Venture Capital Investment Committee: Process, Roles, and Decision Criteria

Learn what a venture capital investment committee does, who participates, how the IC process works, and what candidates and founders should expect.

A venture capital investment committee is the group inside a VC firm that decides whether the fund should make an investment. The deal team may source the company, run diligence, build the investment memo, and recommend a term sheet, but the committee is where the firm tests the case before committing capital.

For candidates, the investment committee process explains why VC interviews often emphasize judgment, memo writing, market sizing, risk framing, and objection handling. For founders, it explains why a partner can be excited about the company while still needing to win internal approval. For funds, it is one of the main places where investment discipline, speed, and partnership culture show up.

What a VC investment committee does

A VC investment committee, often shortened to IC, exists to decide whether a proposed investment fits the fund. It usually reviews the opportunity, the investment thesis, diligence findings, proposed terms, portfolio fit, and major risks before approving, rejecting, or sending the deal team back for more work.

The committee is different from the deal team. The deal team owns the work of building conviction. The committee owns the final decision or final recommendation, depending on the fund's governance model.

Common IC responsibilities include:

- Testing whether the company fits the fund's stage, sector, check size, ownership target, and return profile.

- Reviewing the investment memo, diligence findings, and proposed terms.

- Asking the deal sponsor to defend the upside case and the most important risks.

- Comparing the opportunity with the fund's existing portfolio and reserves plan.

- Deciding whether to approve the investment, pass, delay, or approve only with changed terms.

The best committees do not exist only to slow deals down. They create a structured moment where the firm can challenge assumptions before the fund wires money.

Who sits on the investment committee

Investment committee composition varies by firm size and strategy. A small seed fund may have two or three general partners who make decisions together. A larger multi-stage firm may have a more formal committee with senior partners, functional specialists, and observers.

Typical participants include:

| Participant | Role in the process | Usually votes? |

|---|---|---|

| Deal sponsor | Champions the company and presents the recommendation | often |

| General partners | Test the investment case and approve capital allocation | yes |

| Senior investment partners | Challenge assumptions and compare the deal with fund strategy | often |

| Analysts and associates | Prepare research, diligence, models, market maps, and memo sections | usually no |

| Advisors or operating experts | Add sector, technical, talent, or go-to-market perspective | sometimes |

| Founder or management team | May present in some processes, especially later-stage rounds | no |

The important distinction is voice versus vote. Junior investors may influence the decision through strong diligence and clear writing even if they do not have voting authority. Candidates should understand that analyst and associate work often shapes the IC conversation before the meeting starts.

