Form ADV: Definition, Parts, Filing Requirements, and How to Read It

Learn what Form ADV means, what Parts 1, 2, and 3 disclose, who files it, where to find it, and how VC candidates and fund operators should read it.

Form ADV is the uniform disclosure and registration filing used by investment advisers to register with the SEC and state securities authorities. In finance, ADV is commonly used as shorthand for "adviser" in the SEC's investment adviser filing system, not as a separate investment product. The filing tells regulators and the public how an adviser is organized, what services it offers, how it is paid, where conflicts may exist, and whether the firm or its people have reportable disciplinary history.

For Venture Capital Careers readers, Form ADV is useful for more than compliance trivia. It can help candidates research a venture firm, founders understand the adviser behind a fund, and emerging managers learn the vocabulary regulators use for adviser disclosures.

What is Form ADV?

Form ADV is officially the Uniform Application for Investment Adviser Registration and Report by Exempt Reporting Adviser. The SEC's Investor.gov Form ADV glossary explains that investment advisers use it to register with both the SEC and state securities authorities, and that public parts of the filing are available through the SEC's Investment Adviser Public Disclosure system.

Think of Form ADV as a structured disclosure file. It is not a pitch deck, fund memo, or performance report. It is closer to a regulatory profile: ownership, advisory business, client types, fees, conflicts, private fund reporting where applicable, and disciplinary disclosures.

That distinction matters. A venture firm may have a polished website and an impressive portfolio page, but Form ADV can show a different layer of information: legal name, adviser status, related entities, regulatory assets under management, private fund disclosures, and brochure language about fees and conflicts.

