Pay-to-Play Provision in VC: Definition, Example, and Down-Round Impact

A pay-to-play provision requires existing startup investors to join a future financing, usually pro rata, or lose protections such as anti-dilution rights or preferred-stock status.

A pay-to-play provision is a venture capital financing term that requires existing investors to participate in a future round, often up to their pro rata share, if they want to keep specific rights. If they do not "pay," they may lose anti-dilution protection, preferred-stock rights, board rights, information rights, or other negotiated protections.

The clause matters most when a startup needs capital in a difficult financing environment. In a clean up round, investors usually want allocation. In a down round or recapitalization, a pay-to-play clause forces a harder choice: support the company with new money or accept worse economics and governance rights.

Pay-to-play is sometimes called a cram-down provision. That label is accurate when the penalty is severe, but not every pay-to-play clause is equally harsh. Some simply condition anti-dilution protection on continued participation. Others convert non-participating preferred shares into common stock and meaningfully reset the cap table.

How a pay-to-play clause works

The basic structure is simple:

- The company raises a new financing round.

- Existing investors are offered the right or obligation to invest, usually in proportion to their current ownership.

- Investors who participate keep the rights attached to their preferred stock.

- Investors who do not participate lose some negotiated benefits.

"Pro rata" means the investor participates in proportion to its ownership or contractual allocation. If an investor owns 10% of the company on the relevant calculation basis, a full pro rata participation requirement may require that investor to fund 10% of the new round. For background on the concept, see VCC's guide to pro rata rights.

The exact drafting matters. A clause may require full pro rata participation, partial participation, participation above a minimum dollar threshold, or participation only if the investor receives proper notice before the round closes. It may also apply only to major investors rather than every small angel or employee holder.

