Right of First Refusal (ROFR): How It Works in Venture Capital

A practical explanation of ROFR in startup share transfers, including the process, a worked example, related rights, and a clause-review checklist.

A right of first refusal (ROFR) gives a company, investor, or other holder the opportunity to buy existing shares before a covered shareholder sells them to a third party. In a typical startup transaction, the seller first develops an outside offer, then gives the ROFR holder a defined period to match the applicable terms.

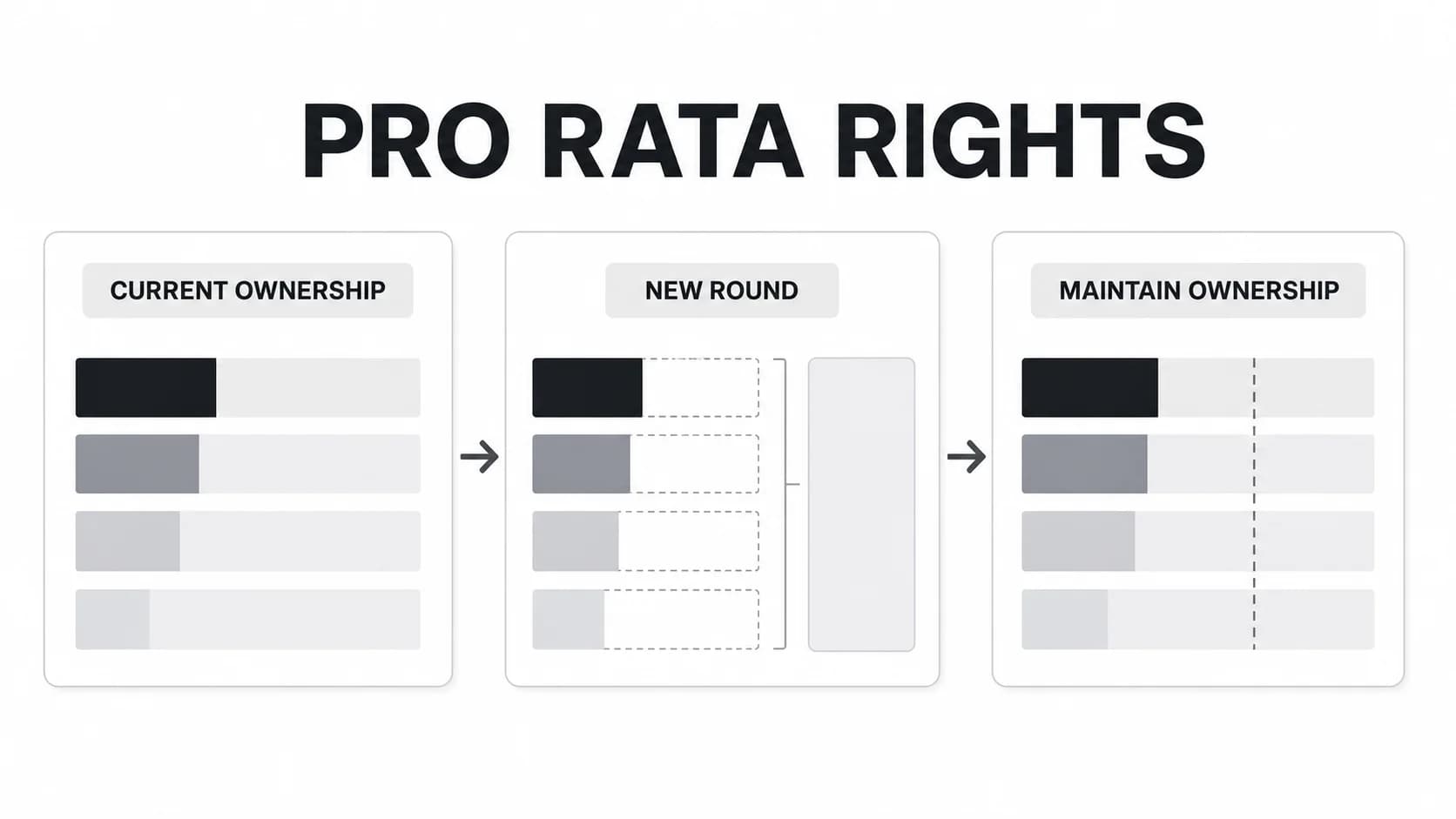

The distinction that matters most: a ROFR usually controls a transfer of existing shares. It does not, by itself, protect an investor from dilution when the company issues new securities. Pro rata rights or preemptive rights address that different problem.

