Venture Capital Investment Memo: Template and Examples

Learn how to write a venture capital investment memo, including the core sections, examples, common mistakes, and a case-study-ready template.

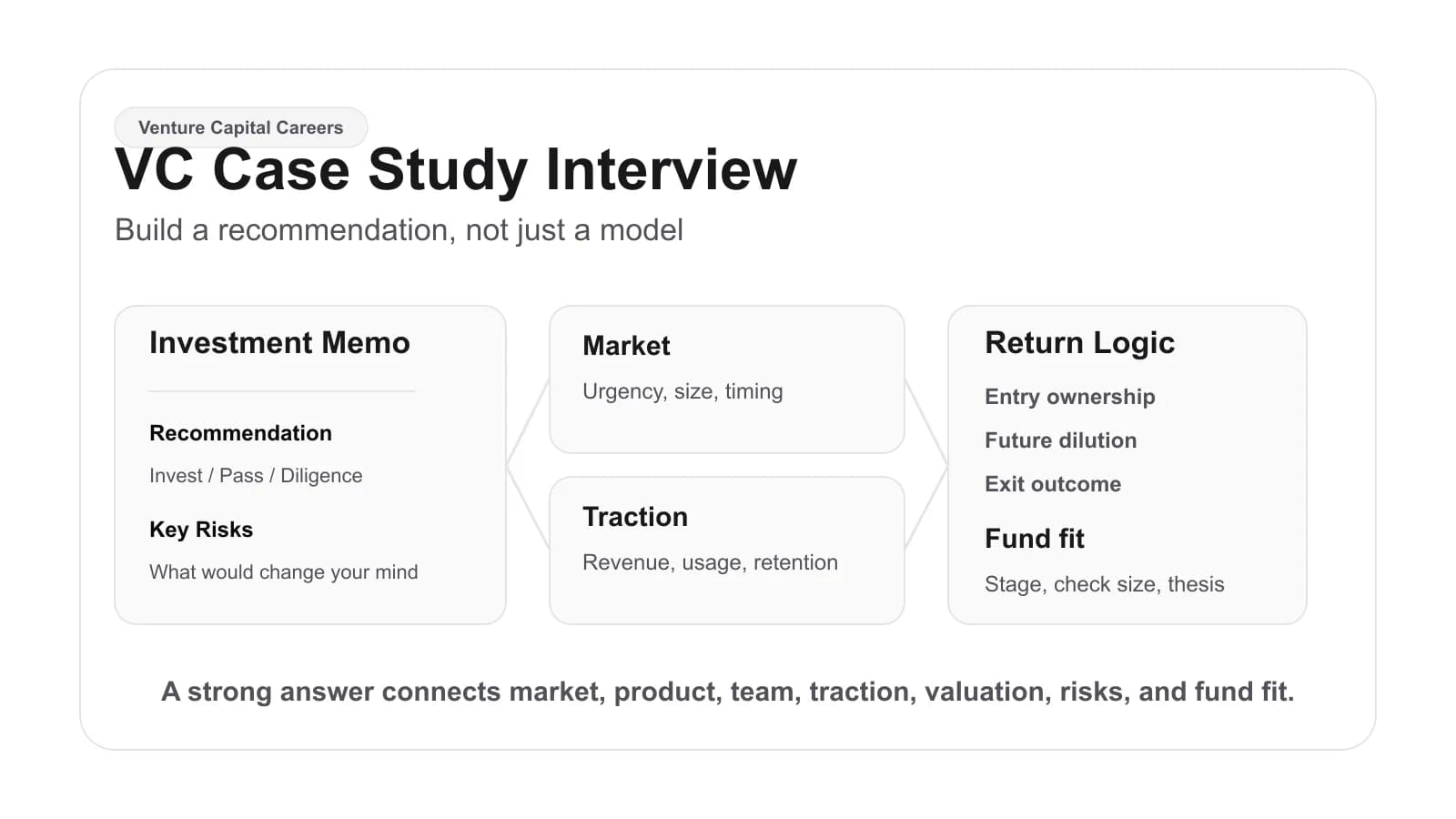

A venture capital investment memo is the written argument for why a fund should invest in, keep researching, or pass on a startup. It turns scattered diligence into a clear recommendation: what the company does, why the opportunity matters now, what evidence supports the case, what could break it, and why the decision fits the fund.

