Venture Capital Portfolio Strategy: How Funds Allocate Capital

A practical framework for turning fund size and investment thesis into first checks, ownership targets, reserves, pacing, and portfolio decisions.

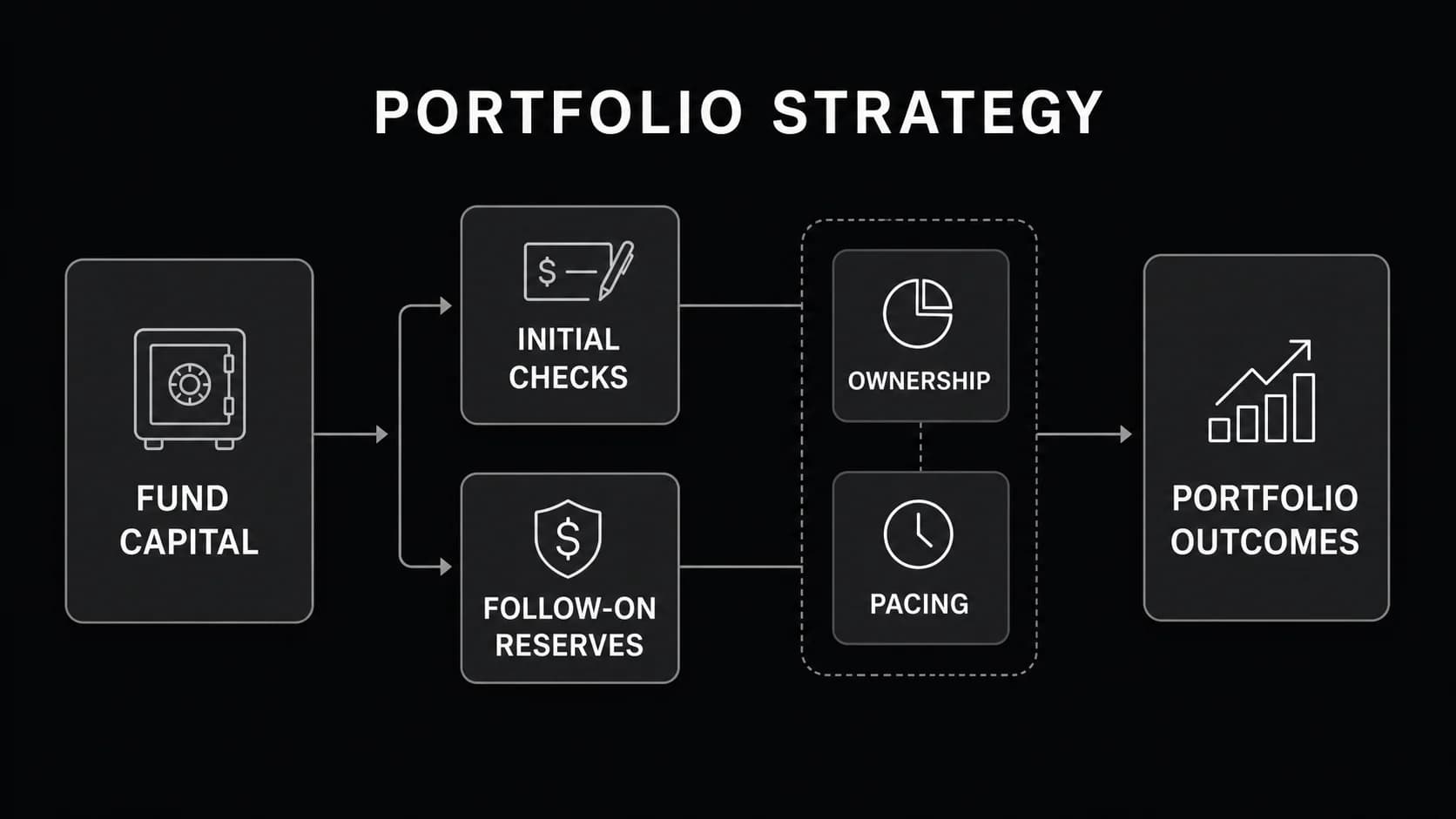

A venture capital portfolio strategy is the set of rules a fund uses to turn capital and an investment thesis into actual checks. It defines portfolio size, first-check size, ownership targets, follow-on reserves, deployment pace, concentration, and when the team can make exceptions.

