Venture Capital Portfolio Review: Process, Metrics, and Template

Learn how venture capital portfolio reviews work, what metrics firms track, who leads the meeting, and how review decisions turn into founder support.

A venture capital portfolio review is a recurring internal meeting where a fund reviews portfolio company performance, identifies risks, decides where partners or platform teams should help, and updates follow-on or reserve priorities. A good review is not a passive status meeting. It should end with decisions, owners, and follow-up actions.

For candidates, portfolio reviews are useful because they show how venture work continues after a deal closes. For funds, they are one of the main rituals that turn scattered founder updates, board decks, investor notes, and KPI reports into operating judgment.

What is a venture capital portfolio review?

A venture capital portfolio review is a structured review of active portfolio companies. The fund looks across the portfolio and asks: which companies are compounding, which need help, which may need more capital, and which assumptions have changed since the last review?

It is different from a board meeting. A board meeting is company-specific and includes company leadership and directors. A portfolio review is usually internal to the fund. It is also different from an investment committee. An investment committee decides whether to invest in a new or follow-on opportunity; a portfolio review monitors what already exists and prepares the team for better follow-on, support, and reporting decisions.

It is also not the same as LP reporting. LP reporting turns fund and portfolio performance into investor communication. A portfolio review is the working session that helps the team understand what is actually happening before that information is summarized for LPs.

The strongest reviews have a clear operating question: what should the fund do differently because of what it learned?

What a portfolio review is supposed to decide

The most useful portfolio reviews produce a decision, not just a spreadsheet discussion. The decision does not always need to be dramatic. Sometimes the right answer is "monitor." But the meeting should make the next step explicit.

Common outputs include:

| Decision | What it means | Typical next action |

|---|---|---|

| Monitor | Company is broadly on plan | Keep cadence, update notes, watch agreed metrics |

| Support | Company is healthy but needs help | Make introductions, help hiring, support GTM, share operators |

| Diagnose | Performance is unclear or deteriorating | Schedule partner follow-up, request more data, review root causes |

| Reserve / follow-on | Company may need capital or deserves more ownership | Update reserve model, prepare follow-on memo, discuss round timing |

| Escalate | Risk is material | Prepare board discussion, financing plan, restructuring support, or strategic options |

This is where the review becomes more than reporting. A partner may decide to spend more time with a founder. A platform lead may commit to a hiring sprint. A finance or portfolio operations person may flag cash runway. An associate may prepare a follow-on note. The review creates the operating queue for the fund.

Who leads the review and who participates

The owner depends on fund size and operating model.

At a small seed fund, a partner may lead the review directly because the team is compact and every company matters. At a larger fund, the meeting may be run by a platform leader, portfolio operations manager, finance lead, chief of staff, or investor who owns portfolio monitoring. The best owner is the person with the broadest view across company updates, firm priorities, and follow-up actions.

Typical participants include:

| Role | What they contribute |

|---|---|

| Partner or GP | Judgment on company trajectory, founder support, reserves, and board-level issues |

| Associate or principal | Company notes, metrics synthesis, market context, follow-on preparation |

| Platform or portfolio operations | Founder support needs, hiring, GTM, community, benchmarks, and action tracking |

| Finance or fund operations | Valuations, ownership, runway, reserves, reporting, fund-level metrics |

| Investor relations | LP communication context and reporting implications |

Not every review needs every person. A weekly operating review may be small and action-focused. A quarterly full-portfolio review may include the broader partnership and finance team.

