What is a Liquidation Preference?

In the realm of startups and venture capital investments, numerous financial terms and mechanisms hold significant importance for both entrepreneurs and investors. One such crucial term is "liquidation preference." But what exactly is a liquidation preference, and why should you care? This blog post will provide an in-depth exploration of liquidation preferences, helping you understand their role and impact on investment deals.

Liquidation preferences are provisions in the investment agreements that determine the order and priority of payouts during a liquidity event, such as the sale or merger of a company. These preferences are often used to protect investors' interests, ensuring they receive a return on their investment before other shareholders, like the company's founders and employees.

Understanding liquidation preferences is essential for anyone involved in startups and venture capital investments. For venture capital investors, it provides a layer of security and helps manage risk, while for entrepreneurs, it can influence the company's valuation and the distribution of proceeds in an exit scenario. This post will guide you through the ins and outs of liquidation preferences, empowering you to make more informed decisions in your entrepreneurial journey or investment endeavors.

What Are Liquidation Preferences?

Liquidation preferences are specific provisions included in investment agreements that outline the order of payouts and priority for investors and shareholders during a liquidity event. A liquidity event refers to a situation where a company's assets are sold, the company is acquired or merged, or it goes public through an initial public offering (IPO). The primary purpose of liquidation preferences is to ensure that investors, particularly those holding preferred shares, receive a predefined return on their investment before any distribution of proceeds to other shareholders, such as founders or employees holding common shares.

Liquidation preferences play a vital role in determining startup valuations and returns for investors. They can influence the outcome of negotiations between investors and founders, often leading to a higher valuation for the company. When investors have a liquidation preference, they are assured a certain return on their investment, reducing their risk and making them more comfortable with a higher valuation.

Moreover, liquidation preferences can impact returns for investors in scenarios where a company's exit value is lower than anticipated. With a liquidation preference, investors are more likely to recoup their initial investment or even make a profit, while common shareholders may receive little or nothing. As a result, understanding how liquidation preferences work is crucial for investors and founders alike when entering into investment deals.

There are several common types of liquidation preferences that vary based on the degree of investor protection and participation in the proceeds of a liquidity event. These include:

Non-participating preferred stock: This type of liquidation preference allows investors to receive their initial investment back plus any accrued dividends before any distribution to common shareholders. After this payout, they do not participate in any remaining proceeds.

Participating preferred stock: In addition to receiving their initial investment and accrued dividends, investors with participating preferred stock also share in the remaining proceeds with common shareholders, typically based on their ownership percentage.

Capped participating preferred stock: This type of liquidation preference is similar to participating preferred stock but includes a cap on the total return an investor can receive. Once the cap is reached, any remaining proceeds are distributed among common shareholders.

Understanding the different types of liquidation preferences can help both investors and founders make informed decisions when negotiating investment deals and navigating the complex world of startup financing.

How Liquidation Preferences Work

In this section, we'll explore the mechanics behind liquidation preferences, including the seniority (preference stack), priority of payouts during liquidation events, and the impact of conversion rights on liquidation preferences.

The preference stack represents the hierarchy of payouts during a liquidity event, with different classes of preferred stock having varying levels of seniority or priority. The most common seniority structures are:

Pari passu: In this structure, all preferred stock classes share the same level of seniority. This means that during a liquidity event, all preferred shareholders receive their liquidation preferences simultaneously, with proceeds being distributed pro-rata based on their investment amounts.

Sequential seniority: In a sequential seniority structure, each class of preferred stock has a different level of priority in the preference stack. In this scenario, the payouts during a liquidity event occur in a predetermined order, with higher-priority classes receiving their liquidation preferences before lower-priority classes.

Standard seniority: In this structure, liquidation preferences are paid out in order from the latest investment round to the earliest rounds. This means that new investors in the most recent funding round receive their liquidation preferences first, followed by earlier round investors in descending order, e.g. early-stage investors get paid last.

Liquidation preferences are typically reflected as multiples of the original investment amount, such as 1x or 2x liquidation preference. This liquidation preference multiple indicates the minimum return an investor expects to receive during a liquidity event before any distribution to other shareholders.

The priority of payouts during liquidation events is determined by the liquidation preference structure and seniority of each class of stock. When a liquidity event occurs, the proceeds are distributed in the following order:

Any outstanding debts and obligations of the company are settled

Investors with preferred stock receive their respective liquidation preferences based on seniority

Remaining liquidation proceeds, if any, are distributed among common stockholders.

