Venture Capital Method Valuation: Formula, Example, and Dilution Check

Use the VC method to backsolve a startup's post-money and pre-money value from exit value, target return, investment size, ownership, and dilution.

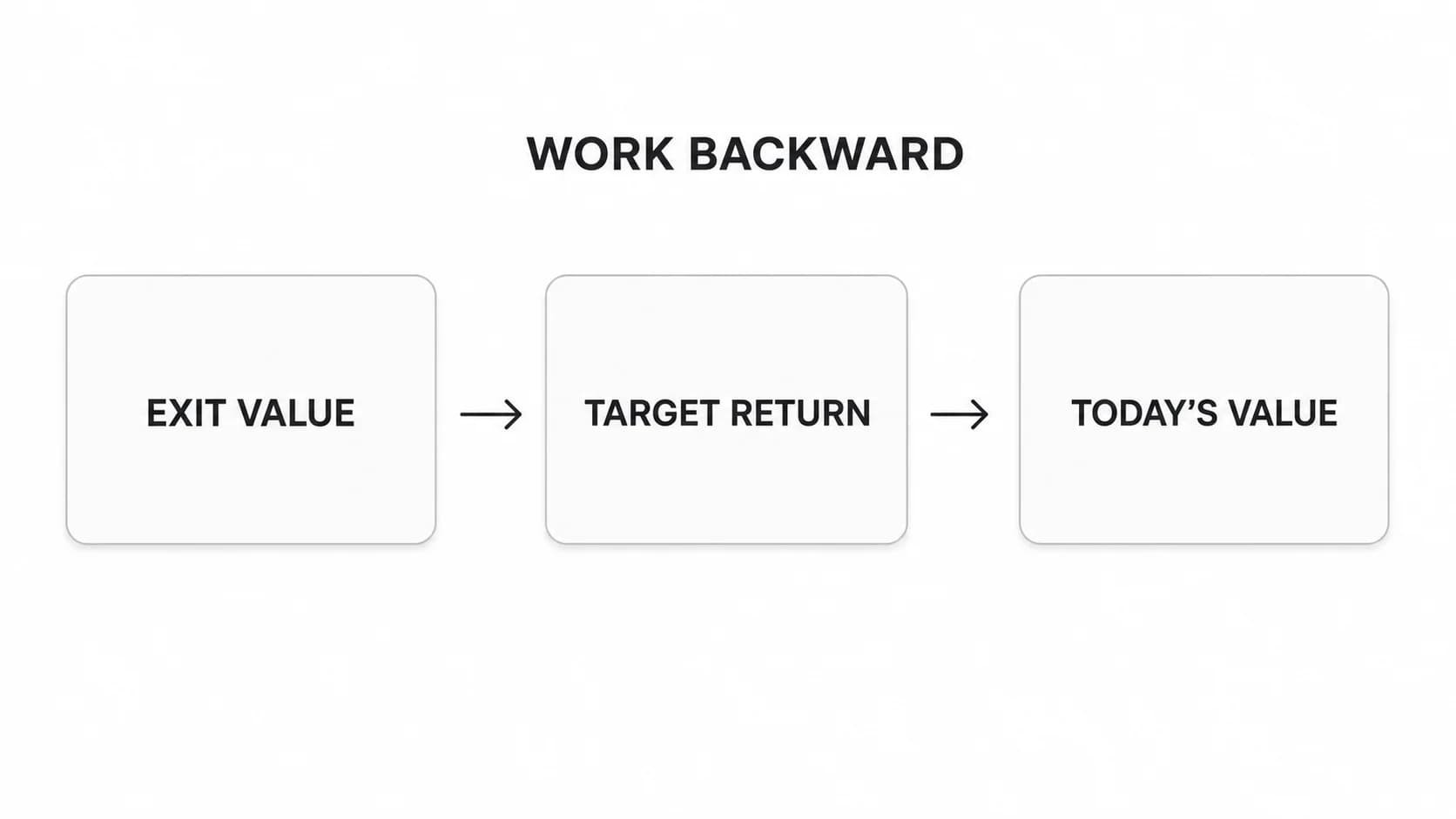

The venture capital method works backward from a possible exit to calculate what a startup can be worth today. Divide exit equity value by the investor target MOIC—or discount it by an annual target return—to get post-money value. Subtract the new investment for pre-money value, then test whether future dilution changes the ownership required at entry.

