Pre-money SAFE vs. Post-money SAFE

How pre-money and post-money SAFEs differ, why the distinction changes ownership math, and what founders and investors should model before signing.

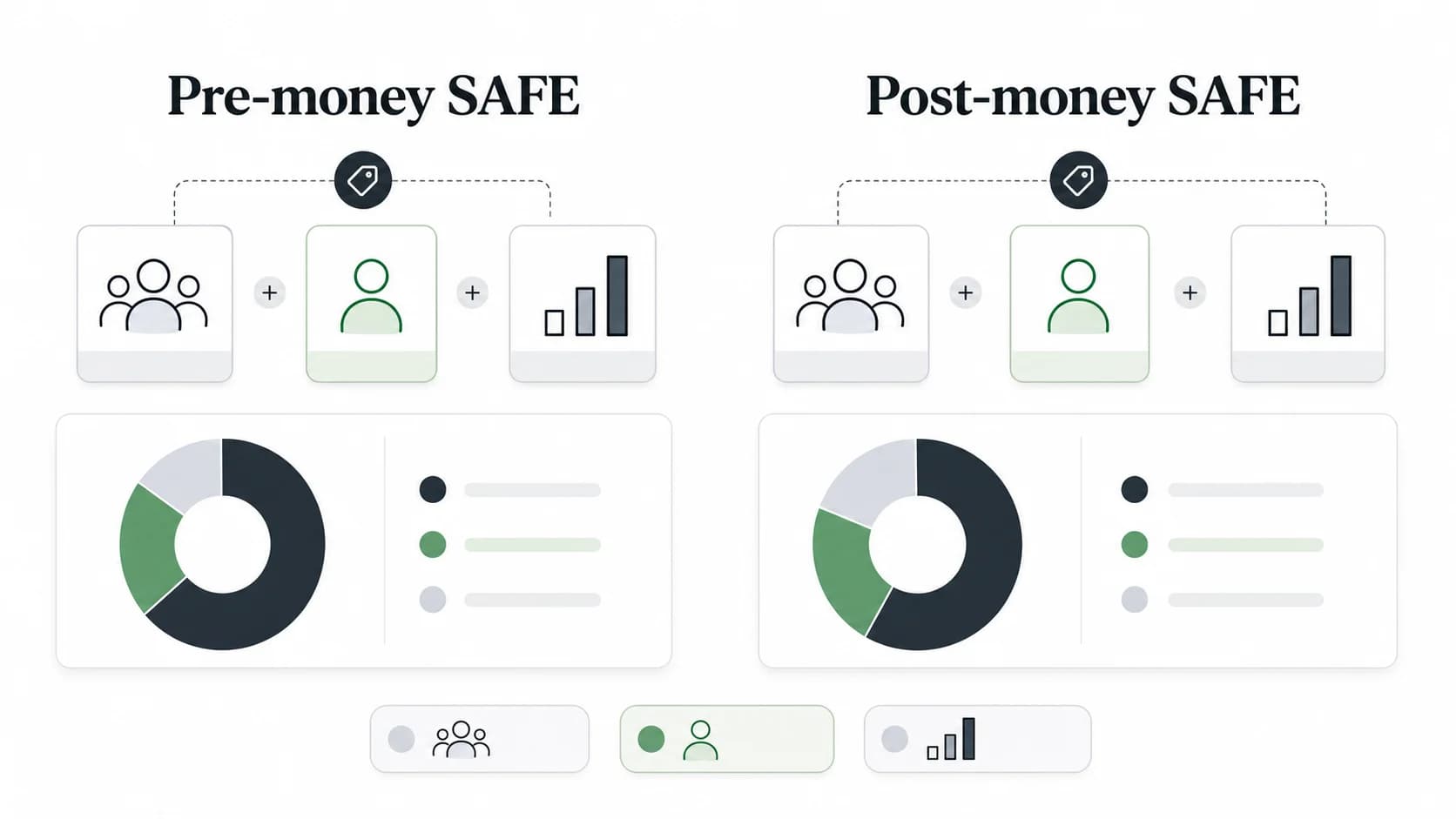

A pre-money SAFE and a post-money SAFE both let a startup raise money now and issue shares later, usually when a priced round closes. The difference is how the SAFE investor's ownership is calculated. A pre-money SAFE calculates conversion against the company's value before the SAFE money is counted. A post-money SAFE measures ownership after the SAFE money is counted, which makes the investor's implied ownership easier to estimate at signing.

That distinction sounds technical, but it changes the cap table. Founders, operators, and investors should not compare two SAFE caps until they know whether each cap is pre-money or post-money.

