Venture Capital Fund Structure: How Funds, GPs, LPs, and Fees Fit Together

Learn how a venture capital fund, GP, management company, and LPs fit together—and how capital, fees, carry, decisions, and VC jobs move through the structure.

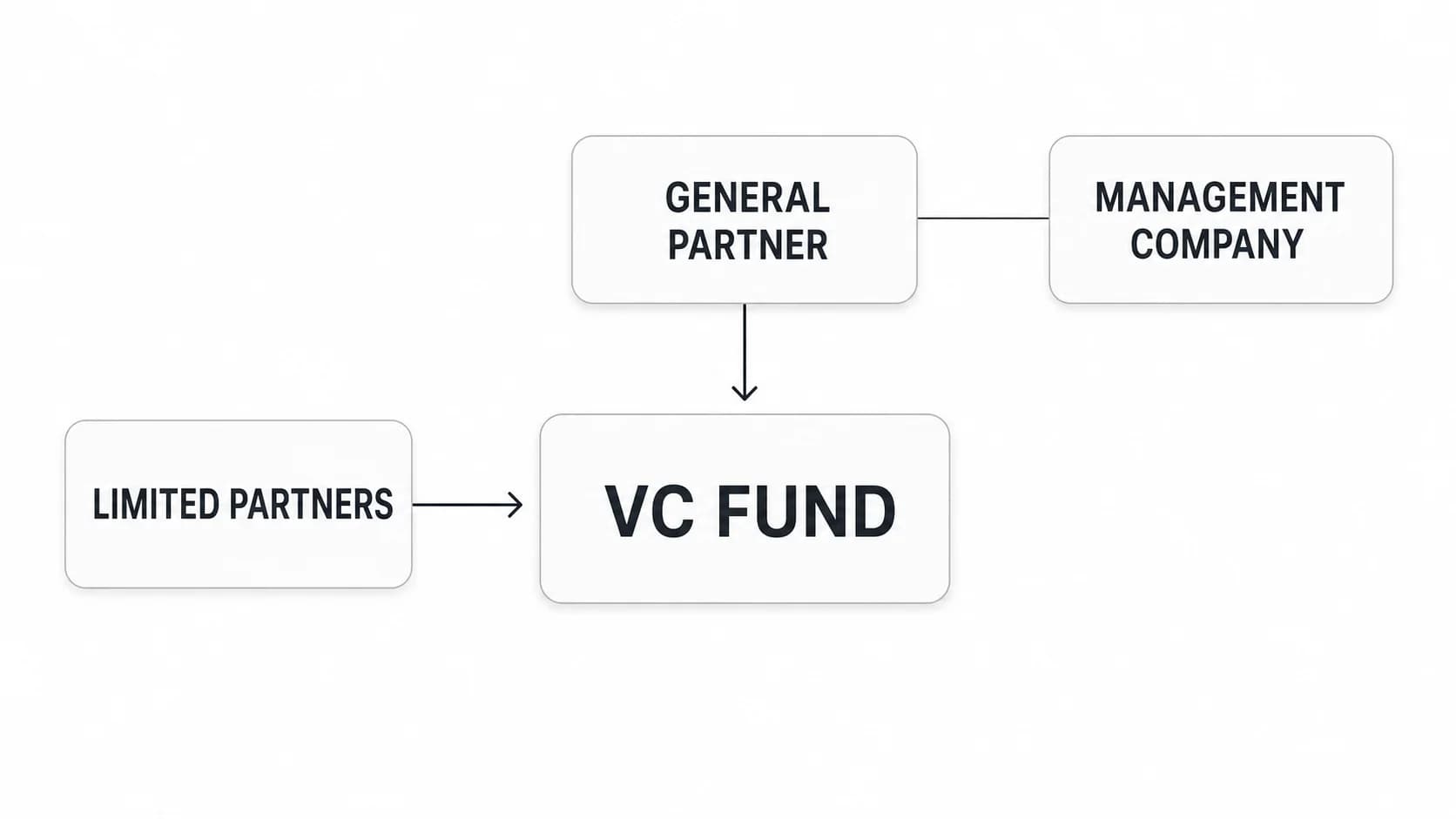

A typical venture capital fund is a limited partnership. Limited partners commit most of the capital, a general partner controls investment decisions, and a separate management company employs the team and runs the business. The fund itself holds the portfolio investments. Management fees generally support operations; carried interest rewards performance after distributions are calculated under the fund's governing agreement.

The important point is that a VC firm is not one legal box. The brand on the website may sit above several funds, GP entities, special-purpose vehicles, and one management company. Understanding those boundaries makes fund economics, decision rights, and VC job descriptions much easier to interpret.