What the venture capital method is really solving

The venture capital method values a startup by working backward from a possible exit. Estimate what the company could be worth at exit, divide that value by the investor's target return, and you have an implied post-money value today. Subtract the new investment to get pre-money value.

The method is useful when near-term cash flow is too uncertain for a conventional DCF but an investor can still form a view on an exit metric, exit multiple, holding period, and required return.

It is best understood as an entry-price backsolve. It answers, “What can the investor pay today and still reach the target return if these assumptions hold?” It does not prove the company's intrinsic value, and it should not turn a speculative forecast into a precise fact.

Venture capital method formula

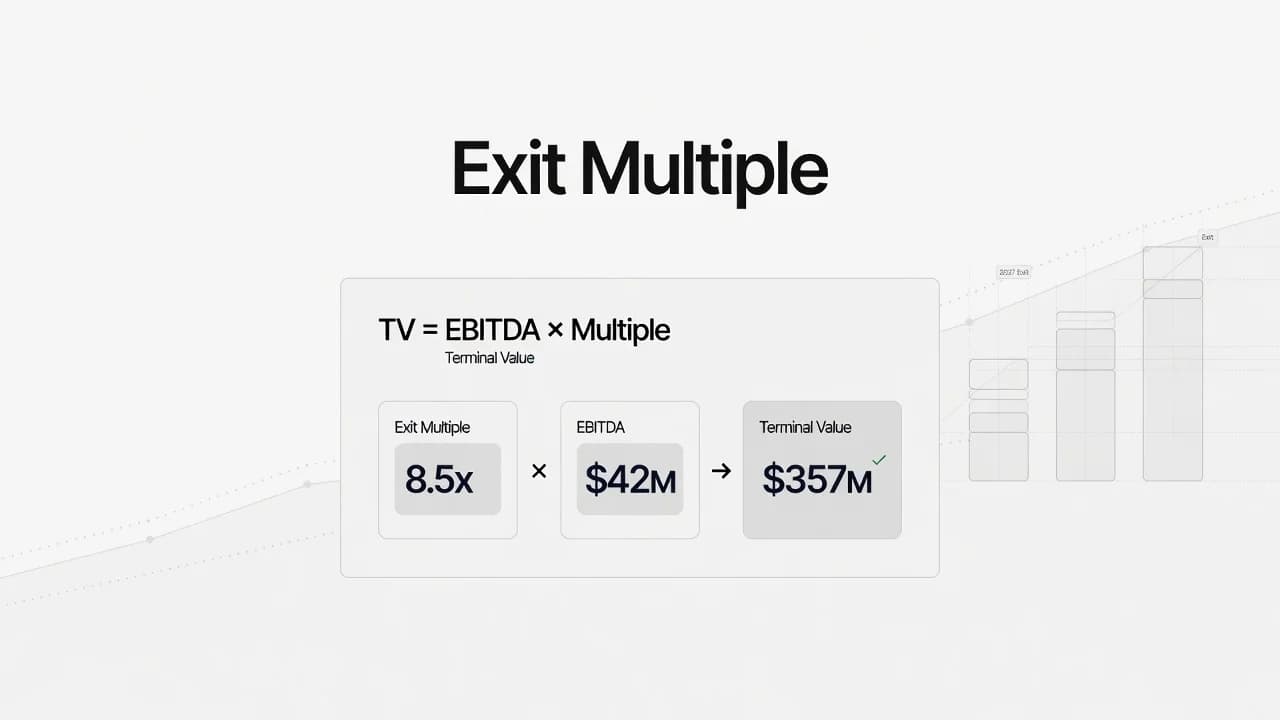

Start with an exit value. If the company is forecast to produce a financial metric in the exit year, apply an appropriate exit multiple:

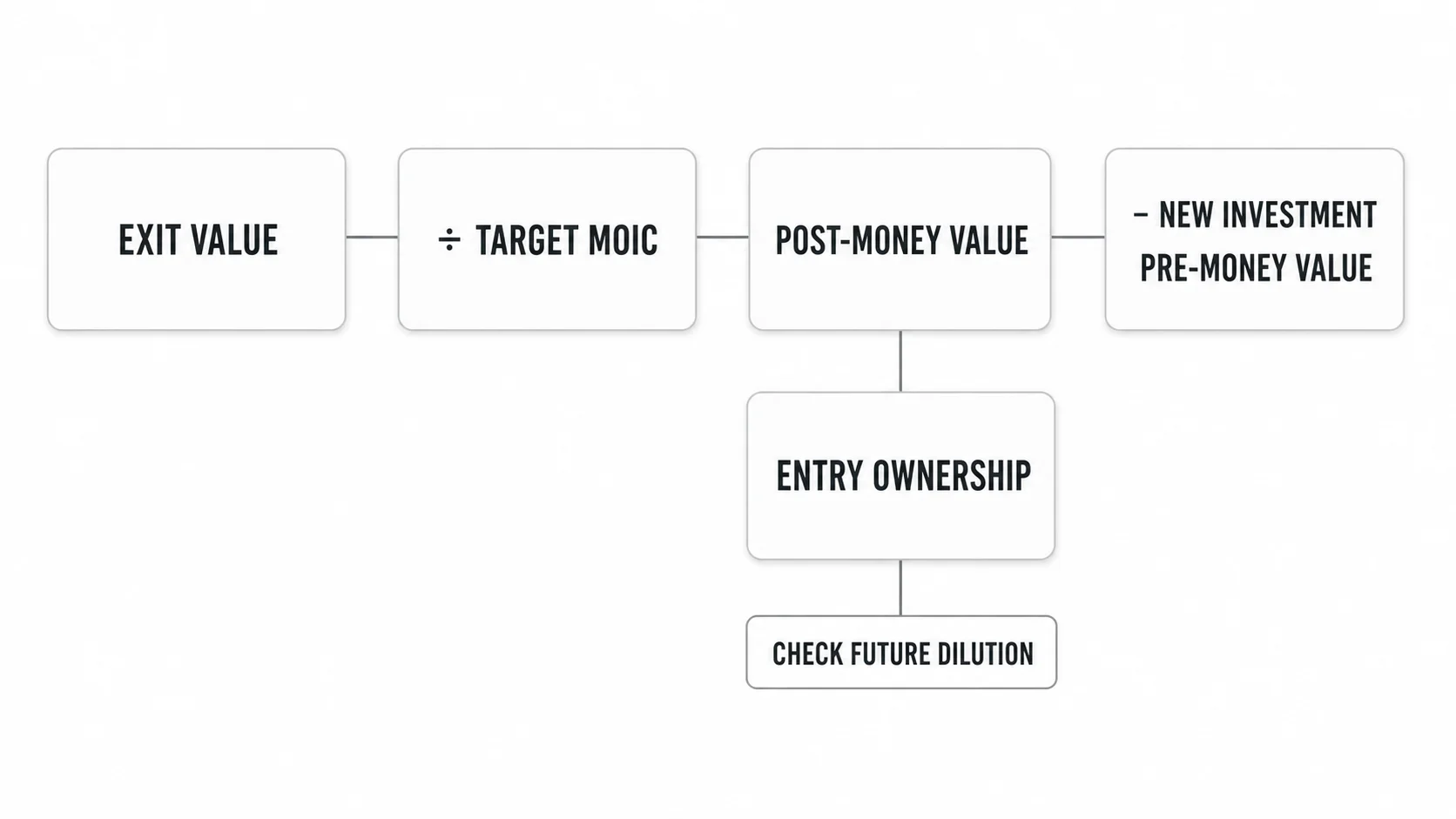

Exit equity value = Exit-year metric × Exit multiple − Net debt at exitFor a startup expected to have no net debt at exit, enterprise value and equity value may be the same. If debt or excess cash is material, bridge from enterprise value to equity value before calculating investor proceeds.

Next, discount the exit equity value using either a target multiple on invested capital (MOIC) or an annual target return. Do not mix the two.

