Anti-Dilution Provision: Definition, Formula, and VC Example

Learn how anti-dilution provisions work in VC term sheets, including full ratchet vs weighted average, broad vs narrow based formulas, and founder/investor tradeoffs.

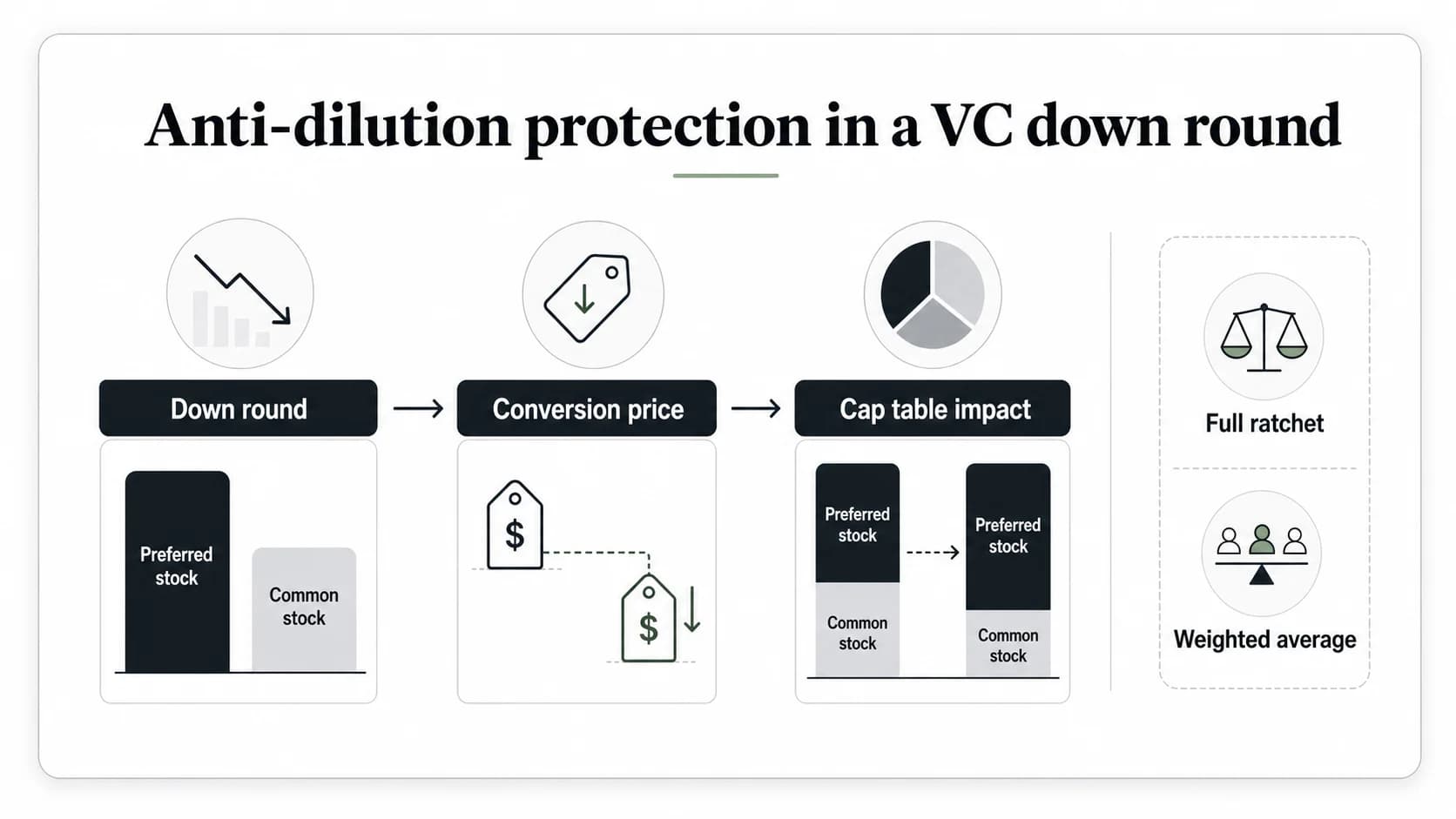

An anti-dilution provision is a financing term that protects preferred shareholders when a company later issues shares at a lower price. In a VC deal, it usually works by lowering the preferred stock's conversion price, which lets the protected investor convert into more common shares than before.