How the IC process works

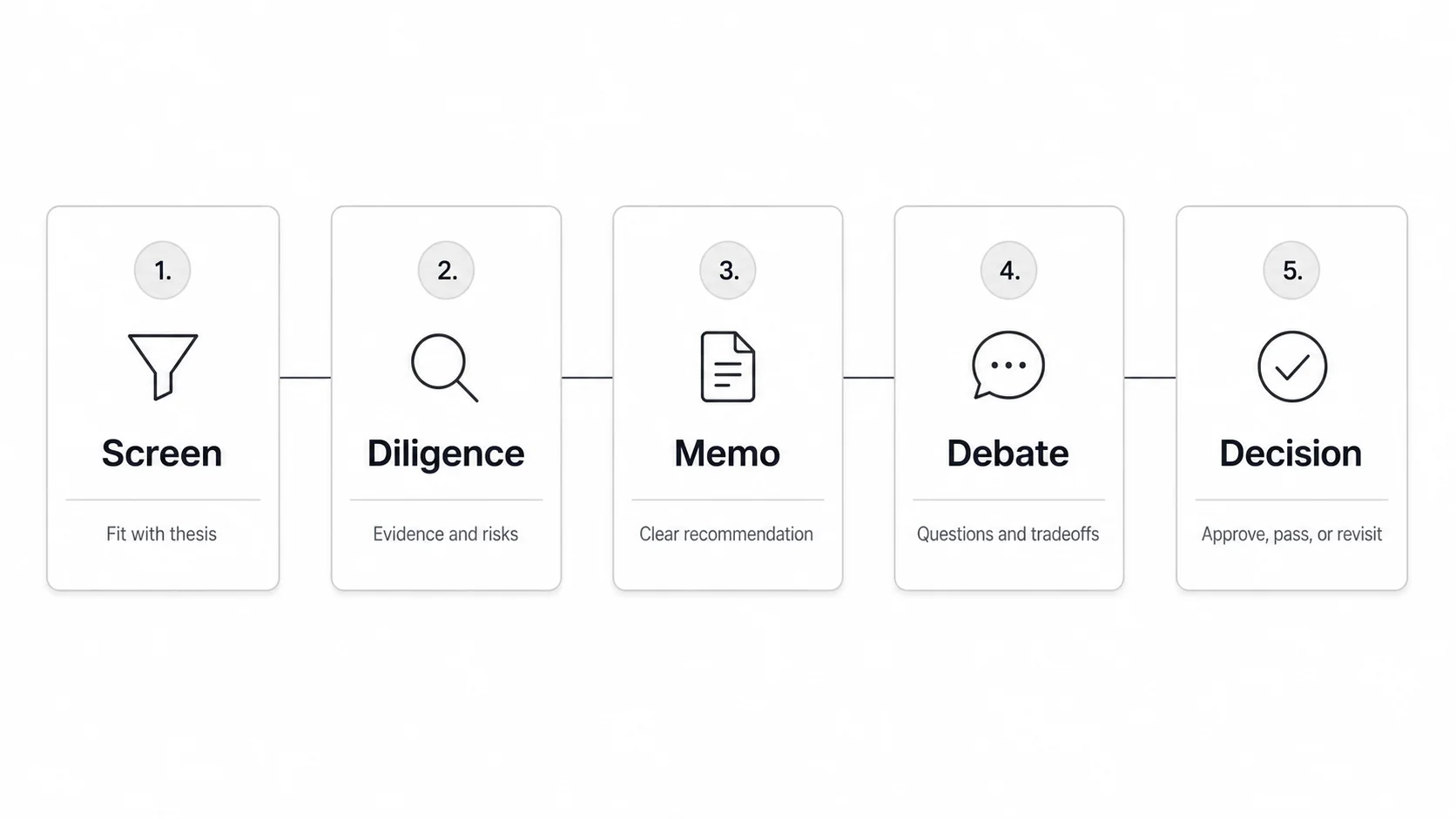

Most venture investment committee processes follow the same basic arc: screen the company, run diligence, write the memo, debate the opportunity, and decide what happens next.

1. Screen

The deal team first decides whether the company is worth deeper work. The screen usually tests basic fit: stage, sector, geography, check size, ownership target, founder quality, market scale, and whether the company fits the fund's thesis.

2. Diligence

If the company passes the screen, the deal team gathers evidence. That can include customer calls, market research, competitive mapping, product review, founder references, financial analysis, technical diligence, legal review, and portfolio conflict checks.

3. Memo

The investment memo turns diligence into a decision document. A good memo does not bury the committee in information. It states the recommendation, explains why the upside could matter, names the key risks, and shows what would need to be true for the investment to work.

For a deeper template, use the venture capital investment memo guide.

4. Debate

The committee meeting is where partners pressure-test the case. Questions usually focus on the market, founder-market fit, product differentiation, customer evidence, competition, valuation, exit path, ownership, reserves, and the biggest reasons the deal could fail.

5. Decision

The committee can approve the investment, pass, ask for more diligence, change the proposed terms, reduce the check size, wait for a milestone, or approve only if specific conditions are met. An approval usually gives the deal sponsor authority to move toward a term sheet or final investment documents.

What the committee evaluates

Every fund has its own decision model, but most VC investment committees evaluate a similar set of questions.

| Question | What the committee is testing |

|---|---|

| Thesis fit | Does this company match the fund's strategy and right to win? |

| Market size | Could the outcome be large enough for venture returns? |

| Founder quality | Does the team have unusual insight, urgency, resilience, and hiring ability? |

| Product evidence | Is there a real customer problem and credible product pull? |

| Traction | Are usage, revenue, retention, pipeline, or customer signals strong enough for the stage? |

| Competition | Why can this company win despite incumbents, substitutes, or fast followers? |

| Valuation and ownership | Do the terms support the fund's return target and ownership model? |

| Portfolio construction | Does the investment fit the fund's reserves, sector exposure, and concentration limits? |

| Risk | Which risks are acceptable, which are fatal, and which require more diligence? |

The committee is not trying to eliminate all uncertainty. Venture capital depends on uncertainty. The real test is whether the upside, evidence, and price justify the risk.