Quick comparison

| Question | Pre-money SAFE | Post-money SAFE |

|---|---|---|

| What does the valuation cap exclude or include? | Usually excludes the SAFE money from the valuation cap. | Includes the SAFE money in the ownership calculation for the SAFE round. |

| Is investor ownership clear at signing? | Less clear, especially if more SAFEs are issued before the priced round. | Clearer, because ownership is measured after the SAFE money is accounted for. |

| Who bears dilution from later SAFEs before the priced round? | Earlier SAFE investors can be diluted by later SAFE investors. | Founders and other pre-SAFE holders more directly absorb the dilution from the SAFE stack. |

| What is easier to model? | One SAFE can be simple; multiple SAFEs can become messy. | Multiple SAFEs are usually easier to model as a seed round. |

| Common use today | Older SAFE forms and some legacy financing docs. | YC's current standard SAFE forms for US companies are post-money. |

What a SAFE does before a priced round

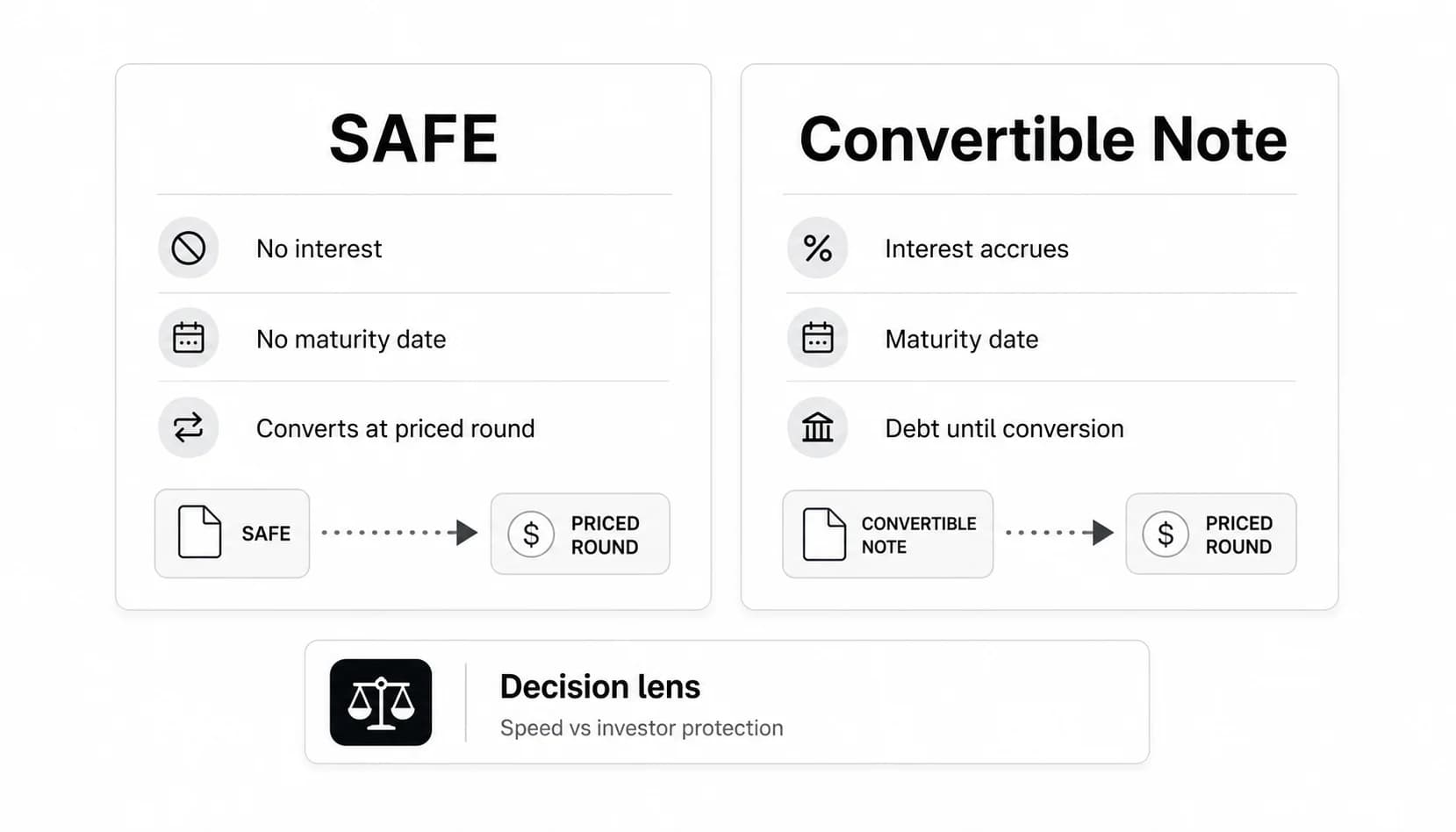

A SAFE is a simple agreement for future equity. The investor sends money now. The company does not issue priced preferred stock immediately. Instead, the SAFE converts into equity later, typically when the company raises a priced round such as a Series A.