There is no universal ideal number of companies or reserve ratio. The choices must work together: a larger portfolio creates more chances to find an outlier, but usually leaves less ownership in each company; larger reserves protect ownership in winners, but reduce capital for new names.

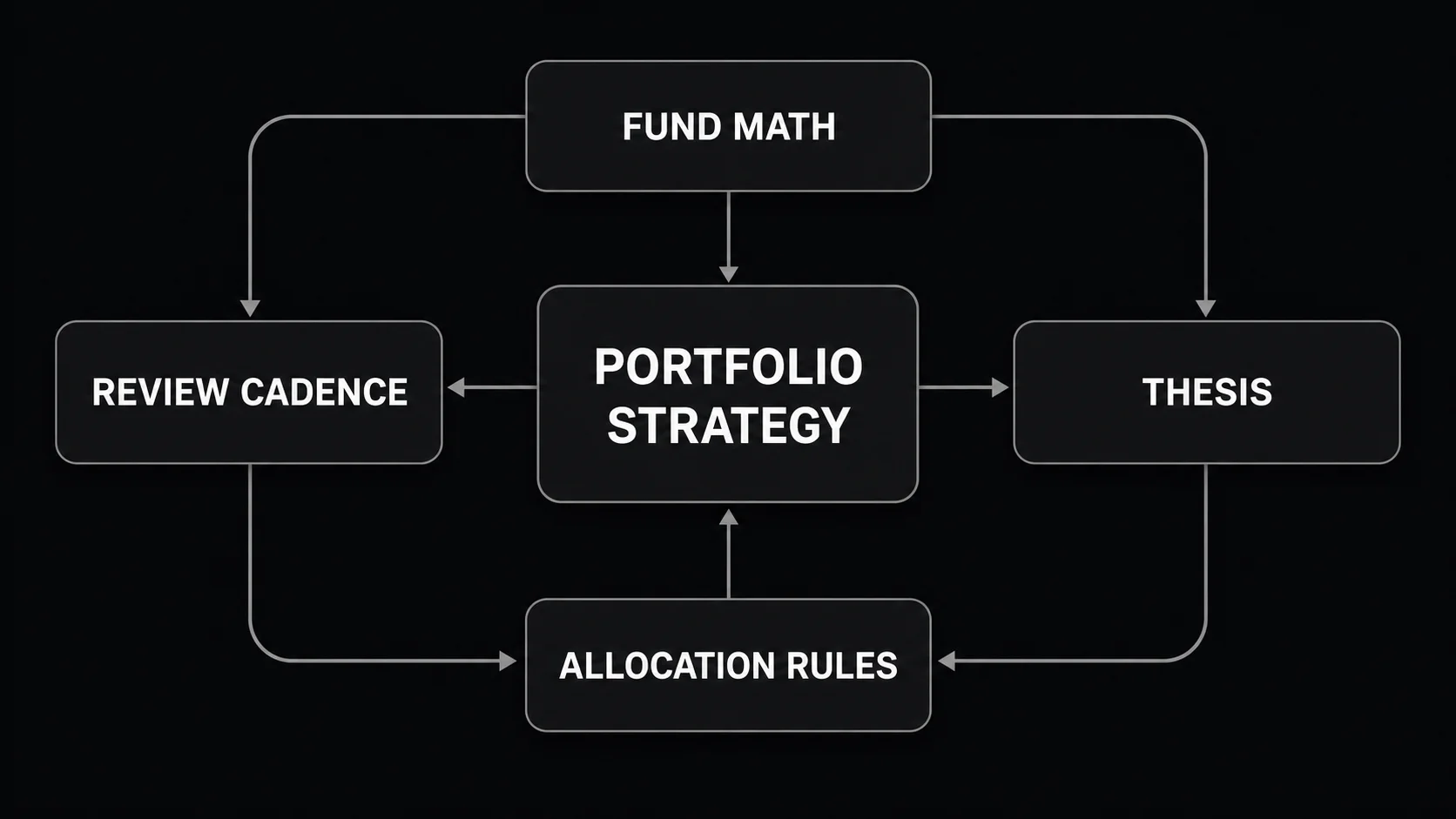

The strongest strategy is an operating system with four linked parts: fund math, thesis constraints, allocation rules, and a review cadence.

What is a venture capital portfolio strategy?