The term matters most in a down round. If a startup raised a Series A at $1.00 per share and later raises a new round at $0.50 per share, anti-dilution protection can shift some of the economic pain away from the earlier preferred investors and onto common shareholders, founders, employees, or other unprotected holders.

Anti-dilution does not stop all dilution. It does not guarantee a return. It is a conversion-price adjustment that changes who absorbs dilution when a later financing is priced below an earlier round.

What is an anti-dilution provision?

An anti-dilution provision is a clause in preferred-stock financing documents that adjusts the conversion terms of preferred shares after certain lower-priced issuances. In VC practice, it is protection for convertible preferred stock when new shares are issued below the earlier investor's price, with the main approaches being full ratchet and weighted average anti-dilution.

In startup financings, the clause usually appears in the term sheet and then in the company's charter or certificate of incorporation. The NVCA's model legal documents are a useful reference point because they are widely used starting documents for venture financings and include the core financing documents where these rights are negotiated.

The clause answers a practical question: if the company sells cheaper shares later, should earlier preferred holders get more common-stock conversion shares to compensate?

How anti-dilution works in a VC financing

Preferred stock usually converts into common stock at a conversion price. At issuance, that conversion price often equals the original purchase price. If an investor buys Series A preferred at $1.00 per share, the starting conversion price may also be $1.00, so each preferred share converts into one common share.

If the company later issues shares below $1.00, an anti-dilution clause may reduce the Series A conversion price. A lower conversion price means each Series A preferred share converts into more common shares.

The basic relationship is:

| Item | Meaning |

|---|---|

| Original issue price | The price the earlier preferred investor paid. |

| Conversion price | The price used to determine how many common shares preferred stock converts into. |

| Conversion ratio | Original issue price divided by current conversion price. |

| Down-round price | The lower price used in the later financing. |

| Adjustment | The clause lowers the conversion price, increasing the conversion ratio. |

For example, if a preferred share has a $1.00 original issue price and the conversion price is reduced to $0.80, the conversion ratio becomes 1.25x. One preferred share now converts into 1.25 common shares.

That extra common-share entitlement is the protection. The cost shows up as dilution elsewhere in the cap table.

Full ratchet vs weighted average anti-dilution

The two main types are full ratchet and weighted average. The difference is how aggressively the old conversion price is adjusted.

| Type | How it works | Who it favors | Typical effect |

|---|---|---|---|

| Full ratchet | Resets the old conversion price to the lower price paid in the new round. | Earlier preferred investors. | Strong protection for earlier investors; harsh dilution for common holders and potentially harder future financing. |

| Weighted average | Adjusts the old conversion price using both the lower price and the size of the new issuance. | A compromise between earlier investors and the company. | More moderate adjustment because a small down round does not fully reset the earlier price. |

Full ratchet is simple and severe. If the old conversion price is $1.00 and the company sells any covered shares at $0.50, full ratchet changes the old conversion price to $0.50. That kind of protection can make future funding rounds more difficult because it is costly to founders and later investors.

Weighted average is more common as a balanced concept because it considers both price and magnitude. A tiny issuance at a low price should not have the same effect as a major financing round at that price.

Broad-based vs narrow-based weighted average

Weighted average anti-dilution has two important variants: broad-based and narrow-based.

| Variant | What the formula base usually includes | Practical effect |

|---|---|---|

| Broad-based weighted average | A broad set of common-stock equivalents, often including common stock, preferred on an as-converted basis, options, and warrants depending on drafting. | Less protective for the earlier preferred investor because the base is larger. |

| Narrow-based weighted average | A smaller base, often focused on preferred or a narrower set of shares. | More protective for the earlier preferred investor because the base is smaller. |

The basic distinction is simple: broad-based includes more equity categories, while narrow-based excludes more categories such as options or warrants. The drafting details matter because a few words in the denominator can change the outcome.

For founders, broad-based weighted average is usually less painful than narrow-based weighted average. For investors, narrow-based gives stronger protection. For anyone modeling the round, the question is not just "weighted average or not?" It is "weighted average over what base?"