For candidates, the memo is often the most important part of a VC case-study interview. For analysts and associates, it is the artifact that helps a team decide whether a company deserves partner time, deeper diligence, or an investment committee discussion.

The mistake is treating the memo like a cleaned-up pitch deck summary. A good memo is not a transcript of what the founder said. It is a judgment document.

What is a venture capital investment memo?

A venture capital investment memo is a structured note that explains an investment opportunity and recommends an action. Depending on the fund, it may be called a deal memo, diligence memo, investment committee memo, IC memo, case-study memo, or recommendation memo.

The format changes by firm and stage, but the purpose is consistent: help investors decide what to do next.

| Memo type | Typical use | Main question |

|---|---|---|

| Sourcing note | Early screening after finding a company | Is this worth a first or second meeting? |

| Diligence memo | After calls, research, and data review | Is the opportunity strong enough to advance? |

| Investment committee memo | Before a formal partner decision | Should the fund invest, and on what terms? |

| Case-study memo | VC interview or take-home exercise | Can the candidate think like an investor? |

The memo should make the reader smarter and faster. If a partner reads it quickly, they should understand the company, the core thesis, the evidence, the risks, and the recommendation without needing to reconstruct your entire diligence process.

What a good VC memo has to prove

The best memos are not long because they are exhaustive. They are useful because they are selective.