Post-money value today = Exit equity value ÷ Target MOICIf the problem gives an annual target return instead:

Post-money value today = Exit equity value ÷ (1 + annual target return)^holding periodThen calculate the remaining outputs:

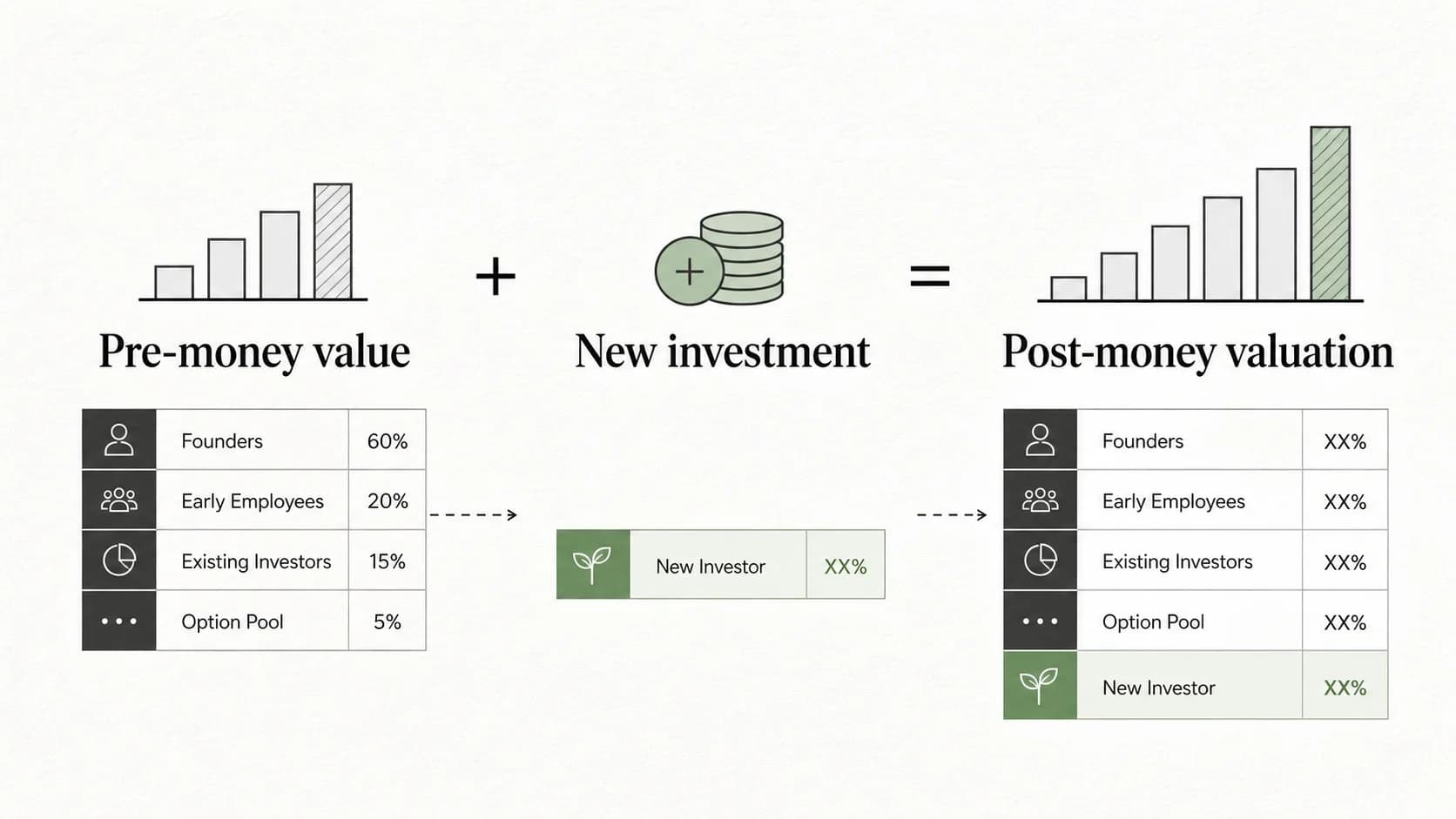

Pre-money value = Post-money value − New investment

Investor ownership at entry = New investment ÷ Post-money valueThe discounted result is post-money because it represents the value immediately after the modeled investment. Subtracting the investment produces pre-money value. This bridge matches the terminology in VCC's pre-money valuation and post-money valuation explainers.

| Input or output | Unit | Guardrail |

|---|---|---|

| Exit metric | dollars | Use the metric that matches the selected multiple. |

| Exit multiple | x | Revenue multiple applies to revenue; EBITDA multiple applies to EBITDA. |

| Target MOIC | x | Divide once; do not raise MOIC to the holding period. |

| Annual target return | percent per year | Compound it across the holding period. |

| Post-money value | dollars | Value immediately after new capital. |

| Pre-money value | dollars | Post-money value minus new investment. |

| Entry ownership | percent | New investment divided by post-money value. |

Worked example: from exit value to ownership

Assume a startup is raising $5 million. An investor builds the following illustrative case:

- Exit in year five.