Conversion rights can also significantly influence liquidation preferences. These rights allow investors holding preferred stock to convert their shares into common stock, usually on a one-to-one basis. The decision to exercise conversion rights depends on the potential returns from a liquidity event. If the return for an investor with preferred stock is greater when exercising their conversion rights, they may choose to convert their shares, impacting the overall liquidation preference payouts. However, if the return for retaining their preferred stock and liquidation preference is higher, the investor would likely opt to maintain their preferred shares.

Understanding the interplay between the preference stack, priority of payouts, and conversion rights is essential for investors and founders to effectively navigate liquidation preference structures and make informed decisions during investment negotiations and liquidity events.

Why Liquidation Preferences Exist

Liquidation preferences serve several essential purposes in the context of startup investments and venture capital deals. These include protection for investors, encouraging investments by mitigating risk, and aligning investor and founder interests.

One of the primary reasons liquidation preferences exist is to provide a level of protection for investors in the event that a startup underperforms or faces a liquidation event. By ensuring that investors receive a predetermined return on their investment before any distribution to other shareholders, liquidation preferences help reduce the financial risk for investors, especially in situations where the startup's value at the time of the liquidity event is lower than expected.

Liquidation preferences can also serve as an incentive for investors to provide capital to startups by mitigating the inherent risks associated with early-stage investments. By offering a guaranteed return in the form of liquidation preferences, startups can attract investors who might otherwise be hesitant to invest due to the uncertain nature of startup ventures. This can be particularly important for startups seeking substantial capital to fund their growth and development.

Finally, liquidation preferences can help align the interests of investors and founders, promoting a collaborative approach to achieving the company's goals. By ensuring that both parties have a vested interest in the success of the startup, liquidation preferences can motivate investors and founders to work together towards the common objective of maximizing the company's value. This alignment of interests can contribute to a more productive working relationship and a higher likelihood of a successful outcome for all stakeholders involved.

Liquidation preferences play a critical role in the startup investment ecosystem, providing protection for investors, encouraging investment by reducing risk, and fostering a collaborative environment between investors and founders. Understanding the rationale behind liquidation preferences is essential for both parties to negotiate fair terms and work together effectively towards the success of the startup.

The Role of Liquidation Preferences in Venture Capital

Liquidation preferences play a significant role in venture capital investments, serving as a key component in investor protection and risk management, influencing deal negotiations and term sheets, and appearing in various forms across VC deals.

Investor protection and risk management are central to venture capital investing. Given the high-risk nature of investing in early-stage companies, preferred investors seek ways to safeguard their investments and manage potential losses. Liquidation preferences serve this purpose by ensuring that investors receive a predetermined payout before other shareholders in the event of a liquidity event. By prioritizing their returns, investors can mitigate some of the financial risks inherent in venture capital investing.

Deal negotiations and term sheets are also heavily influenced by liquidation preferences. As investors and founders work to agree on the terms of an investment, liquidation preferences often emerge as a crucial point of discussion. These preferences can be used as bargaining chips, with investors seeking stronger liquidation preferences in exchange for more money or a more favorable valuation. Conversely, founders may push for less aggressive liquidation preferences to retain a more significant portion of the potential upside. The resulting term sheets often reflect a balance between the interests of both parties, with liquidation preferences being a key factor in reaching an agreement.

Examples of liquidation preferences in VC deals can vary widely, depending on factors such as the startup's stage of development, the investor's risk appetite, and the overall market conditions. In some cases, preferred investors may require only a modest liquidation preference, such as a 1x multiple of their investment. In other instances, particularly in more competitive funding environments or where the perceived risk is higher, investors may seek higher multiples, such as 2x or even 3x liquidation preference. Additionally, the structure of these preferences, such as participating or non-participating preferred stock, can also differ based on the specific deal terms.

Liquidation preferences are a fundamental aspect of venture capital investing, playing a critical role in preferred investor protection, deal negotiations, and term sheet formation. Understanding the various ways liquidation preferences can manifest in VC deals is essential for both investors and founders as they navigate the investment process and work towards mutually beneficial outcomes.

