First Chicago Method for Startup Valuation

Learn how the First Chicago Method values startups with probability-weighted scenarios, plus a formula, worked example, assumptions checklist, and VC use cases.

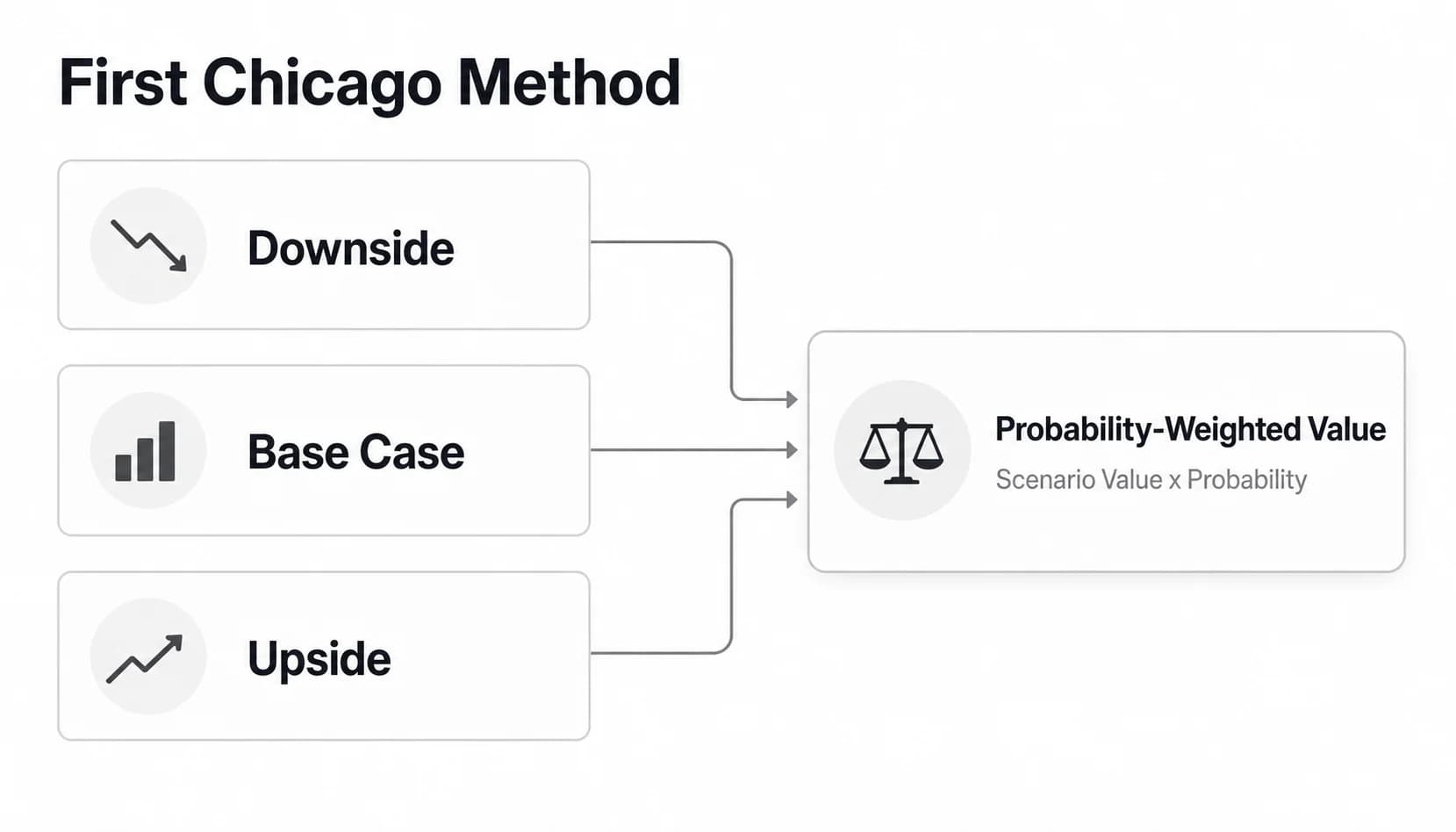

The First Chicago Method is a startup valuation approach that values a company across multiple scenarios, assigns a probability to each scenario, and adds the probability-weighted results together. It is used most often for startups and growth companies where a single-case DCF or comparable-company analysis is too brittle.