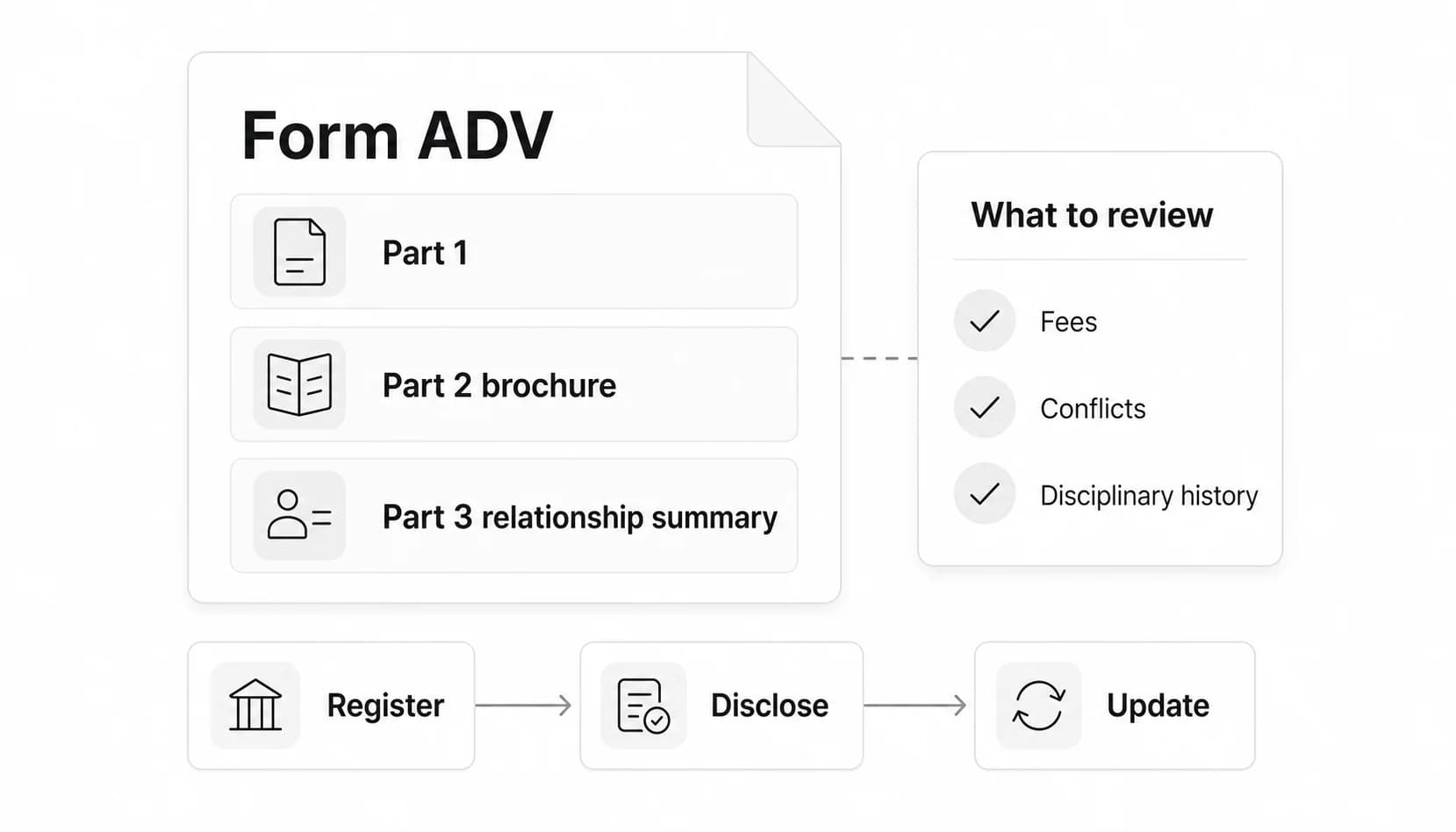

Form ADV parts at a glance

| Part | Also called | What it usually covers | Why it matters |

|---|---|---|---|

| Part 1 | Application / check-the-box filing | Business, ownership, clients, employees, affiliations, disciplinary events, private fund reporting schedules | Helps regulators and readers understand the adviser's structure and reported business facts |

| Part 2A | Brochure | Services, fees, methods of analysis, investment strategies, risks, conflicts, disciplinary information | The most readable long-form explanation of how the adviser describes its business |

| Part 2B | Brochure supplement | Information about supervised persons who provide advisory services | More relevant for client-facing advisers than for many venture-fund searches |

| Part 3 | Relationship summary / Form CRS | Short retail-investor summary of services, fees, conflicts, standard of conduct, disciplinary history, and questions to ask | Relevant when an SEC-registered adviser offers services to retail investors |

Official Form ADV filing instructions are the source of truth for filing details. For a reader, the practical move is simpler: use Part 1 for structured facts, Part 2A for plain-English business disclosure, and Part 3/Form CRS when the adviser serves retail investors.

Who files Form ADV and when is it updated?

Investment advisers that register with the SEC or state securities authorities file Form ADV. Some exempt reporting advisers also report on Form ADV. The exact registration or reporting obligation depends on the adviser's assets, clients, exemptions, state law, and business facts, so firms should treat this as a compliance question for counsel rather than a blog checklist.

At a high level, Form ADV is filed through IARD, the Investment Adviser Registration Depository. Advisers generally submit an annual updating amendment and must amend certain information sooner when it becomes materially inaccurate. The filing instructions use defined terms such as regulatory assets under management, advisory affiliate, and custody, which is why those phrases matter when you read the form.

For candidates and founders, the update cadence matters because an old brochure may not reflect a firm's current strategy, staff, or conflicts. Check the filing date, then compare it with the firm's website, fund announcements, and other public materials.

Form ADV glossary: key terms

| Term | Plain-English meaning | What it helps you answer |

|---|---|---|

| ADV | SEC shorthand tied to investment adviser registration and reporting | Is this a regulated adviser disclosure or just generic finance jargon? |

| IARD | The electronic filing system advisers use for Form ADV | Where does the filing come from? |

| IAPD | The public SEC adviser lookup site | Where can I search for a firm's public filing? |

| Registered investment adviser | An adviser registered with the SEC or state securities authorities | Is the firm presenting itself as a registered adviser? |

| Exempt reporting adviser | An adviser that may be exempt from full registration but still reports certain information | Why does a private-fund adviser have a shorter public record? |

| RAUM | Regulatory assets under management | How large is the advisory business for regulatory reporting purposes? |

| Part 2A brochure | Narrative disclosure document for clients | How does the firm describe services, fees, risks, and conflicts? |

| Part 2B brochure supplement | Disclosure about advisory personnel | Who provides advice and what is their background? |

| Form CRS / relationship summary | Short retail-client relationship summary | What should a retail investor know before engaging the adviser? |

| DRP | Disclosure Reporting Page | Is there reportable disciplinary or regulatory history? |

| Custody | Holding or having access to client assets under regulatory rules | Are there asset-control risks or special safeguards to understand? |

| Conflicts of interest | Situations where adviser incentives may diverge from client interests | How might the firm get paid or act in ways a client should evaluate? |