Types of Liquidation Preferences

Liquidation preferences come in several forms, each with its unique implications for investors and founders. The most common types are non-participating preferred stock with a non-participating liquidation preference, participating preferred stock with participation rights, and capped participating preferred stock. Each type has its unique characteristics, and understanding their differences is crucial for both investors and founders when negotiating terms and assessing the implications of a specific liquidation preference structure.

Non-participating preferred stock, or non-participating liquidation preference, provides investors with a fixed return on their investment during a liquidity event. With this structure, investors receive their liquidation preference (typically a multiple of the original issue price of their preferred stock) before any distribution to equity holders. Once the liquidation preference has been paid, non-participating preferred stockholders do not participate in any further distribution of proceeds. This type of liquidation preference is generally considered more founder-friendly, as it allows founders and equity holders to receive a larger share of the remaining proceeds after the liquidation preference has been paid.

In contrast, participating preferred stock provides investors with a double-dip return structure. With this type of liquidation preference, investors first receive their liquidation preference (as with non-participating preferred stock), and then they also participate in the distribution of the remaining proceeds alongside common shareholders, typically on a pro-rata basis. This structure is more favorable to investors, as it allows them to benefit from both their liquidation preference and any additional gains resulting from the startup's growth and success.

Capped participating preferred stock is a variation of participating preferred stock, where the investor's participation in the remaining proceeds is limited to a predetermined cap or multiple of their original investment. Once the cap is reached, investors cease to participate in further distributions, and the remaining proceeds are allocated to common shareholders. This structure provides a middle ground between non-participating and participating preferred stock, offering investors some additional return potential while still protecting the interests of founders and common shareholders.

Each type of liquidation preference comes with its advantages and drawbacks for both investors and founders. Non-participating preferred stock may be more appealing to founders, as it allows them to retain a larger share of the proceeds in a liquidity event. However, it may be less attractive to investors, as it limits their return potential. Participating preferred stock offers investors greater return potential, but it may be viewed as less founder-friendly, as it can result in a smaller share of the proceeds for founders and common shareholders. Capped participating preferred stock attempts to strike a balance between the interests of both parties, offering investors some additional upside while still providing protection for founders and common shareholders.

Understanding the different types of liquidation preferences and their implications for investors and founders is essential for negotiating fair investment terms and managing expectations during liquidity events. Both parties should carefully consider the structure and terms of liquidation preferences, seeking a balance that aligns the interests of all stakeholders involved in the deal.

Negotiating Liquidation Preferences

Negotiating liquidation preferences is a critical aspect of venture capital deals, as the terms agreed upon can significantly impact the outcome for both investors and founders. There are several factors that both parties should consider, including balancing interests and employing effective negotiation tactics to reach fair terms.

Factors to consider for both investors and founders include the startup's stage of development, the perceived risk associated with the investment, the amount of capital being raised, and the desired return on investment. Additionally, both parties should consider the potential impact of the liquidation preference structure on future financing rounds and the overall health of the company.

Balancing interests between parties is crucial during negotiations. Investors typically seek stronger liquidation preferences to protect their investments and ensure a favorable return. Conversely, founders often strive for more lenient liquidation preferences to maintain a larger share of the company's upside potential. It is essential to strike a balance that addresses the concerns of both investors and founders while keeping the best interests of the company in mind.

Here are some tips for negotiating fair terms:

Be prepared: Both investors and founders should enter negotiations with a clear understanding of their objectives and priorities. This includes researching market norms for similar deals, understanding the potential implications of different liquidation preference structures, and being aware of the key concerns of the other party.

Establish a collaborative mindset: Approaching negotiations as a collaborative effort rather than a competition can lead to more productive discussions and mutually beneficial outcomes. Both parties should focus on finding solutions that address their concerns while promoting the long-term success of the company.

Be flexible: Maintaining flexibility during negotiations can help facilitate agreement on terms that are acceptable to both parties. This may involve being open to alternative structures or adjusting other aspects of the deal, such as valuation, to accommodate the other party's concerns.

Communicate openly and honestly: Transparent communication between investors and founders is crucial for building trust and fostering a productive negotiation process. Both parties should be candid about their concerns and objectives while listening carefully to the other party's perspective.

Seek professional advice: Engaging legal and financial advisors can provide valuable guidance during the negotiation process, ensuring that both parties understand the implications of different liquidation preference structures and helping to navigate complex deal terms.

