Stock Holding Period: How to Calculate It and What It Changes

A practical guide to stock holding periods, U.S. tax-date rules, holding-period return, special cases, and private-share restrictions.

A stock holding period is the time between acquiring shares and disposing of them. For U.S. federal tax purposes, however, the clock generally starts the day after the purchase trade date and includes the sale trade date. A position held for more than one year is generally long-term; one year or less is short-term.

That clock is not the same as holding-period return. The first measures time and classifies a gain or loss. The second measures investment performance over a chosen interval. Mixing them produces avoidable tax and return errors.

What a stock holding period means

“Holding period” can refer to three related but different ideas:

| Clock | What it measures | What it answers | Common mistake |

|---|---|---|---|

| Ownership duration | Time from acquisition to disposal | How long did I own the asset? | Assuming ordinary elapsed time always matches the tax rule |

| U.S. tax holding period | A rule-based count that generally begins after acquisition and includes disposal | Is the gain or loss short-term or long-term? | Using settlement date or treating exactly one year as more than one year |

| Holding-period return window | The interval over which price change and income are measured | What total return did the investment produce? | Calling the return percentage the “holding period” or omitting dividends |

An investor may use all three for the same position. A VC fund may also use “holding period” to describe the years between investing in a portfolio company and exiting it. That is an underwriting assumption, not the investor’s public-stock tax calculation.

How to calculate the holding period for U.S. capital gains

For securities traded on an established market, use the trade dates shown on the confirmations—not the later settlement dates. The IRS holding-period rules in Publication 550 give a three-step process:

- Find the trade date on which you bought the shares.

- Begin counting on the following day.

- Include the trade date on which you sold the shares.

If the result is more than one year, the gain or loss is generally long-term. If it is one year or less, it is generally short-term.

Worked trade-date example

Suppose you buy stock on January 15, 2025. Your tax holding period starts on January 16, 2025.

| Sale trade date | Classification | Why |

|---|---|---|

| January 15, 2026 | Short-term | The position was not held for more than one year |

| January 16, 2026 | Long-term | The position was held for more than one year |

The one-day difference can change the classification. It does not mean waiting is always the right investment decision. A material thesis break, concentration problem, or liquidity need can outweigh a potential tax benefit.

What the classification changes

Net short-term capital gains are generally taxed as ordinary income. Long-term gains follow separate capital-gains rules. Rates and thresholds depend on the tax year and the taxpayer, so use the current IRS capital gains and losses guidance rather than a static rate table.

The classification applies to gains and losses, not the sale proceeds themselves. Gain or loss is calculated from the amount realized and adjusted basis. Basis can be more complicated for gifts, inheritances, employee equity, reorganizations, and reinvested distributions.

How to calculate holding-period return

Holding-period return, or HPR, is the total investment return over the measurement window. It combines the change in value with income received.

HPR = (Ending value − Beginning value + income received) ÷ Beginning value

Income can include cash dividends, interest, or other distributions attributable to the investment. A withdrawal from the account is not investment income. If you add or withdraw capital during the period, the simple formula may not fairly measure performance; a money-weighted or time-weighted calculation may be more appropriate.

Worked HPR example

You invest $10,000 in a stock. At the end of the period, the position is worth $10,900 and you have received $200 in cash dividends.

HPR = ($10,900 − $10,000 + $200) ÷ $10,000 = 11%

The investment produced an 11% total return over that specific window. The formula does not say whether the gain is short-term or long-term for tax purposes; that depends on the acquisition and disposition dates.

When to annualize the return

HPR reports the actual return for the selected period. To compare periods of different lengths, analysts often convert it to an annualized rate:

Annualized return = (1 + HPR)^(1 ÷ years held) − 1

Annualization is a comparison convention. It assumes a compounded annual pace and does not mean the investor received that amount in each calendar year. For an investment with irregular cash flows, use an appropriate cash-flow-based method rather than forcing the simple formula.