Exact triggers, priorities, deadlines, exceptions, and remedies come from the signed documents and governing law. The explanations and examples below are practical education, not legal or tax advice.

How a ROFR works in a startup share sale

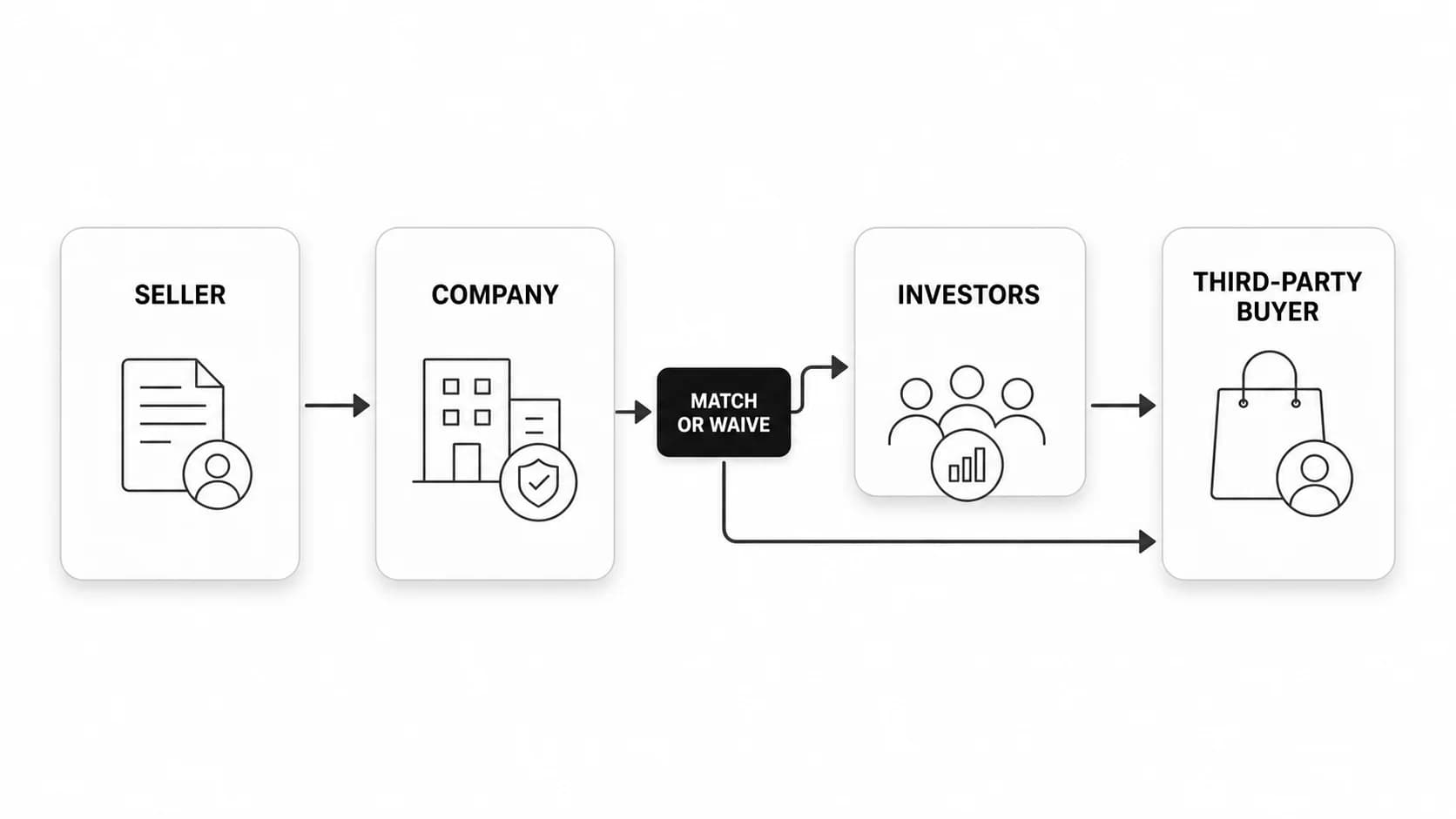

A startup ROFR usually becomes relevant when a covered shareholder—often a founder, executive, employee, or other “key holder”—wants to sell existing shares to an outside buyer. The exact order comes from the company’s bylaws, stock purchase or award agreement, and any stockholders’ or ROFR and co-sale agreement.