The basic formula is simple:

Probability-weighted value = (downside value x downside probability) + (base-case value x base-case probability) + (upside value x upside probability)

The work is not in the arithmetic. The work is in building scenarios that are distinct, defensible, and tied to how the company could actually perform. A weak First Chicago model is just three guesses with percentages attached. A useful one shows how valuation changes if the company misses, meets, or materially exceeds the investment case.

What is the First Chicago Method?

The First Chicago Method combines scenario analysis with valuation techniques such as discounted cash flow and exit-multiple analysis. A common definition describes it as a venture capital and private equity valuation approach that blends multiples-based valuation and DCF-style valuation for different possible outcomes (Wikipedia).

In practice, an investor usually builds three cases:

- Downside case: the company underperforms, exits at a lower value, or returns little capital.

- Base case: the company performs close to the investment team's expected plan.

- Upside case: the company reaches the stronger outcome that makes the investment attractive.

Each case gets its own forecast, exit value, discounting or return assumption, and probability. The final valuation is the weighted average of those cases.

That makes the method useful for venture capital because startup outcomes are not normally distributed. A company might fail, sell modestly, or become a fund-returning outcome. The First Chicago Method forces the investor to show those paths separately instead of hiding them inside one forecast.

First Chicago Method formula

The core formula is:

| Scenario | Scenario value | Probability | Weighted value |

|---|---|---|---|

| Downside | Downside valuation | Downside probability | Downside valuation x downside probability |

| Base case | Base-case valuation | Base-case probability | Base-case valuation x base-case probability |

| Upside | Upside valuation | Upside probability | Upside valuation x upside probability |

| Total | 100% | Probability-weighted valuation |

Wall Street Prep describes the method as a probability-weighted valuation using different cases and a probability assigned to each case (Wall Street Prep). That is the cleanest way to think about it: build the case values first, then weight them by likelihood.

The scenario value can come from different approaches. In venture work, it often comes from an exit multiple applied to forecast revenue or EBITDA at exit, then discounted back or tested against a required return. In other cases, it can come from a DCF within each scenario.

A simple First Chicago Method example

Assume a VC analyst is valuing a software startup over a five-year holding period. The analyst builds three exit cases:

| Scenario | Exit value today after discounting | Probability | Weighted value |

|---|---|---|---|

| Downside | $0 million | 30% | $0 million |

| Base case | $80 million | 50% | $40 million |

| Upside | $250 million | 20% | $50 million |

| Probability-weighted value | 100% | $90 million |

The First Chicago valuation is $90 million in this simplified example.

That number is not a magic answer. It is a decision anchor. If the company is raising at a $120 million pre-money valuation, the investor needs to believe either the upside case is more likely, the upside value is larger, the downside is less severe, or the deal has strategic reasons that the model does not capture.

If the investor owns 15% after the round, the same scenario logic can be applied to the investor's expected proceeds. That is where the method becomes especially useful in venture capital: it connects company valuation, ownership, dilution, exit outcomes, and fund-return math.