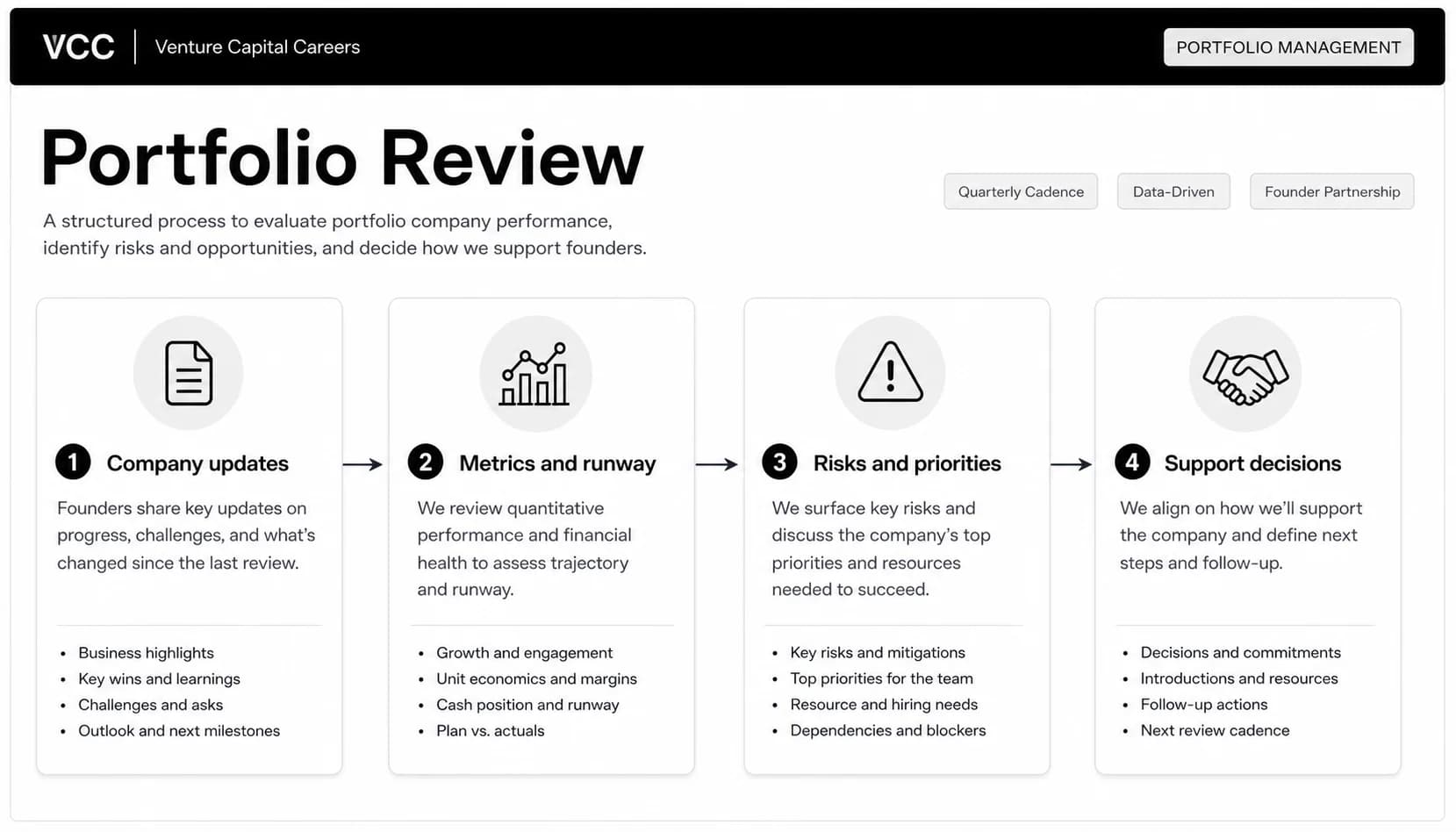

The VC portfolio review process

A practical portfolio review usually has six steps.

First, collect company updates. These may come from founder updates, board decks, monthly KPI forms, emails, CRM notes, or partner conversations. The key is consistency. If one company reports ARR, burn, and runway while another gives only narrative updates, the team cannot compare risk or progress cleanly.

Second, normalize the metrics. Early-stage companies are messy, so the goal is not false precision. The goal is to make each company legible: current stage, last round, cash runway, growth signal, customer signal, hiring priorities, major risks, and next financing context.

Third, identify exceptions before the meeting. The team should know which companies deserve real discussion. A company that is on plan may need five minutes. A company with three months of runway, a missed sales plan, or a founder conflict needs more time.

Fourth, review company-by-company. The best discussions start with what changed. Did customer demand improve? Did churn increase? Did a strategic hire slip? Did a fundraising timeline move forward? Did a market assumption break?

Fifth, assign support actions. This is where platform, partner, and investor work becomes specific. "Help with hiring" is not enough. "Introduce two VP Sales candidates by July 15" is a useful action.

Sixth, update records and follow up. The review should leave behind a source of truth: action owners, next review date, support commitments, reserve implications, and open questions.

Portfolio software vendors often emphasize data collection and dashboards. That matters. Visible frames portfolio review meetings around structured updates, review cadence, and portfolio company dashboards. Standard Metrics emphasizes benchmarks as a way to add market context to internal reviews. Those are useful inputs, but the operating discipline is broader than any one tool: the team still has to decide what the data changes.