Effectively negotiating liquidation preferences requires a thorough understanding of the factors at play, a focus on balancing the interests of all parties involved, and the use of effective negotiation tactics to reach fair and mutually beneficial terms. By considering these aspects, both investors and founders can work together to establish liquidation preferences that support the long-term success of the company.

Liquidation Preference Scenarios and Outcomes

Understanding how liquidation preferences play out in various scenarios can provide valuable insights for investors and founders when negotiating terms and evaluating the potential impact on investor returns and founder equity. By examining illustrative examples and learning from real-life cases, both parties can make more informed decisions when structuring and agreeing to liquidation preferences.

Here are three hypothetical scenarios that demonstrate how different liquidation preferences might affect the distribution of proceeds during a liquidity event:

Non-participating preferred stock: In a $100 million exit, an investor with a $20 million investment and a 1x non-participating liquidation preference would receive $20 million. The remaining $80 million would be distributed among the common shareholders, including the founders.

Participating preferred stock: In the same $100 million exit, an investor with a $20 million investment and a 1x participating liquidation preference would receive $20 million plus their pro-rata share of the remaining $80 million. For example, if the investor owned 25% of the company, they would receive an additional $20 million (25% of $80 million), totaling $40 million.

Capped participating preferred stock: In the same $100 million exit, an investor with a $20 million investment, a 1x liquidation preference, and a 2x cap would receive $20 million plus their pro-rata share of the remaining $80 million, up to a total of $40 million (2x their original investment). If the investor owned 25% of the company, they would reach their cap and receive $40 million in total.

The choice of liquidation preference structure significantly impacts investor returns and founder equity. In the examples above, non-participating preferred stock results in the most favorable outcome for founders, while participating preferred stock provides the highest return for investors. Capped participating preferred stock attempts to balance the interests of both parties.

Real-life cases, such as the acquisition of Good Technology, demonstrate the importance of understanding and carefully negotiating liquidation preferences. In these instances, the liquidation preference structures resulted in lower payouts for common shareholders, including founders and employees. These cases highlight the need for both investors and founders to consider the potential implications of liquidation preferences on all stakeholders and to strike a balance that promotes the long-term success of the company.

Examining liquidation preference scenarios and outcomes can help investors and founders better understand the impact of different structures on investor returns and founder equity. By learning from illustrative examples and real-life cases, both parties can make more informed decisions when negotiating and structuring liquidation preferences, ultimately leading to more successful investment outcomes.

Liquidation Preferences in Context: Other Investor Protection Mechanisms

While liquidation preferences are an essential component of venture capital deals, they are not the only mechanism designed to protect investors. Several other investor protection mechanisms work in conjunction with liquidation preferences to help safeguard investments and ensure favorable returns. These mechanisms include anti-dilution provisions, protective provisions, preemptive rights, and board representation.

Anti-dilution provisions protect investors from dilution of their ownership stake in the event of future financing rounds at a lower valuation (known as a "down round"). These provisions adjust the conversion rate of preferred shares into common shares to maintain the investor's ownership percentage, thus preserving their investment value.