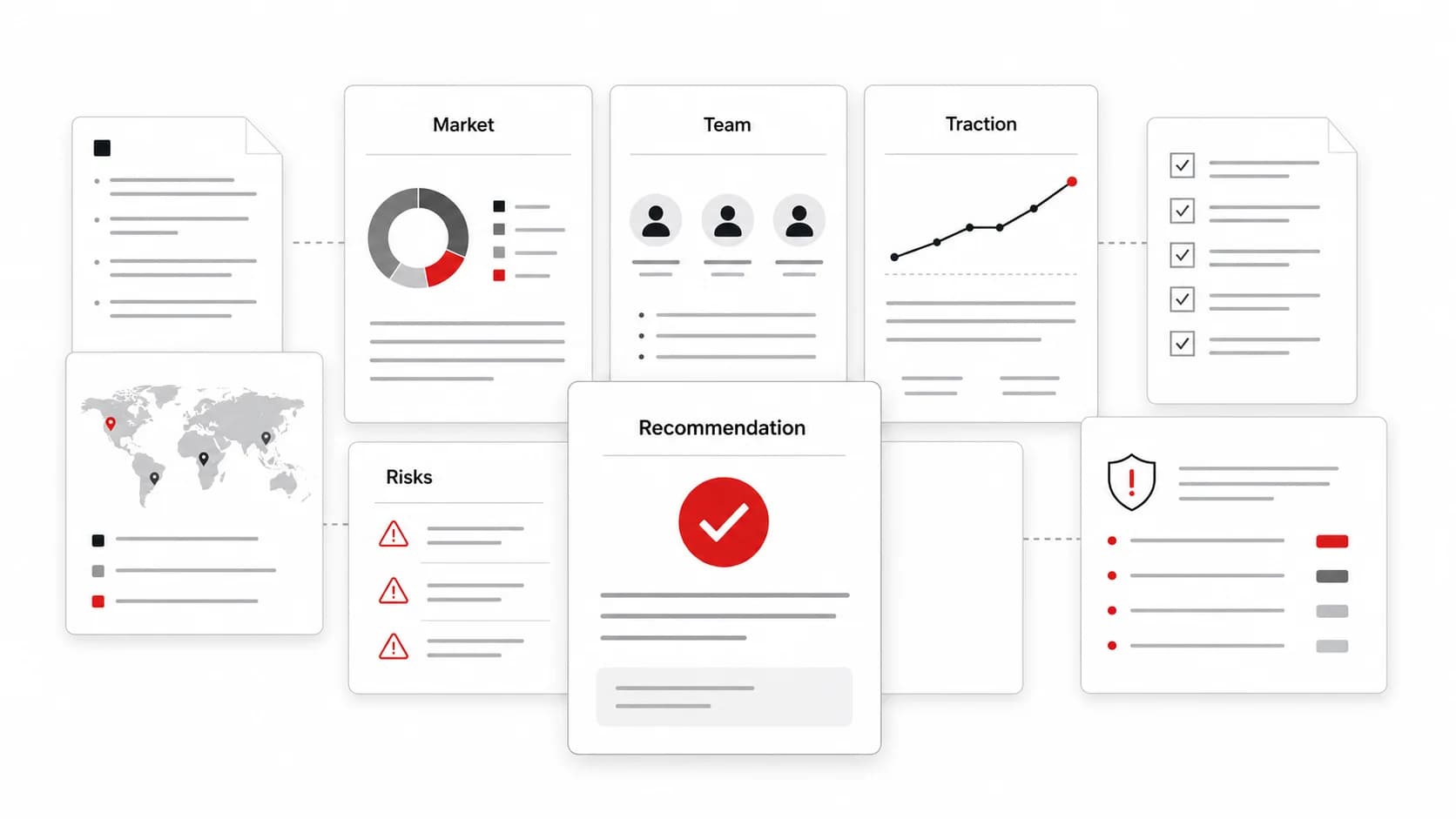

A strong VC memo usually proves six things:

| What to prove | What the reader needs to see |

|---|---|

| The opportunity is venture-scale | The market, business model, and outcome potential can support VC returns. |

| The timing is credible | There is a reason this company can win now, not just someday. |

| The company has a wedge | The product, distribution, data, community, technology, or workflow advantage is specific. |

| Evidence supports the thesis | Customer behavior, usage, revenue quality, pipeline, retention, founder insight, or market pull backs up the argument. |

| The risks are real | The memo names the biggest objections instead of hiding them. |

| The recommendation is clear | The reader knows whether you would invest, pass, or keep diligencing. |

The return case should state the expected exit path and holding-period assumption because the same MOIC produces different IRRs over different time horizons.

That last point matters. Many candidates write careful memos that never make a decision. In venture, judgment is the job. You can be cautious, but you still need a point of view.

VC investment memo template

Use this template when you need a practical structure for a startup investment memo or VC case-study memo.

| Section | Question it answers | What good looks like |

|---|---|---|

| One-sentence recommendation | What should we do? | Clear invest, pass, or continue diligence recommendation. |

| Company snapshot | What does the company do? | Plain-English description of product, customer, stage, geography, and round. |

| Investment thesis | Why could this be a meaningful company? | Specific argument about market change, customer pain, timing, and advantage. |

| Market | How big and attractive is the opportunity? | Bottom-up reasoning, segment clarity, and why the wedge can expand. |

| Product and customer pain | What problem is being solved? | Evidence that the product addresses a painful, frequent, or expensive problem. |

| Traction and evidence | What proves this is working? | Metrics, customer proof, usage, revenue quality, or pipeline signals appropriate to stage. |

| Team | Why this team? | Founder-market fit, speed, recruiting ability, technical edge, or earned insight. |

| Business model and economics | How can this become durable? | Pricing, margins, retention, payback, sales motion, or unit economics where relevant. |

| Deal context and fund fit | Why should this fund care? | Stage, check size, ownership, sector, portfolio fit, and follow-on logic. |

| Risks and mitigants | What could break the investment? | Ranked risks with evidence, not boilerplate. |

| Decision | What happens next? | Recommendation, open diligence questions, and next actions. |

How to write each memo section

Start with the recommendation

Open with the decision. Do not make the reader wait until the end to learn where you stand.

Good memo openers are direct:

- "Recommend advancing to partner diligence."

- "Recommend passing because the market wedge is too narrow for our fund."

- "Recommend a second founder call focused on retention, buyer urgency, and sales cycle length."

For a case-study interview, you do not need to pretend certainty. You can recommend "continue diligence" if the prompt gives limited data. But you should still explain what would change your mind.

Write a plain company snapshot

The company snapshot should be boring in the right way. It is not where you sell the deal. It is where you make the company legible.

Include:

- Company name and category.

- Product description.

- Customer or user.

- Stage and round, if known.

- Geography, if relevant.

- Business model.

- Current traction, if provided.

Weak: "Company X is revolutionizing healthcare operations with an AI-powered platform."

Stronger: "Company X sells workflow software to specialty clinics that automates prior authorization tasks for operations teams. The company is raising a seed round after signing five design partners and converting two to paid pilots."

The stronger version gives the reader something to evaluate.