Special holding-period rules that can change the answer

The basic trade-date rule is only a starting point. IRS Publication 550 describes situations in which a prior owner’s period carries over, a new clock starts, or a separate qualification test applies.

| Scenario | General U.S. federal rule | What to check before acting |

|---|---|---|

| Gifted property | If basis is determined from the donor’s adjusted basis, the donor’s holding period generally carries over. If basis is determined by fair market value, the period generally starts the day after the gift. | Donor basis, fair market value, gift records, and the gain/loss calculation |

| Inherited property | A later gain or loss is generally treated as long-term regardless of how long the beneficiary actually held the property. | Estate documents and the basis rules that apply to the inheritance |

| Taxable stock dividend | The new shares generally start a holding period on the distribution date. | Whether the distribution was taxable |

| Nontaxable stock dividend or spin-off | The new shares generally inherit the holding period of the original shares. | Issuer tax documents and allocation of basis |

| Reinvested dividend or capital-gain distribution | Each newly purchased share generally begins its own period the day after purchase. | Lot-level purchase records; original and reinvested shares may have different classifications |

| Wash sale replacement shares | The replacement shares generally include the holding period of the shares sold at a disallowed loss. | Transactions in substantially identical securities and adjusted basis |

| Qualified dividends on common stock | The stock generally must be held for more than 60 days during the 121-day window around the ex-dividend date; days with diminished risk of loss may not count. | Ex-dividend date, hedges/options, and whether the dividend otherwise qualifies |

Basis and holding period interact, but they are not interchangeable. Basis answers how much gain or loss exists. Holding period usually answers how that gain or loss is classified. When records are incomplete or the transaction is unusual, verify the lot history and ask a qualified tax professional before filing or timing a sale.

What holding period means in venture capital and private shares

Private-company investors and employees can face several clocks at once. Calling all of them “the holding period” obscures the real constraint.

Restricted securities and Rule 144

SEC Rule 144 provides one route for publicly reselling restricted and control securities. Under the current electronic Code of Federal Regulations for Rule 144, restricted securities of a reporting company generally require at least a six-month holding period; securities of a non-reporting company generally require at least one year. Affiliate status, public information, sale volume, manner of sale, notices, and restrictive legends can add conditions.

Meeting the time requirement does not automatically make shares liquid or guarantee that a buyer exists. Rule 144 is also not the only possible exemption. Holders should review grant and purchase documents and obtain legal advice for an actual resale.

Four private-market clocks to keep separate

| Clock | What it governs |

|---|---|

| Rule 144 holding period | When restricted securities may become eligible for a public resale safe harbor, subject to other conditions |

| Contractual lock-up | When an agreement prevents a holder from selling, often around a financing or public offering |

| Vesting schedule | When an employee or founder earns ownership under the equity award terms |

| Investment holding period | How long a fund or investor expects to own the position before a secondary sale, acquisition, IPO, or other liquidity event |

Satisfying one clock does not satisfy the others. Vested shares may still be restricted. A Rule 144 period may have elapsed while a lock-up remains. An investment may be legally transferable but economically unattractive to sell.