- $40 million of revenue in the exit year.

- A 4x revenue exit multiple.

- No net debt at exit.

- An 8x target MOIC.

These are teaching assumptions, not market benchmarks. A real model should justify each input using the company's stage, sector, operating plan, comparable exits, and fund return requirements.

1. Estimate exit equity value

$40m exit revenue × 4x revenue multiple = $160m exit equity valueThe choice of exit multiple is usually the most visible assumption. VCC's exit multiple explainer covers how the metric and multiple must stay consistent.

2. Backsolve post-money value today

$160m exit equity value ÷ 8x target MOIC = $20m post-money value3. Calculate pre-money value

$20m post-money value − $5m investment = $15m pre-money value4. Calculate entry ownership

$5m investment ÷ $20m post-money value = 25% entry ownershipThe basic VC method therefore implies a $15 million pre-money value and 25% investor ownership.

Add future dilution before you trust the ownership result

The simple result assumes the investor keeps 25% until exit. That is rarely a safe default when the company may raise later rounds or expand its option pool.

Suppose the investment must produce 8x on $5 million. The investor needs $40 million of exit proceeds:

$5m investment × 8x target MOIC = $40m required exit proceedsAt a $160 million exit equity value, the investor must own 25% at exit:

$40m required exit proceeds ÷ $160m exit equity value = 25% required exit ownershipNow assume the investor expects 20% cumulative dilution between entry and exit. To finish with 25%, the investor must start with more:

Required entry ownership = 25% ÷ (1 − 20%) = 31.25%That entry ownership implies a lower valuation:

$5m investment ÷ 31.25% = $16m post-money value

$16m post-money value − $5m investment = $11m pre-money valueThe dilution adjustment moves the implied pre-money value from $15 million to $11 million. That is not a small modeling footnote; it is a different entry price.

Avoid double counting. If the target MOIC already incorporates a fully diluted ownership model or if the exit proceeds are calculated from a cap table that includes later rounds, do not apply a second generic dilution haircut. VCC's pro forma cap table guide is the better place to model round-by-round ownership precisely.

Sensitivity matters more than the headline valuation

The VC method is mechanically simple and assumption-heavy. A polished model should show how the answer changes when the exit value or required return changes.

Using the same $5 million investment and ignoring future dilution for the moment:

| Exit equity value | Target MOIC | Implied post-money | Implied pre-money | Entry ownership |

|---|---|---|---|---|

| $120m | 10x | $12m | $7m | 41.7% |

| $160m | 8x | $20m | $15m | 25.0% |

| $200m | 6x | $33.3m | $28.3m | 15.0% |

The table is not a set of comparable scenarios unless each exit value and target return is supported. Its job is to reveal which assumptions control the answer.

A useful base case should sit beside a downside and upside case. If the valuation only works under the highest exit multiple and fastest revenue plan, the model is signaling fragility rather than conviction.

How to choose the inputs

Exit metric and multiple

Choose a metric that a plausible buyer or public-market investor could use at exit. Revenue may fit a high-growth company that is not yet profitable. EBITDA may fit a later-stage business with durable margins. Never apply an EBITDA multiple to revenue.

Use current and relevant comparables cautiously. A high multiple can reflect superior growth, margins, retention, market position, or temporary market enthusiasm. Document why the selected company deserves that multiple.

Holding period

The holding period matters when the required return is annual. A five-year and eight-year path to the same exit value produce different present values.

MOIC alone does not encode time. An 8x outcome over five years and an 8x outcome over ten years have the same multiple but very different annual returns.

Target return

Use the return convention the investment problem actually provides. If the investment committee thinks in target MOIC, model MOIC. If the case specifies an annual return, compound the return over the holding period.

The target should reflect the fund's strategy, stage, risk, ownership model, and portfolio construction. There is no universal target return that belongs in every VC method model.