Make the thesis specific

The thesis is the spine of the memo. It should explain why this company could matter.

A useful thesis usually combines four elements:

- Customer pain: What problem is urgent enough to create budget or behavior change?

- Market change: Why is this opportunity opening now?

- Company wedge: Why might this company win initial adoption?

- Expansion path: How could a narrow wedge become a larger company?

Weak: "This is a large market with strong tailwinds."

Stronger: "Specialty clinics are under pressure to reduce administrative labor while payer requirements keep increasing. If Company X can own prior authorization workflows, it can expand into adjacent revenue-cycle tasks and become the operating layer for small specialty practices."

The stronger version can be debated. That is the point.

Treat market size as a logic exercise

Market sections often go wrong because the writer drops in a top-down TAM number and moves on. VC investors care about market size, but they also care about market structure.

Ask:

- Who is the initial customer?

- How many of those customers exist?

- What do they spend today?

- What budget does the product replace or create?

- Why is the entry segment attractive?

- How does the company expand beyond the first wedge?

For early-stage companies, a crisp bottom-up market argument is usually more useful than a giant headline number. It shows whether the writer understands how the company actually grows.

Separate product description from customer pain

Do not only describe features. Explain the pain the product removes.

Weak: "The product has dashboards, automation, and integrations."

Stronger: "The product reduces manual follow-up for clinic operations teams that currently track prior authorization status across payer portals, spreadsheets, and phone calls."

Features matter, but only after the reader understands why the customer cares.

Match traction evidence to stage

A pre-seed company and a Series B company should not be evaluated with the same evidence standard.

| Stage | Useful evidence |

|---|---|

| Pre-seed | Founder insight, customer discovery, prototypes, design partners, early usage, credible wedge. |

| Seed | Paid pilots, early revenue, usage frequency, customer references, sales pipeline, retention signals. |

| Series A | Revenue growth, retention, gross margin, customer concentration, sales efficiency, team quality. |

| Growth | Cohort performance, unit economics, market expansion, competitive durability, exit path. |

In a case-study memo, be explicit about what the prompt does and does not prove. If you only have a pitch deck, say which evidence would need diligence before investing.

Explain why this team has an edge

"Strong team" is not analysis. Say why the founders are unusually suited to the opportunity.

Useful team signals include:

- Founder-market fit from direct operating experience.

- Technical depth in a hard problem.

- Customer access or distribution advantage.

- Evidence of speed and iteration.

- Recruiting ability.

- Prior founder or domain experience.

Avoid lazy credential summary. A famous employer can be a signal, but it is not the same as earned insight.

Keep business model analysis stage-appropriate

The business model section should answer how the company can become valuable, not just how it charges customers.

For a software company, look at pricing model, gross margin, retention, payback, expansion, and sales motion. For a marketplace, look at liquidity, take rate, supply acquisition, demand frequency, and disintermediation risk. For deep tech, look at commercialization path, capital intensity, milestones, and technical risk.

If the company is too early for clean metrics, say so. Then explain what would need to be true for the model to work.

Include deal context and fund fit

Many candidate memos ignore fund fit. Real investors cannot evaluate a deal in the abstract.

Ask:

- Does the stage match the fund?

- Can the fund write the required check?

- Is the ownership target realistic?

- Does the sector fit the fund's thesis?

- Would the fund be helpful to this company?

- Is there a portfolio conflict?

- What follow-on capital might be needed?

Use the Venture Capital Careers companies directory to study how different firms describe stage, sector, and portfolio focus. If you are recruiting, that same research helps you target funds where your memo examples will feel relevant.

Rank risks instead of listing generic concerns

Every startup has risks. The memo should identify the risks that matter most for this specific company.

Weak risk section:

- Competition.

- Execution.

- Hiring.

- Market adoption.

Stronger risk section:

| Risk | Why it matters | What to diligence |

|---|---|---|

| Buyer urgency | Clinics may agree the problem exists but delay purchase because budgets are constrained. | Conversion from pilot to paid, budget owner, sales cycle, lost-deal reasons. |

| Workflow depth | A narrow automation feature may not support a venture-scale platform. | Product roadmap, adjacent workflows, customer willingness to consolidate tools. |

| Data access | Integrations with payer portals may be brittle or hard to maintain. | Technical architecture, integration failure rates, support burden. |

The stronger version helps the team decide what to ask next.