A common sequence looks like this:

- The seller obtains a bona fide third-party offer. The proposed buyer and seller agree on enough material terms to trigger the clause. Price matters, but so can payment timing, representations, closing conditions, and non-cash consideration.

- The seller delivers a transfer notice. The notice identifies the buyer, shares, price, and other terms required by the governing documents.

- The company gets its decision window. If the company holds the first right, it can buy some or all of the offered shares, subject to the agreement, available funds, and corporate approvals.

- Investors or other holders get the next decision. The documents may let specified investors purchase shares the company did not take, sometimes with an oversubscription process if demand exceeds the remainder.

- The sale closes or the right is waived. If the holders decline or the exercise period expires, the seller may close with the proposed buyer—but usually only within a stated period and on terms no more favorable to that buyer.

Cooley GO notes that private-company common stock ROFRs may sit in bylaws, award agreements, or other contracts, and that companies increasingly layer separate board-approval rights onto transfers. That means a ROFR waiver may be necessary without being sufficient: the board or another rights holder may still need to consent.

If the outside deal changes materially in the buyer’s favor—say the price falls or the seller accepts slower payment—the seller may have to restart the notice process. The clause, not a generic ROFR definition, determines whether a re-offer is required.

Worked example: a founder sells 100,000 shares

Assume a founder receives an outside offer to buy 100,000 common shares for $4.50 per share, payable in cash at closing. The company has a first-priority ROFR; specified investors have a secondary ROFR over any shares the company does not purchase.

The founder sends a compliant notice. Three outcomes illustrate why the agreement matters:

| Outcome | What happens |

|---|---|

| Company exercises in full | The company buys all 100,000 shares for $450,000 on the required terms. The outside buyer receives no shares. |

| Company takes 60,000; investors take 40,000 | This works only if the documents permit partial exercise and allocate the remainder to the investors. The founder still sells 100,000 shares, but to the ROFR holders. |

| Everyone declines | The founder may sell to the named buyer during the permitted closing window, on the notified terms. A lower price or another buyer-favorable change may require a new notice. |

The ROFR does not guarantee an internal buyer. A company or investor must be willing and able to fund the purchase. Cooley’s founder-stock discussion makes the same practical point: the right controls ownership only when a holder can actually pay for the shares (Cooley GO).

The example also shows why “matching the price” is incomplete shorthand. If the outside offer includes an earn-out, installment payments, indemnity obligations, or a bundle of assets, matching may be difficult. Well-drafted documents say how to treat non-cash or unusual consideration, and complex cases belong with company counsel.

None of the numbers above are market standards. Exercise windows, allocation rules, closing mechanics, and company repurchase constraints vary by document and jurisdiction.

A ROFR is not the same as anti-dilution or pro rata rights

The most important distinction is the transaction itself:

| Question | Secondary transfer | Primary issuance |

|---|---|---|

| What moves? | Existing shares move from one holder to another | The company issues new shares or securities |

| Who receives the cash? | The selling shareholder | The company |

| Does the transaction itself dilute other holders? | No; no new shares are created | It can, because the outstanding share count increases |

| Which right is usually relevant? | ROFR, co-sale, transfer restriction, board consent | Pro rata or preemptive right; sometimes anti-dilution protection |

Carta’s private-secondary explainer confirms that a direct secondary transfers existing shares and does not itself dilute the ownership percentages of other shareholders. By contrast, Orrick’s financing-document overview places future-issuance rights in the Investors’ Rights Agreement and transfer restrictions in the separate ROFR and Co-Sale Agreement.

That distinction changes the diligence question:

- If a founder or employee sells existing shares, check the ROFR, co-sale provisions, transfer restrictions, and board approvals.

- If the company raises a new round, check pro rata rights, shareholder preemptive rights, and the financing documents.