Voting and decision models

VC firms use different IC decision rules. The right model depends on fund size, stage, partnership culture, and how much autonomy individual partners have.

Common models include:

- Consensus: the firm wants broad partner support before approving the deal.

- Majority vote: the committee approves if enough voting members support the investment.

- Unanimous approval: every voting member must support the deal, which can reduce risk but may filter out non-consensus winners.

- Sponsor or champion model: a partner with strong conviction can lead the deal if they can defend the case and carry accountability.

- Veto rights: certain partners, fund managers, or committee members can block investments that violate strategy, risk limits, conflicts, or governance rules.

Early-stage VC firms often need room for conviction because the best investments can look strange before the market agrees. Later-stage or growth funds may use more structured consensus because checks are larger, diligence data is richer, and downside risk is more visible.

What candidates should know

If you want to work in venture capital, the investment committee process matters because it reveals what investment-team work is actually for. Sourcing matters, but a sourced deal only becomes useful if the team can build and defend a credible investment case.

Analysts and associates are often responsible for:

- Building market maps and competitive landscapes.

- Summarizing customer, founder, product, and financial diligence.

- Drafting memo sections or preparing supporting analysis.

- Finding the weak points in the investment case before the committee does.

- Turning ambiguous evidence into a clear recommendation.

- Preparing answers to likely partner objections.