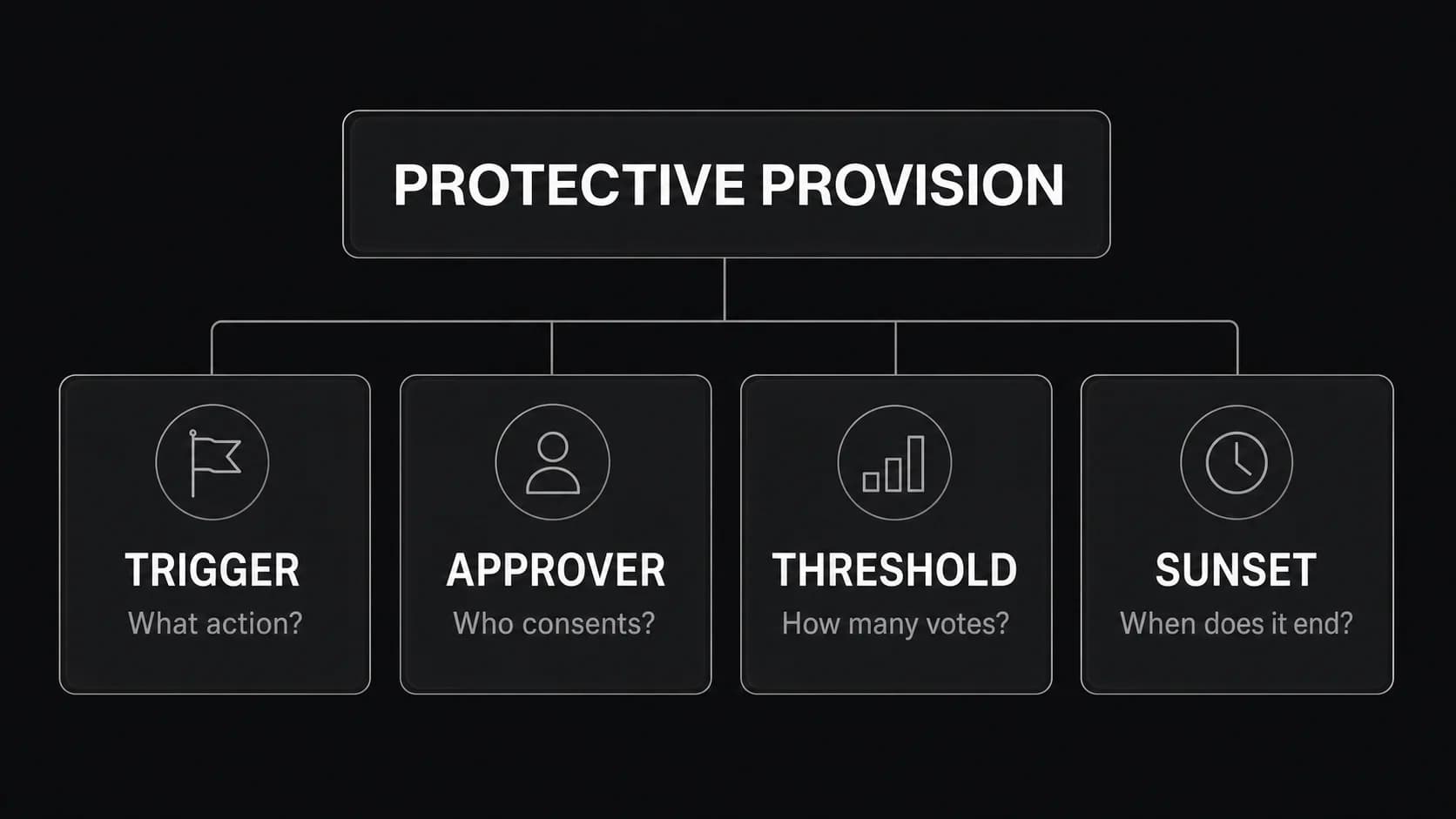

Protective provisions grant investors veto power over certain significant corporate actions or decisions, such as issuing new shares, merging with another company, or selling substantial assets. These provisions ensure that investors have a say in critical decisions that could potentially impact their investment.

Preemptive rights grant investors the option to participate in future financing rounds to maintain their ownership percentage. This right allows investors to invest additional capital in subsequent rounds, protecting their ownership stake from dilution and ensuring they can continue to participate in the company's growth.

Board representation. Investor representation on the company's board of directors ensures that investors have a direct influence on the strategic direction and decision-making processes of the company. By having a voice on the board, investors can better protect their interests and actively contribute to the company's success.

Liquidation preferences are just one of several investor protection mechanisms employed in venture capital deals. By understanding the context of liquidation preferences alongside other mechanisms such as anti-dilution provisions, protective provisions, preemptive rights, and board representation, both investors and founders can better navigate the complexities of venture capital investments and work together to create successful outcomes for all parties involved.

Conclusion

In conclusion, liquidation preferences are a crucial aspect of venture capital investments that directly impact the distribution of proceeds during a liquidity event. They serve as an essential tool for investor protection and risk management, influencing deal negotiations and term sheets. Understanding the different types of liquidation preferences, such as non-participating, participating, and capped participating preferred stock, is vital for both investors and founders.

It is essential to recognize the importance of carefully negotiating liquidation preferences to balance the interests of all parties and ensure successful investment outcomes. By examining various liquidation preference scenarios and considering other investor protection mechanisms like anti-dilution provisions, protective provisions, preemptive rights, and board representation, investors and founders can make more informed decisions when structuring and agreeing to liquidation preferences.