Anti-dilution formula and worked example

A common weighted average formula is:

New conversion price = old conversion price x (A + B) / (A + C)

| Variable | Meaning |

|---|---|

| A | Shares outstanding before the new financing, measured under the clause's chosen base. |

| B | Shares the company could have issued for the new money at the old conversion price. |

| C | Actual shares issued in the new lower-priced financing. |

Here is a simplified example.

| Input | Example |

|---|---|

| Series A original issue price | $1.00 |

| Series A old conversion price | $1.00 |

| Shares outstanding before down round | 10,000,000 |

| New money raised | $500,000 |

| New down-round price | $0.50 |

| Actual new shares issued | 1,000,000 |

Under full ratchet, the Series A conversion price resets from $1.00 to $0.50. The conversion ratio doubles. One million Series A preferred shares would convert into two million common shares.

Under weighted average, the adjustment is more moderate:

| Step | Calculation |

|---|---|

| A | 10,000,000 pre-financing shares |

| B | $500,000 new money divided by $1.00 old conversion price = 500,000 shares |

| C | $500,000 new money divided by $0.50 new price = 1,000,000 shares |

| New conversion price | $1.00 x (10,000,000 + 500,000) / (10,000,000 + 1,000,000) = about $0.9545 |

| New conversion ratio | $1.00 / $0.9545 = about 1.0476x |

The full ratchet gives the Series A investor a much larger adjustment. The weighted average clause still protects the investor, but it recognizes that the down round was only one million new shares against a larger existing base.

This is why anti-dilution review is cap-table work, not just legal vocabulary. You need the price, the number of shares, the pre-money share base, and the exact formula language.

What triggers an anti-dilution adjustment?

The usual trigger is a covered issuance below the protected series' conversion price. In plain English: the company sells equity or equity-linked securities cheaper than the earlier preferred round.

But the exceptions are just as important as the trigger. Term sheets often exclude routine or pre-agreed issuances so the company does not trigger anti-dilution every time it grants employee options or issues shares under an existing plan.

Common items to check:

| Clause item | Why it matters |

|---|---|

| Covered securities | Defines which shares, options, warrants, notes, SAFEs, or convertible securities can trigger the adjustment. |

| Excluded issuances | Often carves out option-plan grants, existing convertible securities, acquisition consideration, strategic partnerships, or lender warrants. |

| Series-specific protection | Determines whether one series is protected or all preferred holders share the protection. |

| Formula base | Determines whether the weighted average is broad-based or narrow-based. |

| Pay-to-play condition | May require investors to participate in the new round to keep some rights. |

| Waiver threshold | Defines who can waive or amend the protection. |

If you are reviewing a clause, do not stop at the label. "Weighted average" is not enough. The economic answer is in the definitions.

Who benefits and who gets diluted?

Anti-dilution protection benefits the protected preferred holders. It reduces the effect of a lower-priced issuance on their conversion economics.

The dilution has to go somewhere. It usually lands on some mix of:

- Founders and other common shareholders.

- Employees holding common stock or options.

- Unprotected preferred holders.

- New investors, if they must price around the overhang.

- The company, if the term makes the next financing harder to complete.

For founders, the hardest part is that anti-dilution can magnify an already difficult round. A down round lowers valuation. The anti-dilution adjustment then shifts more ownership to earlier preferred holders. If the company also needs to refresh the option pool, common shareholders can be hit from several directions at once.

For investors, the clause is downside protection. It helps preserve economic position if the company raises at a lower price. But it can also complicate the next financing, especially if later investors do not want old protections to consume too much of the post-money cap table.

How founders should negotiate anti-dilution

Founders rarely eliminate anti-dilution entirely in a priced preferred round. The practical negotiation is usually about scope and severity.

Use this checklist:

| Negotiation point | Founder-friendly direction | Investor-friendly direction |

|---|---|---|

| Type | Broad-based weighted average | Full ratchet or narrow-based weighted average |

| Trigger | Only meaningful below-price financing | Broad coverage of equity-linked issuances |

| Exclusions | Clear option-plan, acquisition, lender, and strategic exceptions | Fewer exceptions |

| Waiver | Flexible preferred vote or majority threshold | Series-specific veto rights |

| Pay-to-play | Investors must participate to keep enhanced rights | Protection survives even if investor does not participate |

| Duration | Narrower period or financing-linked protection | Continues until conversion or exit |

The founder goal is not to pretend dilution will never happen. It is to avoid a clause that makes a recovery financing impossible or transfers too much upside away from the team after a difficult round.