YC introduced the SAFE as an alternative to convertible notes. In YC's original SAFE announcement, it described a SAFE as similar to a convertible note in economic purpose, but without debt features such as a maturity date or interest. If you need the broader instrument comparison, start with SAFE vs convertible note.

The SAFE usually has one or more conversion economics:

- Valuation cap: the maximum valuation used to price the SAFE investor's conversion.

- Discount: a percentage discount to the future priced round share price.

- MFN clause: a term that can let the SAFE holder adopt more favorable terms from later SAFEs.

- Pro rata side letter: a separate right to participate in later rounds and maintain ownership.

The pre-money vs post-money question is mostly about the valuation cap and ownership math.

What "pre-money" means in a SAFE

In regular financing language, pre-money valuation means the company's value before the new investment. Investopedia's pre-money and post-money overview explains the basic timing distinction: pre-money excludes the new money, while post-money includes it.

In a pre-money SAFE, the valuation cap is generally applied before the SAFE money is counted. That can make ownership uncertain until the priced round because the final share count depends on what else happens before conversion:

- How many SAFEs are issued.

- Whether those SAFEs have different caps or discounts.

- Whether the company increases the option pool before the priced round.

- Whether the next priced round has a lower price, higher price, or special conversion mechanics.

For a single SAFE, the math can look straightforward. For a stack of SAFEs, founders can end up surprised because each instrument is converting around the same future financing event.

What "post-money" means in a SAFE

In a post-money SAFE, the SAFE investor's ownership is measured after the SAFE money is accounted for, but before the new money in the priced round that triggers conversion. YC explains this distinction on YC's SAFE documents page, where it says the post-money SAFE was designed to make it possible to calculate how much ownership has been sold when the SAFE is signed.

That is the core advantage: cleaner ownership math.

If an investor puts in $250,000 on a $5 million post-money valuation cap, the investor is economically buying about 5% of the company on a post-money SAFE basis:

| Input | Amount |

|---|---|

| SAFE investment | $250,000 |

| Post-money valuation cap | $5,000,000 |

| Implied SAFE ownership | 5.0% |

That does not mean the investor will own exactly 5% forever. The investor can still be diluted by the next priced round, option pool changes, and later financing. It means the SAFE round itself is easier to understand at signing.

Simple example: $250,000 on a $5 million cap

Assume a founder raises $250,000 from one investor on a $5 million valuation cap.

With a post-money SAFE, the headline ownership is simple:

| Calculation | Result |

|---|---|

| $250,000 investment / $5,000,000 post-money cap | 5.0% |

The investor can look at the SAFE and say, before the next priced round, this SAFE represents about 5% on a post-money SAFE basis.

With a pre-money SAFE, the same $5 million cap does not communicate the same thing. If you treat the $5 million as pre-money, then the company is valued at $5 million before the $250,000 investment. The implied post-money value is $5.25 million:

| Calculation | Result |

|---|---|

| Pre-money cap | $5,000,000 |

| SAFE investment | $250,000 |

| Implied post-money value | $5,250,000 |

| $250,000 / $5,250,000 | 4.76% |

That difference looks small with one investor. It gets more important when several SAFEs are issued before the priced round.

What changes when you stack multiple SAFEs

Most SAFE surprises come from the stack, not the first check.

Assume the company raises $1 million total on post-money SAFEs, all at a $5 million post-money cap. The SAFE investors as a group are buying about 20% before the priced round:

| SAFE stack | Amount |

|---|---|

| Total SAFE money | $1,000,000 |

| Post-money valuation cap | $5,000,000 |

| Implied SAFE ownership before priced-round new money | 20.0% |

That is clear. It may or may not be acceptable, but the founder can see it before signing the last SAFE.

With pre-money SAFEs, later SAFEs can change the dilution picture for earlier SAFE holders and common shareholders. The final answer depends on the conversion formula, the future priced round, the option pool, and other securities. That is why a founder should model the whole seed round instead of thinking, "This investor is only putting in $100,000."

A useful rule: every new SAFE is not just cash in the bank. It is a claim on the future cap table.

Which is better for founders?