A venture capital portfolio strategy converts committed capital and an investment thesis into a portfolio the team can actually build. It defines how many initial investments the fund can make, the size and ownership target of each check, how much capital stays available for follow-ons, how quickly the fund deploys, and when the team can make exceptions.

The strategy has two connected parts:

| Part | Question it answers | Typical outputs |

|---|---|---|

| Portfolio construction | What portfolio are we trying to build? | Investable capital, stage mix, check size, company count, ownership target, reserve budget |

| Portfolio management | Are actual investments still consistent with the plan? | Pacing, concentration, follow-on decisions, reserve reallocations, risk flags, exit scenarios |

AngelList's portfolio construction overview makes the same useful distinction: construction designs the investing strategy, while management tracks actual investments against it. The practical mistake is to treat them as separate spreadsheets. A good strategy connects them through four linked decisions:

1. Fund math: how much capital is actually available to invest? 2. Thesis: which stages, sectors, geographies, and ownership positions does the fund pursue? 3. Allocation rules: how much goes into first checks, follow-ons, and exceptional opportunities? 4. Review cadence: what evidence causes the team to keep, change, or override those rules?

The venture capital fund structure is the legal and economic wrapper. Portfolio strategy is the operating logic inside that wrapper.

Start with constraints, not a target company count

“How many companies should the fund invest in?” is usually the wrong first question. Portfolio count is an output of several constraints that must reconcile.

Investable capital

Committed fund size is not automatically equal to capital available for portfolio companies. Management fees, operating expenses, and other fund obligations reduce the investable pool. Use the amount the fund can actually deploy, and state whether the model is gross or net of those obligations.

Stage and check size

A pre-seed fund can often spread smaller first checks across more companies. A Series A or growth fund may need larger checks to earn a meaningful allocation. The round sizes available in the target market constrain what a spreadsheet can claim.

Ownership target

Some funds optimize for access to more companies; others require enough ownership for a successful exit to matter at fund level. Target ownership and average check size must agree with expected post-money valuations:

initial ownership = investment ÷ post-money valuation

If a $750,000 check enters at a $15 million post-money valuation, the simplified initial ownership is 5%. If the strategy requires 10%, either the check, valuation, or target must change.

Follow-on policy

Reserving capital reduces the amount available for new names. A 40% reserve budget is not a free extra pool; it means fewer or smaller initial checks. The policy should say which companies can earn that capital and when unused reserves return to the unallocated pool.

Team capacity and access

A portfolio of 60 companies is not diversified if the team cannot source 60 thesis-fit investments, win allocation, complete diligence, or support the companies. Capacity is not an administrative footnote. It is a portfolio constraint.

Only after these inputs agree should the model solve for company count:

planned initial investments = initial-check budget ÷ average first check

A worked VC portfolio strategy example

Consider a simplified $30 million seed fund. The figures below are illustrative, gross, and deliberately round; they are not a benchmark or recommendation.

| Input | Illustrative assumption |

|---|---|

| Committed fund size | $30.0m |

| Investable capital after modeled fund obligations | $24.0m |

| Initial-check allocation | 60% of investable capital |

| Follow-on reserve allocation | 40% of investable capital |

| Planned initial investments | 20 |

| Average first check | $720k |

| Initial ownership target | 8% |

| Illustrative ownership at exit after dilution | 5% |

Step 1: Reconcile first checks and reserves

- Initial-check budget:

$24.0m × 60% = $14.4m - Reserve budget:

$24.0m × 40% = $9.6m - Average first check:

$14.4m ÷ 20 = $720k

The first consistency test is simple: the planned checks cannot exceed the initial-check budget. A model that assumes 25 first checks of $750,000 would require $18.75 million, so the fund would need to cut check size, reduce company count, or reduce reserves.

Step 2: Test the ownership assumption

An 8% initial stake from a $720,000 investment implies a $9 million post-money valuation:

$720k ÷ 8% = $9.0m

If the fund's real target rounds are commonly priced much higher, the model may not be executable. The team must either accept lower ownership, write larger checks, lead smaller rounds, or change stage.

Step 3: Test whether a winner can move the fund

At 5% ownership on exit, the company would need a $600 million exit for the fund to receive $30 million in simplified gross proceeds:

$30m ÷ 5% = $600m

At 3% diluted ownership, that threshold rises to $1 billion. This does not predict the exit. It tests whether the fund's check size, ownership, and target market can plausibly create fund-level outcomes.

