Redemption Rights in VC: Definition, Example, and Term Sheet Checklist

Learn what redemption rights mean in venture capital, how preferred stock redemption clauses work, and what founders and investors should check in a term sheet.

Redemption rights give preferred shareholders the right to require a company to repurchase their shares after a specified period or event. In venture capital, they usually appear in preferred-stock financing documents and function as a negotiated exit pressure valve: if the company has not gone public, sold, or otherwise created liquidity by a certain date, investors may be able to ask the company to redeem their preferred shares.

That does not mean a startup can always write a check on demand. Redemption rights sit inside corporate law, the company's charter, board duties, and the practical reality of whether the company has cash legally available. They are also different from the statutory right of redemption in foreclosure law, which lets a borrower reclaim real property by paying the required amount before or after a foreclosure sale in some states.

What are redemption rights?

In a startup financing, a redemption right is a preferred-stock term that lets specified investors require the company to buy back their preferred shares, usually at the original purchase price plus any declared or accrued dividends, after a negotiated waiting period.

The right normally lives in the certificate of incorporation or preferred-stock terms, not in a casual side conversation. The NVCA model legal documents are a common reference point for venture financing document structure, including the charter and investor-rights documents where these kinds of preferred-stock terms are negotiated.

The practical question is simple: if the company stays private too long, can the preferred investors force a liquidity event by making the company redeem their shares?

Redemption rights vs similar terms

Redemption rights are easy to confuse with other VC terms because they all affect investor downside protection. The distinction matters in a term sheet review.

| Term | What it does | When it matters |

|---|---|---|

| Redemption right | Lets preferred holders require the company to repurchase shares after a trigger date or event. | When investors want a contractual path to liquidity if the company remains private. |

| Liquidation preference | Sets payout priority when the company is sold, liquidated, or has another liquidation event. | When exit proceeds are distributed among preferred and common holders. |