The investor goal is also rational. If an investor funded the company at a higher price, they may want protection against a lower-priced issuance that reprices the company before key milestones are reached.

How investors and candidates should read the clause

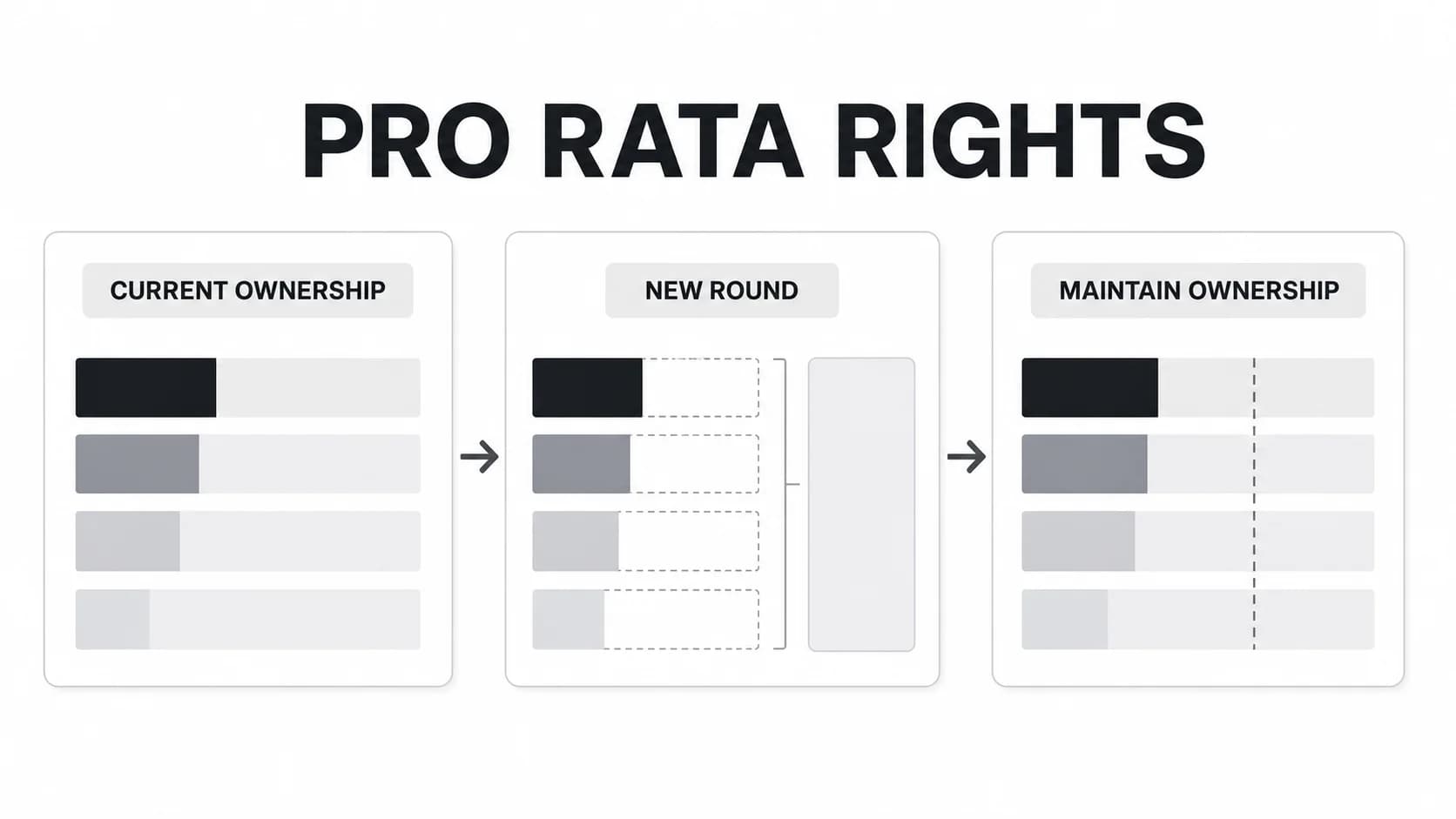

For investors, anti-dilution is part of the broader preferred-stock package. It should be read alongside liquidation preference, protective provisions, pro rata rights, and board/control terms.