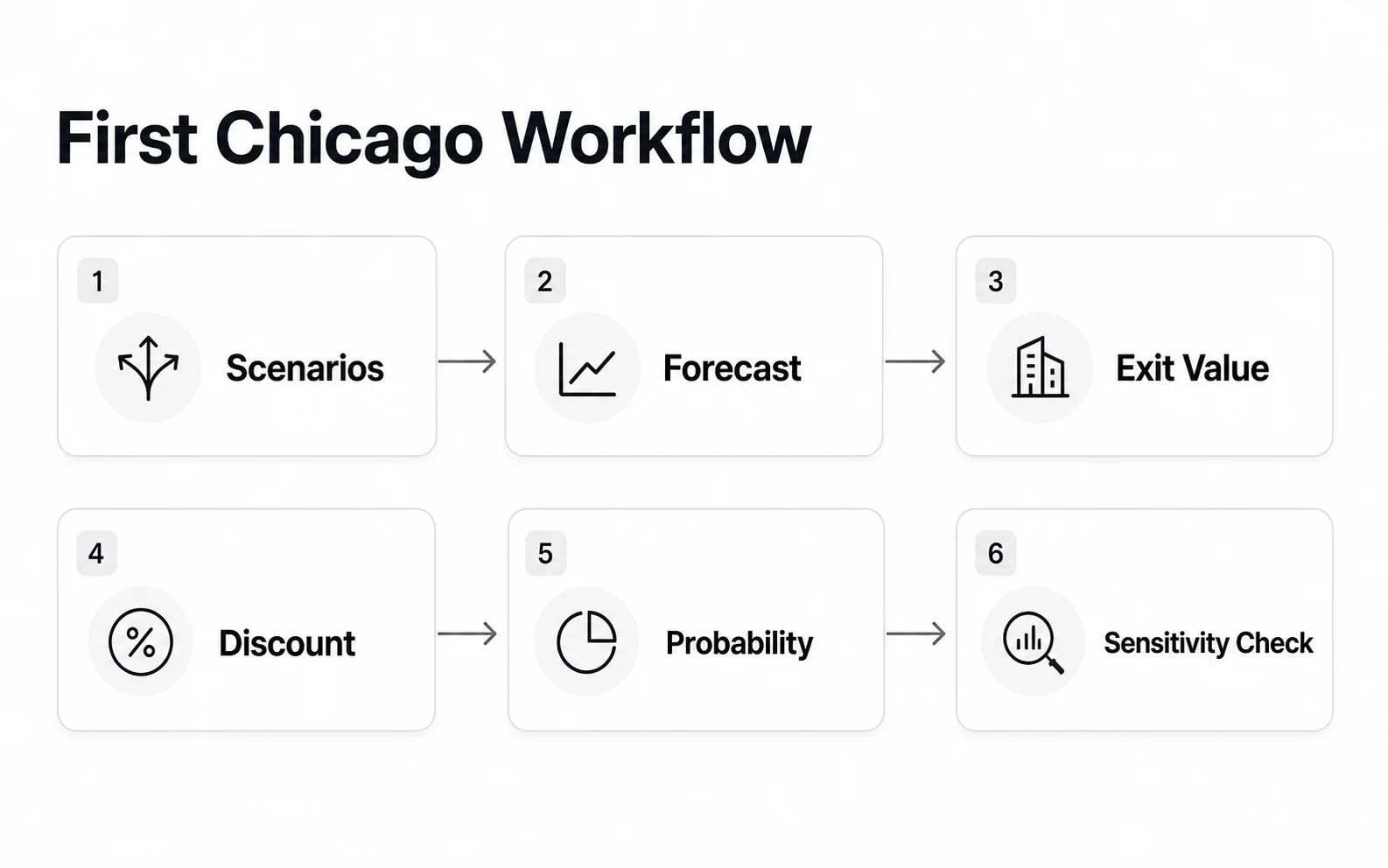

How to build a First Chicago model

Define the investment question

Start with the decision you are trying to support. Are you estimating a fair company value, testing whether a proposed round price works, or comparing multiple investments? The model should answer one decision, not every possible valuation question.

For a founder, the question might be: "What valuation range can I defend in a fundraising conversation?" For a VC analyst, it might be: "At this entry valuation, can this deal return enough capital under realistic scenarios?"

Build three genuinely different scenarios

The scenarios should differ because the business performs differently, not because the spreadsheet has cosmetic changes.

A useful downside case might include slower revenue growth, lower gross margin, a later exit, a lower exit multiple, or a financing outcome that dilutes existing holders. A base case should reflect the deal team's central underwriting view. An upside case should capture the outcome that makes the company matter to the fund.

If all three cases use nearly identical revenue growth, margin, and exit multiple assumptions, the model is not doing much work.

Forecast operating performance

For each scenario, forecast the operating metric that will drive value. In software, that might be ARR or revenue. In marketplace businesses, it might be GMV, take rate, contribution margin, and net revenue. In more mature companies, EBITDA or free cash flow may matter more.

Do not make the forecast more detailed than the evidence supports. A seed-stage company probably does not need a 12-tab operating model. A later-stage company with retention, cohorts, and sales productivity data can support more detail.

