Corporate Venture Capital: Definition, Examples, Benefits, and Risks

Corporate venture capital is startup investing by large companies for both strategic advantage and financial return. Learn how CVC works, examples, benefits, risks, and career implications.

Corporate venture capital is startup investing by an established company, usually through a dedicated investment team or corporate venture arm. A CVC investor may want financial return, but it is also investing for strategic reasons: market insight, access to new technology, commercial partnerships, future acquisition options, or a stronger ecosystem around the parent company's core business.

That strategic motive is what makes CVC different from traditional venture capital. A normal VC fund is accountable mainly to financial limited partners. A corporate venture investor is also accountable to a parent company with products, customers, distribution channels, and internal politics. That can make CVC unusually valuable for the right startup and unusually complicated for the wrong one.

What is corporate venture capital?

Corporate venture capital, often shortened to CVC, is the investment of corporate funds into external startups. The investor is usually a large operating company or a venture arm backed by that company. The startup typically gives the investor an equity stake, just as it would with a traditional VC firm.

The important distinction is motivation. CVC investors normally care about both financial return and strategic return. Strategic return can mean learning about a new market, finding future acquisition targets, supporting a partner ecosystem, testing emerging technology, or helping the parent company stay close to startup innovation.

Some CVC teams behave almost like independent venture funds. Others sit close to corporate development, product strategy, or business-unit leadership. That difference matters because it shapes decision speed, founder support, follow-on appetite, confidentiality expectations, and whether the investor can help after the round closes.

How corporate venture capital works

A corporate venture capital process usually starts with a strategic thesis. The parent company decides where outside innovation matters: AI infrastructure, healthcare, climate, fintech, cybersecurity, industrial automation, developer tools, or another market tied to its business.

The CVC team then sources startups, screens for stage and sector fit, performs diligence, and recommends investments. Some teams have independent investment committees. Others need approval from business-unit leaders, finance, legal, or corporate development. The more integrated the CVC team is with the parent company, the more the investment process may depend on internal stakeholders.

After investment, a good CVC investor should offer more than capital. The support can include customer introductions, distribution, product feedback, technical expertise, procurement guidance, regulatory context, or a path to a commercial partnership. The best CVC investors are clear about what they can actually deliver. The weakest ones imply strategic value but cannot mobilize the parent company after the wire hits.

Corporate venture capital vs traditional VC, strategic investors, and corporate development

These terms overlap, but they are not interchangeable.

| Investor or function | Primary goal | Capital source | Typical startup value | Main risk for founders |

|---|---|---|---|---|

| Corporate venture capital | Strategic value plus financial return | Parent-company balance sheet or CVC vehicle | Capital, market access, technical expertise, potential partnership | Slower process, conflicts, unclear follow-on support |

| Traditional venture capital | Financial return | Fund capital raised from limited partners | Capital, fundraising guidance, network, board support | Less strategic help from a specific operating company |

| Strategic investor | Business advantage from the investment or partnership | Operating company balance sheet | Commercial relationship, validation, customer access | Investment may serve the corporate strategy more than the startup's financing plan |

| Corporate development | M&A, partnerships, strategic transactions | Parent company | Acquisition or partnership path | May signal acquisition interest rather than independent venture support |

A CVC investor can also be a strategic investor. A corporate development team can also help source or evaluate CVC deals. The practical question is not the label; it is who controls the decision, what the investor wants after investing, and whether the startup can still operate independently.

Examples of corporate venture capital

Well-known CVC examples include GV, Salesforce Ventures, and Intel Capital. Each has a different relationship to the parent company's strategy, but all illustrate the same basic model: a large company uses venture investing to participate in startup innovation outside its own walls.

GV is often discussed as a more independent venture platform associated with Alphabet. Salesforce Ventures is closely tied to the enterprise software and cloud ecosystem around Salesforce. Intel Capital reflects the strategic importance of hardware, compute, semiconductors, software, and adjacent technology markets.

Other corporate venture arms exist across healthcare, financial services, industrials, energy, consumer, telecom, media, and transportation. The best examples are not necessarily the biggest names. The best fit is the investor whose parent company has a real reason to care about the startup's market and a credible way to help.

Benefits of corporate venture capital

For startups, the appeal is straightforward: CVC can combine capital with market access. A corporate investor may be able to introduce enterprise customers, validate a product category, explain procurement, share technical knowledge, or help the company understand a regulated industry.