How to find and read a Form ADV filing

Use the SEC's Investment Adviser Public Disclosure site to search by firm name, CRD number, or SEC number. If a venture firm has a separate management company, search the legal adviser name as well as the brand name. Fund websites, Form D filings, and portfolio pages sometimes use different entity names.

Read in this order:

- Start with Part 1 for the legal name, office locations, ownership, client types, private fund schedules, RAUM, and disciplinary responses.

- Open Part 2A for the narrative brochure. Look for fees, conflicts, investment strategy, methods of analysis, risk language, and disciplinary history.

- Check whether Part 3/Form CRS exists. It is most relevant for retail-facing advisers, so its absence is not automatically a red flag for a private-fund adviser.

- Compare the filing date with current public claims. If the brochure is stale, look for newer amendments or corroborating public materials.

- Treat unusual or unclear disclosures as prompts for better questions, not automatic conclusions.

The official Form ADV form is long because it serves regulators, advisers, and the public at once. A reader does not need to master every schedule to get value from it. The main job is to identify the adviser's legal identity, conflicts, private-fund footprint, and any disclosure items that deserve follow-up.

What VC candidates, founders, and fund operators should review

For a VC candidate, Form ADV can sharpen firm research before an interview. Use it alongside venture capital firm profiles, the firm's website, and recent fund news. The filing can help you understand whether the platform is a registered adviser, how many private funds it reports, whether it discloses related businesses, and what language it uses around strategy and conflicts.

For a founder, Form ADV is not a substitute for referencing calls or legal review, but it can help identify the adviser behind a fund brand. That is useful when a firm has multiple funds, affiliates, or management entities.

For an LP or emerging manager, the filing gives a baseline vocabulary for diligence conversations: RAUM, custody, conflicts, disciplinary events, and private fund reporting. It also shows why a firm's compliance posture is part of its operating model, not a back-office afterthought.

For a career switcher, Form ADV is one more way to move beyond surface-level firm research. Pair it with the venture capital career path and venture capital due diligence guides so your outreach and interviews speak to how the firm actually operates.

What Form ADV does not tell you

Form ADV is a disclosure document, not a complete commercial assessment. It usually will not tell you whether a fund is performing well, whether a partner is helpful to founders, whether a team is hiring, or whether the firm's strategy is differentiated in practice.

It can also be easy to over-read structured responses. A disclosure item may be serious, technical, old, resolved, or tied to an affiliate. The right response is to read the relevant brochure language, check dates and entities, and ask informed follow-up questions when the relationship justifies it.

For broader context on how venture firms operate, start with the Venture Capital Careers overview of venture capital. Form ADV is one input in that picture: useful, public, and structured, but not the whole story.

Form ADV FAQ

What does ADV stand for in finance?

In this context, ADV refers to the SEC investment adviser registration and reporting form. The full official title is Uniform Application for Investment Adviser Registration and Report by Exempt Reporting Adviser.

Is Form ADV public?

Many Form ADV disclosures are public through IAPD. Public availability can vary by adviser type and filing component, but Part 1 and brochures are commonly available for registered advisers.

What is Form ADV Part 2A also known as?

Part 2A is commonly called the brochure. It is the narrative disclosure document that explains the adviser's services, fees, risks, conflicts, and disciplinary information in plain English.

Is Form CRS the same as Form ADV Part 3?

Form CRS is the relationship summary associated with Part 3 for certain SEC-registered advisers that offer services to retail investors. It is designed to be brief and easier to compare than the full brochure.

Do venture capital firms file Form ADV?

Some venture advisers register or report on Form ADV, and some may rely on exemptions or structures that affect what is publicly available. Search the adviser's legal name in IAPD and avoid assuming that the fund brand and adviser entity always match.