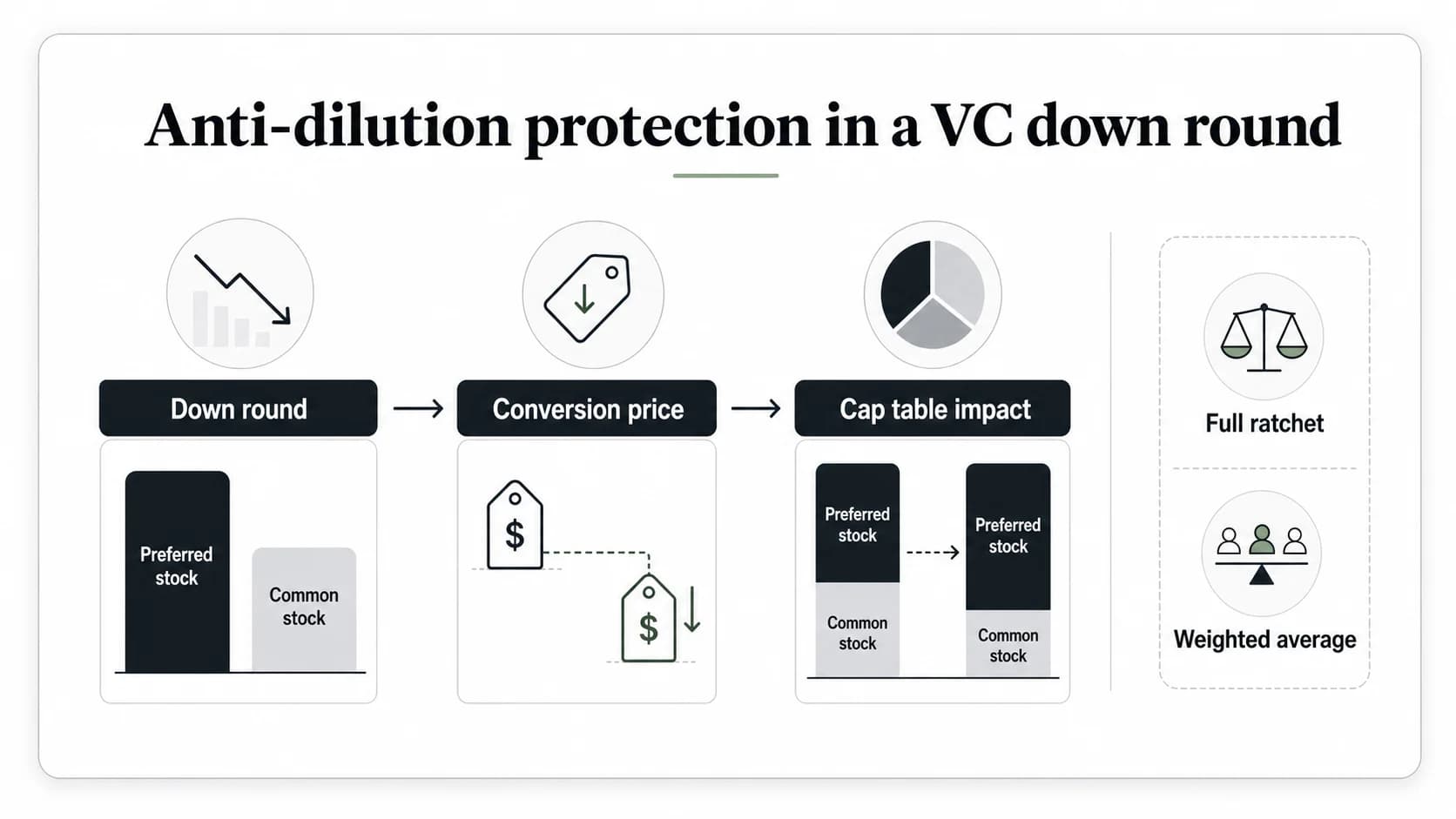

Pay-to-play example in a down round

Assume a startup raised a Series A at a $40 million post-money valuation. The Series A investors received preferred stock with weighted-average anti-dilution protection. Two years later, the company needs more cash but can only raise a Series B at a $25 million post-money valuation.

Without pay-to-play, an existing Series A investor might refuse to invest in the Series B while still benefiting from anti-dilution protection. That means the investor can preserve part of its economics while other investors put in the rescue capital.

With pay-to-play, the Series B term sheet can say: if a Series A investor does not buy its required share of the Series B, that investor loses anti-dilution protection or has its Series A preferred stock converted into common stock. The participating investors supply the new money and keep preferred protections. The non-participating investors are diluted or lose priority.

That is why pay-to-play is less about a normal growth round and more about capital discipline. The clause separates investors willing to fund the next stage from investors who want the old protections without adding capital.

What investors can lose if they do not participate

Pay-to-play penalties usually fall on a spectrum.

| Penalty | What changes | Severity |

|---|---|---|

| Loss of anti-dilution protection | The investor no longer receives conversion-price adjustment protection for the new financing. | Moderate |

| Loss of future pro rata rights | The investor may lose the right to maintain ownership in later rounds. | Moderate |

| Loss of investor rights | Information, registration, or major-investor rights may fall away. | Moderate to high |

| Loss of board or observer rights | The investor may lose governance influence. | High |

| Conversion to shadow preferred | The investor keeps some preferred economics but loses selected rights. | High |

| Conversion to common stock | The investor loses preferred-stock preferences and participates like common holders. | Highest |

Conversion to common is the most aggressive version because preferred stock often carries liquidation preference, protective provisions, and other rights that common stock does not. For a refresher on that priority stack, see VCC's guide to liquidation preference.

Pay-to-play vs anti-dilution protection

Anti-dilution protection helps preferred investors when a company issues shares at a lower price than the earlier preferred round. Investopedia describes anti-dilution provisions as clauses that adjust conversion prices when lower-priced shares are issued, commonly through full-ratchet or weighted-average formulas (Investopedia).

Pay-to-play changes who gets that protection.

Without pay-to-play, an investor may receive anti-dilution protection even if it does not help fund the down round. With pay-to-play, anti-dilution protection can become conditional: investors keep it only if they participate in the new financing.

This is why the clause is often negotiated alongside anti-dilution language in a term sheet. A founder-friendly version may say investors lose only anti-dilution protection if they sit out. A more investor-led recapitalization may say non-participants convert into common or shadow preferred.

The distinction matters because full-ratchet anti-dilution can be especially punitive to founders and common shareholders. Pay-to-play can soften that effect by limiting the benefit to investors who keep supporting the company.

Why startups use pay-to-play provisions

Startups and lead investors use pay-to-play provisions for several reasons.

- To force an investor commitment decision. Investors cannot sit out and keep all downside protections.

- To reduce free riding. The investors funding the round are not carrying investors who refuse to participate.

- To make a difficult round fundable. New investors may not want to invest if old investors keep strong protections without contributing capital.

- To clean up the cap table. The company can distinguish active financial backers from passive holders.

- To signal insider support. Participation by existing investors can help validate a bridge, extension, or down round.

A pay-to-play provision can help a company in a financing crunch, but it can also strain investor relationships and create governance friction if drafted too aggressively.

Risks for founders, employees, and existing investors

For founders, the biggest risk is overcorrection. A harsh pay-to-play clause may help close the current round but damage relationships with early backers, small funds, angels, or strategic investors who cannot write follow-on checks quickly.