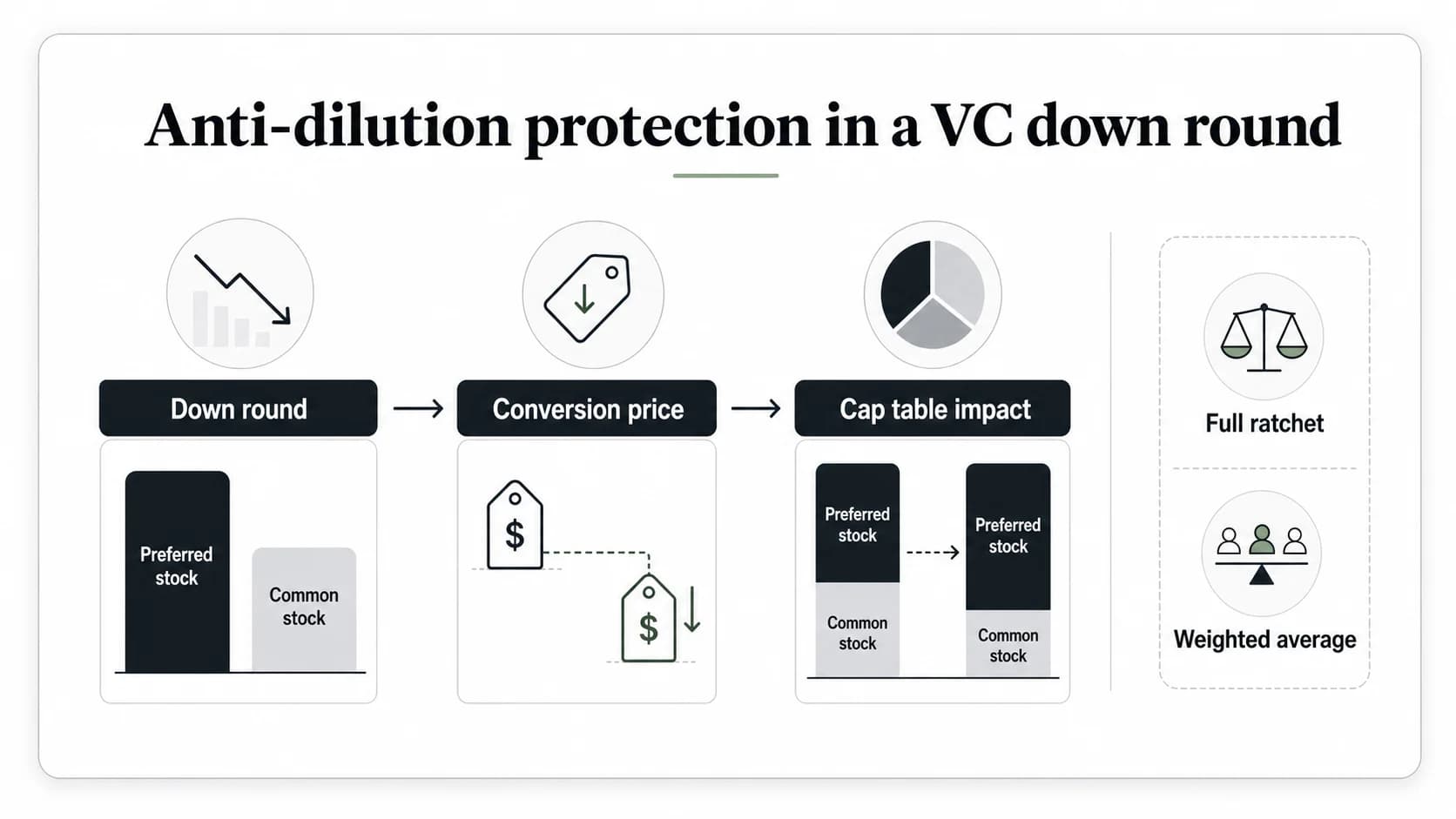

- If a down round changes the conversion economics of preferred stock, review the anti-dilution provision.

People sometimes use “preemptive right” broadly enough to include a ROFR. In venture documents, that shorthand can hide the key issue. Always ask whether the holder is getting priority over existing shares being transferred or new securities being issued.