Weak versus stronger memo examples

Use the "evidence, not adjectives" rule. If a sentence relies on adjectives, rewrite it around proof.

| Weak framing | Stronger framing |

|---|---|

| "The team is exceptional." | "The founders spent six years managing revenue-cycle operations at specialty clinics and have direct access to the first 20 design partners." |

| "The market is massive." | "The initial wedge is 8,000 specialty clinics with high administrative labor costs; expansion could move into adjacent revenue-cycle workflows after prior authorization." |

| "The product is highly differentiated." | "The product's initial differentiation is workflow depth inside payer-specific prior authorization tasks, not a generic AI assistant." |

| "Competition is a risk." | "The main risk is that incumbents add lightweight automation before Company X proves enough workflow depth to become the system of record." |

This is the difference between sounding excited and sounding like an investor.

How to use a memo in a VC case-study interview

In a VC case-study interview, the memo is less about being "right" and more about showing how you think.

Interviewers are usually testing whether you can:

- Structure ambiguous information.

- Identify the most important diligence questions.

- Distinguish evidence from assertion.

- Understand market and fund fit.

- Make a recommendation with incomplete data.

- Defend your view when challenged.

Pair the memo with the venture capital case study interview guide before you practice. Then use the venture capital interview questions guide to prepare for the follow-up discussion.

When you present the memo, lead with your recommendation and the two or three reasons that matter most. Do not walk through every section in order unless asked. Partners and principals will interrupt. That is how investment discussions work.

Common mistakes in VC investment memos

Summarizing the pitch deck. A memo should evaluate the company, not repackage founder materials.

Hiding the recommendation. If the decision is buried, the memo feels like notes instead of judgment.

Using market size without a wedge. A large market does not matter if the company has no credible entry point.

Writing generic risks. Competition, execution, and hiring are always risks. Name the specific version that could break this company.

Overweighting model precision. Financial analysis matters, especially at later stages, but false precision can distract from customer pull, timing, and market structure.

Ignoring fund fit. A good company can still be a poor fit for a particular fund's stage, ownership target, sector, or check size.

Failing to distinguish knowns from unknowns. The memo should make clear what is proven, what is assumed, and what requires diligence.

Final VC memo checklist

Before you send or present the memo, ask:

- Is the recommendation clear in the first few lines?

- Can the reader explain what the company does after one paragraph?

- Does the thesis say why this company could win now?

- Is the market argument bottom-up enough to be credible?

- Does the memo include real evidence, not just adjectives?

- Are the top risks specific and ranked?

- Does the decision fit the fund?

- Are the next diligence questions obvious?

- Could you defend the memo out loud in five minutes?

If the answer to any of these is no, tighten the memo before adding more length.

FAQ

How long should a VC investment memo be?

It depends on the use case. A sourcing memo might be one page. A case-study memo is often two to five pages. A formal investment committee memo can be much longer because it includes deeper diligence, financial analysis, references, and deal terms. For interviews, clarity matters more than length.

What is the difference between an investment memo and an investment thesis?

An investment thesis is the core argument for why an opportunity is attractive. An investment memo is the full decision document that includes the thesis plus company context, market analysis, evidence, risks, deal fit, and recommendation.

Do VC analysts write investment memos?

Yes, analysts and associates often write sourcing notes, diligence memos, market maps, and case-study memos. At some funds, junior investors draft large parts of the investment committee memo with input from principals and partners.

Should a VC memo ever recommend passing?

Yes. A pass recommendation can be strong if it is well reasoned. In interviews, a thoughtful pass can be better than a weak invest recommendation if the evidence does not support venture-scale returns or fund fit.

What should candidates include in a VC case-study memo?

Include a clear recommendation, company snapshot, thesis, market view, product/customer pain, traction evidence, team assessment, risks, and next diligence questions. Keep it concise enough that you can defend the key points in conversation.

Turn the memo into a recruiting asset

The best memo is not just a writing exercise. It shows that you can think like a junior investor: find the important questions, weigh imperfect evidence, and make a decision.

If you are using memos to break into VC, build a target list with the Venture Capital Careers companies directory, study open investment roles on the VC job board, and use your memo practice alongside your VC resume and interview prep. A sharp memo gives you something more useful to discuss than generic interest in startups.