Step 4: Pressure-test the plan

Run at least three cases:

- Access case: the fund receives only half its target allocation in the strongest deals.

- Dilution case: ownership falls faster than planned because winners raise several large rounds.

- Reserve case: more companies qualify for follow-on capital than the reserve budget can support.

The output should be a decision, not false precision. If one assumption breaks, identify which lever changes and who can approve the exception.

Choose a concentration–ownership tradeoff

Venture outcomes are uneven. A small number of companies can drive most of a fund's value, which is why portfolio size matters. But “more companies” and “more ownership” compete for the same capital.

Toptal's portfolio strategy analysis argues strongly for the home-run nature of venture returns. The useful conclusion is not that downside never matters. It is that every initial investment must have enough plausible upside to matter, while the portfolio must contain enough independent opportunities to find an outlier.

| Strategy shape | More likely to emphasize | Main advantage | Main risk |

|---|---|---|---|

| Broad | More initial investments, smaller stakes, limited reserves | More independent shots and lower single-company dependence | A winner may not return enough capital because ownership is thin |

| Balanced | Moderate company count, explicit ownership floor, selective reserves | Preserves both coverage and meaningful stakes | Requires disciplined allocation and hard follow-on choices |

| Concentrated | Fewer companies, larger stakes, active follow-ons | One winner can have a very large fund impact | Higher selection risk and fewer chances to find the outlier |

Diversification in VC is not a target number. It is a relationship among company count, correlation, ownership, and fund-return potential.

Twenty enterprise software companies with the same buyer, geography, stage, and pricing risk may be less diversified than twelve companies across different technical and market exposures. Conversely, superficial sector variety does not help if the fund has no sourcing or judgment advantage in those markets.

Write the chosen tradeoff explicitly. A useful policy says what the fund is willing to give up—ownership, number of names, reserves, or stage flexibility—to protect what matters most.

Turn reserves into decision rules

A reserve budget is capital held for existing portfolio companies. It is not an entitlement that every company receives automatically.

BDC's practitioner advice on portfolio management recommends writing the reserve policy down, reviewing it often, and shifting reserves from weaker companies to potential portfolio-makers. That principle becomes more usable when the policy defines four states:

| State | Evidence | Portfolio action |

|---|---|---|

| Maintain | Company is near plan; next round timing and ownership needs are unchanged | Preserve the modeled reserve |

| Increase | Evidence has strengthened and the company can materially affect fund returns | Reallocate within policy or seek IC approval for an exception |

| Release | Company no longer needs the expected amount, or the fund will not defend its full stake | Return excess reserve to the unallocated pool |

| Stop | Thesis is broken, financing risk is unacceptable, or more capital cannot change the outcome | Do not follow on solely to protect sunk cost |

The policy should also answer:

- Is follow-on capital pro rata, stage-based, milestone-based, or discretionary?

- Does the fund reserve for every company or only for a defined subset?

- Can reserves fund a bridge round, and under what evidence standard?

- When does unused capital become available for new investments?

- Who can move capital between companies?

The follow-on investment guide explains the transaction itself, while pro rata rights explains the right to maintain ownership. Portfolio strategy decides whether exercising that right is the best use of scarce fund capital.

The hardest reserve decision is often not whether a company is “good.” It is whether another dollar invested there has a better fund-level expected outcome than the next-best use of that dollar.

Build a portfolio operating cadence

Portfolio strategy should change more slowly than company data, but it cannot remain frozen for ten years. Use a cadence that separates data collection from strategy changes.

Monthly: keep the decision inputs current

Track the minimum company signals needed for capital decisions: cash runway, financing timing, revenue or usage trend, major hiring changes, product milestones, ownership, latest valuation, and the fund's remaining reserve.

Do not collect a KPI because a dashboard supports it. Each recurring field should inform a defined question: follow on, release reserves, increase support, prepare an exit, or revise the portfolio forecast.

Quarterly: review the portfolio as one capital pool

The venture capital portfolio review should compare actual deployment with the original plan:

- Initial checks completed versus plan.

- Capital deployed and time elapsed.

- Ownership at entry and current estimated ownership.

- Reserve committed, reserved, released, and unallocated.

- Concentration by company, stage, sector, geography, and common risk factor.

- Expected financing needs over the next four quarters.

- Companies that can return a meaningful share of the fund under current ownership.