The four layers of a venture capital fund structure

Most traditional VC structures have four core layers. Exact names and legal forms vary by jurisdiction and agreement, but the jobs of the entities are broadly consistent.

| Layer | What it does | What it owns or controls | What flows through it |

|---|---|---|---|

| The fund | Pools committed capital and makes investments | Portfolio-company securities and other fund assets | Capital calls, investment proceeds, expenses, and distributions |

| General partner entity | Legally manages the fund | Investment authority and other rights granted by the LPA | GP commitment and, depending on the structure, carried interest |

| Management company | Runs the operating business | Employees, vendor contracts, brand, and day-to-day systems | Management fees and operating expenses |

| Limited partners | Supply most of the committed capital | Partnership interests and negotiated information/governance rights | Contributions, reports, and distributions |

1. The fund

The fund is the investment vehicle. In a common US structure, it is formed as a limited partnership. LPs subscribe for interests in that partnership, and the fund becomes the legal owner of shares, SAFEs, convertible notes, or other securities purchased from portfolio companies.

That distinction matters. A partner may lead the deal and an associate may build the model, but the fund—not the individual professional or the management company—usually appears on the portfolio company's cap table.

2. The general partner entity

The general partner, or GP, is the entity with authority to manage the fund. It signs on behalf of the partnership, approves investments through the firm's governance process, calls capital, and oversees distributions. The individuals called “general partners” at a firm usually act through this legal GP entity.

The GP's authority is not unlimited. The limited partnership agreement sets the mandate, economics, conflicts process, reporting duties, key-person provisions, and other boundaries. It is the core governing agreement between the GP and the fund's LPs.

3. The management company

The management company is the operating business behind the funds. It typically employs analysts, associates, finance staff, investor-relations professionals, platform teams, and other employees. It pays salaries, software bills, office costs, insurance, and vendors.

Keeping the management company separate from each fund also explains how one firm can operate Fund I, Fund II, and Fund III without creating a new employer for every vintage. The team can work across vehicles while the investments and investor obligations remain separated.

4. The limited partners

Limited partners, or LPs, are the investors in the fund. They can include pension plans, endowments, foundations, family offices, funds of funds, corporations, and qualified individuals. They commit capital but usually do not select individual portfolio investments.

“Limited” refers to both liability and management participation. LPs negotiate rights through the LPA and side letters, receive reports, and may sit on a limited partner advisory committee. Those oversight rights are different from running the daily investment process.