Estimate exit value

Most venture models use an exit value at the end of the holding period. That value often depends on an exit multiple applied to the relevant metric in each scenario.

For example:

- Downside: 3.0x revenue on $20 million of revenue = $60 million exit value.

- Base case: 6.0x revenue on $80 million of revenue = $480 million exit value.

- Upside: 10.0x revenue on $200 million of revenue = $2 billion exit value.

Those multiples should not be picked to make the answer work. They should reflect company quality, growth, margins, market conditions, comparable companies, and likely buyers.

Discount or return-test each scenario

The First Chicago Method is often described as combining market-oriented valuation and fundamental analysis. Venionaire's practitioner explanation frames the process around scenario forecasts, terminal value, required return, and probability weighting (Venionaire).

In a company-level valuation, you may discount each scenario's exit value back to today. In a venture-return model, you may calculate the investor's proceeds and compare the result with the fund's required return.

Be careful not to double-count risk. If the downside scenario already captures a high chance of failure, and the probabilities capture outcome risk, using an extremely high discount rate on every scenario can punish the same risk twice.

Assign probabilities

The probabilities must add to 100%. More importantly, they should reflect underwriting judgment, not spreadsheet convenience.

For early-stage venture, a high probability of the upside case is usually hard to defend. The upside may drive most of the expected value even when its probability is low. That is normal in venture. What matters is whether the case is plausible enough and large enough to justify the investment.

Sensitivity-check the answer

The output is only as good as the assumptions. After calculating the weighted value, test the variables that matter most:

- exit multiple;

- revenue or EBITDA at exit;

- holding period;

- required return or discount rate;

- ownership and dilution;

- downside recovery value;

- probability assigned to each case.

If a small change in one assumption changes the investment decision, that assumption deserves more diligence.

What each scenario should include

| Scenario | What it should represent | Useful assumptions |

|---|---|---|

| Downside | The company misses the plan, raises on difficult terms, exits modestly, or returns little capital | Slower growth, lower margins, delayed exit, lower multiple, more dilution, lower strategic interest |

| Base case | The company executes the central investment plan | Realistic growth, normal hiring, credible margin path, achievable exit multiple |

| Upside | The company becomes meaningfully larger or more valuable than the base case | Faster adoption, stronger retention, better pricing power, larger market capture, premium exit multiple |

The downside case should not always be zero. Sometimes a company has enough revenue, assets, or strategic value to support a modest exit. Other times, especially at the earliest stages, a zero or near-zero downside is realistic.

The upside case should not be fantasy. It should connect to a clear mechanism: a large market, unusually strong retention, category leadership, strategic scarcity, or operating leverage that can show up in financial results.

When to use the First Chicago Method

Use the First Chicago Method when a company has multiple plausible outcomes and enough information to model those outcomes.

It works best for:

- venture-backed startups with some evidence of traction;

- growth companies where several exit outcomes are plausible;

- investments where downside, base, and upside cases have materially different implications;

- VC case studies and investment memos where the reviewer wants to see assumptions, not just a single valuation number;

- situations where comparable-company analysis alone misses the company's option value.

It is especially useful when the same business could reasonably be worth very different amounts depending on execution. That is common in venture capital. A company can look expensive in the base case and still be attractive if the upside case is large enough, plausible enough, and tied to ownership economics.

When not to use it

The First Chicago Method is not always the right tool.

Do not lean on it when:

- the startup is too early for financial scenarios to mean much;

- the business has no credible path to revenue or exit value;

- the company is mature and stable enough for a standard DCF or market multiple to do the job;

- the scenarios are just optimistic, normal, and pessimistic labels with no real operating differences;

- the investor cannot defend the probabilities;

- ownership, dilution, or liquidation preferences matter but are left out of the model.

For very early pre-revenue companies, qualitative methods such as Berkus or Scorecard may be more appropriate as a starting point. For priced financing rounds, you also need to understand pre-money valuation, post-money valuation, and the cap table impact.