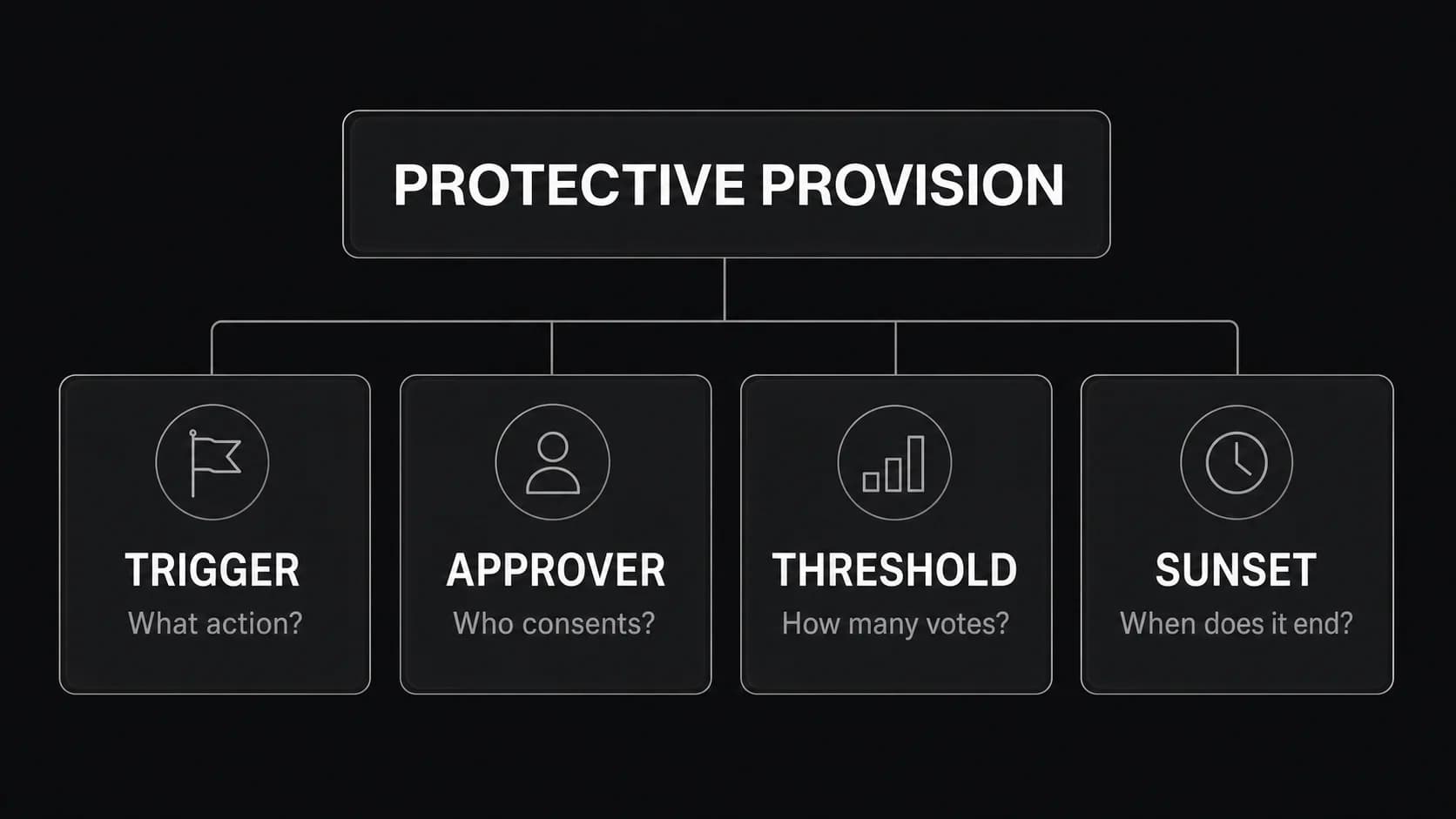

| Protective provisions | Give preferred holders approval rights over major company actions. | When the company wants to issue new securities, sell assets, change the charter, or take other protected actions. |

| Repurchase right | Often lets the company repurchase founder or employee shares, especially unvested shares. | When someone leaves the company or violates equity terms. |

| Share buyback | A company-initiated repurchase of shares. | When the board chooses to return capital or clean up ownership, subject to legal limits. |

| Statutory right of redemption | A real-estate/foreclosure concept, not a VC preferred-stock term. | When a borrower may reclaim foreclosed property by paying the required amount under state law. |

For the broader economic stack, read VCC's guides to liquidation preference, protective provisions, and anti-dilution provisions.

How a VC redemption clause works

A redemption clause is not one term. It is a bundle of mechanics. The most important pieces are:

| Clause element | What to check |

|---|---|

| Who can trigger it | A majority of preferred? A specific series? A major-investor threshold? All holders voting together? |

| When it starts | Often several years after the financing, not immediately after closing. |

| Redemption price | Original purchase price, accrued dividends, declared-but-unpaid dividends, a premium, or a formula. |

| Payment schedule | One lump sum or installments over several quarters or years. |

| Legal availability | Whether the company can lawfully redeem shares without impairing capital or violating creditor constraints. |

| Remedy if unpaid | Board rights, penalty dividends, voting changes, or simply a continuing obligation. |

| Interaction with other terms | Liquidation preference, conversion rights, dividends, debt covenants, and future financing terms. |

Delaware law is a common reference point because many startups are Delaware corporations. Under Delaware General Corporation Law Section 160, a corporation's ability to redeem or purchase its own shares is limited when capital is impaired or the redemption would cause impairment, and redeemable shares must be authorized consistently with the statute and certificate of incorporation. That is the legal backdrop, not a substitute for counsel.

The finance takeaway: a redemption right can look like a fixed investor exit on paper, but enforceability and timing depend on the company's legal capacity, cash position, and governing documents.

Example: Series A redemption right

Assume a startup raises a $6 million Series A. The preferred stock includes a redemption right exercisable after five years by holders of a majority of the Series A preferred.

| Input | Example |

|---|---|

| Series A investment | $6,000,000 |

| Redemption trigger | At least five years after closing |

| Holder threshold | Majority of Series A preferred |

| Redemption price | Original purchase price plus declared but unpaid dividends |

| Payment schedule | Three annual installments |

If the company has not exited after five years, the required holders could demand redemption. If the full $6 million is redeemable over three years, the company may owe roughly $2 million per year before dividends or other adjustments.

That obligation can become meaningful. A profitable later-stage company might handle it. A cash-burning startup may not have legally available funds or enough runway. A board may also need to weigh creditor obligations, fiduciary duties, and the effect on employees and common shareholders.

This is why redemption rights are often more useful as leverage than as a clean repayment path. They can force a conversation about liquidity, sale timing, recapitalization, or a new financing round, but they do not magically turn illiquid startup equity into cash.

Why investors ask for redemption rights

Venture funds have time horizons. A fund may need to return capital to limited partners even when a portfolio company is still private, growing slowly, or unwilling to sell. Redemption rights give investors a negotiated tool if the company becomes a long-duration private asset without a credible liquidity plan.

Investors may ask for redemption rights when:

- The company is later stage and has enough revenue or cash flow to make redemption plausible.

- The round is structured more like growth equity than early seed risk capital.

- Existing investors want pressure on the board to consider sale, dividend, recapitalization, or secondary options.

- The preferred stock has a negotiated package of downside protections, not just upside conversion rights.

They also fit the broader logic of preferred stock. VC investors commonly receive preferred shares rather than common stock because preferred stock can carry negotiated economic and governance rights. The broad preferred-vs-common distinction is that preferred stock can receive priority over common stock for dividends and liquidation distributions, while startup preferred-stock documents can add negotiated rights beyond that baseline.