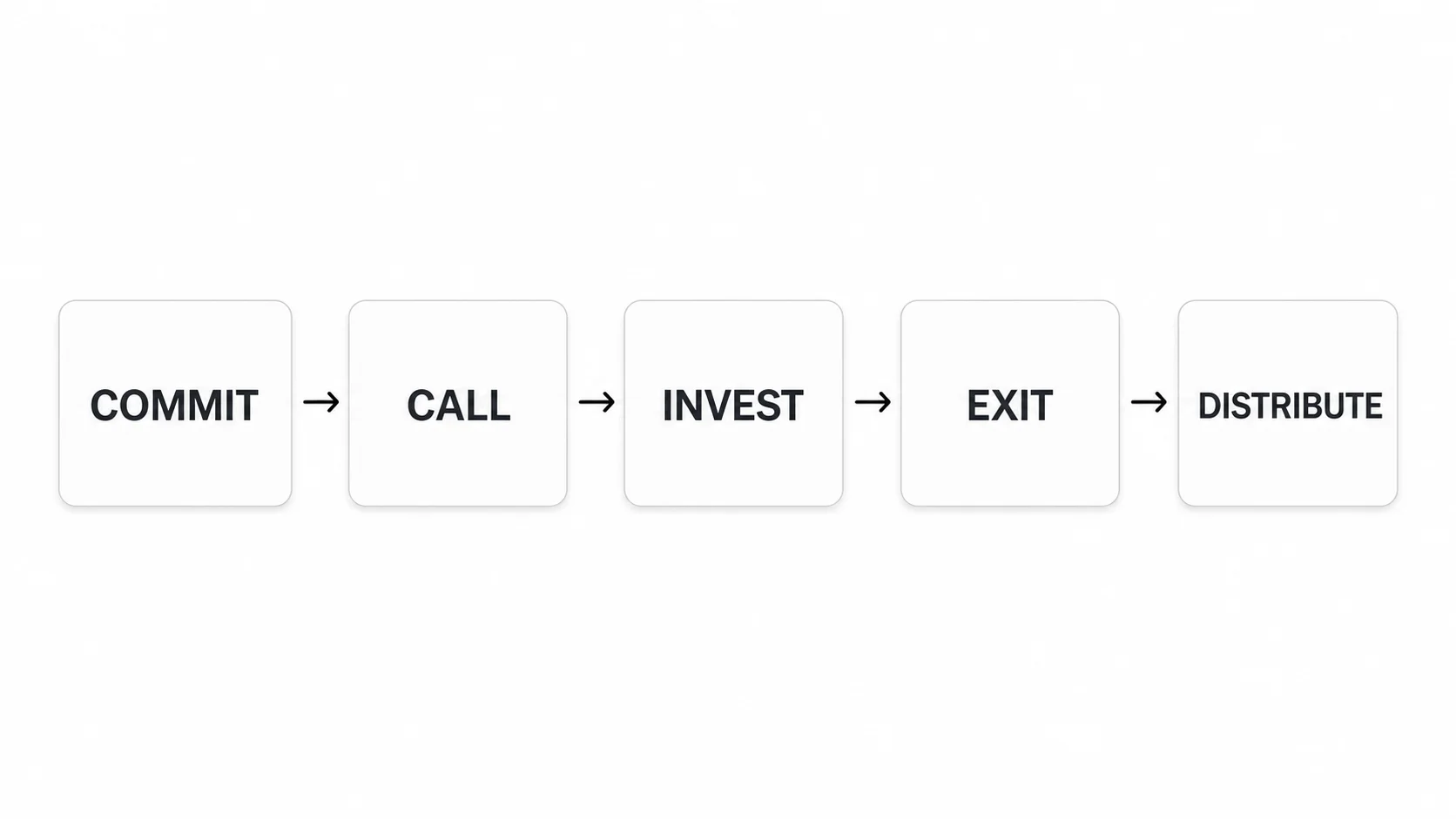

Follow the money through a VC fund

The cleanest way to understand venture capital fund structure is to trace the cash rather than memorize entity names.

- Commit. An LP signs subscription documents and agrees to provide a stated amount over the fund's life. A $5 million commitment is a legal obligation, not usually a same-day transfer of $5 million.

- Call. The GP issues a capital-call notice when the fund needs cash for an investment, fee, or permitted expense. Each LP contributes its share according to the agreement.

- Invest. The fund sends capital to a portfolio company or seller and receives securities. The investment team sources and diligences the deal, but the fund vehicle holds the asset.

- Exit. If a portfolio company is acquired, goes public, or supports a secondary sale, proceeds return to the fund.

- Distribute. The fund allocates and distributes proceeds under the LPA's waterfall, including return of capital and any carried-interest calculation.

Consider a deliberately simple illustration. LPs commit $100 million to a fund. The fund does not need the full $100 million on day one, so the GP calls capital over time. If the fund calls $8 million for an investment and permitted expenses, the LPs transfer their pro-rata shares. Years later, an exit sends $24 million back to the fund. That cash is then allocated and distributed under the LPA—not automatically split the moment it arrives.

The numbers are illustrative, not a market standard. Actual calls can include fees and expenses; proceeds can be recycled; investments can be written off; and distribution waterfalls vary.

How management fees and carried interest fit

Management fees and carried interest pay for different things and usually travel through different parts of the structure.

Management fees fund operations. The fund pays a fee under the LPA, and the management company uses that revenue to run the firm. The fee base and rate may change over the fund's life. Some agreements calculate it on committed capital during the investment period and on a smaller base later. Large, established, emerging, and specialist funds can negotiate different terms.

Carried interest rewards investment performance. Carry is a share of profits allocated to the GP or another carry vehicle according to the distribution waterfall. The calculation can include return-of-capital requirements, a preferred return, catch-up mechanics, escrow, clawback provisions, and deal-by-deal or whole-fund rules.

“Two and twenty” is useful shorthand for a 2% management fee and 20% carry, but it is not a law or a universal quote. A strong candidate asks what the fee is charged on, when it steps down, how the waterfall works, and which team members actually participate in carry.

One VC firm can manage several funds

A firm brand is an umbrella, not necessarily the investment vehicle. A simplified platform might look like this:

- Northstar Ventures Management LLC employs the team and supports the platform.

- Northstar Ventures Fund I, LP owns the first vintage of portfolio investments.

- Northstar Ventures Fund II, LP owns a later, legally separate portfolio.

- Each fund has its own GP entity, LPA, LP group, mandate, accounting records, and performance.

- A separate opportunity fund or SPV may hold follow-on or single-company exposure.

The separation protects accounting and governance boundaries. An LP in Fund II did not automatically invest in Fund I. A win in one vehicle does not move freely into another. Expenses, allocations, and conflicts must be handled under the relevant agreements.

This is also why fund research should go beyond the logo. When using the Venture Capital Careers companies directory, look for the active fund vintage, stage, geography, sector mandate, check size, and whether a role supports one strategy or the whole platform.