Neither structure is automatically better for founders. The founder-friendly answer depends on the valuation cap, total SAFE amount, and future financing plan.

Post-money SAFEs can be better for founders when clarity matters. You can see how much of the company you are selling before the priced round. That makes it easier to set a fundraising limit, explain the round internally, and avoid stacking too much dilution.

Pre-money SAFEs can feel easier early because the investor's ownership is less explicit at signing. That is not always a benefit. It can postpone the hard conversation until the priced round, when the conversion math is harder to renegotiate.

Founders should ask four questions before signing:

- How much total SAFE money do we expect to raise before a priced round?

- What ownership does the full SAFE stack imply, not just this one check?

- Will the option pool increase before or as part of the priced round?

- Do any investors have pro rata rights or side letters that affect future dilution?

If the answer is unclear, build a pro forma cap table before signing.

Which is better for investors?

Investors often prefer post-money SAFEs because they provide cleaner ownership expectations. If the investor writes a check at a post-money cap, the ownership math is visible without waiting to see how many later SAFEs the company issues.

That clarity matters when an investor is comparing opportunities across venture capital firms or building a seed portfolio. A $250,000 check at a $5 million post-money cap has a different ownership profile from a $250,000 check at a $5 million pre-money cap.

Investors still need to check the rest of the terms. A post-money SAFE does not solve every issue. The investor should understand:

- Whether the SAFE has a valuation cap, discount, or both.

- Whether there is an MFN clause.

- Whether pro rata rights are included in the SAFE or in a side letter.

- What happens in a sale before a priced equity round.

- How the company is thinking about the next priced round and option pool.

The valuation cap is important, but it is not the whole deal.

Terms to check before signing

Use this checklist before comparing SAFE offers or explaining a SAFE round to a board, investor, or candidate:

| Term | Why it matters |

|---|---|

| Pre-money or post-money | Determines whether the cap includes the SAFE money in ownership math. |

| Valuation cap | Sets the maximum conversion valuation for the SAFE investor. |

| Discount | Can give the investor a lower conversion price than new investors in the priced round. |

| Total SAFE amount | Determines how much of the company may be sold before the priced round. |

| Option pool treatment | Can move dilution between founders, SAFE holders, and new investors. |

| Pro rata rights | May let investors maintain ownership in future rounds. |

| MFN clause | May let earlier investors adopt better terms issued later. |

| Conversion event | Defines when the SAFE turns into shares or pays out. |

If you are reviewing term sheets, do not stop at the headline cap. Ask for the pro forma cap table.

How to read this on a cap table

A good SAFE model should show at least three views:

- Current ownership before SAFEs.

- Pro forma ownership after all SAFEs convert but before new priced-round money.

- Pro forma ownership after the priced round, including the new investor and any option pool refresh.

This matters for founders and operators because the practical question is not "What is the SAFE cap?" It is "What will everyone own after the next financing?"

It also matters for VC candidates and startup employees. If you are interviewing at a company that raised multiple SAFEs, the headline amount raised may not tell you how much dilution has already been promised. You do not need to ask for confidential investor documents, but you should understand that SAFEs can reshape the cap table when they convert.

FAQs

Why did YC move from pre-money to post-money SAFEs?

YC says its original SAFE was pre-money because SAFEs were initially used for smaller checks ahead of a priced round. As early-stage fundraising evolved into larger seed rounds, YC released the post-money SAFE in 2018 to make ownership sold through SAFEs easier to calculate.

Are YC SAFEs pre-money or post-money today?

YC's current public SAFE forms for US companies are post-money forms. The current documents include versions with a valuation cap, with a discount, and with an uncapped MFN structure.

Is a post-money SAFE more dilutive?

It can make dilution more visible, but the real answer depends on total SAFE dollars, valuation cap, option pool, and priced-round terms. Post-money SAFEs usually make it easier to see how much ownership the SAFE round is selling before the priced round.

Can a SAFE have both a valuation cap and a discount?

SAFE forms can vary. Some use a valuation cap, some use a discount, and some use other structures such as MFN. Read the actual document rather than assuming every SAFE has the same economics.

What is the biggest founder mistake with SAFEs?

The biggest mistake is modeling each SAFE in isolation. Model the full SAFE stack, the option pool, and the next priced round together. That is the only way to see the practical dilution.

Bottom line

Pre-money and post-money SAFEs are not just different labels. They answer the ownership question differently.

If you are a founder, compare SAFE terms by modeling the whole round. If you are an investor, confirm whether the cap is pre-money or post-money before comparing ownership. If you are learning venture financing, remember the practical rule: the SAFE's valuation cap is only useful when you know what money is counted inside it.