For employees, the risk is indirect but real. If a pay-to-play financing is part of a broad recapitalization, common stock and options may be diluted heavily. If the round also reprices the option pool, employees may need a separate refresh grant conversation.

For existing investors, the risk is capital allocation. A fund may believe in the company but lack reserves, have concentration limits, or face partnership constraints. Pay-to-play can force that investor to choose between funding a challenged asset and losing rights it negotiated in an earlier round.

For new investors, the risk is enforceability and cleanup. If the existing documents do not clearly support the penalty, the company may need approvals, waivers, charter amendments, or investor consents before the round can close. Counsel should confirm the mechanics before anyone treats the clause as automatic.

How to negotiate a pay-to-play provision

Founders should not negotiate pay-to-play as a slogan. The useful negotiation is in the details.

- Participation threshold: Is the investor required to buy its full pro rata share, a partial amount, or a minimum dollar amount?

- Triggering round: Does it apply to every financing, only down rounds, or only qualified financings above a size threshold?

- Investors covered: Does it apply to all preferred holders, only major investors, or only investors above a percentage threshold?

- Notice period: How much time does an investor get to decide and fund?

- Penalty: Does the investor lose anti-dilution only, lose major-investor rights, convert to shadow preferred, or convert to common?

- Carve-outs: Are there exceptions for legal restrictions, fund life limits, sanctions issues, strategic investors, or very small holders?

- Required approvals: Does the charter, investor rights agreement, voting agreement, or board approval process need to change?

Investors should focus on the same points from the other side. A reasonable pay-to-play clause can align everyone around continued support. A vague clause can become a future dispute.

Pay-to-play clause checklist

Before agreeing to the term, review the clause with company counsel and ask:

- What exact financing triggers the obligation?

- What amount must each investor contribute to remain protected?

- What rights are lost for non-participation?

- Does the penalty apply automatically or only after a vote or amendment?

- Are notice, deadline, and wiring mechanics clear?

- Does the clause treat major investors, small holders, founders, and strategic investors differently?

- Does it interact cleanly with anti-dilution, protective provisions, board rights, and information rights?

- Would the clause still feel acceptable if the company needs another bridge round in six months?

If the answer to any of those questions is unclear, the risk is not only economic. It is also procedural. Unclear pay-to-play mechanics can delay a financing at the exact moment the company needs speed.

Related VC terms

Pay-to-play sits inside a broader set of venture financing terms:

- Down round: a financing at a lower valuation than a prior round.

- Anti-dilution provision: a mechanism that adjusts preferred-stock conversion economics after lower-priced issuances.

- Pro rata rights: rights that let investors maintain ownership by participating in future financings.

- Protective provisions: consent rights that give preferred investors approval power over major company actions.

- Term sheet: the financing document where these economics are usually negotiated before definitive documents.

For readers building a broader understanding of how VC firms evaluate financing terms, Venture Capital Careers also maintains a VC job board and a VC companies directory for researching firms by strategy and market.

Frequently asked questions

What is a pay-to-play provision?

A pay-to-play provision is a startup financing term that requires existing investors to participate in a future round if they want to keep specified rights. Non-participating investors may lose anti-dilution protection, preferred-stock rights, board rights, or other investor protections.

Why is it called pay-to-play?

The phrase means an investor must contribute new capital to keep playing with the same rights. In VC, it usually appears when a company needs insider support in a bridge, down round, recapitalization, or other difficult financing.

Is pay-to-play the same as a cram down?

Not always. A pay-to-play clause becomes a cram-down-style term when the penalty is severe, such as converting non-participating preferred stock into common stock. Milder versions may only remove anti-dilution protection or future pro rata rights.

How does pay-to-play neutralize anti-dilution in a down round?

Anti-dilution protection can give preferred investors better conversion economics after a down round. A pay-to-play clause can make that protection conditional on participating in the new financing. If the investor does not invest, the anti-dilution adjustment may be reduced or eliminated.

Who benefits from a pay-to-play provision?

Participating investors and the company usually benefit most. Participating investors avoid carrying non-participants, and the company has a stronger chance of raising the capital it needs. Non-participating investors, common shareholders, and employees may be worse off depending on the penalty and the broader recapitalization.

Should founders accept a pay-to-play clause?

Sometimes. A narrow clause can be reasonable when the company needs investor support to close a financing. Founders should push for clear triggers, fair notice, proportionate penalties, and counsel-reviewed mechanics. A broad clause that converts non-participants to common stock in many scenarios deserves much closer scrutiny.