ROFR versus adjacent rights

Preferential rights often appear together, but they solve different problems.

| Right | Trigger | Holder can do | Main purpose |

|---|---|---|---|

| Right of first refusal (ROFR) | Covered seller receives or is ready to accept a third-party offer | Match the specified transaction terms | Control transfers of existing shares |

| Right of first offer (ROFO) | Owner decides to sell, before a third-party deal is negotiated | Make the first offer or negotiate first | Give priority without making an outside buyer a stalking horse |

| Pro rata / preemptive right | Company proposes a new securities issuance | Buy part of the new issuance | Maintain ownership through a financing |

| Co-sale / tag-along right | Covered holder proposes a third-party sale and the ROFR is not fully exercised | Participate as a seller | Share a liquidity opportunity |

| Board approval right | A shareholder requests approval for a transfer | Approve or reject under the governing standard | Control the shareholder base even if no one buys |

| Purchase option | Contractual exercise event or window occurs | Buy on pre-agreed mechanics without first matching an outside offer | Create a direct purchase right |

ROFR and co-sale are complements, not synonyms. A ROFR gives someone the chance to be the buyer. A co-sale right gives an investor or other holder the chance to join the seller’s transaction. Cooley’s worked founder-stock example shows how a co-sale can reduce the number of shares the original seller may transfer so other eligible holders can participate (Cooley GO).

ROFR and ROFO differ mainly in timing. Under a typical ROFR, the seller first develops a third-party deal and then gives the holder a chance to match. Under a ROFO, the holder gets the first negotiation opportunity before the seller shops the asset. That makes a ROFR stronger for the holder but potentially more frustrating for an outside buyer that has spent time establishing the deal. Harvard Business Services describes this as a stalking-horse problem: the buyer’s work can set terms that the holder later takes.

Do not rely on the label alone. Some contracts call a first-offer process a ROFR or define hybrid mechanics. Read the trigger, notice, exercise, and closing provisions.

What to check in a ROFR clause

Use this checklist to understand a clause before negotiating or approving a private-company share transfer:

- Covered sellers: Does the right apply to founders, employees, all common holders, major holders above a threshold, or every shareholder?

- Covered securities: Common stock only, preferred stock, options after exercise, convertible securities, or any equity interest?

- Trigger: Must there be a bona fide third-party offer, a signed letter of intent, definitive documents, or only a decision to sell?

- Notice: What details and supporting documents must the seller provide, and how must notice be delivered?

- Priority: Does the company decide first? Which investors or other holders decide second?

- Allocation: Can holders exercise partially? Are remaining shares allocated pro rata, and is oversubscription allowed?

- Matching standard: Must the holder match every material term or only price? How is non-cash consideration valued?

- Exercise and closing windows: When does each clock start, and what happens if a holder elects to buy but fails to close?

- Permitted transfers: Are estate-planning, family, trust, affiliate, or de minimis transfers exempt? Does the transferee remain bound?

- Third-party sale window: After waiver, how long does the seller have to close with the named buyer?

- Changed terms: Which buyer-favorable changes force a new notice?

- Assignment and termination: Can the right be assigned, and does it end at an IPO, acquisition, agreement termination, or another event?

- Other approvals: Is board consent, securities-law compliance, or another contractual waiver still required?

Shutts & Bowen’s ROFR/ROFO analysis emphasizes duration, response time, pricing, persistence, and written waiver evidence (Shutts & Bowen). For venture financings, the NVCA model legal documents are a useful market reference, but a company’s signed documents—not a model—control its transaction.

A checklist is not a substitute for legal review. ROFR enforceability, remedies, repurchase authority, securities compliance, and tax consequences depend on the facts and governing law.

Benefits and risks by stakeholder

| Stakeholder | Potential benefit | Main risk or cost |

|---|---|---|

| Company | Keeps more control over who joins the cap table; may consolidate ownership | Must fund a purchase to exercise; delays and administration can strain liquidity |

| Existing investor | Can prevent an unwanted buyer or increase an existing position | May need to decide and wire funds quickly; passing can reveal lack of interest |

| Founder or employee seller | Can establish market terms with an outside buyer | Transfer takes longer and the buyer may discount its offer for execution risk |

| Prospective buyer | Can access hard-to-buy private shares if rights are waived | May spend on diligence and negotiation only to lose the deal to a ROFR holder |

| Other shareholders | May benefit from a controlled cap table and, if covered, co-sale access | The ROFR alone does not give them liquidity or protect them from new-share dilution |

A ROFR can preserve cap-table control, but it is not costless control. Direct secondary sales are already slower and less standardized than public-market trades. Carta describes private secondaries as opaque transactions with transfer restrictions, inconsistent pricing, and extended settlement cycles. A ROFR adds another decision path.