Who does the work inside the structure

Most employees work for the management company, but their work serves one or more funds. The entity map helps explain why two people at the same firm can have very different responsibilities.

| Team | Typical work | Structural knowledge that matters |

|---|---|---|

| Analysts and associates | Sourcing, screening, market work, models, diligence, memo support | Which fund can make the investment, ownership targets, reserves, and decision authority |

| Principals and partners | Thesis, deal leadership, IC sponsorship, boards, portfolio decisions | Mandate, conflicts, allocation across vehicles, GP duties, and fund economics |

| Finance and fund operations | Capital calls, valuations, expense allocation, reporting, audit support | Fund-by-fund books, fee calculations, cash controls, and administrator workflows |

| Investor relations and capital formation | Fundraising, DDQs, LP updates, annual meetings | LPA terms, performance reporting, pipeline, strategy, and LP obligations |

| Legal and compliance | Formation, regulatory filings, conflicts, contracts, policies | Adviser status, offering exemptions, side letters, governance, and portfolio documentation |

| Platform and talent | Portfolio support, recruiting, community, events, go-to-market programs | Which services are funded by the management company and which costs may be allocated to a fund or portfolio company |

Adviser registration, fund exemptions, investor eligibility, and offering rules depend on facts and jurisdiction. Candidates should understand the operating map, but fund formation and compliance require qualified legal and tax advice.

For job seekers, the most revealing question is often: “Which cash flow or decision does this role own?” An investing associate and a fund accountant may both support Fund II, but one shapes portfolio selection while the other protects the accuracy of calls, allocations, and reporting.

Fund structure is not deal structure

These two phrases are easy to confuse:

- Fund structure describes the vehicle that pools capital: fund, GP, management company, LPs, agreements, fees, and governance.

- Deal structure describes how that vehicle invests in a company: SAFE, convertible note, preferred stock, valuation, liquidation preference, board rights, and other term-sheet provisions.

Use a simple test. If the question is “Who owns the portfolio and who controls the vehicle?”, it is about fund structure. If the question is “What security did the startup issue and what rights came with it?”, it is about deal structure.

Both layers meet in the investment process. An associate may model the financing terms, write an investment memo, and prepare the recommendation for an investment committee. The fund's mandate determines whether the deal belongs in that vehicle; the deal documents determine what the fund buys.

What candidates should be able to explain in an interview

Memorizing abbreviations is not enough. A candidate should be able to answer these questions in plain language:

- What is the difference between the firm and the fund? The firm is the operating platform and brand; each fund is a separate investment vehicle.

- Why is there a GP entity and a management company? The GP controls the fund under the LPA; the management company employs the team and runs operations.

- Why do LPs commit capital instead of wiring everything immediately? Calls align cash funding with investments, fees, and permitted expenses over time.

- Where do management fees and carry go? Fees generally support the management company; carry is a performance allocation through the GP or a carry vehicle.

- Who owns a startup investment? Usually the fund or an affiliated SPV, not the individual partner who sourced it.

- How does structure affect an investment decision? The vehicle's mandate, remaining capital, reserves, ownership strategy, conflicts, and approval rules constrain the deal.

That knowledge strengthens both investing and operations applications. Pair it with the analytical and relationship abilities in Venture Capital Skills and the role progression in the Venture Capital Career Path.

Common misconceptions

“LPs hand over the whole fund on day one.” Usually they commit first and fund capital calls over time.

“The management company owns the portfolio.” The fund vehicle generally owns the investments; the management company runs the operating business.

“Every person called a partner is the legal GP.” Titles describe seniority and economics; legal authority is exercised through the GP entity and the firm's governance process.

“Two and twenty explains the whole business.” It leaves out the fee base, step-downs, expenses, GP commitment, waterfall, carry allocation, and clawback terms.

“A new fund is just more money in the old pool.” A new vintage is normally a separate vehicle with its own LP interests, portfolio, mandate, and return record.

Frequently asked questions

What is the typical structure of a venture capital fund?

A traditional VC fund is commonly a limited partnership. LPs commit capital, a GP entity manages the partnership, and a management company employs the team and runs operations. The fund owns portfolio investments and distributes proceeds under its LPA.

Is a VC firm the same as a VC fund?

No. The firm is the brand and operating platform. A fund is one investment vehicle managed by that firm. Established firms often manage several funds and SPVs at once.

Do limited partners choose startup investments?

Usually not. LPs delegate investment authority to the GP within the LPA's mandate. They may retain reporting, consent, removal, conflict-review, or advisory-committee rights without selecting each deal.

Where do VC employees work?

Most are employees of the management company, even when their daily work supports a specific fund. Employment and compensation arrangements vary, especially for partners and carry participants.

How long does a venture capital fund last?

Traditional funds are designed to hold illiquid startup investments for years. The LPA sets the term, investment period, extension rights, and wind-down mechanics; there is no single duration that fits every strategy.

Understanding the structure is only useful if you can connect it to a real firm and role. Research venture capital firms, then browse open VC jobs and test each description against the entity, cash flow, and decision it actually supports.