For the parent company, CVC is a way to learn faster than internal R&D alone. A CVC program can create visibility into emerging technologies, business models, competitors, customer behavior, and possible acquisition targets. The British Business Bank emphasizes that CVC funding can bring expertise, networks, and contacts alongside financing.

The benefit is strongest when the strategic relationship is specific. "We know your sector" is not enough. "We can introduce you to three business-unit owners who buy this category" is more useful. "We can help validate your technical roadmap with our platform team" is more useful. "We invest in innovation" is usually too vague to matter.

Risks and red flags

CVC is not automatically better than traditional VC. A corporate investor can create real financing and operating risk if incentives are unclear.

Watch for these red flags:

- The CVC cannot explain whether it is investing for financial return, strategic access, future M&A, commercial partnership, or some mix of those goals.

- The parent company wants broad data rights, exclusivity, right of first refusal, or commercial restrictions that could limit future fundraising or customer growth.

- The investment process depends on too many internal approvals and cannot match the timing of the round.

- The CVC promises customer access but has no named business sponsor.

- The investor is not clear about follow-on reserves or whether it will support the company in the next round.

- The parent company competes with the startup's current or future customers.

- The CVC team is enthusiastic, but the business unit that would create strategic value is not involved.

Some of these issues can be solved in the term sheet and commercial agreement. Others are culture problems. A founder should diligence the parent company, not just the investment team.