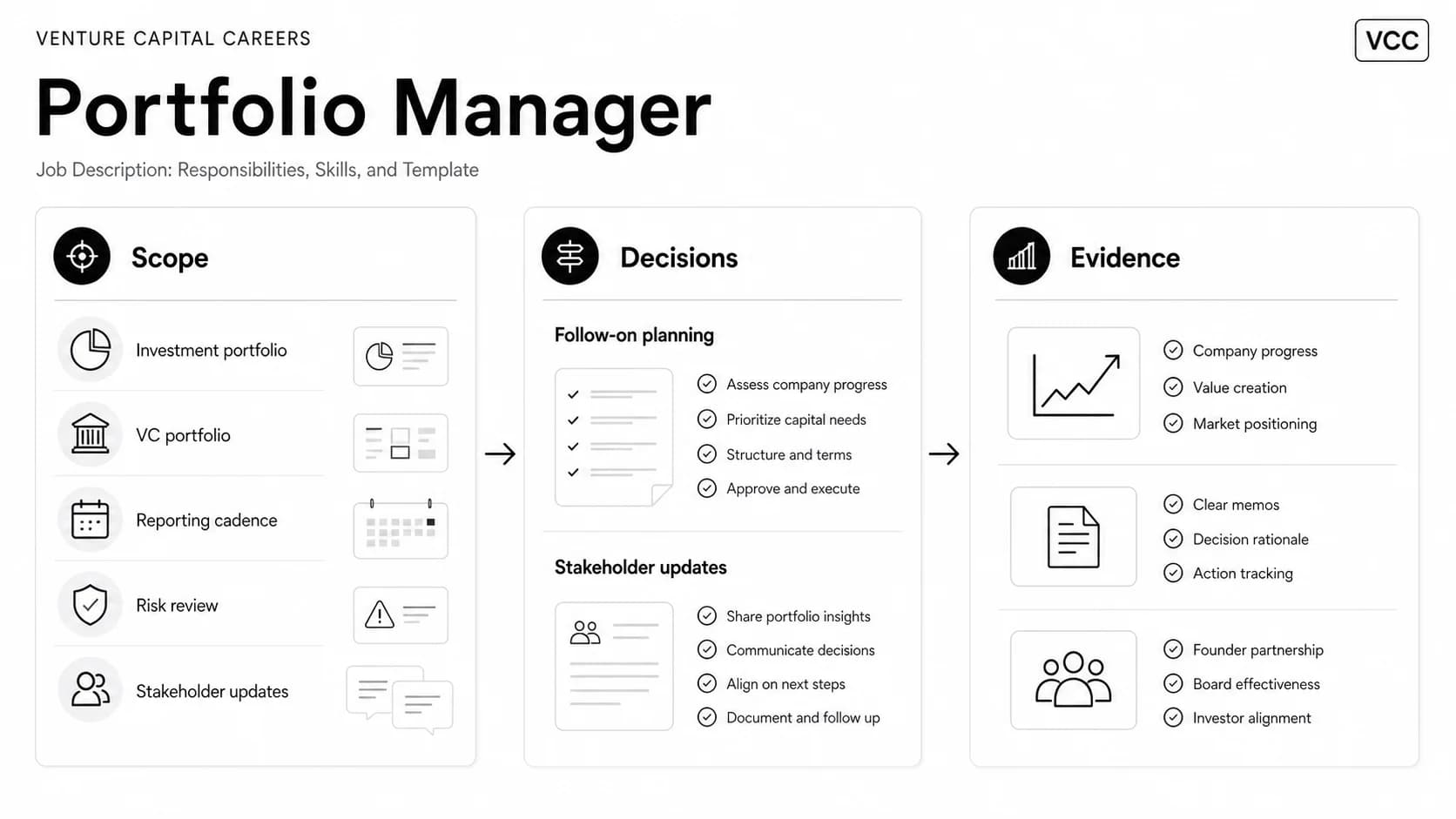

Portfolio review agenda template

Use this agenda when building a lightweight review process for a VC fund.

| Agenda item | Owner | Core question | Output |

|---|---|---|---|

| Portfolio overview | Review lead | What changed across the portfolio since the last review? | Top themes and exception list |

| Company exceptions | Partner / associate | Which companies need real discussion? | Prioritized company list |

| Metrics review | Finance / portfolio ops | Which metrics changed enough to matter? | Growth, runway, margin, retention, plan variance notes |

| Support needs | Platform / partner | Where can the fund help? | Hiring, GTM, customer, product, fundraising, or board actions |

| Follow-on and reserves | Partner / finance | Which companies may need more capital or ownership decisions? | Follow-on watchlist and memo owners |

| Risk review | Partner / review lead | What could break the plan? | Risk owner and next check-in |

| Action log | Review lead | Who owns each next step? | Named owner, deadline, and follow-up date |

The agenda should be short enough to repeat. A portfolio review that requires a custom deck every time will eventually become too heavy to maintain. A better system uses a consistent company one-pager, a small set of core metrics, and a living action log.