For the selling shareholder, the buyer’s “stalking horse” concern is real. If the buyer believes its negotiated price and diligence will simply be handed to an insider, it may offer less, insist on expense reimbursement, or walk away. A ROFO can reduce that risk because the holder acts before the outside negotiation, but it gives the holder less certainty about the market-clearing terms.

For companies, a ROFR is only one layer of a secondary policy. Board consent, information-access concerns, tax and securities review, and a preference for company-sponsored liquidity may matter just as much. The best clause is not automatically the strongest restriction; it is the one that balances cap-table control with a credible path for appropriate shareholder liquidity.

A practical review workflow before a secondary sale

Before a founder, employee, or investor promises shares to an outside buyer:

- Collect the governing documents. Review the certificate or charter, bylaws, stock purchase or award agreement, Investors’ Rights Agreement, ROFR and Co-Sale Agreement, voting agreement, stock legends, and any later amendments or waivers.

- Classify the transaction. Confirm that this is a transfer of existing shares—not a new company issuance, option exercise, tender offer, company repurchase, or acquisition.

- Map every gate. List the ROFR priority, co-sale rights, board consent, company approval, securities restrictions, and any platform or broker requirements.

- Compare complete terms. Capture the buyer’s identity, share class, quantity, price, payment form, timing, conditions, representations, and side arrangements.

- Build the notice calendar. Record delivery method, exercise deadlines, allocation steps, funding deadlines, outside closing window, and any re-offer trigger.

- Confirm execution capacity. A holder that exercises needs funds and approvals; a seller and buyer need a closing plan that respects every restriction.

- Use counsel and tax advisers. Cooley’s secondary-sale overview flags securities, tax, 409A, corporate-law, antitrust, and cross-border issues that can arise depending on the transaction (Cooley GO).

Common mistakes

- Calling a ROFR anti-dilution protection. It usually governs existing-share transfers, not new issuances.

- Checking only one agreement. The ROFR may sit in the bylaws while board consent or co-sale rights sit elsewhere.

- Matching only the headline price. Payment form, timing, conditions, and non-cash consideration can be material.

- Treating one waiver as permanent. A waiver often applies only to the notified transaction and closing period.

- Ignoring permitted transfers. A family or trust transfer may be exempt but still bind the recipient.

- Starting expensive diligence too early. A buyer should understand the ROFR and obtain evidence of waiver or expiration before assuming it can close.

- Missing a changed-term re-offer. A buyer-favorable amendment can restart the process.

The purpose of the workflow is not to make every seller avoid secondaries. It is to establish the rights and decision path before parties spend money or make commitments they cannot honor.

Frequently asked questions

Does a letter of intent trigger a right of first refusal?

Sometimes. A non-binding expression of interest may be too preliminary, while a signed LOI with agreed material terms may be enough under a particular clause. The agreement’s definition of a bona fide offer, the binding provisions in the LOI, and the specificity of the deal terms control. Sellers should not assume they can wait until definitive documents are signed.

How long does a right of first refusal last?

The duration and each exercise window are contractual. A ROFR may last until an IPO, acquisition, agreement termination, a specified date, or another event. The holder’s response window may be much shorter. There is no universal 30- or 60-day rule for startup shares.

Can a ROFR apply to buying a business?

