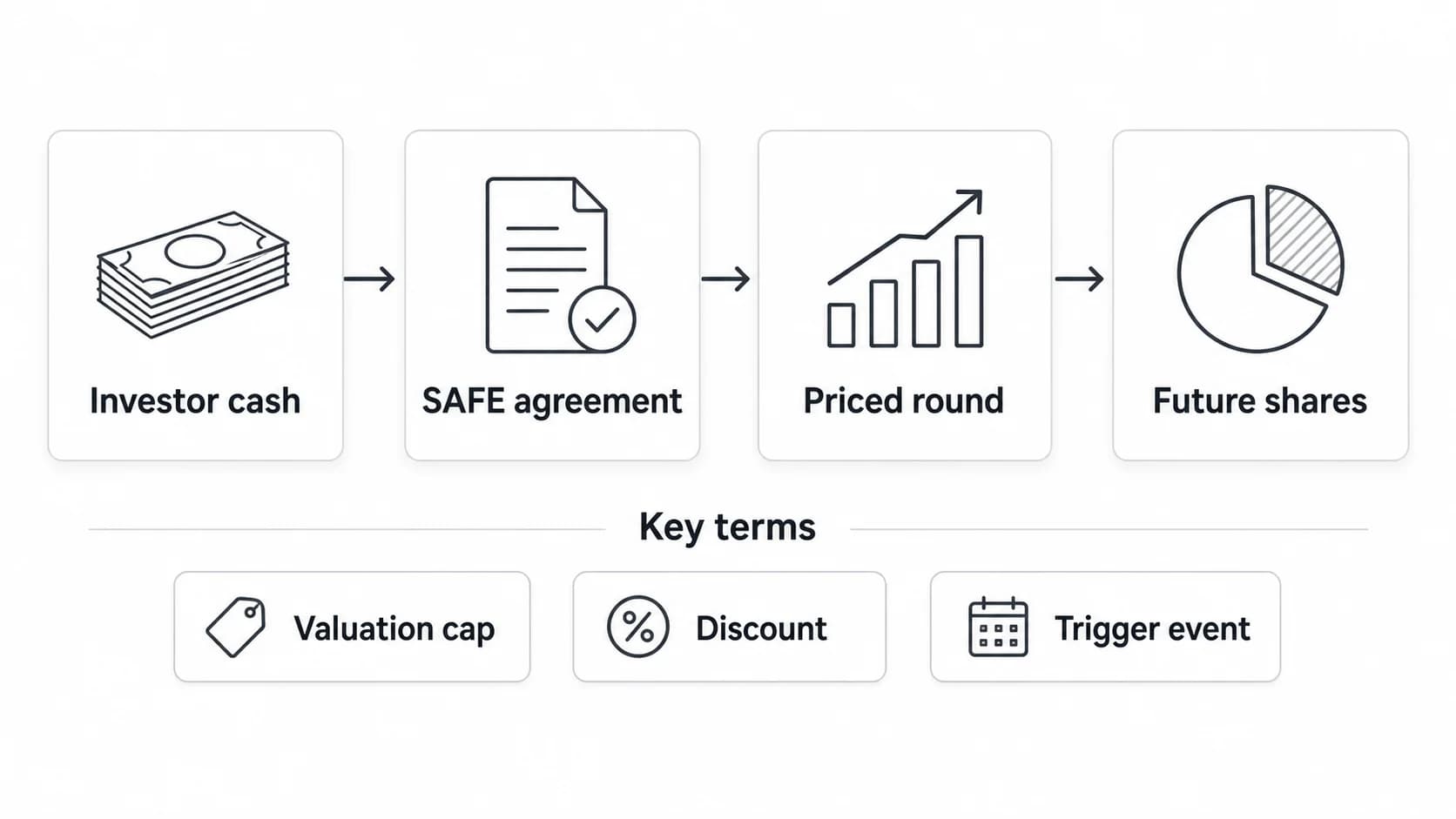

Option pools, SAFEs, and preferred stock

Three details often change how post-money valuation feels in practice.

Option pool placement

If investors require an option-pool increase before the financing, that increase usually dilutes existing holders more than the new investor. A term sheet might say the pre-money valuation is $8 million, but also require a 10% or 15% post-closing option pool. The founder should ask whether the pool is included in the pre-money calculation and model the fully diluted result.