Future dilution

Estimate dilution from likely follow-on rounds and option-pool changes. The cleanest model works through the future cap table. A simplified retention factor is acceptable for a first pass only when the assumption is explicit.

Investment amount and option pool

Confirm whether the option-pool increase is included in the pre-money capitalization. A pre-money pool top-up can shift dilution toward existing holders and change the effective price even when the headline pre-money value does not change.

The best model keeps valuation, ownership, and capitalization connected instead of treating them as separate worksheets.

When to use the VC method—and when not to

Use the VC method when the investor can form a defensible view on exit value and required return, but near-term cash flows are too uncertain for a conventional DCF. It is especially useful for an investment-screening backsolve: “What entry price would make this outcome work?”

Do not use it as the only answer when the exit case is little more than a guess. The method can hide weak assumptions behind clean arithmetic.

| Method | Best fit | What it adds | Main weakness |

|---|---|---|---|

| Venture capital method | Startup with a plausible exit metric, holding period, and investor return target. | Direct link between entry price, ownership, and exit proceeds. | Highly sensitive to exit value and target return. |

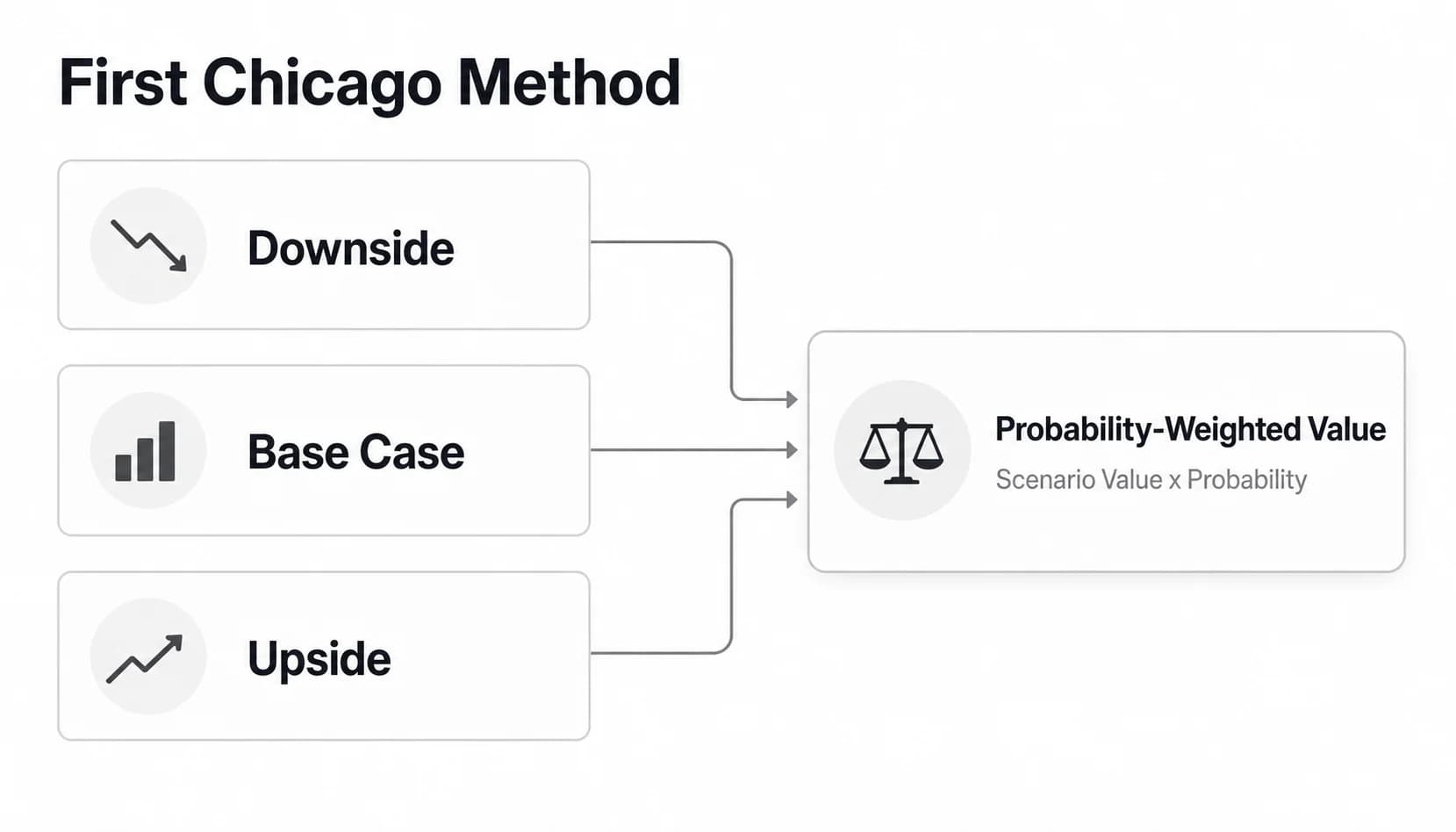

| First Chicago method | Startup with several credible operating outcomes. | Probability-weighted downside, base, and upside cases. | Scenario probabilities can be subjective. |

| DCF | Business with forecastable free cash flow. | Values the stream of cash flows rather than only the exit. | Unstable for early-stage companies with negative or uncertain cash flow. |

| Scorecard or Berkus method | Very early or pre-revenue company with limited financial evidence. | Forces a structured qualitative comparison. | Less connected to investor exit economics. |

These methods answer different questions. A strong investment case can use the VC method to test entry price, First Chicago to represent outcome dispersion, and a cap table to model dilution. Triangulation is more credible than averaging unrelated outputs without understanding why they differ.

Common mistakes in a VC method model

- Treating an enterprise value as equity value without subtracting net debt.

- Applying a revenue multiple to EBITDA or the reverse.

- Using annual return as if it were a simple MOIC.

- Calling the discounted result pre-money before subtracting the investment.

- Ignoring future dilution while assuming later funding rounds.

- Applying both a dilution haircut and a fully diluted cap-table model.

- Selecting only the scenario that supports the desired valuation.

- Presenting illustrative return targets as universal market standards.

How the VC method appears in interviews and investment memos