How to evaluate a CVC investor

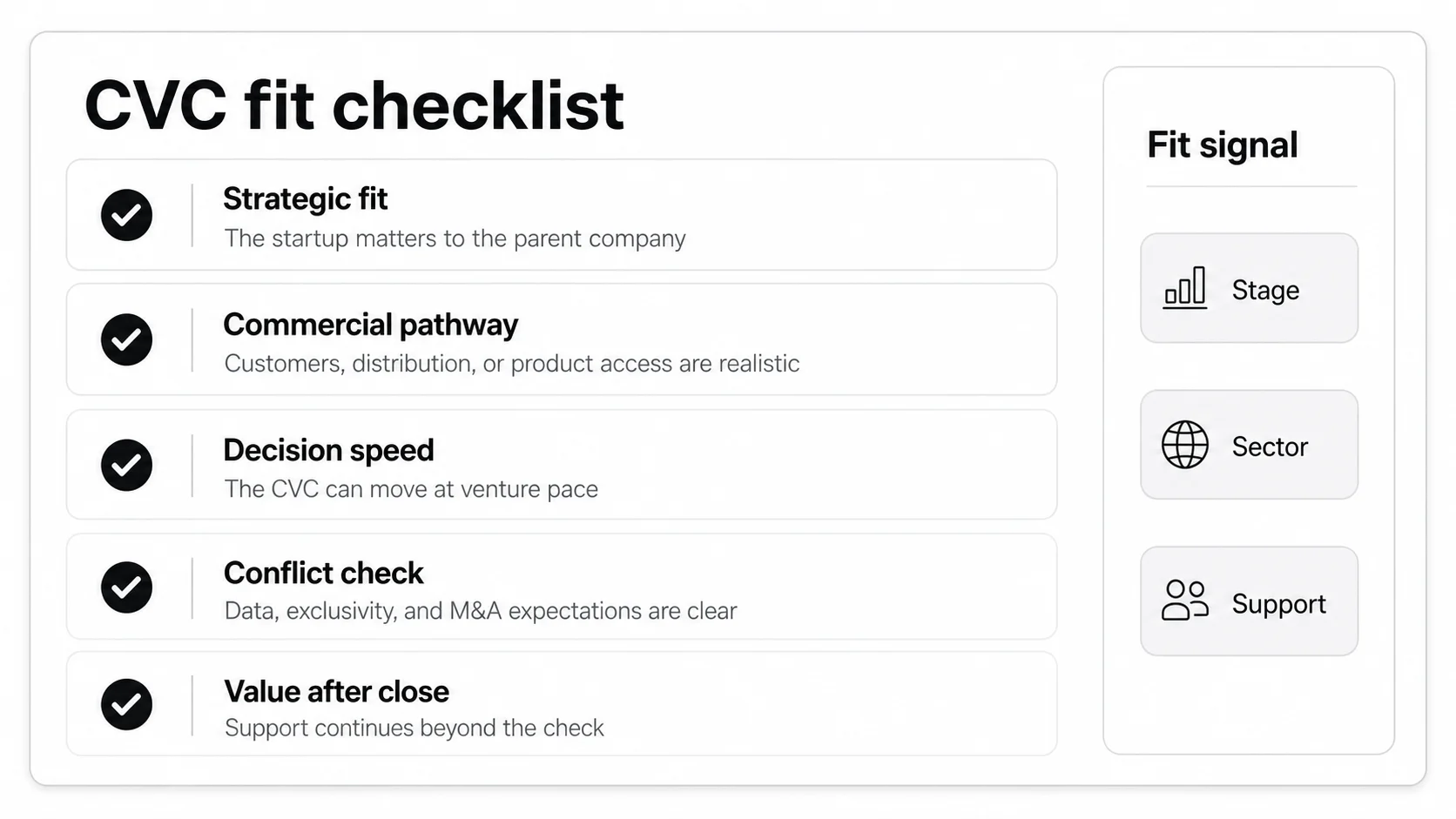

Founders should evaluate corporate venture capital investors on fit, speed, and post-investment value. The core question is whether the investor can help the company reach its next proof point without narrowing the startup's market too early.

Use five tests before accepting CVC money:

- Strategic fit: Is your company genuinely relevant to the parent company's market, customers, technology roadmap, or ecosystem?

- Commercial pathway: Can the investor name the customers, product teams, channels, or business-unit sponsors that could help?

- Decision speed: Can the CVC move at the pace of the round, or will internal approvals slow the process?

- Conflict check: Are data access, exclusivity, M&A expectations, customer conflicts, and information rights clearly bounded?

- Value after close: Will the investor still be helpful after the round, especially if the company misses plan?

If the answer is weak on two or more of those tests, the CVC may still be a useful participant, but it probably should not be the investor that defines the whole round.

What candidates should know about CVC roles

Corporate venture capital roles can look like traditional VC roles, corporate development roles, or strategy roles depending on the team. A CVC analyst or associate may source startups, map markets, evaluate founders, build investment memos, support diligence, monitor portfolio companies, and coordinate with business-unit leaders.

The main career question is how independent the CVC team is. More independent CVC funds tend to feel closer to traditional venture investing: sourcing, conviction-building, portfolio construction, and founder support. More integrated CVC teams may involve more corporate strategy, partnership work, internal stakeholder management, and commercial validation.

Neither model is inherently better. Candidates who want a pure investing track should study whether the team leads deals, takes board seats, has follow-on capital, and rewards financial performance. Candidates who want exposure to innovation strategy may prefer a team that works closely with product, corporate development, and business-unit executives.

Venture Capital Careers can help candidates research the market from two angles: browse open roles on the VC job board and use the companies directory to study firms, fund types, and investment platforms. If you are preparing application materials, the venture capital resume guide is a useful next step because CVC roles still reward evidence of sourcing judgment, market mapping, financial analysis, and founder empathy.

Frequently asked questions

Is corporate venture capital the same as venture capital?

No. Corporate venture capital is a type of venture capital, but the investor is backed by an operating company and usually has strategic goals alongside financial return. Traditional VC funds are primarily accountable to financial investors.

What is a corporate venture capital firm?

A corporate venture capital firm or unit is an investment arm backed by a larger company. It invests in startups that may create financial return, strategic insight, partnership opportunities, or future acquisition relevance for the parent company.

What are examples of corporate venture capital?

Examples include GV, Salesforce Ventures, Intel Capital, and many sector-specific CVC arms attached to healthcare, financial services, industrial, energy, and technology companies. The useful question is not only whether a CVC is famous, but whether its parent company can help the startup.

Why do startups take corporate venture capital?

Startups take CVC funding for capital, credibility, industry expertise, customer access, distribution, technical support, and potential commercial partnerships. The tradeoff is that founders must manage conflicts, expectations, information rights, and strategic dependency carefully.

Is corporate venture capital a good career path?

It can be, especially for candidates who want a mix of venture investing and corporate strategy. The role is best when the CVC team has a clear mandate, real decision authority, strong deal flow, and a parent company that can help portfolio companies without distorting investment judgment.