First Chicago Method vs other startup valuation methods

| Method | Best used for | What it emphasizes | Main limitation |

|---|---|---|---|

| First Chicago Method | Startups or growth companies with several plausible outcomes | Scenario-specific value x probability | Can look precise even when assumptions are weak |

| Venture capital method | VC return underwriting and target ownership | Exit value, target return, ownership | Often compresses risk into one exit case |

| DCF | Companies with forecastable cash flows | Present value of future cash flows | Fragile for early startups with uncertain cash flows |

| Comparable-company analysis | Companies with relevant public or transaction comps | Market multiples | Weak when comps are poor or growth profiles differ |

| Berkus Method | Very early pre-revenue startups | Qualitative risk factors | Not built for companies with meaningful revenue forecasts |

| Scorecard Method | Seed-stage relative valuation | Team, market, product, traction vs peers | Less useful for detailed return modeling |

The First Chicago Method is strongest when a company is past pure idea-stage uncertainty but not yet predictable enough for a single-case model. It lets the investor show the shape of the bet.

Common mistakes

Treating the weighted value as a precise answer

The result is an estimate, not a price tag. A $90 million output does not mean the company is worth exactly $90 million. It means the selected assumptions produce a weighted value of $90 million.

Using probabilities to justify a desired valuation

If the valuation only works after assigning a high probability to an aggressive upside case, the model is telling you something. Do not bury that signal.

Double-counting risk

Risk can appear in the operating cases, discount rate, exit multiple, and probabilities. If every layer is punitive, the model may be too conservative. If every layer is generous, it may be underwriting hope.

Ignoring dilution

Company value is not the same as investor proceeds. A VC fund cares about ownership after the round, future dilution, option pool expansion, follow-on requirements, and exit proceeds. A company-level First Chicago model should eventually connect back to ownership math.

Forgetting liquidation preferences

Preferred terms can change outcomes, especially in downside cases. If a company exits below the last round valuation, investor proceeds may not follow simple ownership percentages.

Building scenarios without diligence

The model should point to diligence questions. If the upside case depends on enterprise sales productivity, retention, pricing power, or strategic M&A interest, those assumptions should be tested in venture capital due diligence.

How VC candidates and analysts should use it

For candidates, the First Chicago Method is useful because it shows how you think under uncertainty. In a case study or investment memo, the exact valuation matters less than whether your assumptions are coherent.

Use it to show:

- you understand the difference between company valuation and investor returns;

- you can separate downside, base, and upside cases;

- you know which assumptions drive the model;

- you can explain why a deal works or does not work at a given entry price;

- you can connect valuation to ownership, dilution, and exit outcomes.

This is the kind of work that appears in VC analyst and associate roles: market sizing, company diligence, financial modeling, memo writing, and investment judgment. If you are preparing for those roles, pair this article with the VCC guides to VC analyst responsibilities, venture capital skills, and the broader venture capital career path.

You can also use the Venture Capital Careers job board and companies directory to see how firms describe valuation, diligence, investment memo, and portfolio-support responsibilities in live VC roles and firm profiles.

Frequently asked questions

Is the First Chicago Method the same as the venture capital method?

No. They are related, but not identical. The venture capital method often starts with a target exit value and required return to infer today's valuation or required ownership. The First Chicago Method builds multiple scenarios and probability-weights them.

Does the First Chicago Method work for pre-revenue startups?

Sometimes, but it is usually weaker for very early pre-revenue startups because the financial forecast may be too speculative. In that case, methods such as Berkus, Scorecard, or market-based seed benchmarks may be more useful as a starting point.

How many scenarios should a First Chicago model use?

Three is the standard structure: downside, base, and upside. More scenarios can be added if they represent genuinely different outcomes, but more cases do not automatically make the model better.

Which discount rate should you use?

Use a rate that matches the risk, stage, and investor return requirement, then test sensitivity. In venture work, many analysts focus less on a textbook WACC and more on whether the investor's ownership and exit proceeds can meet the fund's return threshold.

Is the result pre-money or post-money?

It depends on what you are valuing. If the model estimates the company before new financing, it can support a pre-money valuation. If it includes the new cash from a round, it may support a post-money valuation. Be explicit, because the distinction changes dilution and ownership.

What is the main limitation of the First Chicago Method?

The main limitation is assumption quality. The method can make uncertain outcomes look more scientific than they are. It is useful only when the scenarios, values, probabilities, and ownership assumptions are defensible.