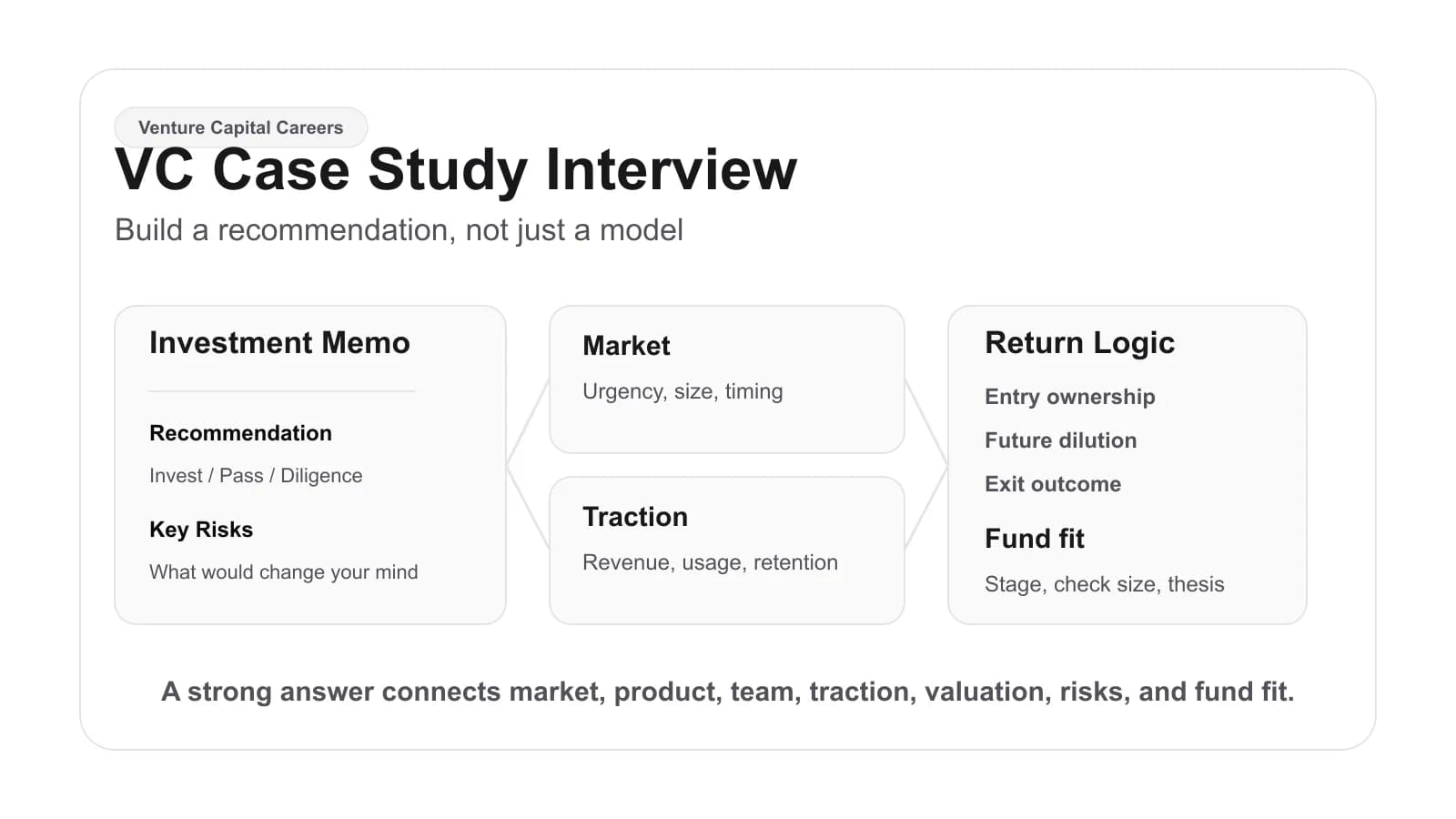

That is why VC case-study interviews often ask candidates to evaluate a startup and make an investment recommendation. The exercise is a simplified version of IC work. If you are preparing for interviews, pair this article with the venture capital case study interview guide, the VC associate job description, and the venture capital resume guide.

Candidates can also browse open roles on the Venture Capital Careers job board and research firms through the VC companies directory.

What founders should expect

Founders do not always present directly to the investment committee. At some firms, the deal sponsor presents the company internally. At others, the founder joins part of the meeting, especially if the round is later-stage, competitive, or strategically important.

Founders should expect the sponsor to need clear evidence for:

- why the problem is urgent;

- why the market can support a venture-scale outcome;

- why the team is unusually suited to win;

- why the product or distribution motion is defensible;

- what milestones the company can reach with the proposed financing;

- why the proposed valuation and terms make sense.

An IC process can end with a yes, a no, or a conditional next step. Conditional outcomes are common: more customer calls, revised terms, additional partner meetings, a smaller check, a different ownership target, or a request to wait for a milestone.

Common mistakes in IC preparation

The most common IC mistake is treating the memo as a summary instead of a recommendation. The committee does not only need facts. It needs a clear view on why the investment should or should not happen.

Other common mistakes include:

- Hiding the main risk instead of naming it directly.

- Presenting market size without explaining why this company can capture value.

- Relying on founder charisma without enough customer or product evidence.

- Ignoring valuation, ownership, reserves, or fund fit.

- Bringing a deal to committee before the investment ask is clear.

- Optimizing for consensus so strongly that no one owns the actual conviction.

Strong IC preparation makes the decision easier even when the answer is no. A well-run committee can pass quickly, approve with confidence, or identify exactly what evidence would change the decision.

FAQ

Is an investment committee the same as an investment memo?

No. The investment memo is the written recommendation and evidence package. The investment committee is the decision process or group that reviews the opportunity and decides what happens next.

Do founders present to the investment committee?

Sometimes. Some VC firms keep IC internal and have the sponsoring partner present the company. Others invite founders to answer questions or present part of the case, especially in later-stage deals.

Can analysts or associates vote in IC?

Usually not, but they can still influence the decision. Junior investors often prepare diligence, write memo sections, build market maps, and answer questions that shape partner conviction.

How long does the IC process take?

It depends on the fund, stage, round dynamics, and amount of diligence required. A competitive seed deal may move quickly. A later-stage round can require several meetings, deeper diligence, and more formal approval.

What happens after IC approval?

The deal team usually moves to a term sheet, final diligence, legal documents, or investment closing. Approval can still come with conditions, revised terms, or a smaller check size.

How should employers write roles that involve IC work?

Be specific about whether the role prepares memos, leads diligence, presents to partners, owns sourcing, supports portfolio companies, or has voting authority. Employers hiring for these roles can post a venture capital job and describe the IC responsibilities clearly.