In a venture capital case study interview, the arithmetic is usually the easy part. The interviewer is testing whether you can structure uncertain inputs and explain what drives the answer.

A concise five-part response is stronger than jumping straight to a valuation:

1. Define the exit case. State the exit year, operating metric, multiple, and bridge from enterprise value to equity value. 2. State the return convention. Name the target MOIC or annual return and explain the holding period. 3. Backsolve valuation. Calculate post-money, subtract the investment for pre-money, and derive entry ownership. 4. Model dilution. Show the required exit ownership and how later rounds change entry ownership. 5. Stress-test the decision. Present downside, base, and upside cases and identify the assumptions that would change your recommendation.

In a venture capital investment memo, do not bury these inputs in a spreadsheet. Put the key assumptions and sensitivity next to the recommendation so an investment committee can see why the price works—or does not.

Candidates can strengthen this skill by researching a firm's stage, sectors, check sizes, and portfolio before practicing the model. Use the VCC companies directory to choose relevant firms, then adapt the exit metric and risk discussion to the strategy rather than rehearsing one generic answer.

Frequently asked questions

What is the venture capital method of valuation?

It is a backward-looking entry-price method. Estimate exit equity value, divide by the investor's target return to calculate today's post-money value, then subtract the new investment to get pre-money value.

Is the VC method result pre-money or post-money?

The exit value discounted by the target return is post-money value. Pre-money value equals that post-money value minus the new investment.

How do you calculate ownership in the VC method?

Entry ownership equals the new investment divided by post-money value. If later dilution is expected, gross up the required exit ownership to calculate the required entry ownership.

Should I use MOIC or IRR?

Use the convention provided by the investment case. Divide exit value by target MOIC, or discount it by the compounded annual target return across the holding period. Do not mix the formulas.

Does the VC method include dilution?

The basic formula does not automatically include future dilution. Add a transparent retention assumption or, preferably, model later rounds in a pro forma cap table.

What is the biggest weakness of the VC method?

Small changes in exit value, exit multiple, timing, and target return can move today's implied valuation substantially. A sensitivity table is therefore part of the answer, not an optional appendix.

The method is most useful when it sharpens a decision: which exit outcome must happen, which ownership is required, and which assumptions deserve diligence. Once you can explain those tradeoffs, browse open venture capital roles and look for teams where you can apply the work in sourcing, diligence, and investment analysis.