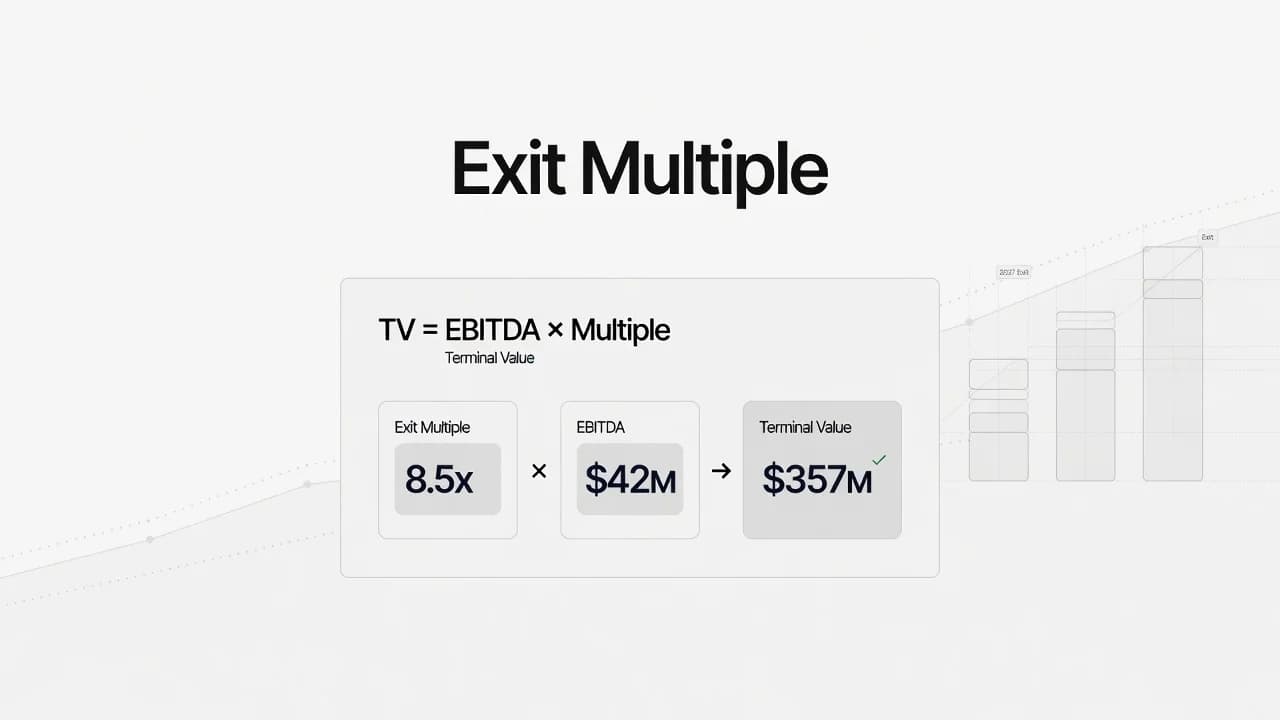

Where VC analysts use the assumption

A planned holding period appears in an investment memo, connects operating forecasts to an exit-multiple assumption, and affects IRR even when MOIC is unchanged. During a portfolio review, the team should revisit the expected exit path, financing runway, ownership, and time to liquidity rather than letting the original date become false precision.

If that combination of company analysis, return modeling, and portfolio judgment is the work you want to do, browse open venture capital roles.

How long should you hold a stock?

There is no universally optimal duration. An average stock holding period describes market behavior; it does not tell you when a specific position should be sold. The relevant question is whether the expected return still justifies the risk and opportunity cost.

Before holding solely to cross a tax threshold—or selling solely because a target date arrived—check:

- Thesis: Has the reason you bought the company materially changed?

- Valuation: Does the current price still offer an acceptable expected return?

- Concentration: Has the position or sector become too large relative to the portfolio?

- Liquidity: Do you need cash, or is the capital more useful elsewhere?

- Costs: What trading costs, spreads, contractual restrictions, or penalties apply?

- Taxes: What gains, losses, lot-selection choices, and holding-period rules apply?

A longer period can reduce turnover and may produce favorable tax treatment, but time does not repair weak economics. A shorter period can be rational when risk has changed or capital has a better use. The holding period should reflect the investment thesis and constraints, not replace them.

Common holding-period mistakes

- Using settlement date for exchange-traded stock. The federal tax clock generally uses trade date.

- Treating exactly one year as long-term. The general threshold is more than one year.

- Confusing elapsed time with HPR. One is a duration; the other is a percentage return.

- Leaving income out of HPR. Cash dividends and interest belong in total return; withdrawals do not become investment income.

- Assuming every lot has the same date. Reinvested distributions and later purchases create separate lots and clocks.

- Applying the basic rule to a special case. Gifts, inheritances, wash sales, stock distributions, and hedged positions may change the result.

- Treating a lock-up expiry as a sell signal. Eligibility to sell is not a recommendation to sell.

- Letting tax classification override material risk. A potential rate benefit should be weighed against thesis deterioration, concentration, and liquidity needs.

Frequently asked questions

Does the holding period include the purchase date?

For securities traded on an established market, the U.S. federal tax holding period generally begins the day after the purchase trade date. The sale trade date is included.

Is a stock held for exactly one year long-term?

Generally, no. A capital gain or loss is long-term when the asset was held for more than one year. A sale exactly one year after the purchase trade date is generally still short-term; the next day crosses the boundary.

What is the difference between holding period and holding-period return?

Holding period measures time. Holding-period return measures total performance over that time by combining the change in value with investment income and dividing by the beginning value.

Does the stock holding period start on trade date or settlement date?

For securities traded on an established market, the federal tax rule generally uses trade dates. The clock starts the day after the purchase trade date and ends on the sale trade date.

Is there a minimum holding period for public stocks?

Ordinary public shares generally do not have a universal minimum ownership period before they can be sold. Taxes, broker policies, trading rules, qualified-dividend tests, restricted securities, employee plans, and contractual lock-ups can create separate consequences or constraints.

The useful sequence is simple: identify the clock, apply the correct dates, calculate performance separately, then decide whether to hold or sell based on the thesis and constraints. Time changes the classification; it does not make the decision for you.