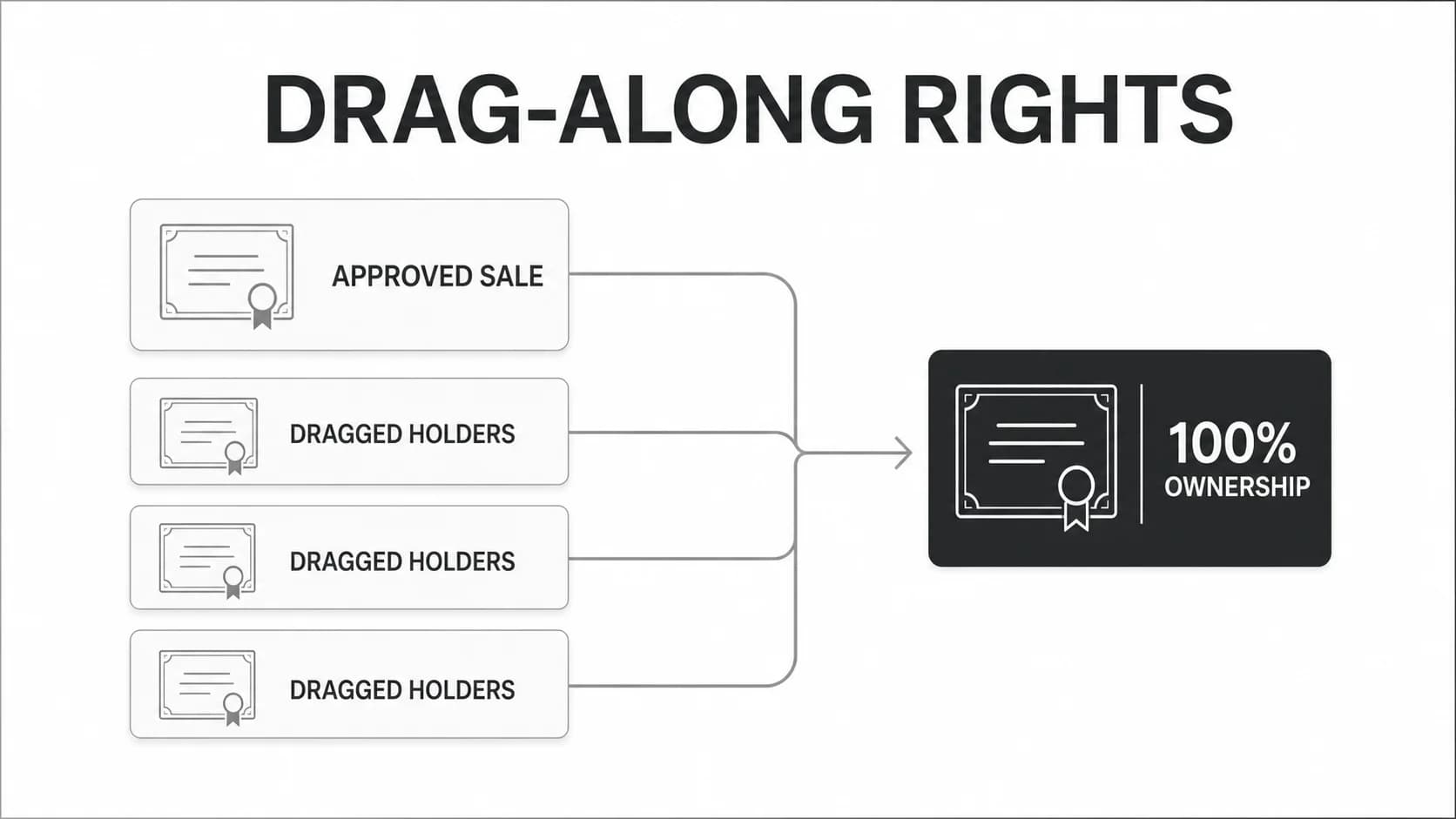

Yes. A ROFR can cover an equity interest, business asset, joint-venture opportunity, real estate, or another transaction. But a right over a founder’s shares is not automatically a right to buy the entire company or its assets. Check the defined asset, covered transaction, and trigger. Whole-company sale rights may instead appear in voting, drag-along, investor, or acquisition agreements; see VCC’s explanation of drag-along rights.

What happens if the holder declines?

The seller can usually proceed with the notified buyer during a specified period and on the notified terms. If the sale does not close in time or changes materially in the buyer’s favor, the seller may have to re-offer the shares.

What happens if someone violates a ROFR?

The remedy depends on the contract, governing law, and transaction status. Possible consequences can include damages, an injunction, refusal by the company to record the transfer, or other contractual relief. A party facing an actual breach should obtain jurisdiction-specific legal advice immediately.

Is a right of first refusal good or bad?

It is useful when cap-table control is worth the liquidity friction. Companies and investors gain a chance to block or internalize a transfer; sellers and outside buyers accept more delay and execution risk. A narrow clause with clear triggers, short workable deadlines, sensible permitted transfers, and coordinated co-sale and board-approval mechanics is usually easier to operate than an open-ended restriction.

The practical takeaway

Start by classifying the transaction. If existing shares are moving from a founder, employee, or investor to a new buyer, map the ROFR, co-sale rights, transfer restrictions, and board approvals before anyone commits to a closing. If the company is issuing new securities, move to the pro rata, preemptive-rights, and financing documents instead.

That simple split prevents the most common conceptual error and makes the rest of the clause review far easier. For candidates building transaction fluency for investing roles, Venture Capital Careers publishes practical explainers on term sheets and cap tables, and lists current venture capital roles.