For candidates preparing for VC analyst or associate roles, anti-dilution is a useful test of term-sheet fluency. In deal work, you should be able to answer:

- What event triggers the adjustment?

- Is the clause full ratchet or weighted average?

- If weighted average, what is included in the base?

- What issuances are excluded?

- Who can waive the provision?

- Does a pay-to-play provision affect the right?

- What does the adjustment do to the cap table in a downside case?

That is the level of understanding that matters in a financing memo or investment committee discussion. Definitions are table stakes; the cap-table consequence is the work.

If you are building that fluency for a investing role, browse open roles on the Venture Capital Careers job board. Term-sheet literacy is not just academic; it is part of how junior investors become useful in live financing processes.

Anti-dilution vs similar VC terms

Anti-dilution is easy to confuse with other investor-protection terms. The distinctions matter.

| Term | What it protects | How it differs |

|---|---|---|

| Anti-dilution provision | Conversion economics after lower-priced issuances. | Adjusts conversion price or conversion ratio; does not give the investor new cash. |

| Pro rata right | Ability to buy into future rounds to maintain ownership. | Investor must usually invest more money to maintain ownership. |

| Preemptive right | Right to buy new shares before outside buyers in certain issuances. | A purchase right, not a conversion-price adjustment. |

| Liquidation preference | Payout priority in a sale or liquidation event. | Affects exit proceeds, not future financing conversion price. |

| Protective provision | Approval right over major company actions. | A governance veto or consent right, not an economic formula. |

| SAFE valuation cap | Conversion pricing mechanic for a future equity round. | Applies to SAFE conversion; not the same as preferred-stock anti-dilution. |

| Convertible note discount | Discounted conversion into a future round. | A note-conversion term, not ongoing preferred-stock protection. |

For related financing mechanics, see VCC's guides to SAFE, convertible notes, and pre-money vs post-money SAFEs.

What about anti-dilution levy?

"Anti-dilution levy" is usually a fund-investing term, not a VC preferred-stock term. In fund contexts, it can refer to a charge used to protect existing fund investors from transaction costs when other investors enter or exit the fund.

That is a different intent from startup anti-dilution protection. If you are reading a VC term sheet, charter, or preferred-stock financing document, the relevant meaning is the conversion-price adjustment described above.

FAQs

How does anti-dilution work?

Anti-dilution works by adjusting the conversion price of protected preferred stock after a covered lower-priced issuance. A lower conversion price lets each preferred share convert into more common shares, reducing the impact of the down round on the protected investor.

What is an anti-dilution adjustment clause?

An anti-dilution adjustment clause is the detailed language that defines the trigger, formula, exclusions, waiver threshold, and resulting conversion-price adjustment. The label matters less than the specific drafting.

What is full ratchet anti-dilution?

Full ratchet anti-dilution resets the earlier preferred stock's conversion price to the new lower issuance price. It is highly protective for earlier investors and usually more dilutive to founders, employees, and common shareholders.

What is weighted average anti-dilution?

Weighted average anti-dilution adjusts the conversion price based on both the lower price and the size of the new issuance. It is usually less severe than full ratchet because a small low-priced issuance does not fully reset the earlier conversion price.

What is the difference between broad-based and narrow-based weighted average?

Broad-based weighted average uses a broader share base in the formula, which usually produces a smaller investor adjustment. Narrow-based weighted average uses a smaller base, which usually gives the protected investor more additional conversion shares.

Does anti-dilution protect founders?

Usually no. In VC term sheets, anti-dilution usually protects preferred investors. Founders can negotiate for broader bases, clearer exclusions, pay-to-play conditions, and waiver flexibility, but the right is typically investor-side protection.

Is anti-dilution the same as pro rata rights?

No. Anti-dilution adjusts conversion economics after a lower-priced issuance. Pro rata rights let an investor buy more shares in future rounds to maintain ownership, usually by investing additional capital.

Do SAFEs have anti-dilution provisions?

SAFEs usually have conversion mechanics such as valuation caps or discounts, not the same preferred-stock anti-dilution clause used after a priced equity round. Once SAFEs convert into preferred stock, the resulting preferred shares may have whatever anti-dilution rights are negotiated in that financing.