Post-money SAFEs

A SAFE is not a priced equity round, but it can still use post-money language. Y Combinator's current SAFE document set includes post-money SAFE forms for U.S. companies, including valuation-cap, discount, and uncapped MFN versions. That matters because a post-money SAFE is designed to make ownership from the SAFE easier to calculate before the next priced round.

For a dedicated explanation, read pre-money SAFE vs post-money SAFE and the broader guide to SAFEs in venture capital.

Preferred-share economics

Most institutional venture rounds issue preferred stock, not common stock. The headline valuation may assume a share price, but the investor is buying a security with negotiated rights. The NVCA model legal documents are a useful reference point for the standard venture financing document set, including the certificate of incorporation, stock purchase agreement, investors' rights agreement, voting agreement, and right of first refusal and co-sale agreement.

Common mistakes when using post-money valuation

Treating the headline valuation as the full economic answer

A $20 million post-money valuation does not mean every shareholder participates equally in every exit. Preferences, seniority, and conversion rights matter.

Ignoring the option pool

If the option pool is expanded before the round, founders and existing holders may take more dilution than the simple investment divided by post-money formula suggests.

Mixing pre-money and post-money language

Do not say "the round is at $10 million" without specifying whether that is pre-money or post-money. The ownership difference can be material.

Forgetting future dilution

The post-money cap table is a snapshot. Future SAFEs, notes, option grants, down rounds, follow-on rounds, and acquisitions can all change ownership.

Assuming valuation equals price discipline

A high valuation can be good for dilution today and bad for fundraising later if the company cannot grow into it. A lower valuation with cleaner terms may be better than a higher valuation with aggressive preferences or a difficult option-pool requirement.

How VC candidates should use post-money valuation

Post-money valuation is a basic concept, but interviewers use it to test whether a candidate understands ownership and returns.

In an interview or investment memo, do not stop at "pre-money plus investment." Show the ownership math and the implication:

- What percentage does the investor buy?

- Is the share count fully diluted?

- Does the round include an option-pool increase?

- Are SAFEs or convertible notes converting in the round?

- What future valuation or exit value would the fund need for the investment to work?

Candidates looking at analyst and associate roles can use the Venture Capital Careers job board to see how firms describe valuation, cap table, diligence, and investment memo responsibilities. The companies directory is also useful for researching funds before interviews.

Related valuation terms

| Term | Why it matters |

|---|---|

| Pre-money valuation | Starting value before the new investment |

| Post-money valuation | Value after the new investment |

| Fully diluted shares | Share count used to calculate ownership, usually including options and other convertible securities |

| Option pool | Shares reserved for current or future employees |

| SAFE valuation cap | Conversion cap used in a SAFE, not the same as a priced-round valuation |

| Liquidation preference | Determines who gets paid first in a sale or liquidation |

| Down round | A round priced below a prior round's valuation |

FAQ

How do you calculate post-money valuation?

Add the new investment amount to the pre-money valuation. If a company raises $3 million at a $12 million pre-money valuation, the post-money valuation is $15 million.

How do you calculate investor ownership from post-money valuation?

Divide the investment amount by the post-money valuation. A $3 million investment at a $15 million post-money valuation equals 20% ownership.

Is post-money valuation higher than pre-money valuation?

Usually yes in a priced round, because post-money valuation includes the new investment. The exception is when people are using the terms imprecisely or comparing different rounds.

Does post-money valuation include debt?

In startup financing conversations, post-money valuation usually refers to equity value after the round, not enterprise value. Debt can still affect how investors think about risk and value, but it is not normally added in the simple post-money formula.

Is post-money valuation the same as market capitalization?

It is similar in structure because both can be calculated from shares and share price. The difference is context: market capitalization is used for public companies with traded shares, while post-money valuation is used in private financing rounds.

Why does the option pool affect post-money valuation?

The option pool affects dilution and share count. If the pool is increased before the round, existing holders usually absorb that dilution. If it is increased after the round, the dilution is shared by more holders, including the new investor.

Is a post-money SAFE the same as a post-money valuation?

No. A post-money SAFE is a financing contract designed to define future ownership more clearly when the SAFE converts. A post-money valuation in a priced round is the company value after the new equity investment closes.