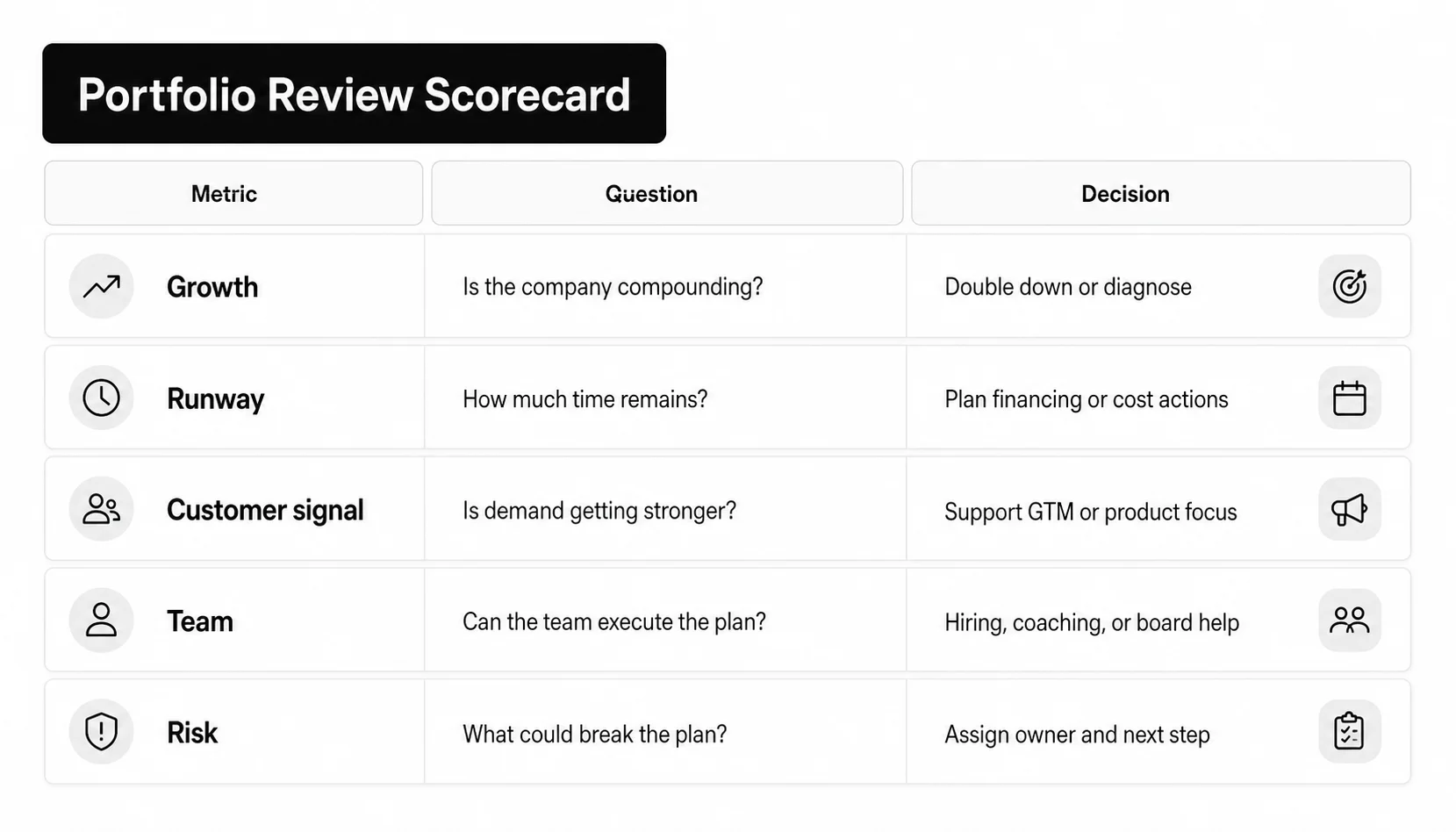

Metrics to review by company stage

The wrong metric at the wrong stage creates bad discussion. A pre-seed company should not be judged like a Series B company, and a growth company should not hide behind early-stage narrative.