This is where company signals become fund decisions. A dashboard that shows burn and ARR but never changes reserve or pacing decisions is reporting, not portfolio management.

Annually: reset assumptions without rewriting history

Review whether valuations, round sizes, graduation rates, exit timelines, allocation access, or team capacity have changed enough to update the strategy. Preserve the original plan alongside the revision so LPs and the investment team can see what changed and why.

Maintain an exception log

For every check outside policy, record the broken rule, decision owner, reason, expected portfolio effect, and review date. The venture capital investment committee can approve exceptions, but repeated exceptions usually mean the strategy itself needs revision.

Common portfolio strategy mistakes

Optimizing company count in isolation

A target of 30 companies says little without check size, ownership, stage, reserves, and sourcing capacity. Solve the full system.

Confusing ownership at entry with ownership at exit

Initial ownership looks impressive in a deck. Fund returns depend on the stake retained after employee option pools, new rounds, secondaries, and other dilution. Model more than one dilution path.

Treating reserves as static

Equal reserves for unequal companies feel disciplined but can waste capital. Review reserves as evidence changes, and document reallocation rules before the decision becomes emotional.

Allowing every exception to become precedent

One off-thesis deal can be a rational exception. Five off-thesis deals are a new strategy without the honesty of calling it one. Track exceptions and review patterns.

Monitoring companies without managing the fund

Company KPIs are inputs. Portfolio decisions are outputs. Define which signal triggers which capital, support, or pacing decision.

Managing “my deals” instead of one portfolio

Partner ownership improves accountability, but it can bias reserve decisions. A portfolio-wide owner or committee should compare every capital request against the same opportunity-cost standard.

Using precision to hide uncertainty

A model with six decimal places is still only a set of assumptions. Use ranges, show sensitivities, and name the variables that the team can actually control.

What candidates should understand about portfolio strategy

Portfolio strategy appears in analyst and associate work even when the job description does not use the phrase.

Before an interview, research the firm's stage, sector, typical check, lead/follow behavior, fund size, portfolio count, and follow-on pattern. The Venture Capital Careers companies directory can help you build a shortlist of firms, but verify important claims against each firm's own current materials.

Then connect the strategy to likely work products:

- A market map tests whether the thesis has enough investable opportunities.

- A sourcing pipeline shows whether planned deployment is achievable.

- An investment memo tests ownership, dilution, upside, and concentration.

- An IC model shows how a proposed check affects remaining capital and reserves.

- A portfolio review turns company updates into follow-on and support decisions.

Strong interview answers do not propose a universal “best” portfolio. They identify the fund's constraints, reconcile the math, and explain the tradeoff. If you are ready to apply that thinking on the job, browse current roles on the Venture Capital Careers job board.

Frequently asked questions

How many companies should be in a venture capital portfolio?

There is no universal ideal. The number must reconcile investable capital, average first check, ownership target, reserve budget, stage, sourcing access, and team capacity. Calculate company count from those constraints rather than choosing it first.

What is the difference between portfolio construction and portfolio management?

Portfolio construction designs the target portfolio before and during deployment. Portfolio management compares actual investments with that plan and changes pacing, reserves, support, and exit scenarios as evidence develops.

How much should a VC fund reserve for follow-ons?

There is no ratio that fits every fund. Reserve needs depend on stage, ownership goals, expected future rounds, pro rata access, fund size, and whether the manager prefers more first checks or more capital behind proven winners. Whatever the amount, define who can earn it and when it can be released.

Is a larger VC portfolio always more diversified?

No. More companies can reduce dependence on one selection, but correlated exposure may remain high, and smaller stakes can limit the value of an outlier. Evaluate company count together with ownership and shared risk factors.

How often should a VC portfolio strategy be reviewed?

Keep company data current monthly, review fund-level allocation and reserves quarterly, and revisit major model assumptions at least annually or after a material market or fund change.

Make the strategy usable

A useful venture capital portfolio strategy is not a target company count or a one-time spreadsheet. It is a short set of linked assumptions and decision rules that the team can use in every investment committee and portfolio review.

Start with one page: investable capital, stage, first-check budget, ownership range, reserve policy, pacing, concentration limits, exception rights, and review dates. Pressure-test the arithmetic, then keep the original plan visible when reality forces a change. The quality of the strategy shows up in better decisions, not in how precise the model looks.