Why founders push back

Founders usually resist strong redemption rights because a forced repurchase can drain cash at exactly the wrong time. The company may need capital for hiring, product, sales, or debt service. A redemption demand can also send a negative signal to new investors: existing preferred holders are asking for money out instead of backing the next stage.

Common founder concerns:

- Runway risk: cash used for redemption is cash not used to operate the business.

- Financing risk: new investors may treat redemption overhang as a senior claim on future cash.

- Control pressure: investors can use the threat of redemption to push for a sale or recapitalization.

- Common-stock impact: founders and employees usually sit behind preferred holders economically.

- Legal uncertainty: the company may not be able to redeem shares even if the contract says holders can request it.

The negotiation is not simply "redemption rights: yes or no." Founders can negotiate timing, thresholds, installment periods, remedies, and whether the right applies to one series or all preferred together.

What to check before accepting or modeling redemption rights

Use this checklist when reviewing a term sheet, charter, or financing model:

| Question | Why it matters |

|---|---|

| Who controls the redemption vote? | A single series may have leverage over the whole company. |

| How long is the waiting period? | A short fuse can create pressure before the company has a realistic exit path. |

| Is the price limited to original purchase price? | Premiums, dividends, and interest-like economics can make the obligation larger than expected. |

| Are payments installment-based? | Installments may reduce cash shock but extend overhang. |

| What happens if the company cannot legally pay? | The right may continue, trigger governance changes, or create negotiation leverage. |

| Does it rank ahead of other obligations? | Debt, vendor obligations, payroll, and legal capital rules matter. |

| Does it interact with conversion rights? | Investors may choose between common-stock upside and redemption pressure. |

| Does it affect future financing? | New investors will model the redemption claim when pricing the next round. |

For early-stage deals, redemption rights are often less central than SAFE, convertible note, pro rata, and liquidation-preference terms. For later-stage preferred rounds, they deserve real attention in the model.

Statutory right of redemption vs VC redemption rights

"Statutory right of redemption" is usually a foreclosure term. It refers to a borrower's legal right, in some states and circumstances, to reclaim property by paying the required amount before or after foreclosure. The general right of redemption concept covers that real-estate meaning.

That is not the same as a VC redemption right. A startup redemption right is contractual and corporate. It concerns shares, preferred-stock terms, and the company's ability to repurchase equity. A statutory foreclosure redemption right concerns real property and state foreclosure law.

If your search is about mortgages, foreclosure auctions, or post-sale redemption periods, you need a real-estate/legal source. If your search is about preferred stock, venture financing, or redeeming shares, this VC/corporate-finance meaning is the relevant one.

Where redemption rights show up in VC work

For candidates preparing for venture capital analyst or associate roles, redemption rights are not usually the first term tested in interviews. But they are a useful signal of whether someone can read beyond valuation and option pool headlines.

In real deal work, redemption rights can appear in:

- Term sheet comparison.

- Charter review.

- Late-stage preferred-stock financing.

- Downside-case return analysis.

- Exit-timing discussions.

- Recapitalization or pay-to-play negotiations.

If you are learning the VC financing stack, pair this article with VCC's guides to term sheets, pro rata rights, pay-to-play provisions, and venture capital career paths.

If you want to apply this kind of term-sheet fluency in a real investing role, browse open roles on the Venture Capital Careers job board.

FAQs

What is a redemption right?

A redemption right is a right to have shares, property, or another asset bought back under specified conditions. In venture capital, it usually means preferred shareholders can require the company to repurchase their preferred shares after a negotiated trigger date or event.

What are redemption rights in VC?

In VC, redemption rights are preferred-stock terms that can let investors ask the company to redeem their shares, often after several years without an IPO, sale, or other liquidity event. The clause usually defines who can trigger redemption, when it can be triggered, how the price is calculated, and how payments are made.

What is redemption of shares?

Redemption of shares means a company repurchases or retires shares according to the rights attached to those shares. In a startup, redemption usually refers to preferred stock being repurchased under a charter provision, subject to corporate-law and cash-availability limits.

Are redemption rights the same as liquidation preference?

No. A liquidation preference controls payout priority when the company is sold, liquidated, or has another covered liquidity event. A redemption right concerns whether investors can require the company to repurchase their shares after a trigger date or event.

What is statutory right of redemption?

Statutory right of redemption is usually a foreclosure concept. Depending on state law, it may let a borrower reclaim foreclosed property by paying the required amount within a specified period. It is separate from VC preferred-stock redemption rights.

Are redemption rights founder-friendly?

Strong redemption rights are usually investor-friendly because they create liquidity pressure on the company. Founders may accept a narrower version in later-stage rounds, but they should negotiate timing, holder thresholds, payment schedule, remedies, and interaction with future financing.

Do startups actually redeem preferred stock?

Sometimes, but it is not as simple as paying an invoice. The company must have legal capacity and available funds, and the board must consider broader obligations. In many cases, the right creates negotiating leverage rather than immediate cash redemption.