| Company stage | Metrics and signals to review | What the fund is trying to learn |

|---|---|---|

| Pre-seed / seed | Founder progress, product milestones, design partners, usage frequency, early revenue, hiring, runway | Is the company learning fast enough and finding a real wedge? |

| Series A / B | ARR or revenue growth, net retention, gross margin, pipeline quality, sales cycle, burn multiple, team buildout | Is the company turning early traction into repeatable growth? |

| Growth | Revenue scale, retention, margin profile, sales efficiency, expansion, leadership depth, cash planning | Is the company durable enough to support larger follow-on decisions? |

| Watchlist / underperforming | Runway, burn, churn, missed plan, founder alignment, financing options, customer concentration | What could break the company, and what intervention is realistic? |

Qualitative signals matter too. A company may have acceptable metrics but a weakening founder relationship, stalled executive search, or customer segment problem. Another may miss a quarterly plan but show stronger product pull than the numbers suggest. The review should make room for judgment while still forcing the team to name evidence.

Common mistakes in VC portfolio reviews

The first mistake is reviewing every company the same way. A fund with 60 portfolio companies cannot spend equal time on all of them. The review should separate companies that are on plan from companies that need decisions.

The second mistake is using stale data. A beautiful dashboard from last quarter can be worse than a messy founder update from last week if the company is running out of cash. Data freshness should be visible in the review pack.

The third mistake is turning the meeting into status theater. If each investor reads updates aloud, the meeting is doing work that should have happened beforehand. Discussion time should go to exceptions, judgment, and decisions.

The fourth mistake is failing to assign owners. Portfolio support sounds helpful until everyone assumes someone else is handling it. Every action should have a person and a date.

The fifth mistake is confusing LP reporting with founder support. LPs need accurate fund communication. Founders need useful help. A portfolio review can inform both, but the meeting should not become an LP-reporting exercise at the expense of company-level action.

What candidates should know about portfolio reviews

Portfolio reviews show how different VC roles actually work.

An associate may be asked to maintain company notes, update performance summaries, prepare market context, or draft a follow-on memo. A principal may own deeper company discussion and partner recommendations. A platform hire may translate repeated founder needs into hiring, GTM, community, or operator-support programs. A portfolio manager or finance-oriented role may focus on data quality, valuations, runway, reserves, and reporting.

If you are interviewing for a portfolio, platform, associate, or principal role, be ready to discuss:

- how you would identify which companies need discussion;

- which metrics matter by stage;

- how you would separate a temporary miss from a real risk;

- how you would turn a founder update into a partner-ready summary;

- how you would track follow-up actions after the meeting;

- how portfolio support differs from investment selection.

For broader role context, compare this article with the portfolio manager job description, venture capital platform role, and venture capital investment committee guides.

How VCC readers can use this workflow

If you are a job seeker, portfolio review knowledge helps you read job descriptions more accurately. A role that mentions portfolio monitoring, founder support, KPI tracking, board materials, or investor reporting may involve this workflow. Use the Venture Capital Careers job board to compare active roles across platform, portfolio operations, investor, and finance titles.

If you are researching firms, use the companies directory to understand each fund's stage, geography, and portfolio model. A seed fund with a small team will run portfolio reviews differently from a multi-stage fund with dedicated platform and finance functions.

If you are hiring, be specific about the portfolio review work in the job description. Candidates can evaluate the role better when they know whether the work is mostly data collection, founder support, finance, investor relations, platform operations, or follow-on analysis. When the role is ready, employers can post a VC job on Venture Capital Careers.

FAQ

How often should a VC firm run portfolio reviews?

Many firms use a quarterly portfolio review for the full portfolio, with more frequent weekly or biweekly check-ins for watchlist companies or action items. The right cadence depends on portfolio size, fund stage, and how actively the firm supports companies.

Is a portfolio review the same as an investment committee?

No. An investment committee decides whether to make an investment or follow-on investment. A portfolio review monitors existing investments and decides what support, risk management, or follow-up work is needed.

What is the difference between portfolio review and LP reporting?

Portfolio review is an internal operating process. LP reporting is external communication to fund investors. A good portfolio review improves LP reporting because the fund has cleaner context, but the two workflows have different audiences.

What does a portfolio manager do in a VC portfolio review?

A portfolio manager may prepare company data, track performance, update valuations or ownership records, monitor runway, coordinate reporting, and maintain the action log. The exact role depends on whether the fund uses "portfolio manager" to mean finance, platform, portfolio operations, or investment-team support.

Turn portfolio updates into decisions

A portfolio review is only useful if it changes what the fund does next. The best reviews make company performance visible, focus partner time on exceptions, and turn vague concern into owned actions.

For candidates, understanding this workflow is a signal that you know venture work extends beyond sourcing and deal memos. For funds, it is a way to make portfolio support more repeatable instead of relying on memory, scattered emails, or the loudest issue in the room.